Capital Intensity Isn't Bad

How Hard Tech Can Be More Capital Efficient Than Software

Welcome to the 938 newly Not Boring people who have joined us since our last essay! Join 245,548 smart, curious folks by subscribing here:

Today’s Not Boring is brought to you by… Rox

Rox is on a mission to empower every business owner to secure and grow their revenue.

The best sellers at the fastest-growing companies, like OpenAI, Ramp, and MongoDB, trust Rox to power their revenue. By combining warehouse-native architecture with swarms of AI agents that keep you smart on your top customers, Rox helps top sellers do more in less time.

When I wrote about Rox last year, I heard from a lot of you that this is the revenue tool you’ve been waiting for. No overpromises. No Salesforce implementation. Just insights and assistance. So Ishan and I decided to team up to get more Not Boring readers on Rox.

You’re probably sick of getting AI-generated inbound. I certainly am. AI is not good enough to replace salespeople, which is why Rox doesn’t do that. Instead, it gives sellers superpowers. To hear from the man himself, watch Ishan and I discuss how Rox helps companies grow here.

Want to feel why the fastest-growing companies are choosing Rox as their new system of record? Run your own Rox Agent Swarms, with no cost (and no pain) to start.

Hi friends 👋 ,

Happy Tuesday!

Not Boring is weird. A couple of weeks ago, I wrote about Modern Magnificenza, drawing on Iain McGilchrist and Italian history to argue that tech billionaires should lead a right-brain renaissance. This week, I’m teaming up with William Godfrey at Tangible to argue that capital intensity isn’t bad, as long as you finance it correctly.

These seem like two entirely different ideas, but they’re connected. We’re not going to get the world we want unless we get the nitty gritty right. To colonize Mars, we need to finance rockets. To fix the grid, we need battery-backed loans. To get really big, impactful hard tech companies, we need startups to finance themselves correctly.

And we need investors to understand that capital intensity isn’t a bad thing.

Let’s get to it.

Capital Intensity Isn’t Bad

William Godfrey x Packy McCormick

The conventional wisdom that hard tech startups are inherently more dilutive than software companies has become venture capital's most expensive Boogeyman.

While hard tech startups1, or Vertical Integrators, can require more capital than software startups, those capital needs don’t necessarily translate into more dilution for equity investors. In fact, hard tech startups that master structured finance achieve lower dilution than software companies burning equity on customer acquisition.

The capital they do spend tends to go to more productive uses; hard tech spend is more differentiating than software spend. Factories are deeper moats than increasingly expensive customer acquisition in competitive markets. And because so much capital is required, and potential winners are identifiable earlier, the leading hard tech companies actually can use capital as a moat. Not everyone can raise the mix of equity and debt required to build big things, which means less competition for those who can.

This is an argument I’ve tried to make before, and a conversation that I have with practically every LP I speak with about Not Boring Capital, and a conversation that every hard tech company has with practically every VC they speak with.

So I figured it was time to call in the big guns.

William Godfrey is the co-founder of Tangible, which helps hardware businesses structure, raise and manage asset-backed debt capital, and the co-author, along with my friend Brett Bivens, of the essay The Rise of Production Capital. After I mentioned the essay in Everything is Technology, William and I spoke and decided to try to kill this Boogeyman once and for all, with data, case studies, and financing structures that hard tech startups can use to turn their capital intensity into an advantage.

In the first half of the essay, we’re going to talk about why hard tech startups’ capital intensity isn’t necessarily a disadvantage and how using different types of financing can limit dilution and juice equity returns. To do that well, we’ll need to give you the context.

In the second, we’re going to get very specific about one type of financing: Asset-Backed Securitisation (ABS). We’ll explain what they are, how they work, the flavors they come in, and what hardware operators should be thinking about to set themselves up to issue them when the time is right. Then we’ll do some case studies, both real and illustrative, to make it all clear.

It starts out as an argument and turns into a handbook. Hopefully, having digested the former, you’ll find the latter useful.

Structured finance seems… not not boring. We hear you. But the goal of everything we talk about here isn’t simply to make cool products and watch them wither away into bankruptcy. It’s to scale them to the point at which they can make a real impact. And to do that, at some point or another, you’ll need structured finance.

As technology businesses get more complex and sophisticated, the capital that supports them needs to, as well. Capital structures need to rise to meet the opportunity.

We’ll explain how, and why getting it right can turn capital intensity into an advantage.

First, though, we need to get on the same page about what capital intensity is.

Capital Intensity is Neither Good Nor Bad

Capital intensity is the measure of how much capital (assets, equipment, infrastructure) a company needs to generate revenue.

At the extreme ends of the spectrum, a vibe coded software product might have very low capital intensity and a rocket company might have very high capital intensity.

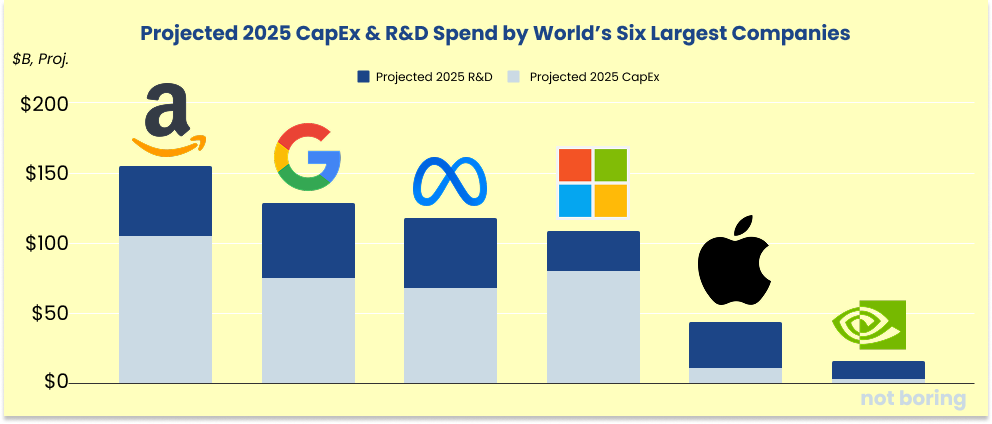

Many companies start out looking capital-light but become capital-intense over time. Google. Amazon. Microsoft. Meta. The four largest “software” companies will spend more than $300 billion combined on CapEx this year, largely due to data center and AI investments. Apple, always a hardware company with some software, will spend less this year, but committed to spending more than $500 billion in US investments over the next four years. That is on top of another $230 combined projected R&D spend.

