Everything is Technology

Trillions of Dollars of Venture Capital Addressable Value

Welcome to the 583 newly Not Boring people who have joined us since our last essay! Join 243,199 smart, curious folks by subscribing here:

Today’s Not Boring is brought to you by… Ramp

Today’s essay is all about the idea that technology companies will displace incumbents with products that are so much better than what existed before that the shift is inevitable. It’s hard to think of a better example than Ramp.

Ramp is more than a corporate card (although it makes a great one). The card is the portal into a full suite of products designed to help your business grow intelligently and help you save time.

With Ramp, your finance team has the best engineers in fintech working on your behalf to make sure that you get the control and visibility they need, without the busywork.

Ramp is one of my favorite companies in the world. It’s the only company I’ve written about four times, invested in three times, and now, the only company I’ve done a commercial with.

Ramp is so much better than the alternatives that I bet your team will eventually run on Ramp. Just start now, and start compounding the benefits of working with a company that makes your company run better. Reply to this email to let me know when you switch.

Upgrade your team to Ramp: The Official Business Card of Not Boring.

Hi friends 👋 ,

Happy Tuesday! If you’ve been reading Not Boring for a while, you know that I think the most important shift happening in business is that modern technology companies are displacing sclerotic incumbents.

I keep yelling the idea as loudly as I can, but I don’t think it’s quite sunk in. If it had, people would, for example, understand why VC megafunds actually make a lot of sense. I believe that tens of trillions of dollars of value is being created as we speak.

Here’s a quick TL;DR:

The world changes faster than we expect, and the resulting outcomes are bigger than we expect.

There are two ways tech eats the world:

Direct displacement (e.g. Tesla vs legacy autos)

Market aggregation/creation (e.g. Uber vs taxis)

$1B exits are now ~85th percentile, not 99th. $1B outcomes shouldn’t be expected to return funds, and VC megafunds aren’t dumb.

Asset managers who saw regime shifts early (Blackstone, Vanguard, etc.) scaled to $1T+. Megafunds are doing the same.

A wave of $1B+ exits and $5B+ raises in 2025 is the appetizer. The next 20 years will see trillions in VC Addressable Value emerge.

Everything is technology.

This is my most succinct attempt to make the case to date, using numbers and a little history.

Let’s get to it.

Everything is Technology

The world can flip more quickly than you expect. Things we take for granted today can disappear in a decade, replaced by things we didn’t even know we wanted.

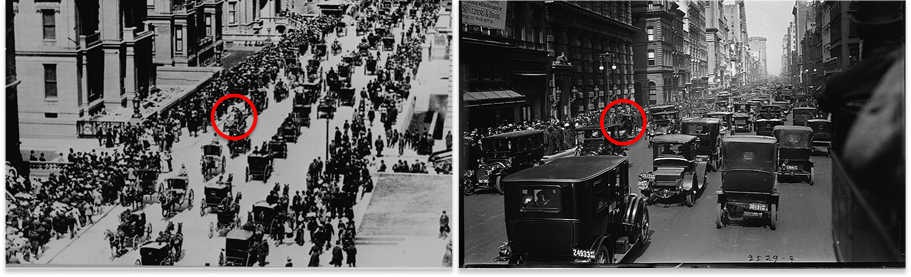

There’s this famous pair of images, both taken of the Easter Parade on New York City’s Fifth Avenue, one in 1900, the other in 1913.

The one on the left shows a street roughly the way it may have looked for millennia: full of horse drawn carriages, with just one motor-car (circled in red). The one on the right shows the same street on the same day thirteen years later, full of motor-cars, with just one horse-drawn carriage (circled in red).

Ford introduced the Model T in 1908. If he’d asked customers what they wanted, he quipped, they would have asked for faster horses. Just five years later, the deequinization of New York City was practically complete. The Model T was both faster and cheaper than horses, and it didn’t shit all over the street.

By 1919, a Census year, the Census showed that all 2,544 establishments across the entire Carriages and Wagons and Materials industry generated $118.2 million in “Value of products.” That same year, Ford sold over 900,000 Model T’s at $360 a pop, for $324 million, or more than twice the total product value of the industry it had displaced.

Technology had won the day.

Over time, if a new technology is successful enough, it stops being lumped in with “technology” and earns its very own industry. In the internal combustion engine’s (ICE) case, that was the automotive industry.

