Welcome to the 784 newly Not Boring people who have joined us since our last essay! Join 242,616 smart, curious folks by subscribing here:

Hi friends 👋 ,

Happy Tuesday!

There’s that famous Warren Buffett quote, “Be greedy when others are fearful, and fearful when others are greedy.” I’m working on being fearful when others are greedy, but I thrive on being greedy when others are fearful.

The economy is chaotic right now. Tariffs, trade wars, and uncertainty rule the day.

For the companies that we talk about here at Not Boring, for the very best startups, this is the opportunity of a generation. This is when orders change, when new Techno-Economic Paradigms are born. This is when plucky startups start to become industry leaders.

I turned to ancient myths, underappreciated academic frameworks, case studies, and Game of Thrones to explain why chaos is a ladder. It’s as much fun as I’ve had writing a piece in a while, seeing so many weird and disparate ideas click into place.

If you want to read the whole thing online, you can do that here. And if you learn something useful, if you come out of this more excited about the future, please share it and help spread the word.

The word is this: you can’t control chaos, but you can play with it.

By automating up to 90% of the work needed for SOC 2, ISO 27001, and more, Vanta gets you compliant fast. Vanta opens the door to growth.

It works. Over 9,000 companies like Atlassian, Factory, and Chili Piper streamline compliance with Vanta’s automation and trusted network of security experts. Whether you’re closing your first deal or gearing up for growth, Vanta makes compliance easy.

The gods of industry have spent decades attempting to insulate themselves from risk, constructing globe-spanning architectures to maximize efficiency. But life is risk, and what you don’t pay for today, you will pay for tomorrow.

Now, chaos is at our door. It will be painful for everyone. But it will be more painful for those whose grooves are most deeply entrenched. Which means they’re an opportunity for those who would seek to topple them.

There is no Creative Destruction without destruction.

Shall we do a little Norse mythology?

In Norse mythology, Loki is the trickster god. He is of the enemy Jötunn race of giants by birth, but becomes blood brothers with Odin and is accepted among the Æsir, the principal gods. As the trickster, he plays a role familiar in mythology everywhere: he brings both chaos and innovation.

So one day, Baldr, “the Pure One of the Norse pantheon”, “so fair of face and bright that a splendour radiates from him,”1 begins to have nightmares indicating that harm will come to him. He shares his dreams with his mother, Frigg, who sets off across heaven and earth to extract oaths from everyone and everything – “from men and beasts, from fire and water, from metals and stones—not to harm Baldr.” Oaths sworn, Baldr protected, the Æsir amuse themselves by throwing things at him, only to watch them drop “before they touch his shining body.”

“All this annoys Loki, who disguises himself as a woman and quizzes Frigg as to the details of her oath-taking. In this way, he discovers that she has, in fact, omitted one item. ‘West of Valhalla,’ she says, ‘grows a little bush called a mistletoe. I did not exact an oath from it; I thought it too young.’”

If you have read any mythology whatsoever, you can guess what happens next. Loki fashions a dart from mistletoe wood and approaches one of the gods, Hod, who stands off to the side, not throwing anything at Baldr. “Why are you not honoring Baldr as the others are,” Loki asks the blind god. He gives Hod the mistletoe dart and guides his hand. “The dart goes straight through Baldr and he falls dead to the ground.”

Loki Tricks Hod into Killing Baldr with Mistletoe

The distraught gods try to bring Baldr back from the underworld and fail. They capture Loki and bind him “beneath the earth with cords made from the guts of one of his own children.” They hang a snake above Loki to drip venom on him for all eternity, and allow his wife to hold a dish to catch the poison, but she has to leave to empty the dish from time to time, at which points the venom drips on Loki’s face and cause him anguish. He writhes in pain. “The periodic writhings of Loki beneath the earth is what we now call earthquakes.”

While none of the Norse literature, according to Lewis Hyde, “says that what happens next in the sequence happens because Loki has been bound, the sequence of events is always the same and so the cause and effect is implied. The gods’ binding of Loki is always followed by the prophecy of Ragnarök, the doom of the gods.”

It begins with Fimbulwinter, three successive winters without summer. “Brothers will kill one another for greed; one wolf will swallow the sun, another the moon. The stars will vanish. All fetters and bonds will be snapped, including the cords that hold Loki to his stone.”

Unbound, Loki will lead an assault on the gods from a ship made from the unclipped fingernails of the dead. Fenrir the Wolf, Loki’s son, escapes his chains and devours Odin. Jörmungandr, the World Serpent, another of Loki's children, rises from the ocean and battles Thor; Thor kills Jörmungandr, but dies from his venom. The fire giant Surtr leads the forces of Muspelheim against the gods; Sutr kills Freyr. For his part, Loki battles the watchman Heimdall, and both die. “Fire will consume the heavens and the earth, and mortals and immortals alike will perish.”

"Ragnarök", Johannes Gehrts (1908)

“The prophecy, however, does not end there,” Hyde writes. “For the world is born again, refreshed, from this apocalypse.”

I want to share with you some of Hyde’s interpretation, from his excellent Trickster Makes This World, because the Norse anticipated Joseph Schumpeter’s Creative Destruction by more than a millennium and a half, and provide it with ancient, unshakeable underpinnings.

“To my mind,” (Hyde’s), “the whole sequence that moves from Baldr’s baleful nightmares to the Norse apocalypse hinges on the moment when Frigg decides to make the world safe for her son.”

“How much control can we have before the good life we’re guarding ceases to be good in any conventional sense?”

“Can we reduce contingency to zero, or must we always have some exposure to things we cannot control?”

“Is the life that has no risk a human life?”

The classicist Martha Nussbaum argues that, according to the Greeks, the good life must periodically occupy “the razor’s edge of luck.”

According to Hyde, the makers of the Norse myth agree. “In this story, we do not get the green world, growing even as it perishes, fruitful even in decay, without the paired forces of order and disorder. There must be right relationship between the two. The Norse gods are reginn, ‘organizing powers,’ and by themselves cannot bring that world to life; they need the touch of disorder and vulnerability that Loki brings, a point we see in its reverse: when Loki is suppressed, the world collapses; when he—and disorder—returns, the world is reborn.”

Líf and Lífþrasir, Louis Moe

Hyde ends this particular chapter with an analysis so germane that I will include it in full:

For [Georges] Duzémil, Baldr embodies the will whose energy is spent, the sovereign whose death is near. He’s the irremediable mediocrity of the present age, and must be killed if there is to be any change for the better.