Nvidia aside (unlike real men, it does not have fabs), the world’s largest companies are among its most capital intensive.

SpaceX, now America’s most valuable private company at $350 billion, has also been among its most capital intensive. But, and this is the big one, its fundraising hasn’t been particularly dilutive. SpaceX has experienced less than 50% dilution since its first outside funding two decades ago, and Elon Musk still personally owns an estimated 42% of the company.

By contrast, Uber is one of Ben Thompson’s canonical examples of a Level 2 Aggregator, which “do not own their supply; however, they do incur transaction costs in bringing suppliers onto their platform.” Its founder, Travis Kalanick, owned just 8.6% of the company at IPO.

The three co-founders of another Level 2 Aggregator, Airbnb, owned a combined 30% of the business at IPO.

How is it possible that the founders of two defining Aggregators owned significantly less of their businesses after a decade than Musk owns of a company that builds (and occasionally blows up) its own rockets after two?

Certainly, SpaceX spends much more on CapEx than Uber or Airbnb. It is more capital intense.

Most investors think that capital intensity is inherently bad. It isn’t. It can be good, actually.

The question is where the capital comes from and where capital intensity lives.

Where Does the Capital Come From?

SpaceX has raised over $9 billion in venture capital and growth equity over its life. Uber raised $15.9 billion before going public. It doesn’t take less money to make rockets than it does to make a ridesharing app. The difference is, as The Washington Post reported in February, as if it were a bad thing, that SpaceX has received over $22 billion from the government (not including classified defense & intelligence contracts).

SpaceX President Gwynne Shotwell said in 2013 that the company would “probably be limping along” without NASA’s support. Last year, Shotwell told an investment conference of the U.S. Government contracts, “We earned that. It’s not a bad thing to serve the U.S. government with great capability and products.”

We agree. SpaceX’s relationship with NASA is one of the most fruitful partnerships between a government and one of its companies in recent memory.

The Post quotes its owner and Blue Origin founder, Jeff Bezos, as saying in 2016: “Elon’s real superpower is getting government money.”

We agree with this one, too, with a qualification: One of Elon’s superpowers is funding his businesses with the cheapest and most appropriate capital available.

This is a superpower more hard tech founders are acquiring, and that they must acquire to win.

We have written at length about our belief that the future will be owned by companies that combine bits and atoms, software and hardware to build better, cheaper, and/or faster products than incumbents. To that belief, we would add money. Bits + Atoms + Dollars.

The future belongs to companies that combine the world's best engineers with the world's best financial engineers.

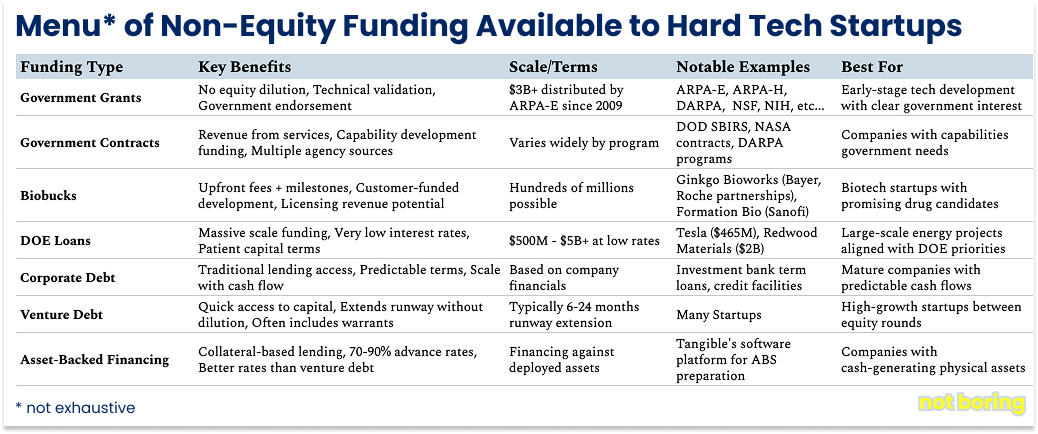

During the hard tech renaissance, smart technical founders have realized that they must also be smart about the way they capitalize their businesses, and have become more aware of the myriad financing options available to them. A few examples include:

Each hard tech company will have a different menu of options available to them depending on what they do and how far along they are. Most founders and investors are familiar with, and take advantage, of most of the appropriate ones.

You would be arrested for dereliction as a defense tech founder, for example, for not pursuing DOD contracts, or as an energy founder for not applying for the appropriate DOE loans. Any CFO with a pulse might try to mix in a little corporate debt on the back of a venture fundraising.

Asset-backed financing, however, perhaps because it can be the most sophisticated and bespoke, is deeply underutilized and underappreciated.

(Plug: AI should help make sense of all of this complexity for you. We built Tangible because watching billion-dollar structures built and managed in hand-crafted Excels was giving us nightmares. Instead of lending against your equity story, Tangible helps you prepare your company story and access lenders, who finance against the actual cash-generating assets you've deployed.)

All Debt is Not Created Equal

As hard tech and venture become more aware that you shouldn’t fund everything with equity, almost everyone now realizes that equity should fund R&D and debt should fund scale.

That is a step in the right direction. But all debt is not created equal.

The two overarching types of debt instruments are corporate debt and asset-backed financing.

Corporate debt gets priced on the strength of your company's balance sheet. If you're a startup, that's deep junk bond territory, because lenders face full enterprise risk plus bankruptcy risk, which is safely assumed to be a zero recovery scenario. Asset-backed debt gets primarily priced on the specific collateral and cash flows (although for very early stage companies there is some degree of corporate risk that is also accounted for but to a lesser extent than corporate debt). Those same charging stations price lower because lenders have first lien on hard assets plus dedicated payment streams that never touch your corporate balance sheet.

When most startups we hear about raise debt, it’s corporate debt in one form or another.

At Breather, we raised venture debt, which ended up being good for neither us nor our lender.

Debt is the promise of paying back the principal with interest in a timely manner, unlike equity, which has no formal obligation to repay. Venture debt attempts to blend these two worlds in a way that sometimes falls short of the mark for helping a hardware company to scale. Debt investors, even “venture” debt investors, primarily care about getting repaid their capital on time and less about your venture story. Venture debt can be useful, but it can also be dangerous.