After an initial period of experimentation, the “Big Three” – Ford, GM, and Chrysler – came to dominate America’s automotive industry.

In 2020’s The Beginning of the End, Ben Thompson wrote that by the 1920’s, aside from a brief challenge from AMC, “The ‘Big Three’ mostly had the market to themselves, at least until imports started showing up in the 1970s.”

The imports did show up in the 70s, and the automotive industry became global. By the end of 2003, the world’s twelve largest automakers sported a combined market cap of ~$450 billion.

Because these were automotive companies, and relatively old ones at that, that $450 billion was not considered tech market cap. It was not VC Addressable Value (VCAV), defined as something like the total value of the companies VCs can invest in.

If Elon Musk had asked customers what they’d wanted in 2003, they probably would have told him “faster ICE SUVs.” Like Henry Ford, Elon did not ask customers. He made electric vehicles (EVs).

Today, Tesla alone is worth nearly $1 trillion, more than twice what all of the big automakers were worth, combined, when it entered the market.

Technology wins again.

This time, it both pulled that value back into tech market cap and VCAV, and grew it. While most of the gains have come in the public markets – Tesla IPO’d with a market cap of ~$1.5 billion and grew to $2.2 billion on the first day of trading – the other company Elon started around that time, SpaceX, is still private, and is valued at $350 billion. VCAV is a loose metric that doesn’t care for details like who went public when.

Two Ways to Eat the World

One of Not Boring’s core theses, maybe the core thesis, is that everything is technology.

I’ve made this argument before, in various ways1. I will make it again. I don’t think people have fully grokked it, and I think it is the most important thing to understand if you’re building or investing in technology companies.

It explains, for example, why VC megafunds aren’t simply greedy fee-grabs, as the general sentiment seems to agree they are.

So I’m going to try to lay out the argument as clearly as possible. Here’s the simple version:

The addressable market for venture-backed tech companies will grow by at least an order of magnitude as they battle incumbents in industries not traditionally considered tech, and as they turn previously fragmented and unaddressable markets into addressable markets.

In other words, software alone is not eating the world, technology – software, hardware, bio (for simplicity’s sake, pretty much anything that a VC can invest in) – is eating the world, and it’s doing so in two main ways: by eating someone else’s lunch or cooking up its own.

Tesla is an example of the former, of eating the automotive industry’s lunch. Using technology to build a better product (and to promise future products like robots and self-driving taxis using its core technology), it’s grown to be larger than the entire automotive industry was by market cap the year it was founded.

Ford is an example of the latter, of turning a fragmented horse and carriage market into a unified addressable market. By using a new technology (ICE) and assembly line manufacturing, it created a new company that filled an existing need better, and at greater volume, than that entire industry could.

Sticking with cars, a modern example of cooking up its own, of turning previously fragmented and unaddressable markets into addressable markets is Uber.

In a now-famous 2014 blog post, How to Miss By a Mile: An Alternative Look at Uber’s Potential Market Size, Benchmark’s Bill Gurley tore apart NYU Stern professor and valuation-modeling superstar Aswath Damodaran’s analysis of Uber. The company had recently been valued at $17 billion. Damodaran reasoned that Uber was only worth $5.9 billion, based on two assumptions: the historical TAM of the “global taxi and car-service market” is something like $100 billion, and that Uber would, at most, capture 10% of that market. Gurley thought that both were terrible assumptions.

The real TAM, he argued, was something like a piece of the $6 trillion annual car ownership cost market – that piece plus the expanded car-for-hire market was something like $450B - $1.35T.

And by offering a much better product, and one that got better as it got bigger, Uber could capture much more than 10% of the market.

Long story short: Uber is worth $175 billion today, 75% larger than Damodaran’s entire TAM. And whereas VCs didn’t invest in taxis or cars-for-hire, they did invest in Uber. That’s around $0.2 trillion in VCAV out of thin air. We could do something similar with Airbnb and hotels/short-term-rentals, but you get the point.

As we’ve discussed at length, it’s not just software that is eating the world, but technology in general. Joseph Schumpeter wrote that “Constant, relentless change is the hallmark of capitalism.” My contention is that as this capitalist churn happens, technology companies will replace non-technology companies.

Sense-check this. Assume that churn continues; new companies replace old. Can you imagine new companies not built with modern technology being the replacers?