Frigg’s attempt to guard her son stands in the way of this necessary end, which is therefore more destructive than it needed to be. Just as violent upheavals increase when no political process allows for change, so here the sneakiness and shock of Loki’s deed is proportional to Frigg’s exaggerated attempt at control. Moreover, the witless gods learn nothing from that violence, for they immediately increase the stakes, binding Loki and, as the inexorable logic plays itself out, bringing their whole world to its apocalyptic end. There is no way to suppress change, the story says, not even in heaven; there is only a choice between a way of living that allows constant, if gradual, alterations and a way of living that combines great control and cataclysmic upheavals.

Those who panic and bind the trickster choose the latter path. It would be better to learn to play with him, better especially to develop styles (cultural, spiritual, artistic) that allow some commerce with accident, and some acceptance of the changes contingency will always engender.

The irremediable mediocrity of the present age must be killed if there is to be any change for the better.

The Norse submit that chaos is inevitable.

Littlefinger adds color: “Chaos isn’t a pit. Chaos is a ladder.”

A ladder represents potential for those who stand at the bottom. A ladder represents danger for those who stand at the top.

It is a rough time to be raising a venture fund.

Pitchbook recently released Q1 fundraising data, which showed that VC firms are on pace to raise less money than they have in any year this decade, and that the money that is raised is going to fewer funds.

There are many good reasons for LPs (limited partners, the people and institutions who invest in funds) to be avoiding venture right now. Most of them boil down to one thing: liquidity.

LPs need returns to fund their university’s research if the government won’t. They can easily sell stocks and bonds at their market value; they can’t sell VC stakes as easily. And VCs have not been returning much capital to their LPs. According to Carta, more than 60% of 2019 VC funds have returned zero cash to LPs. Which means that LPs have less money when they need more money, generally, and have less money to invest in VC, where their money sits tied up, specifically.

Venture funding is a leading indicator. Right now, les bon temps are rouling. AI companies are raising mouth-watering sums at eye-watering valuations. But the data suggests, like much of the economic data suggests, that bad times are ahead. If the trend holds, there will be less money available to invest in startups just when their opportunity is greatest. Just when the old gods fall.

Acknowledging that as an emerging manager myself who would like to raise money I am self-interested here, it is hard to imagine a better setup for venture capital. Specifically, and again with the same caveat, for venture capitalists investing in Vertical Integrators.

This is what this essay is about. Don’t let the trickster talk fool you. It’s about why now, in the chaos, is when startups win.

Startups play with the trickster. Startups are the trickster.

Elsewhere in his analysis of the trickster, Hyde observes that the trickster, specifically Coyote, “seems to have no way, no nature, no knowledge.”

“What conceivable advantage,” he asks, “might lie in a way of being that has no way?”

He answers:

“A first answer might be that whoever has no way but is a successful imitator will have, in the end, a repertoire of ways.”

“Perhaps having no way also means that a creature can adapt itself to a changing world. Species well situated in a natural habitat are always at risk if that habitat changes. One reason native observers may have chosen the coyote the animal to be Coyote the Trickster is that the former in fact does exhibit a great plasticity of behavior and is, therefore, a consummate survivor in a shifting world.”

“So we have a second reason why it might be useful to have no way, no nature, no fixed instinctual responses. Having no way, trickster can have many ways. Having no way, he is dependent on others whose manner he exploits, but he is not confined to their manner and therefore in another sense he is more independent. Having no way, he is free of the trap of instinct, both ‘stupider than the animals’ and more versatile than any.”

Do you see where I’m going with this?

April Fool’s Day came a day late this year. We called it Liberation Day.

A month later, we’re still figuring out what’s actually happening. Tariffs on most countries were paused within days. Tariffs on China went up as high as 145% before President Trump admitted that they’d be a lot lower, that he wouldn’t play hardball. There are reportedly trade deals in the works with allies like Japan and Vietnam, although thus far, they remain as mythical as Loki and Coyote.

The point is not the specifics. They will emerge over time. The point is chaos.

The Economist

And chaos is a ladder.

A ladder represents potential for those who stand at the bottom. A ladder represents danger for those who stand at the top.

Here, 1,900 words and two myths in, is my thesis:

The chaos in global supply chains will accelerate, and increase the odds of, startups replacing incumbents atop large industries. Startups are the trickster, wayless and flexible enough to thrive in chaos. As the economic architecture of the world shifts, they are better positioned to adapt and capitalize than sclerotic incumbents. “When Loki is suppressed, the world collapses; when he—and disorder—returns, the world is reborn.” Loki has returned. The world will be reborn.

I suspect you will want me to back that up with more than myth.

It may be due to chance and contingency that you haven’t heard of Architectural Innovation. It may be good marketing.

Good marketing can be the difference between a big company and a once-promising product. The same is true for ideas.

Most people reading this will be familiar with late Harvard Business School professor Clayton Christensen’s two types of innovation: Sustaining Innovation and Disruptive Innovation. Popularized in his 1997 book, The Innovator’s Dilemma, Sustaining and Disruptive Innovation have become core to how people in tech think about what new technologies will do to the established order.

Disruptive Innovations start out looking like toys and improve their way to the mainstream; by the time incumbents adapt, it’s too late. Sustaining Innovations, on the other hand, benefit incumbents, who incorporate them into existing offerings before startups have a chance to gain a foothold.

Maybe because it was just a paper and not a book, a third type of innovation has remained relatively under the radar, but it may be even more important to understanding the world to come.

According to Henderson and Clark, Architectural Innovation is the reconfiguration of existing product components into new relationships (the architecture) while leaving the core components largely unchanged, creating a particularly challenging type of change for established firms. It undermines their organizational knowledge structures while appearing less threatening than radical innovations.

The toy example they use is the fan. If the established technology were large electric ceiling fans, improvements in blade design would be incremental innovation, easy for incumbents to plug in, while central air conditioning would represent radical innovation, requiring entirely new components and relationships. A portable fan would represent an architectural innovation for fan manufacturers: the core components remain similar, but the architecture changes significantly.

Xerox losing market share to smaller, more reliable copiers in the mid-1970s? That’s disruptive innovation – Xerox made money leasing big, expensive copiers and servicing them when they inevitably broke down - but it’s also architectural innovation - competitors used the same optics, drums, and toner to make small copiers, but they packaged them differently.