Uber got big enough that it didn’t have to raise venture debt but also didn’t only have to rely on its $15.9 billion in venture capital. It raised $1.6 billion in convertible debt from Goldman Sachs in 2015, followed by a $1.15 billion leveraged loan in 2016.

This institutional debt was cheaper than equity but more expensive than asset-backed alternatives since lenders were underwriting the company's overall business risk rather than specific collateral. When we talk about “cheaper” or “more expensive,” we mean the cost of capital. Interest rates on debt are typically lower than the expected returns equity investors demand.

The reason that Uber raised more expensive corporate debt instead of cheaper asset-backed alternatives is simple: ride-sharing platforms are asset-light. They don’t have the assets to use as collateral for their borrowing.

Hence the meme: “Uber owns no cars. Airbnb owns no hotels. [Company X] owns no [Y]. This is the new economy.”

But owning things can be good, actually, if capital intense. The question here is where the capital intensity lives.

For smart hard tech companies, capital intensity doesn't live on their balance sheet, where it can weigh them down. It lives in off-balance sheet structures that actually multiply their capital efficiency, and even generate revenue through servicing fees and yield, while isolating risk.

Asset-backed financing is all about stripping out assets from businesses and packaging them up as a product that the debt capital markets will like.

If you can pull it off, asset-backed financing can be the difference between scale and insolvency. But adding it into the mix can be a tricky transition for startups to make, because what debt capital markets like is almost diametrically opposed to what venture capital likes.

The Two Acts of Hard Tech Companies

Venture capitalists expect founders to sell them the dream, the bigger and riskier the better. Lenders expect borrowers to show them the numbers, the more precise and predictable the better.

To please the former, too many venture-backed hard tech companies high on equity funding have spent their money in ways that make the latter shudder.

Planning ahead can fix this. For hard tech companies, VC and debt each represent one act in the story of a successful business.

Every startup goes through a similar Act I: The Engineering.

In Act I, a startup needs to prove that it can actually do what it thinks it can do. Design the hardware. Prove the technology works. Find product-market fit. Show unit economics. Get to repeatability.

This is pure equity territory. Higher risk, higher returns. You're asking investors to underwrite technical risk, market risk, execution risk. You burn cash to prove that your thing works and people want it. VCs are comfortable here because this feels like every other startup.

Act II: The Financial Engineering is where fortunes are lost and won… and where many VCs check out, because Act II doesn’t look like “tech” anymore.

Act II is about turning your deployed technology into a financial instrument that institutional capital wants to own. You're no longer asking investors to underwrite your startup risk. You're asking them to underwrite the cash flows your technology generates.

In Tesla’s Act II, it became one of America’s largest consumer lenders. In SpaceX’s Act II, it became one of the government’s largest contractors, and could borrow against the US Government’s well-accepted ability to pay those contracts.

Act II changes everything a startup does, even how it thinks about and presents itself.

In Act I, you compete with other startups for expensive equity capital. In Act II, you compete with asset-backed securities and corporate bonds for cheap institutional capital.

In Act I, every dollar of growth requires a dollar of equity. In Act II, every dollar of equity can support multiple dollars of debt-financed growth.

In Act I, you're a technology company that happens to make money. In Act II, you're a financial products company that happens to use technology.

Most capital-intensive companies die in the transition. This is the Valley of Death. They raise equity to prove the technology works, then keep raising equity to scale deployment. They never learn to package their deployed assets into financial products.

Think solar companies that install panels but never securitize the cash flows. EV charging companies that build networks but never turn them into infrastructure bonds. Manufacturing companies that prove unit economics but never create equipment financing programs.

One big challenge to consider is that many hard tech (or, specifically, deep tech) companies build first-of-a-kind (FOAK) products that may be hard to securitize. Venture loves unstandardized and esoteric; credit loves standardized and legible. To be clear: the world needs more of this kind of innovation! But recognize that it makes accessing credit more difficult, and may contribute to capital intensity’s bad reputation. There is a tightrope to walk.

Companies that fail to transition to Act II remain addicted to expensive equity while their competitors graduate to scalable cheaper debt deployments.

At their own peril, they ignore the age-old lesson:

All else equal over time, cheapest cost of capital wins.

Which means that if you’re building a hard tech startup, and you want to turn it into a big hard tech company, you need to understand asset-backed financing.

How Asset-Backed Financing (aka Securitization) Works

The simplest way to understand an asset-backed facility is that it’s like a credit card that you can buy one thing with.

Your Amex can buy anything: dinner, flights, random stuff on Amazon. An ABS is a credit card that can only buy EV charging stations. Or solar panels. Or whatever specific asset you're securitizing.

The credit card company (investors) fronts the money, you buy the assets, and the monthly payments from those assets pay down the credit card balance.

Wall Street thrives on jargon and acronyms, but strip away both, and ABS is simple: you're creating a legal entity that owns specific assets and cash flows, separate from your operating company.

If your startup fails, the assets and their income streams live on. Your job as a hard tech founder is to make these streams reliable and enduring, even in the event of the death of your startup. That the asset might outlive its creator sums up the difference in approaches.

Viewed in this light, the job in Act I is to prove that you can build the crazy thing you say you’re going to build, and that that thing can generate relatively predictable cash flows.

Once you begin generating those cash flows, you can sell a small package of them to investors, and scale up the size of the package as you prove that you’re good for the money and add more assets. Optimally, you’d set up multiple facilities to reflect differences in geography, restraints, and models, and then grow the assets in each as you mature instead of writing new docs each time you need to raise more capital.

This is how successful capital-intensive companies move the capital intensity off their balance sheets: they originate assets, prove the model works, then package and sell those assets to institutional investors backed by steady, predictable returns.

Tesla doesn't keep every car loan on its books; it packages them into a portfolio of loans and sells this portfolio. Solar companies don't hold 25-year power purchase agreements; they securitize them and recycle the capital. Securitization means selling your future cash flows for cash today, at an appropriate discount.

The company keeps the profitable origination business and capital providers get the steady cash flows.

This is financial engineering 101, but it's treated like black magic in venture. Which is fair, actually, because backing companies with tangible assets is not what venture has done for decades. To be even more fair, ABS can be intentionally complex.