There are two ways technology companies eat old industries:

Direct Displacement (eating someone else’s lunch): Competing directly in large existing addressable markets with a better, cheaper, faster product, a la Tesla.

Market Creation and Aggregation(cooking up its own): Creating new addressable markets out of previously fragmented ones with a better, cheaper, faster technology product in place of an analog one, a la Ford and Uber.

History is chock full of examples of both, even if the once new technology companies don’t seem like technology companies today. I gave ChatGPT’s Deep Research the framework and asked for examples of each type. Here’s the report, with case studies, and here’s a table summarizing them:

Technology companies frequently eat incumbents and create new industries. These transitions happen more quickly than you would expect, typically within a decade or two (and the two most recent, at something like the modern speed of change, took only six and eight years). And the new companies created on the backs of new technologies typically end up being larger than the entire industry they replace.

Maybe this time it’s different.

In Defense of Megafunds

I am writing a different version of the same argument I’ve been trying to make for a few years once again because it feels like it’s still not sinking in for most people, even those in VC.

What set my fingers flying on this specific instantiation is the recent (ongoing, but louder recently?) conversation about venture fund math. Specifically, two questions: whether a $1 billion outcome can even return a fund anymore and whether the multi-billion dollar megafunds are just doing it for the fees.

This feels like inside baseball, and megafunds certainly don’t need me to defend them, but it’s hard to find something that better illustrates the delta between where I think the world is heading and where a lot of people in venture think the world is heading than this debate, so bear with me.

A few weeks ago, Harry Stebbings tagged me in a tweet discussing whether a $1 billion outcome can even return the fund for seed managers anymore. It came from his conversation with SaaS investor Jason Lemkin, who observed that the old rule of thumb that a $1 billion outcome should return your fund probably doesn’t work anymore. Most of the discussion in the replies centered around fund size and ownership, and decided that it was really hard to return a seed fund with a $1 billion outcome.

My reply focused on the $1 billion: that’s just not that big an outcome anymore.

$1 billion is a round number. But that doesn’t make it meaningful. What matters in venture, what has always mattered in venture, is backing the top x% of companies, the ones that drive the power law. And $1 billion outcomes are just less extraordinary than they used to be.

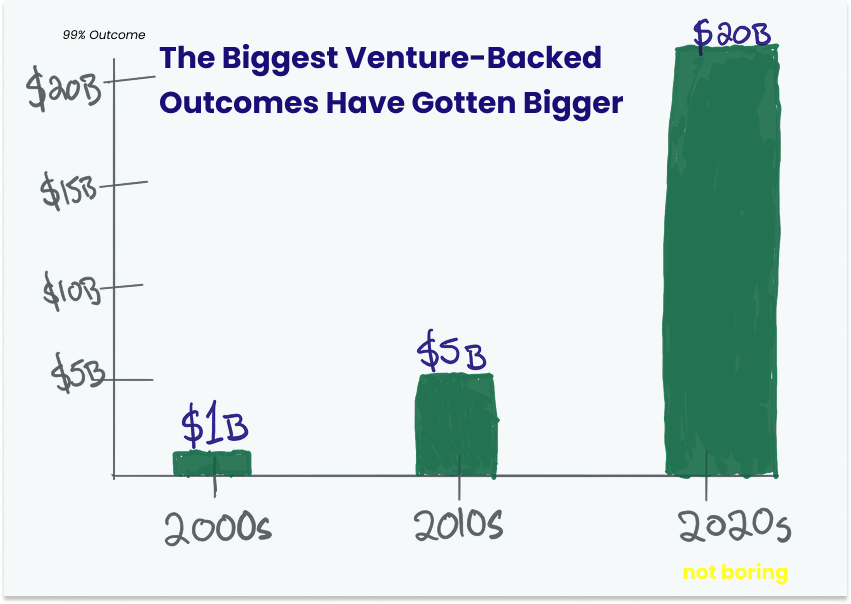

In the early 2000s, a $1 billion outcome was a 99th percentile outcome. By the 2010s, it was a 90th percentile outcome. Today, it’s roughly an 85th percentile outcome.

Put another way, a 99th percentile outcome in the early 2000s was $1 billion. By the 2010s, it was $5 billion. Today, it’s roughly $20 billion.