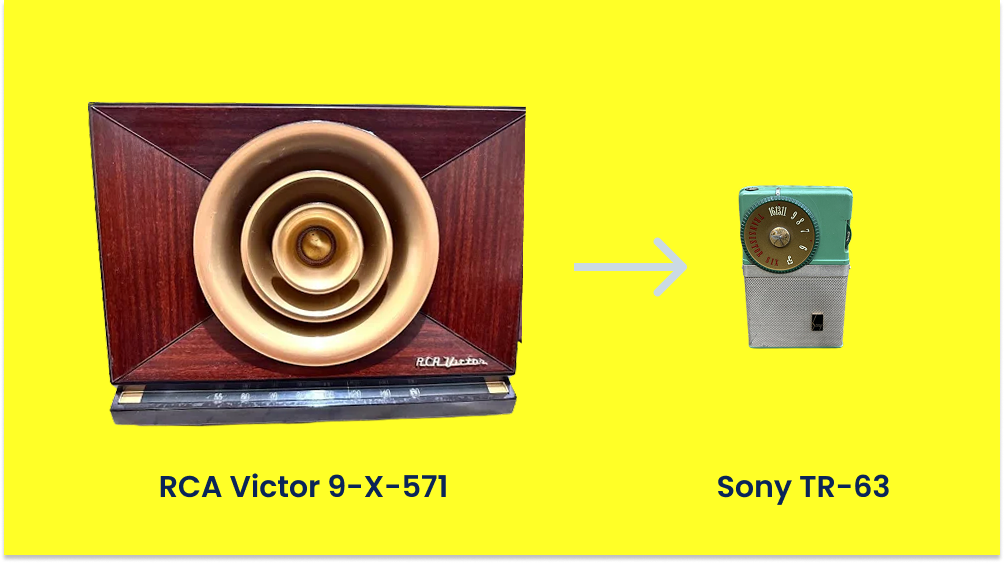

RCA was as dominant in radios in the 1950s as Xerox was in copiers in the early 1970s. Like Xerox, but less famously than Xerox PARC, RCA had an R&D arm that developed new products. In fact, it was RCA engineers who developed a prototype of a portable, transistorized radio receiver. “But RCA,” Henderson and Clark write, “saw little reason to pursue such an apparently inferior technology.” A small, relatively new Japanese company did, though. Sony, using technology licensed from RCA, “used the small transistorized radio to gain entry in the U.S. market” then “introduced successive models with improved sound quality and FM capability.” That is classic disruptive innovation, but it’s also architectural innovation. RCA tried to follow Sony’s lead, “yet RCA had great difficulty matching Sony’s product in the marketplace.”

The core difference between disruptive and architectural innovation is that disruptive innovation focuses on the business model and leaves room for the possibility that incumbents could bring their resources to bear on the seemingly smaller, toy-like opportunity if they were willing to risk the business, while architectural innovation focuses on how products are actually made, and argues that all those resources an incumbent might bring to bear are actually weights that prevent it from pivoting quickly enough to avoid destruction.

It’s the difference between won’t and can’t.

“Species well situated in a natural habitat are always at risk if that habitat changes.”

Writing not about Coyote but about modern manufacturing companies, specifically photolithographic alignment equipment companies, Henderson and Clark explain “why established firms often have a surprising degree of difficulty in adapting to architectural innovation.”

“Much of what the firm knows is useful and needs to be applied in the new product, but some of what it knows is not only not useful but may actually handicap the firm.”

See, in the early days of a new technology, there is a lot of confusion and a lot of experimentation. Trickster paradise. But once companies figure out the new product they can build with the new technology, they switch to optimizing (and ossifying) the process by which they make that product.

co-authored a paper titled A Dynamic Model of Process and Product Innovation. By looking at a study of 120 firms, they found that product innovation is initially dominant but gradually gives way to process innovation as the product design becomes standardized and firms shift their focus to improving production efficiency. As everything that can be squeezed out of a particular process has been, the rates of both product and process innovation trend towards zero.

Abernathy & Utterback, 1975

In the Vertical Integrator Series, we talked about Abernathy and Utterback in terms of the cycle from early vertical integration to later modularization. Henderson and Clark take a different tack.

In the early days of a new technology:

Organizations competing to design successful products experiment with many different technologies. Since success in the market turns on the synthesis of unfamiliar technologies in creative new designs, organizations must actively develop both knowledge about alternate components and knowledge of how these components can be integrated. With the emergence of a dominant design, which signals the general acceptance of a single architecture, firms cease to invest in learning about alternative configurations of the established set of components. New component knowledge becomes more valuable to a firm than new architectural knowledge because competition between designs revolves around refinements in particular components. Successful organizations therefore switch their limited attention from learning a little about many different possible designs to learning a great deal about the dominant design.

“The fox knows many things,” wrote the Greek poet Archilocus, “but the hedgehog knows one big thing.”

Since in an industry characterized by a dominant design, architectural knowledge is stable, it tends to become embedded in the practices and procedures of the organization.

Architectural knowledge becomes embedded in everything from communications channels to reporting structures to information filters to problem-solving strategies to supply chains, and as a result, it becomes automatic, unthinking, set in its way.

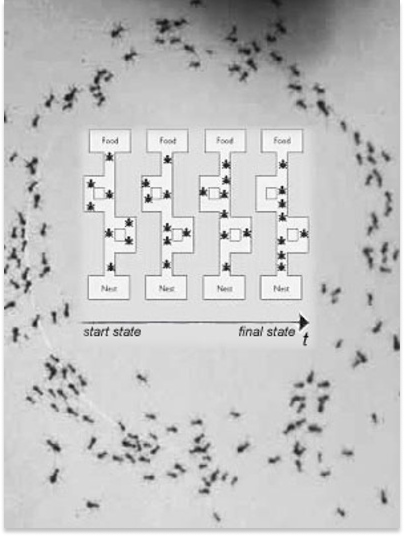

When I was at Breather, one of our ML engineers, Sam, told me about ant colony optimization algorithms. For some reason, the idea has stuck with me.

Ants do this clever thing. When an ant discovers a food source, it leaves a trail of pheromones on the ground as it returns to the nest. These pheromone trails serve as a communication system for other ants in the colony; they light up the path to food, olfactorily speaking. As more ants follow the trail and successfully find food, they reinforce the trail by depositing their own pheromones, creating a positive feedback loop. The more ants find food on a given path, the stronger the scent, the easier it is for the next ants to find food. Brilliant.

Wikipedia

But as you know, there ant no such thing as a free lunch. Several failure modes can occur. Ants can get trapped following each other in circles, reinforcing a loop to nowhere. Wind or rain can throw off the scent, leading ants to reinforce paths that don’t lead to food. Ants can become locked into a certain path, even if a new one emerges and the established one becomes suboptimal.

And of course, predictability itself is like a pheromone to the trickster. The trickster exists to throw people off their established paths.

When there is an architectural innovation, then, it creates problems for incumbents that they might not even realize they have until it’s too late. Henderson and Clark say that these problems have two sources.

First, it takes incumbents a long time to even identify a particular innovation as architectural. They’re on the lookout for component innovations, but their information filters might explicitly filter out information on architectural innovations.