An ABS is basically a massive algorithm for governing this new off balance sheet structure of yours. Every payment that comes in gets sorted, allocated, and distributed according to hundreds of rules. Which investors get paid first? How much goes to reserves? Who gets paid when in the waterfall? What happens if Station #247 stops paying? What covenants stop you from having one customer that gets too big as a % of your originations?

When the risk of misunderstanding that algorithm is the seizure of your business’ productive assets, it’s understandable that some companies and their investors go with the more expensive equity; at least the equity doesn’t come with bond covenants.

Worse, this algorithm usually runs on... spreadsheets. Thousands of them. Excel models so complex they need their own user manuals. One misplaced formula and your entire deal structure falls apart.

Every deal comes with credit agreements that are legitimately thicker than a phone book, full of covenants that read like the legal version of the calming words hypnotists say to knock you out and triggers that sound like nuclear launch codes.

Take this sample covenant: "If the 3-month rolling average of Cumulative Net Loss Rate exceeds 2.50% or if the Payment Rate falls below 15.0% for any two consecutive collection periods, the Revolving Period shall terminate immediately."

Translation: If too many charging stations break or customers stop paying, the growth phase ends and you start paying investors back.

Of course, to translate that, you would have to know that most ABS structures have two phases that determine whether you keep "buying more stuff" (Revolving Period) or start "paying down the balance” (Amortization Period).

During the Revolving Period, you can keep adding new assets to the pool. Install 100 charging stations, securitize them, use that money to install 200 more stations, add those to the same securitization. Rinse, repeat. The investors' "credit line" keeps growing as long as the assets perform well. This is the growth period.

During the Amortization Period, the music stops. No more new assets. All cash flows from existing assets go straight to paying down investor principal. This is usually triggered by time or performance metrics falling below certain thresholds. Putting a deal into an amortization phase more quickly is a risk mitigation feature that can help limit losses.

Think of it like a construction loan that converts to a mortgage. First you build (revolving), then you pay it off (amortizing). Mature companies have multiple facilities, some of which are Revolving and some of which are paying down at any given time.

That’s just one example of the many terms you’ll have to get to know. Wall Street dines on opacity.

There’s good news for those intrepid enough to wade through it all, though: the more complex the structure, the higher the barriers to entry. The algorithm gets more sophisticated, the documentation gets thicker, and your moat gets deeper.

It’s worth learning the basics (and then hiring or working with professionals).

The ABS Basics

So you want to securitize your assets?

Long before that day comes, you need to prepare the company to eventually be in a position to sell to ABS investors. There are a few things you should plan for from the early days of the business (or look for in a hard tech business, if you’re an investor):

Clear offtake agreements: Someone committed to buying your output

Standardizable assets: Repeatable deployments that can be packaged

Predictable cash flows: Instalment sales, subscriptions, leases, usage-based fees

Collateral value: Market value of the assets backing the debt

Reporting: Solid operations and processes to capture every beat

Credit Enhancements: Tools you can make use of to reduce the risk of non payment of interest or principal, for example third-party guarantees (usually from what the market perceives to be credit worthy counterparties with strong credit ratings)

Seed Portfolio: A showcase of assets that you’ve funded yourself to prove that you know how to do your core business

Often, these are things you’ll want to think about anyway. Clear offtake agreements means there will be demand for what you’re supplying. Repeatable deployments makes operations easier and allow you to capture the benefits of scaled manufacturing. Every investor, VC or credit, likes predictable cash flows; that’s why SaaS won. And your robot is more valuable if it can work in any warehouse you put it in or can be sold in the open market for cash; maybe the massive battery you put in the robot is even easy to take out, and sell to someone else. The design choice to have one screw or thirty being the barrier can have a real effect on your fundability. Preparing for asset-backed financing is just another reason to dot these i’s and cross these t’s.

Once you have hardware deployed, or a plan to, and generating cash flows, or contracted to, financing becomes a multi-dimensional puzzle. Most founders think there's one "right" way to finance hardware assets. Actually, you're assembling puzzle pieces across multiple dimensions - and when they fit together perfectly, you can unlock dramatically cheaper capital.

Here's how the best hardware companies think about it:

The Universal Process

Originate Assets: Deploy hardware, sign customer contracts

Pool & Package: Group similar assets with predictable cash flows

Credit Enhancement: Add guarantees, cash reserves, insurance, overcollateralization

Solve the Puzzle: Match all the pieces to create the optimal structure

Recycle Capital: Use proceeds to deploy more assets

Optimize Over Time: Use track record to access better puzzle pieces

The magic happens in Step 4, where you and your team solve the puzzle. There is no universal “best option.” This process is all about finding the combination where all your puzzle pieces fit together seamlessly, which the credit world calls “structuring.”

The ABS Puzzle Pieces

There are six big things (and a million little ones) to consider when determining how to securitize your assets.

Puzzle Piece #1: Your Assets

Physical Characteristics: Solar panels with 25-year warranties fit different financing structures than a fleet of esoteric robots just learning to walk. Durability, technological obsolescence risk, resale value, how easy they are to move and maintenance requirements all shape your options.

Cash Flow Patterns: Predictable monthly payments unlock different capital than seasonal usage spikes. Revenue timing, contract lengths, contracted floors, and payment reliability determine which investors will be interested.

Deployment Model: Distributed assets (thousands of charging stations) need different structures than centralized ones (single large solar farm). Geographic concentration affects risk and operational complexity.

Puzzle Piece #2: Your Customers

Payment Preferences: Monthly subscriptions, usage-based fees, upfront purchases, or long-term contracts. Your financing structure needs to match how customers actually want to pay and can often mean they’ll buy more from you.

Credit Profile: Large companies with strong perceived credit worthiness, such as a utility with a ‘AAA’ rating enables different financing than startups paying monthly. Customer creditworthiness directly impacts not just your borrowing costs but also your ability to access this type of capital. And seeing as you’re now becoming a lender, it’s something you should really care about as well.

Contract Terms: Take-or-pay contracts, termination rights, escalation clauses, early repayment penalties. The specific contract language, who drafted it, all determines cash flow predictability and investor comfort.

Puzzle Piece #3: Your Company Stage

Track Record: Early-stage companies pay premium rates until they prove their model. Each successful deployment expands your financing options.