These are rough numbers that I pulled using Deep Research on Pitchbook and Crunchbase data, so grain of salt (another Deep Research run says that 99th percentile in the 2010s was $3B and in the 2020s was $8B), and they don’t include the impact of crypto tokens, which would bring the numbers up. But they’re good enough to make the point: VCs don’t get paid for 85th percentile outcomes.

There is a similar logic at play when people talk about how the megafunds are becoming too mega to generate returns.

Recently, for example, people called out that Greenoaks’ seed investment in Windsurf, while incredibly impressive at a return north of 100x if the rumors of OpenAI’s $3 billion acquisition are true, wouldn’t even come close to returning the fund. If you haven’t read Jeremy Stern’s excellent profile of Greenoaks’ Neil Mehta (first, what are you doing? bookmark it and read it as soon as you’re done reading this), one takeaway is that Neil Mehta is very smart and is not in this to generate management fees. According to the profile, he’s Greenoaks’ largest LP, personally.

Thrive launched Thrive Holdings in addition to its recent $5 billion venture Fund IX. Founders Fund raised $4.6 billion for a late stage fund. a16z is rumored to be raising $20 billion. The list goes on, and the commentary that goes along with it goes something like: good luck generating meaningful multiples on all that money!

In a great interview with Jack Altman, First Round’s Josh Koppelman, who has kept his funds relatively small and generated excellent returns by doing so, talked about what he calls the Venture Arrogance Score: how much of the total value created by startups does your fund need to capture to 3 or 4x the fund? For a $7 billion fund, that’s something like half of the past decade’s average annual startup value created, when no fund has consistently captured more than 10%.

Josh’s argument is harder to dismiss than the “$1 billion should return a fund!” argument, because if you look backwards, the math doesn’t seem to math. It requires a dangerous leap of faith, the belief that “this time will be different.”

Actually, though, arguing either side requires making that argument.

If you believe that megafunds will generate 3-4x returns, you need to argue that the value of venture outcomes will be much larger in the next decade than it was in the past.

If you believe that megafunds won’t generate 3-4x returns, you need to argue that the VCs that have been among the best at predicting the future over the past decade no longer are, or that they’re just good at seeing the future for the companies they back but not the industry they work in, or that they’re just milking that past success to generate fees. All of them, all at once.

AND you need to argue that the thing that’s been happening for centuries, where new technology companies displace, create, and outgrow existing industries will not happen anymore, at a time when the number and power of new technologies that entrepreneurs have at their disposal is higher than ever before.

You might be thinking, “Yeah, but those were horse-and-buggies. We’re talking about giant, modern conglomerates in defense, energy, and aerospace. We’re talking about government-funded education. We’re talking about Too Big to Fail financial institutions.” To which I will remind you that at the time, horses and buggies seemed so permanent that customers could only imagine faster ones.

I, perhaps unsurprisingly at this point in the essay, am on the side of the megafunds. I think they understand that everything is technology, and are the first to position themselves accordingly. My bet is that the current vintage of eye-poppingly large funds will seem quaint in a few years, as everything becomes technology.

How Asset Managers Grow

This isn’t a piece about megafunds, but something hit me while writing this that I want to share: what megafunds are doing today mirrors what Vanguard, Blackstone, BlackRock, and Brookfield did in earlier capital regime shifts: seeing something early, building relevant muscle, and flexing that muscle across vehicles and larger AUMs.

Just as companies like Ford, Tesla, and Uber rode new technology waves to become bigger than the incumbents in the industries that they displaced or aggregated, asset managers have ridden their own shifts to accumulate trillion dollar AUMs.

I’m going to oversimplify here, but:

Vanguard launched in 1975, right after “May Day” deregulated brokerage commissions and ERISA (Employee Retirement Income Security Act) spawned defined-contribution plans, Vanguard used its mutual-ownership, ultra-low-fee indexing model to satisfy sponsors’ demand for cheap market exposure. It turned its core strength in cost-discipline into ETFs, target-date funds, and global asset-allocation products as fee sensitivity intensified. Today, it manages $9.3 trillion.

Blackstone, founded in 1985 just as ERISA clarifications opened the door for U.S. pensions to back private-equity partnerships, used its deal-structuring and leverage expertise to deliver outsized returns in corporate buyouts. Beginning with its 1991–92 real-estate vehicles and accelerating in the early-2000s low-rate, yield-starved environment, it redeployed the same underwriting muscle and LP network into real estate, credit, secondaries, and other alternative asset classes. Today, it manages $1 trillion.