“Since the core concepts of the design remain untouched,” they write, “the organization may mistakenly believe that it understands the new technology.” The mistake may only become apparent when they test the new components in the old design and fail.

Boeing 707 makes its first flight (1954)

Ironically, given that Boeing is my poster child for sclerotic incumbents ripe for replacement, Henderson and Clark point out that it was such an incumbent failure to recognize architectural innovation that allowed Boeing to rise to aircraft industry leadership.

With the emergence of the jet engine, an obviously important new component, “Established firms in the industry understood that they would need to develop jet engine expertise but failed to understand the ways in which its introduction would change the interactions between the engine and the rest of the plane in complex and subtle ways (Miller and Sawyers, 1968; Gardiner, 1986).” Boeing, as a newer entrant, was able to design a new aircraft with the jet engine in mind. The company soared.

Second, once they recognize that an innovation is architectural, organizations “need to build and apply new architectural knowledge effectively.” This is harder than it sounds. It needs to switch to a new mode of learning, “from one of refinement within a stable architecture to one of active search for new solutions within a constantly changing context.” It needs to invest time and resources. It needs to shift the premium from SOPs to experimentation and design. Then they need to actually learn, and implement, while continuing to operate the existing business.

“Established firms are faced with an awkward problem,” Henderson and Clark write. “Because their architectural knowledge is embedded in channels, filters, and strategies, the discovery process and the process of creating new information (and rooting out the old) usually takes time. The organization may be tempted to modify the channels, filters, and strategies that already exist rather than to incur the significant fixed costs and considerable organizational friction required to build new sets from scratch (Arrow, 1974).”

Here’s the kicker, their words, not mine:

Architectural innovation may thus have very significant competitive implications.

Established organizations may invest heavily in the new innovation, interpreting it as an incremental extension of the existing technology or underestimating its impact on their embedded architectural knowledge.

But new entrants to the industry may exploit its potential much more effectively, since they are not handicapped by a legacy of embedded and partially irrelevant architectural knowledge.

“Perhaps having no way also means that a creature can adapt itself to a changing world.”

If you think the existing system simply needs to be improved, you might want to build or invest in the types of companies that can improve it.

But if you believe that we’re in a moment in which systems need to be rebuilt, then you will want to build or invest in a smaller number of Vertical Integrators that can handle as much complexity as is needed to pull their industry into a new and better way of operating.

I believe that we are in such a moment, that we’re at the beginning of a new Techno-Economic Paradigm. Instead of building things that look like toys, Vertical Integrators are building new architectures around newly-available components - from AI to batteries to electric motors and more - to build products that are better, faster, and cheaper than incumbents. This is Architectural Innovation: “a Vertical Integrator designs a system for optimal performance, taking a risk on the combination of proven technologies.”

In fact, I hadn’t read Henderson and Clark when I wrote that series. I fed Claude all four of the essays and asked what else I should be reading, and Architectural Innovation was the first paper it suggested. Good rec.

But why all this talk of chaos and tricksters?

A brief note on memory and my writing process. I don’t have a great memory. I’ve spent the past couple of days trying to understand whether recessions and crises benefit startups more than incumbents, whether they’re a precursor to new Techno-Economic Paradigms. I read a good 1994 paper by Ricardo Caballero and Mohamad Hammour, The Cleansing Effect of Recessions, in which they cite two other economists, Blanchard and Diamond (1990): “Blanchard and Diamond point out that an explanation along creative destruction lines of the greater cyclicality of job destruction implies that recessions are times of ‘cleaning up,’ when outdated or relatively unprofitable techniques and products are pruned out of the productive system—an idea that was popular among pre-Keynesian ‘liquidationist’ theorists like Hayek or Schumpeter (see De Long 1990).” Then yesterday, I decided to re-read Vertical Integrators: Part II, because I knew that I had written something about what the end of a Techno-Economic Paradigm and the beginning of a new one looks like.

And there it was. Right there.

In that essay, to make sure that I wasn’t just picking facts that fit my thesis, I asked Claude, “According to Schumpeter and Perez, what happens to incumbents at the end of a Techno-Economic Paradigm? What signs would there be that we're at the end of one?”

I copied the whole response in, just to keep myself honest.

The only one missing: “Crisis or Recession: A major economic crisis or recession may signal the end of one paradigm and the potential beginning of another.”

Crisis or recession was the last unchecked sign that the old Techno-Economic Paradigm is dying so that a new one can be reborn.

So are we in a recession? Are we heading towards one?