Performance Data: A minimum of 12-18 months of operating history is typically the threshold where institutional investors start to get comfortable. Before that, you're likely to have more limited choices.

Management Team: Investors finance management teams as much as assets. Prior experience with similar deployments matters enormously. Investors want to hear their mother tongue of ABS from the other side of the table.

Puzzle Piece #4: Market Environment

Regulatory Landscape: Energy sector regulations, transportation rules, tax incentives. Some sectors have specific financing programs or restrictions that shape your options.

Macro Environment: Rising rates favor floating-rate structures, falling rates favor fixed (from the perspective of the lender). The macro environment affects which investors are active, which products have delays in production, which will have tariffs, and any extra political goodwill around asset classes like data centers or robotics.

Competitive Dynamics: How many similar deals are competing for the same capital? Market saturation affects pricing and terms.

Puzzle Piece #5: Investor Appetite

Pension funds want predictable cash flows with minimal risk. Hedge funds or private credit funds want higher returns and can accept complexity, newness or novelty. Matching risk profiles is crucial.

Return Requirements: Different investors have different return hurdles. Senior capital accepts lower returns for safety. Specialty capital demands higher returns for risk.

Investment Mandates: Some investors can only buy certain structures (ABS vs. project finance) or asset classes (energy vs. transportation). Understanding mandates helps target the right capital.

Puzzle Piece #6: Deal Structure Options

Cash Flow Structures:

Pass-Through: Everyone owns everything proportionally

Pay-Through/Sequential: Waterfall with senior/junior tranches that respects the hierarchy of creditors in liquidation

Hybrid: Combines both approaches for flexibility

Financing Vehicles:

Asset-Backed Securitization: Regulated, standardized, public market access

Project Finance: Ring-fenced projects with dedicated cash flows

Equipment Finance/Leasing: Traditional lending secured by physical assets

Master Trusts: Revolving structures for repeatable deployments

Warehouse Facilities: Credit lines before larger securitizations

And much much more!

Solving the Puzzle: Examples

A few examples will demonstrate how fitting your puzzle pieces might work in practice, and show that this part of the work isn’t overwhelmingly complex.

Example 1: Mature EV Charging Network

Assets: Predictable locations, long-term utility contracts

Customers: Investment-grade utilities with take-or-pay agreements

Company: 3 years operating history, experienced management

Market: Supportive regulatory environment, stable rates

Solution: Pay-through ABS with senior/junior tranches

Example 2: Early-Stage Robot Deployment

Assets: New technology, software-dependent, limited resale value

Customers: Mix of startups and established companies, monthly payments

Company: 6 months operating data, first-time founders

Market: High interest rates, limited comparable deals

Solution: Equipment finance with specialty lender, graduate to master trust

Example 3: Utility-Scale Solar

Assets: Single large installation, 25-year power purchase agreement

Customers: State utility with AA credit rating

Company: Experienced developer, multiple prior projects

Market: Tax incentives available, infrastructure funds active

Solution: Project finance with infrastructure debt fund

There is a fair amount of complexity to think through here, which can seem scary when unfamiliar but which is both manageable and learnable. People much dumber than you issue ABS all the time. It’s not… rocket science.

But it can help turn rocket science into a rocket business, or any small-scale project into a large one. For those willing to piece together the puzzle, there are significant, potentially company-defining advantages.

The Advantages of ABS

Remember the lesson: all else equal, cheapest cost of capital wins.

The first advantage is a crucial one: ABS is cheaper than corporate debt.

In the US public markets, asset-backed ABS almost always price inside (at lower spreads and yields than) unsecured corporate bonds of comparable rating and tenor. ABS spreads were 28–36 basis points (bps) tighter and all-in yields roughly 50–60 bps lower than unsecured IG corporates over two recent period-end snapshots.

There are a number of structural reasons for this:

Structural credit enhancement: Subordination, excess spread, over-collateralisation and reserve accounts mean even AAA ABS can withstand large collateral losses. Investors require less spread to compensate for risk.

Shorter interest-rate exposure: Most ABS amortise quickly (2-4 y weighted-average life), so duration risk, and the spread needed to bear it, is lower.

Collateralized vs. unsecured: ABS investors have a direct claim on ringfenced specific cash-flow pools; corporate bondholders rely on the issuer’s general credit and pool of assets in case of bankruptcy.

Ratings mix: In part because of the reasons listed above, AAA/AA tranches dominate the ABS index, whereas the IG corporate index skews A/BBB. Tighter spreads partly reflect their higher ratings.

Less important day-to-day, but existentially important when it counts, a second advantage of ABS is that it is bankruptcy remote. This works two ways.

First, it means that if the parent company goes bankrupt, its creditors can’t reach into the Special Purpose Vehicle (SPV) set up to house the assets and their cash flows. ABS investors will continue to receive the cash flows as long as the assets generate them. This contributes to ABS’ cheaper cost of capital.

Second, it means that, once in an SPV, if the assets underperform, there is generally no recourse to the originator (although for startups, a corporate guarantee may be required). A wipe-out in the SPV can’t force the parent into Chapter 11. It can’t bankrupt the company. It can still hurt earnings. The parent company typically holds the equity piece, which is wiped out, and must often repurchase bad collateral. But the losses are bounded. With unsecured corporate debt, on the other hand, creditors can go after everything and push the company into bankruptcy.

The third advantage of ABS may be the most strategically critical: ABS can turn capital intensity into a force multiplier, giving you the ability to multiply your equity dollars.

If you're able to offload your capital intensity to someone who will buy it from you, you are at worst as good as any other technology company. You have the balance sheet of an asset-light business with the moats of a (well-run) capital intensive one.

Most pure-software companies are fighting in hyper-competitive markets with massive marketing spend. Hardware companies that crack securitization get natural monopolies with lower acquisition costs and potential software company valuations.

Plus, because small-scale success unlocks larger facilities, ABS allows companies to unlock more capital to build more assets without raising additional equity.

The companies that figure this out first will have long lasting competitive advantages - they'll be able to deploy faster, cheaper, and at scale while competitors are still trying to raise equity for each new deployment.

Perhaps most relevant to dispelling the belief that hard tech is too capital intensive to make sense for most VCs, getting your financing right can dramatically lower your dilution.

A toy model will clarify what we mean.