BlackRock, founded in 1988 amid the post-S&L-crisis appetite for sophisticated fixed-income risk management, leveraged its Aladdin analytics engine to give institutions transparency and low-cost beta. Then, just as the post-2008, yield-scarce world embraced passive investing, scaled that same quant platform into ETFs, multi-asset mandates, and eventually alternatives. Today, it manages $11.6 trillion.

Brookfield was reborn in the late 1990s from the Brascan conglomerate just as governments worldwide were privatizing power, property, and infrastructure. The real estate investor applied its operator expertise in long-duration hard assets to offer pensions inflation-protected yield, then recycled the same playbook across global real estate, renewables, infrastructure, credit, and insurance platforms. Today, it manages $900 billion.

Each firm spotted a big shift early, built a differentiated edge around the shift, and parlayed that edge (and LP relationships) into adjacent vehicles to compound into a multi-strategy, trillion-dollar-scale asset manager.

If the current shift is “everything is technology,” then it makes sense that funds are sizing up and expanding out.

If you believe that some of the companies being built today will be larger than the incumbents they displace (i.e. Anduril in defense), and if you believe that others will create markets that were previously unaddressable (i.e. OpenAI in knowledge work), and if you see that they are staying private longer (and enable them to stay private longer through fresh funding and tender offers), then it makes perfect sense to raise larger core funds.

If you believe that tools like AI will bring economies of scale and even light network effects to large, previously fragmented industries like accounting, then this line from the April 29, 2025 DealBook article on Thrive Holdings – “Now the venture capital firm is taking a different approach: creating and buying companies that it believes can benefit from A.I. – including in industries that seem far more humdrum, such as accounting – and holding on to them for a long time.” – makes perfect sense.

It also makes perfect sense, as the article points out, that firms like General Catalyst and 8VC are investing in AI-powered roll-ups. If access to a lower cost of capital was the prime advantage in the early days of private equity, then the firms that could access a lower cost of capital had a structural advantage. If AI is an even bigger lever on returns, then the firms that have expertise in AI (and relationships with companies like OpenAI) have a structural advantage.

I suspect that we’ll see megafunds expand into more new product offerings beyond traditional early stage and growth venture capital as technology eats the world, and as VCAV expands.

The bet is: everything is technology, and that technology people can get finance (perhaps with the help of AI), before finance people can get technology.

Everything is Technology

But remember, this isn’t a piece about megafunds.

It’s just that these particular investors have historically been very good at predicting the future, and because of that, they have access to the very best companies, who can show them a little more clearly where the future is going to go from here, and I guess my point is that what if we assume they’re not greedy idiots and instead notice the moves that all of them seem to be making at the same time?

Remember, the thesis is that every industry currently dominated by large, sclerotic incumbents will come to be dominated by tech companies (typically Vertical Integrators). Studying historical examples of similar transitions, we see that these transitions can happen surprisingly fast (within a decade or two) and that the new companies become larger than the incumbents they replace, often larger than the entire industry. TAM expands when you offer customers a cheaper, better, faster product, and valuations expand when you do so at higher margins and faster growth.

There’s a key difference, though. The previous transitions we discussed and listed in the displacer/creator table were financed in a hodgepodge of ways. The Liverpool-Manchester Railway was essentially a public-private partnership. JP Morgan funded Thomas Edison; George Westinghouse bootstrapped, brought in some outside capital, and used profits from his airbrake business to power his electric business. Richard Sears bootstrapped before bringing in capital from Julius Rosenwald. Henry Ford raised $28k from a small syndicate, including the Dodge brothers, and got profitable fast. Malcolm McLean largely funded his Sea-Land shipping business with profits from his trucking business. Boeing used government contracts and retained earnings to fund the development of the 707.

While those businesses were built on the modern technology of the day, they were not VCAV, because there was no VC. For a quick check on how much value was created, I asked ChatGPT what these displacers and aggregators would be worth if they had been founded and met similar success today.

That’s a total of $15.7 trillion, nearly 10x more value than VC-backed exits created over the past decade. It is obviously illustrative and inaccurate, and plus, these companies were built and went public across many decades.