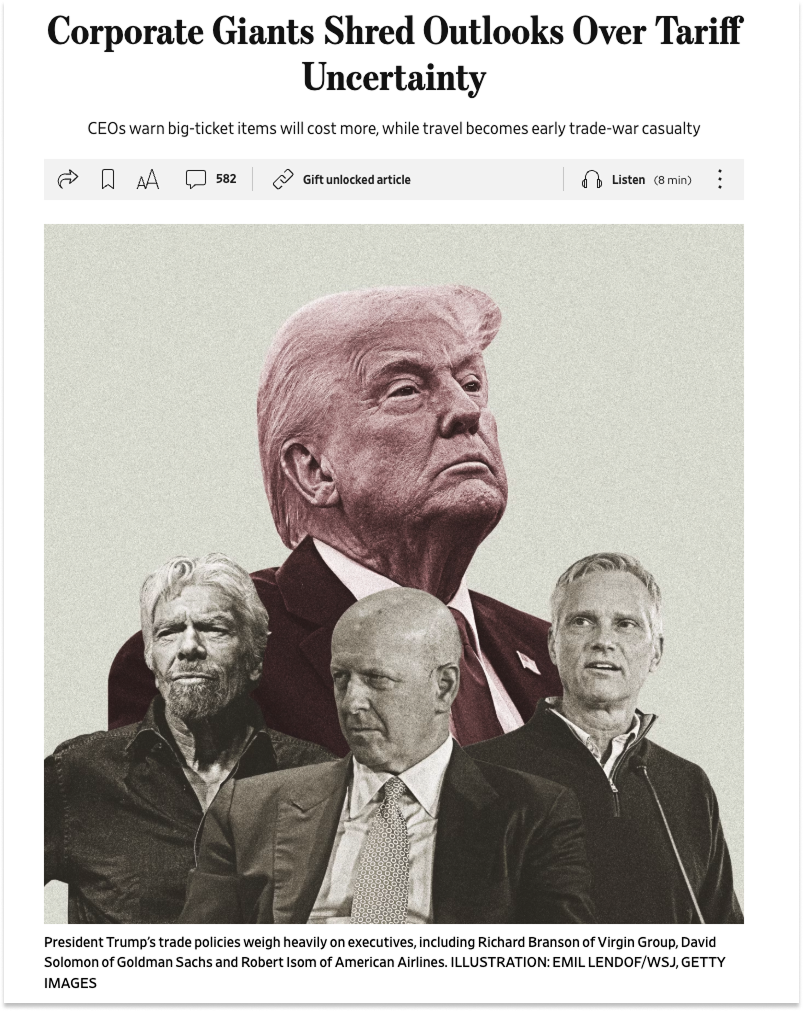

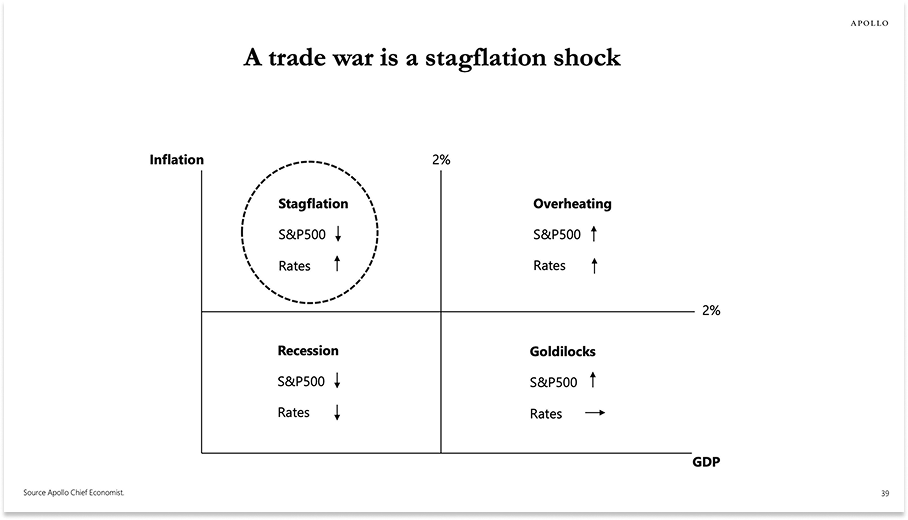

Apollo (the half a trillion dollar asset manager, not the Greek god) put out a report last week – How are US consumers and firms responding to tariffs? – showing chart after chart turning sharply south. If we’re not in a recession yet, Apollo’s Chief Economist predicts, just give it time.

For his part, JPMorgan CEO Jamie Dimon told a crowd last week that “he believes the best case outcome from the trade war would be a mild recession for the U.S. economy.”

I don’t know if we’ll enter a recession. It certainly feels like something bad’s coming. We’ve been talking about things like the dollar losing its reserve status, small businesses going out of business, supply chains in turmoil. On Saturday, this was the top story on wsj.com:

WSJ.com, April 25, 2025

It is the uncertainty that is so disturbing to the incumbents.

“The level of uncertainty is too high,” [Goldman Sachs CEO David] Solomon said. “It’s not healthy and it’s affecting investment, spending and planning, and that will have an effect on growth and the economy.”

“Do the rates stay in place as they’ve been published? How long do they stay in place for? Are we able to further mitigate it in other ways? Do they get rescinded and have other effects?” asked Neil Mitchill, RTX’s chief financial officer. “I don’t know.”

Like Frigg, their plan is to fight uncertainty with control. From the WSJ yesterday:

“Control the controllables and try to help mitigate some of the things we can’t control,” Norfolk Southern CEO Mark George told investors and analysts as he cited plans to wring savings out of fuel and labor costs, among other areas.

International Business Machines CEO Arvind Krishna said the technology company was “focused on areas we can control,” including productivity initiatives throughout the company.

PepsiCo CEO Ramon Laguarta said the company is “controlling what we can” by, in part, making its supply chain more efficient.

These CEOs have read too many balance sheets, too little myth.

There may be a recession. Who knows? Macro is hard. But chaos? There will certainly be chaos.

Chaos, to corporate Friggs, is the mistletoe dart.

Chaos, to startups, is a ladder.

Having studied Henderson and Clark, having studied the trickster, we can see the mechanism.

We have discussed at length, in this essay and others, the idea that as incumbents grow, they ossify.

They switch from product innovation to process innovation. They financialize and outsource. They plan for predictability. They attempt to control contingencies. They lay down pheromones on the path that has led to food so reliably for so long, and like Toucan Sam, follow their nose.

They architect communications channels, reporting structures, information filters, problem-solving strategies, and supply chains as if the trickster were just a myth.

I saw this tweet from Saagar Enjeti a couple weeks ago that encapsulates it all so well:

They forget to read Heinlein, who would have warned them that TANSTAAFL: There Ain't No Such Thing as a Free Lunch. You eventually pay for what you don’t pay for.

Free State of Luna Flag, The Moon is a Harsh Mistress, Robert Heinlein, Wikimedia

I am going to make a small leap, one that I hope you’ll grant me at this point, now that we’ve traveled so far.

Henderson and Clark write about the devastating effect minor architectural innovations can have on incumbents. I spared you the summary of nine pages on the impact that seemingly small changes to photolithographic alignment technology architecture made and broke companies’ fortunes.

These are architectural changes so seemingly small that the companies themselves, and the people within those companies, who spent every hour of every day thinking about photolithographic alignment technology, didn’t realize they were a big deal.

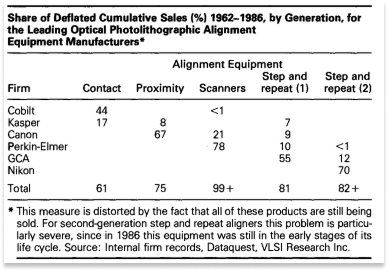

Look at the changes we’re talking about, like the one from the contact aligner to the proximity aligner:

Henderson & Clark

Can you even spot the difference? (Look at the gap between the Mask and Wafer.)

Now look at what this architectural innovation, and others like it, did to these companies’ market share over time:

Henderson & Clark

Cobilt went from market dominance with the contact aligner to irrelevance. Nikon came out of nowhere to capture 70% of the second-generation step and repeat aligner market.

Here’s the leap: if this is what happens because of small architectural changes, what do you think happens when the architecture of the global supply chain changes? When it’s not even clear how it’s going to change? When it’s thrown into chaos?

To be clear, it is a leap. TANSTAAFL. In Henderson and Clark’s view, one of the pernicious things about architectural innovation is that changes seem so small that companies might not even notice them until it’s too late. No one is missing the impact of tariffs.