Why Capital Intensive Doesn’t Necessarily Equal Dilutive

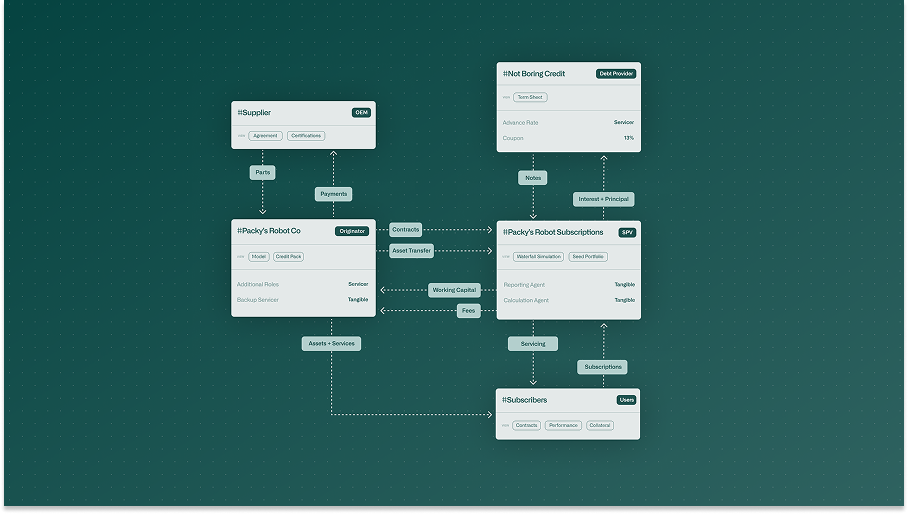

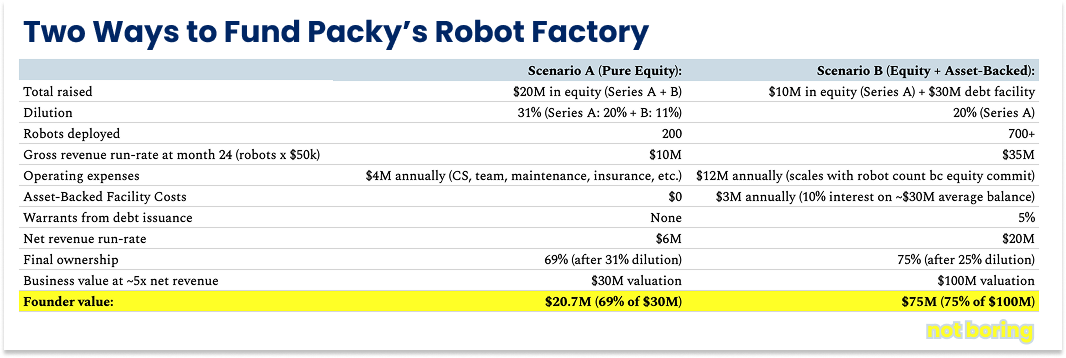

Let's model this with Packy's robot company, which sells warehouse robots on subscription, lowering the CAPEX barrier to entry for our customers and enabling larger deployments, before locking them in with the recurring fees.

There are two ways that we can finance this business: with pure equity, or by combining equity and asset-backed financing. The latter is more capital efficient than the other and results in a lower blended cost of financing over time.

This is a toy model, but the takeaway is clear: more robots, more revenue, less dilution.