But the point I’m trying to make is that I think we’re going to see something similar (but bigger) happen on a compressed timeline over the next two decades, and this time, all of the winners will be backed by venture capitalists. All of the value will be VCAV.

Billion-dollar exits are still big wins, but a unicorn isn’t what it used to be. In the past week or so alone, Coinbase acquired Deribit for $2.9 billion, OpenAI acquired Windsurf for $3 billion, and DoorDash acquired Deliveroo for $3.9 billion and SevenRooms for $1.2 billion. Those follow Google’s $32 billion acquisition of Wiz, SoftBank’s $6.5 billion acquisition of Ampere Computing, Ser Eli Lilly’s $2.5 billion acquisition of Scorpion Therapeutics, Kraken’s $1.5 billion acquisition of NinjaTrader, CoreWeave’s $1.7 billion acquisition of Weights & Biases, PepsiCo’s $1.65 billion acquisition of Poppi, and Ripple’s acquisition of Hidden Road for $1.25 billion. We may get the Figma IPO (and others) soon.

The private markets have been hot in 2025, too, with 67 venture rounds valuing companies at $2 billion or more thus far in 2025. Those companies have a combined valuation of $743 billion, although much of that comes from OpenAI’s $300 billion valuation.

I am sure this list is missing a bunch. Follow Arfur Rock to see deals announced in real-time.

$1B+ exits and $5B+ valuations have become relatively frequent occurrences, and I think they’re appetizers.

There are startups operating today, or soon to be built, that will come to displace incumbents in energy, healthcare, defense, manufacturing, education, housing, finance, and aerospace, and create addressable markets out of fragmented industries like accounting, law, consulting, and labor more broadly. Coinbase joined the S&P 500 yesterday. I’ve written about many of the companies that I think will lead the charge, and will continue to.

If you believe that, you must believe that there will be tens of trillions of dollars of value both transferred from incumbents and created, all of it VC-addressable (even if it means VCs expanding what they can address).

If you don’t believe that, then what are we even doing here?

There is a ton of value currently locked in private markets. One way to view this is that many of the unicorns are actually zombiecorns, companies who raised at high valuations that they’ll never grow into in the froth of 2021. But I just shared a list of fresh $5B valuations with you. Another is that these are just paper marks - you can’t eat DPI! - and that these companies need to get acquired or go public to unlock value and get the wheels spinning. Maybe! I certainly hope so.

But I think another reason VC megafunds make sense is that these companies, companies like Stripe and SpaceX, are staying private longer and compounding in the private markets. Whether this is good for the general public or not (and if you think not, if you would like to invest in these companies, Coatue now has a fund to sell you) is another story, but if you believe that everything is technology, and if I’ve made you start to believe that these companies are going to get bigger than any we’ve seen before, it’s certainly good for the megafunds.

They can continue to buy ownership in companies that they believe will be bigger and more valuable than most people realize, and continue to offer them new financing products. Secondaries are an obvious and commonly used product. I like Brett Bivens’ and William Godfrey’s concept of Production Capital, a mix of venture and credit that provides the most efficient financing as CapEx-heavy companies grow.

Whatever the financing mechanism, historical case studies, modern technological capabilities, and some of the smartest capital allocators in venture are all saying the same thing:

Everything is technology.

Who am I to disagree?

Thanks to ChatGPT and Claude for research and editing help.

That’s all for today. We’ll be back in your inbox Friday with the Weekly Dose.

Thanks for reading,

Packy

I wrote Tech is Going to Get Much Bigger, The Techno-Industrial Revolution, Better Tools, Bigger Companies, and the Vertical Integrators Series (Parts I, II, III, IV, V), not to mention Deep Dives on specific companies that illustrate the general thesis, like Base Power Company (Chapter I & Chapter II), Meter, Astro Mechanica, Cuby, Earth AI, Primer (Deeper Dive), Fuse, Anduril, Varda, Wander, and many more. My last essay, Chaos is a Ladder, argues that market turbulence accelerates the transition from incumbents to startups.

Kho Sim is your assurance of an experience defined by alluring charm and absolute discretion. Seek individuals who are exceptionally bright, engaging, and devoted to ensuring your time together is memorable and flawlessly tailored to your deepest desires. https://khosim.com/

A pure black screen is great for testing brightness/contrast—an online screen testing tool saves me time every week. https://blackscreen.space