But Henderson and Clark also say that even when incumbents notice, they’re slow to move, because moving is hard to do when you’ve built up an entire organization around the way things are and atrophied your “preparing for the way things might be” muscle. And Henderson and Clark are just two voices in a long line of voices – from Norse and Native American myth-makers to Joseph Schumpeter to Carlota Perez to Littlefinger - all saying basically the same thing.

Chaos is a ladder.

A ladder represents potential for those who stand at the bottom. A ladder represents danger for those who stand at the top.

It’s too early to tell which incumbents will tumble when and how as a result of the tariffs.

Boeing seems vulnerable, of course. Scott Christenson recently wrote How Much of a Boeing 737 is Foreign-Made?, in which he breaks down which components come from where. He found that, “40% — 50% of the parts of a Boeing 737 are obtained from foreign suppliers.” Some, like the vertical tail-fin, are sole-sourced or primarily-sourced in China. Christenson believes that switching to a “Made in America” 737 Max would halt production for 3-5 years while Boeing reshores, during which time Airbus would be able to pick off Boeing’s airline customers.

What else?

Something I’ve written about before is that you can see changes that will impact everyone in media first, because media is easier and faster to change than physical products. The internet, for example, came for media first before coming for everything else. The same, I think, is true for crypto. It moves so much faster than other industries that you can see early warning signs in the chart.

Anyway, here is a chart of BTC versus USD since Liberation Day:

Yahoo! Finance, as of April 25, 2025

It is now glib to say that strong companies are started during hard times. Airbnb and Uber came out of the Global Financial Crisis (GFC), you know. But people repeat these things for a reason.

The last time we had real stagflation, on the back of the 1973-1975 Oil Crisis-driven recession, Bill Gates and Paul Allen founded Microsoft in 1975 and Steves Jobs and Wozniak founded Apple in 1976. Those are the two most valuable companies in the world today, valued at a combined $6 trillion. With a T.

Not for nothing, Apollo expects this trade war to precipitate fresh stagflation.

Of course, the changing of the guard doesn’t happen overnight.

Bitcoin was started at least in part as a response to the GFC, too, and it’s taken more than a decade and a half for it to start fulfilling its role as a dollar hedge (if this current trend sticks).

First Bitcoin transaction: “Chancellor on brink of second bailout for banks.”

Crises sow the seeds. And the nature of the crisis determines which types of companies will wither and bloom. It is unsurprising that a financial crisis tied to mortgage-backed loans precipitated Bitcoin and Airbnb, a bank alternative and a way to make extra money to pay your mortgage, respectively. Since the GFC, Bitcoin and Airbnb have ridden the initial chaos to the top of their industries.

Hotels still exist, but by market cap, Airbnb is larger than any of them.

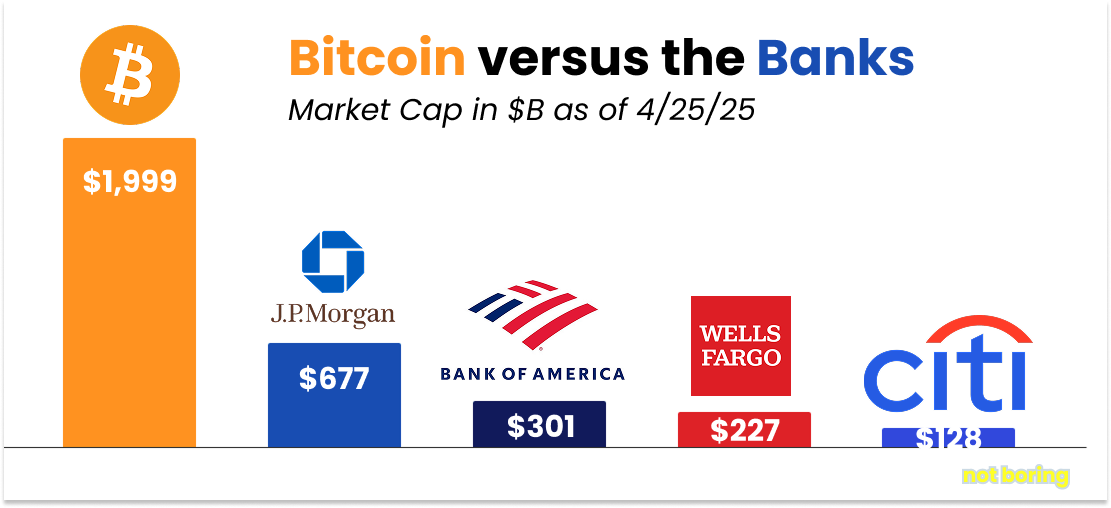

Banks still exist, but by market cap, Bitcoin is larger than the four largest American banks combined.

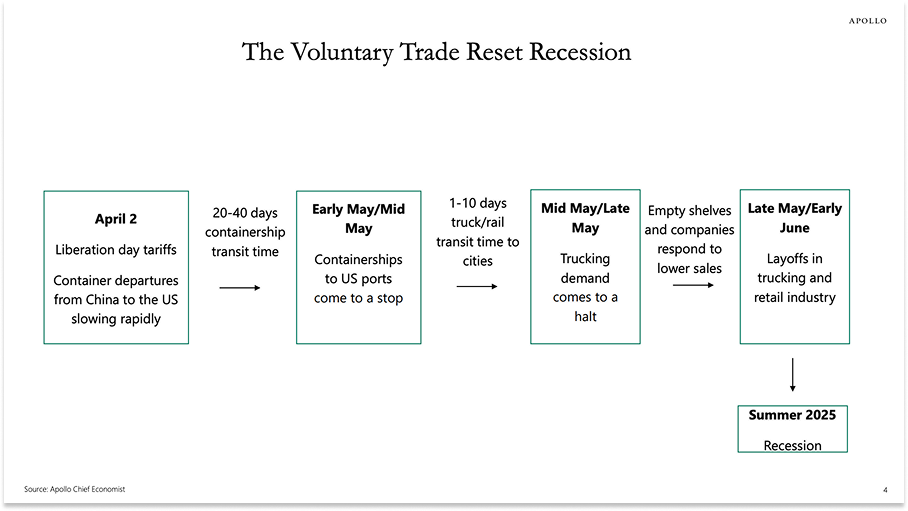

If the current crisis/recession/chaos is the Global Supply Chain Crisis or something – the Voluntary Trade Reset Recession, in Apollo’s words – which is what it looks like it will be, one that forces firms that make physical things to reshape their very architecture, even subtly, my contention is that we will see the same thing play out across practically every industry that makes physical things, which is most industries, over the next 15 years.

While it’s too early to tell which incumbents will tumble when and how as a result of the tariffs, and to tell which startups will replace them by which route, there is recent precedent for a Vertical Integrator handling supply chain disruptions better than modularized incumbents: Tesla.