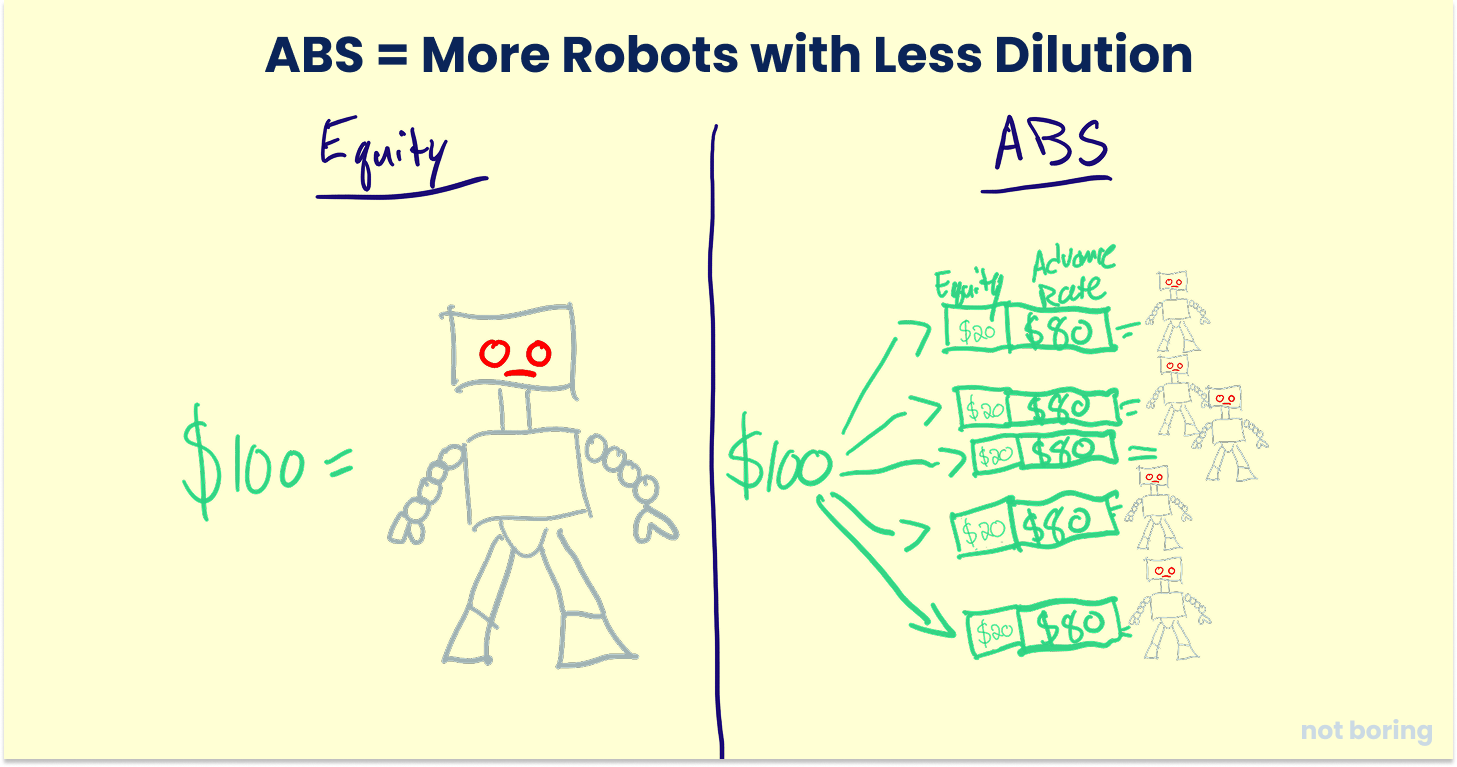

With an initial $1M seed portfolio, Company B unlocks a $30M facility, which funds more than 3x the number of robots as Company A with less equity, and therefore, less dilution. The subscription payments from deployed robots create a self-reinforcing cycle where each new deployment strengthens your ability to access more capital from the facility.

In Scenario B, you keep 6% more equity while deploying more capital to finance more assets. Scale this across multiple rounds, and the difference becomes massive.

The traditional equity financing looks something like this:

Deploy $1 of capital → Generate revenue → Retain all profits

Capital gets "locked up" in assets until payback is reached

Efficiency measured as: Revenue ÷ Total Capital Deployed

The structured finance scenario, the money multiplies and the business becomes more efficient:

Deploy $1 of capital → Generate revenue → Recycle 80% (your advance rate) immediately → Deploy again

Same $1 of equity capital supports multiple asset deployments over time

Efficiency measured as: Total Revenue Generated ÷ Equity Capital Required

Both models achieve the same 5x revenue-to-capex ratio, but the structured approach is more capital efficient because of three factors:

Capital Velocity: Your equity dollar "turns" faster - instead of being locked in one robot, it can support the deployment of multiple robots over time.

Leverage Effect: Each equity dollar leverages debt capital (the AB facility) to deploy more total assets than equity alone could support.

Continuous Deployment: Capital recycling enables continuous scaling and upsizing, although you may want to raise equity to scale even faster.

With ABS, in other words, not only is each dollar “cheaper,” it’s also more productive.

There are, of course, trade-offs, the most important of which is that in the ABS scenario, you accept X% lower margins per robot (i.e. 70% → 62%) in exchange for 4x deployment scale with the same equity base. The "efficiency" comes from maximizing the productivity of your scarce resource (equity capital), not necessarily maximizing the margin on each individual transaction.

It's about making your equity capital work harder and faster, not just making it work more profitably on a per-unit basis.

In short, capital intensive businesses can still be capital efficient, and often even more so when done right.

And no startup has done it better than Crusoe Energy.

Crusoe Energy Case Study

“The guy at the heart of the Stargate build in Abilene is Chase Lochmiller,” said Bloomberg’s Emily Chang, walking onto the construction site. “He’s the founder of Crusoe, the little-known data center startup overseeing this massive project.”

Crusoe is a seven-year-old startup that started out using the gas that would have otherwise been flared off into the atmosphere to mine bitcoin. As the AI boom kicked off, Chase and his co-founder Cully Cavness realized that the same idea would work for AI data centers. Power was a key input, and they could get it cheaply, and latency didn’t matter as much, so they could put the data centers wherever the gas happened to be.

Fast forward, and the company was last valued at $2.8 billion in December 2024 and is now managing the largest AI data center buildout in history, the $500 billion Stargate project, having raised just $1.59 billion in equity from the likes of Founders Fund, Bain Capital Ventures, and Valor Equity Partners.

“Just” is a weird word to put next to $1.59 billion, but there are very few startups more capital intensive than one that builds its own data centers and power generation and buys tens of thousands of GPUs. To fund all of that, Crusoe turned to asset-backed financing.

In August 2023, Chase went on the ACQ2 podcast with Ben and David from Acquired, and laid out how the business financed itself in a way that echoes a lot of the points we have been making. You can listen to the section starting at 1:13:42 and ending around 1:22:26:

We will include a big chunk of that conversation here, because it’s so relevant to everything we’ve written, and bolded for emphasis:

Chase: Obviously our business is not just a pure enterprise SaaS business, right? It’s pretty far from it. We have quite a bit of CapEx, we build technology, we build software solutions, but we also have physical infrastructure and big pieces of heavy machinery that are involved in the overall process… We’ve certainly done a lot of equity, but on the CapEx side, right, we’ve done a bunch of very interesting things around how do we actually scale the business without just plowing equity dollars into CapEx, because at the end of the day that’s not really what we want to do.

Ben: For listeners who don’t come from the finance side, why is it a bad idea to just finance all the CapEx with equity and when in a business’ life cycle can you explore other options? What level of predictability do you need?

Chase: …In our case, we really didn’t want to finance big physical assets with equity dollars because there is collateral there at the end of the day versus…

David: It’s like a mortgage versus venture investment. These are different things.

Chase: Exactly. Most people don’t buy their house with 100% cash because they can get a low-interest mortgage and the bank’s happy to make that loan because there’s existing collateral, if you stop making your payments they can just take over your house and liquidate it for more than the outstanding loan that they have with you. In our case, we have large pieces of power generation equipment that we’ve been able to finance with asset-backed financing. There was one group that we have a large facility with called Generate, there’s another group that we did something with called Northbase, and another group called Spark Fund, all on the electrical and asset-backed financing for electrical systems and power generation equipment.

What’s cool about that is the way those are structured is they are asset-backed, which means it isn’t debt that sort of defaults up to the parent company necessarily, like if we stop paying they’d come and they’d take the generator and they’d go liquidate it on the secondary market, they’d get made whole that way, and it’s not an incremental liability for Crusoe the company. Now, that’s our plan. You know, if my debt holders are listening to the show right now, we entirely intend to continue to make all of our payments.

Ben: But it’s useful for listeners to understand how those sorts of things work and how it connects to the parent company.

David: And this is how most of the non-tech business world works. Like if you’re Procter & Gamble or something, you’re not financing your assembly lines with equity.

Chase: Yup, yup. We essentially have four big pieces of CapEx: we have generators and electrical infrastructure supporting the power generation side, we have GPUs and associated networking equipment and servers, we have bitcoin mining hardware, so ASICS that are used to run the SHA-256D hashing algorithm, and then we have data center infrastructure, the actual physical boxes or buildings that we build to house the actual equipment.