COVID was a freak preview of a world in which global trade slows to a halt. While you were locked inside, automakers scrambled to access the chips that drive the performance of modern automobiles. Most of those chips, ~73% according to ChatGPT via the Semiconductor Industry Association (SIA), were made in East Asia: Taiwan, South Korea, Japan, and China.

ChatGPT pulling from SIA, at least directionally correct

This was predictably catastrophic for incumbent automakers, who’d architected their entire production processes and supply chains around the smooth global flow of goods. When that flow was disrupted, so was their production.

Headlines from AP and Reuters (2020 and 2021)

The headlines worked their way through to the financial and production numbers. By February 2021, CNBC reported that Ford predicted a $1-$2.5 billion 2021 earnings hit, while GM expected to pull in $1.5-$2 billion less. By May 2021, an AutoForecast Solutions study estimated that Ford had taken 326,616 vehicles out of production, GM had removed 277,966, and Stellantis had reduced production by 277,966 vehicles. Yikes.

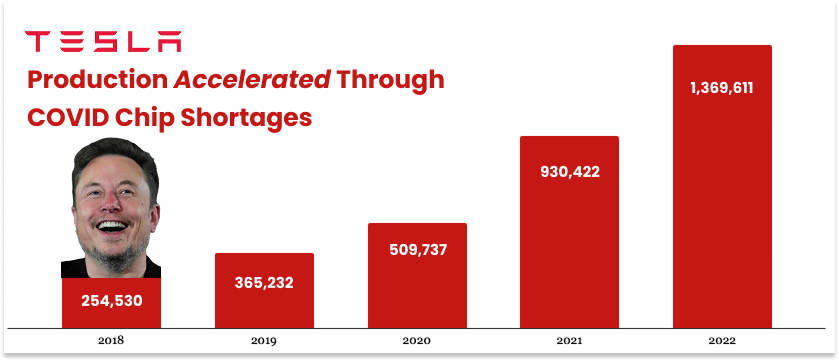

You remember this. Remember when the cost of used cars skyrocketed? What you might not remember (I didn’t) is that not all automakers were impacted equally. One, in fact, increased production in 2021. You guessed it: Tesla.

Source: Tesla Filings

That is remarkable.

Of course, Tesla was starting from a lower base. And it’s not that Tesla didn’t face the same challenges as everyone else. On the company’s Q1 2021 earnings call, Elon Musk said that the company had “insane difficulties” with the supply chain that quarter. "We've had some of the most difficult supply-chain challenges that we've ever experienced in the life of Tesla," he said. Tesla even briefly halted production of the Model 3 at its Fremont facility for two days.

But while Tesla, too, sourced components from around the world, it hadn’t welded the architecture of its product to its supply chain.

“Where trickster is the author of market exchange, he creates a form of commerce that allows strangers to come together without becoming kin;” Hyde explains. “People come into contact in his marketplace but they are not as a result connected.”

When Ford, GM, and Stellantis couldn’t access enough of the specific chips they needed, they had to halt production to match the shortage.

When Tesla couldn’t access the chips it had been using, it rewrote its firmware and rearchitected its cars to use different types of chips and even to use less of them.

“Yes, turns out we had more chips than we needed,” Elon said on the Q2 earnings call.

Because Tesla is vertically integrated, because the system is the product, it was able to use the chaos as an opportunity to not just survive, but to improve its product.

“One reason native observers may have chosen the coyote the animal to be Coyote the Trickster is that the former in fact does exhibit a great plasticity of behavior and is, therefore, a consummate survivor in a shifting world.”

Lewis Hyde could have been an investor. While all automakers (and most companies) ended up doing well in 2021 as chip shortages worked themselves out and consumer demand went bonkers, Tesla’s stock increased 6.6x more than the next best performer, Ford.

Tesla v. Ford v. GM v. Stellantis, 2020-2021; Yahoo! Finance

As importantly, Tesla’s US market share grew from 1.1% pre-pandemic in 2019 to 3.8% post-pandemic in 2022, while Ford and Stellantis’ market share fell by a combined 3%.

Tesla was not the most valuable automaker coming into the pandemic. That was Toyota. By June 2020, it took the lead. It has not looked back.

Today, Tesla is more valuable than the next 11 biggest automakers combined.

Chaos is … well, look at the chart.

Chaos is chaos for everyone.

I know of plenty of startups considering raising prices or even delaying product launches because of tariff uncertainty. My argument is not that this will not be hard. Loki is held beneath the earth, tied up with his children’s guts, poisonous venom dripping on his face before he leads an armageddon that clears the path for the earth to be reborn, refreshed. Startups and incumbents alike will perish in this economic armageddon.

But the world will be reborn. The world is always being reborn.

When it is, new gods will occupy the corporate heavens.

We’ve been waiting for this.

This is the Fourth Turning, “a decisive era of secular upheaval — the old order is toppled and a new one put in its place.” Hopefully, it is a bloodless and primarily economic one.

This is the death of Baldr, “the irremediable mediocrity of the present age” who “must be killed if there is to be any change for the better.”

This is the end of one Techno-Economic Paradigm, to make room for the next.

This is Creative Destruction, accelerated.

We never know what the crisis will look like when it comes, only that it must come.

“There is no way to suppress change, the story says, not even in heaven; there is only a choice between a way of living that allows constant, if gradual, alterations and a way of living that combines great control and cataclysmic upheavals.” The feeling of chaos, despite millennia of warnings, comes from the unpredictability of the mechanism.

For our own little corner of the world, and of history, I’ve tried to tease out that mechanism.

Incumbents, architected for a certain way of doing things, spend years laying down pheromones on the tried and true trail. That makes them efficient in times of certainty. That leaves them vulnerable to architectural innovations. That leaves them stranded on the wrong path when the winds shift, as they do, naturally, as technology progresses, and violently, in times of crisis.

You can see it in the quotes from CEOs, bemoaning uncertainty and preaching control. You can see it more concretely in Tesla’s COVID ascent.

Chaos is hard for everyone, but better for some. And that makes all the difference.

Startups, having no way, can more easily adapt themselves to the changing world. The ancients understood this; Henderson and Clark explained it.

With the benefit of hindsight, we will look back at this time and realize how useful it was for a number of startups that played it right.

It seems like it will be good for certain AI startups: as companies cut costs, an almost-good-enough AI that can replace an expensive human seems more attractive.

It seems like it will be good for certain robotics startups, for the same reason, but more directly tied to reshoring.

It seems like it will be good for certain crypto startups: crypto thrives on chaos. As I’ve tweeted, “Crypto is the purest way to bet that the future will be crazier than the present.”

Generally, Taleb writes that while a single startup is often fragile (it can die), the portfolio of many startups plus the option-like upside of any one success makes the ecosystem antifragile.

But I believe the companies that will benefit the most from this particular flavor of chaos are Vertical Integrators.

For one obvious thing, Vertical Integrators are building physical products (or systems) to compete with the incumbents who, as we’ve discussed, are most vulnerable to a crisis that rearchitects physical supply chains.

For another, the advantages Vertical Integrators have over incumbents in normal times become more advantageous in times of chaos. In Vertical Integrators: Part IV, I wrote that competing directly with powerful incumbents (versus using technology to build net-new capabilities) seems insane, but that there are “Advantages to Vertical Integration.” I will list the most relevant here:

Vertical integration allows for tighter feedback loops. While, per Henderson and Clark, incumbents take the architecture for granted, Vertical Integrators are constantly iterating on both components and architecture. “Hadrian,” I wrote, “Has software engineers working next to machinists in order to build better software and automate what can be automated.” They are constantly thinking about architecture.

Vertical integration allows for trade-offs at the system level as opposed to the product level. See: Tesla during COVID.

Vertical Integrators can control their own supply chains and bring their own core technologies down those curves. I have one portfolio company that was using a component from a large incumbent that kept failing. So they decided to build their own. It’s cheaper, higher performance, and shorter lead-time. They are using it themselves, and selling it to other companies frustrated by the incumbent.

Vertically integrating means better margins, if it works, at scale. Margins, in turbulent times, are room for error.

Finally, vertically integrating means competing for the biggest prizes. It means, as Schumpeter wrote, “striking not at the margins of the profits and the outputs of the existing firms but at their foundations and their very lives.”

Look at Anduril versus the Primes, as one example:

ChatGPT

Anduril works with dozens of Tier-1 suppliers. Lockheed Martin has “13,181 suppliers – more than 12,000 across the US and 932 around the globe. RTX executives said they have 2,000 suppliers in China alone. Of course, Anduril makes fewer, less complex products, but that is the point. So did Tesla. Anduril’s smaller, less global supplier base, vertical integration, software chops, use of COTS parts, and its flexibility of youth will help it weather the storm relatively better than incumbents.

You can play a similar game in every industry dominated by a sclerotic incumbent challenged by a Vertical Integrator. The startup will emerge in a better relative position than it would have without chaos. It will climb the ladder. From the bottom, it will strike at the incumbents’ foundations and their very lives.

At their foundations and their very lives.

Loki struck Baldr with the one weapon that could kill him. The Osettes in the Caucasus mountains of southern Russia tell a tale of Sydron, who rolls a saw-toothed wheel right at a secret weak spot in the nearly-invulnerable Soslan’s knees and cuts him down.

“From this brief story,” Hyde writes, “I would like to entertain the following generalization: the eternals are vulnerable at their joints. To kill a god or an ideal, go for their joints.”

Henderson and Clark might add, “The incumbents are vulnerable in their architectures. To kill an incumbent, go for their architectures.”

I wrote that list in September 2024, before the chaos. I was mainly focused on Vertical Integrators’ ability to benefit from technological (and, I would learn, architectural) change.

Everything I wrote then is a more significant advantage now, when the architecture of the economy is changing in real-time. When the incumbents’ joints are exposed.

Towards the end of Trickster Makes This World, Hyde makes a big reveal: the hymnist who sings of the trickster is the trickster himself; the audience is the cautious, controlling gods.

“If [Greek trickster] Hermes is the hymnist, then where shall we find Apollo? Apollo is the audience listening to the Hymn, and the hymnist’s performance is a sort of Hermes raid on their Apollonian side…

…as it works its magic it draws whoever will listen away from the Apollonian limits and into a dilating world of Hermetic possibility.”

That is my invitation to you. Chaos is inevitable. Learn to play with it. Embrace the uncertainty – instead of attempting to impose control on the world that was, join a Vertical Integrator and bring about the world that will be. Play the trickster.

The Vertical Integrators that play the chaos correctly will create and capture the lion’s share of value and set the stage for the half-century to come.

As uncertain as things seem right now, the uncertainty accelerates that future. Turbulence in the markets - in public markets and venture markets - is short-term noise on a long-term trend.

The hard part might just be embracing chance and contingency, as it always has been for those who feel they’re in control. I hope I have convinced you that that is the only move.

We will look back on 2025 like people look back on the GFC: a moment in time at which obviously Bitcoin, Airbnb, and Uber would have been born. We will wish we had seen it.

These moments are hard to see in the present, standing on the “razor’s edge of luck.”

But it is possible to see them. This is a very old story, one that plays out again and again across eras and cultures. And it’s one backed by both theory and observations.

Might this be an optimistic reading of the myths and the literature? Certainly, there’s a less hopeful way to read this: America is the controlling god, China the trickster. That in the destruction of the old world and the rebirth of the new, China will emerge on top.

But China is top down. China attempts to control. China is Frigg. America, for all of its volatility, can play the trickster. It is good, here, for old companies to die and for new ones to thrive. It’s how the system works, and why it’s antifragile.

What America does better than any country in the world is that we produce the tricksters who strike at the gods’ joints. If we are to win this trade war, emerge stronger, and continue The American Millennium, it will be because of our startups.

Those startup tricksters will become corporate gods one day, too. Vertical integration will give way to optimization. Architectures will ossify. The world will be restored to order.

And then there will be new chaos, new disorder, and new startups. This is the cycle.

Startups play with the trickster. Startups are the trickster. And trickster makes this world.

That’s all for today! We’ll be back in your inbox tomorrow with a special episode of Hyperlegible, and Friday with a Weekly Dose.

The most valuable, practical books I’ve read, thankfully when first published: “Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages.”

Another gem was “The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger”

Published only four years apart, 2002 and 2006, respectively, these books were loaded with practical perspective for the long term.

Loved reading this! I wonder: if vertical-integrator ‘tricksters’ still chase the same scoreboard—capital, scale, TAM—are we really rewriting the saga or just swapping the cast?

What if the gods meet their doom not by being supplanted, but by the quiet reshaping of the heavens they command?

The most valuable, practical books I’ve read, thankfully when first published: “Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages.”

Another gem was “The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger”

Published only four years apart, 2002 and 2006, respectively, these books were loaded with practical perspective for the long term.

Loved reading this! I wonder: if vertical-integrator ‘tricksters’ still chase the same scoreboard—capital, scale, TAM—are we really rewriting the saga or just swapping the cast?

What if the gods meet their doom not by being supplanted, but by the quiet reshaping of the heavens they command?