Our belief is that the best way to structure financing is to have each of those individually with different asset-backed loan facilities, and then we use equity capital to continue to grow, invest in technology, hire the team, and also come up with our piece of the loan essentially. Where it’s like you typically don’t get 100% LTV on something, just like when you buy a house it’s typically not a 0% down payment, you typically put in whatever 20-30% as a down payment on a house, we do a similar thing with generators or GPUs with these asset-backed financing facilities.

David: And I would imagine what’s cool is that there are pools of capital out there that are interested in the risk and reward profiles of each of those different things.

Chase: Exactly. We did a project financing facility with a really clever and creative credit fund called Upper 90, and this was actually focused on our bitcoin mining business, and it had equity-like constructs to it but it had debt-like constructs to it, and it was actually one of the keys to helping us get off the ground was through this facility, and it was cool to see investors like that that were really willing to think deep and creatively about what our actual revenue stream was independent of where we were at in terms of stage of company. Because we did that around our Series A, it ended up being a total of $55M that we deployed through these facilities that really enabled us to kind of grow and scale that digital currency mining business in a way that didn’t dramatically dilute our equity capital.

David: Right, otherwise you would have been adding on another $55M to your Series A, and that would have sucked.

Chase: Exactly. There are just creative financing solutions that, people by default think that they need to go raise the next series of funding, and I don’t think that’s the case, and I think there are a lot of ways founders can end up owning a larger percentage of the company by finding the right investor for the right component of their overall capital stack and capital structure.

We don’t have a time machine, so there’s no way we could have paid him to say all of that.

When I had Chase and Cully on Not Boring Founders, I said, “It’s built what I think is one of the greatest cathedrals to capitalism in startup land.”

I meant that they took a problem (flared gas) and turned it into a solution (cheap energy for compute), economically, and that they financed the whole thing brilliantly. To recap:

In 2019, when Founders Fund led their Seed Round, Upper90 came in with a debt facility that same year.

By 2021, they had 86 data centers and proved the model with a $40M debt round.

In the 2022 Series C, they raised $350M in equity from G2 Venture Partners PLUS $155M in credit facilities from three specialist lenders (SVB, Sparkfund, Generate).

By 2023, as AI boomed, they realized they could use GPUs as collateral, and raised $200 million in asset-backed financing from Upper90, specifically for GPU purchases.

In 2024, they raised $600 million led by Founders Fund at a $2.8B valuation. NVIDIA participated.

This year, in 2025, they raised $225M Upper90 syndicated facility with pension funds and insurance companies (March), $11.6B joint venture development capital for Texas data center expansion as part of Stargate with Blue Owl (May), and $750M in infrastructure debt from Brookfield.

When trillion dollar asset managers start lending to you, you've graduated from startup to infrastructure company.

There are a few key lessons to learn from Crusoe:

Originate Early and Often: Crusoe "helps businesses with predictable revenue and collateral." Crusoe had both. Hard assets that credit investors could touch, feel, and repossess if needed.

Relationship-Driven Debt Compounds: Upper90's relationship "started in 2019 with equipment financing" and evolved through multiple growth stages. Each successful facility made the next one easier and larger.

Think in Instruments, Not Just "Debt vs. Equity": Crusoe used equipment financing, asset-backed lending, infrastructure debt, development joint ventures, and syndicated facilities. Each serves a specific purpose at a specific point in time.

Big Counterparties = Big Money: When NVIDIA becomes an equity investor and Oracle becomes your anchor tenant, credit investors unlock pools of capital that make venture look like pocket change.

If you do all of those things right, and solve all of the engineering challenges required to do things like building data centers powered by stranded energy in the middle of nowhere, you can build something really big, really fast.

The Good Thing About Hard Assets

We’ve thrown a lot at you. We don’t expect you to absorb it all in one setting. Save it, print it out, reference it when you’re thinking about how to finance your business, and then, if you think that asset-based financing makes sense, hire professionals. Feel free to reach out to Will at will@tangible.finance if you want to get pointed in the right direction.

Financing your business the right way might be the difference between life and death, or at least between owning a lot of your company at IPO versus owning a little.

Any business worth building will be capital intensive, either at the beginning or over time.

Software companies will typically need much less money upfront, because software is not inherently expensive to build. You can even vibe code it now. But the thing that makes it easier to build means that they will have to spend more money competing in the competitive Red Queen’s Race, on things like customer acquisition, that don’t contribute to a lasting moat. Remember how many 30% off Ubers you took when they were trying to win the market? If they get really big, like Facebook, Google, and Microsoft, they will need to spend tens of billions to protect their throne and capture the next platform shift or risk destruction.

Deep tech companies need more equity capital upfront, to build a physical thing before they’ve proven that they can, which scares investors. But if they make it through, they face less competition over time because of the inherent difficulty (and capital intensity) of what they’re building. Once they’ve reached the promised land, many hard tech companies can (and should) turn to asset-based financing to fund the deployment of assets with predictable cash flows, building up bigger leads, and digging deeper moats, in the process.

For these companies, properly financing the business can mean less dilution and more speed. Our hypothetical robot company was able to put 3x the robots into the field, faster, with two-thirds the dilution. In infrastructure markets, speed wins. Premium locations get taken. Network effects kick in. Economies of scale create cost advantages. Regulatory favor goes to market leaders. Investors pile into the winner, and cut off competitors’ financial oxygen.

This is why companies like Base Power Company care so much about speed: there are only so many residential battery early adopters, and they’re only going to put one battery on their home. Of course, they are thinking about asset-backed financing. In my first Deep Dive on the company, I wrote:

For now, Base is financing batteries off of its own balance sheet. In the months ahead, it needs to grow the portfolio and prove out the economics of its batteries so that it can secure asset-backed loans to fuel its growth. Building a portfolio that appeals to lenders means that Base can unlock a lower cost of capital, which means more batteries and more profits, and ultimately even lower costs of capital. The moat widens.

As these companies build up a capital markets track record, they can unlock larger facilities and cheaper financing costs, compounding their advantage. Financing itself becomes a moat.

The biggest challenges of our generation cannot be solved with software alone. Solving them requires CapEx, and CapEx isn’t free.

But capital intensity isn’t a bad thing. It’s another challenge to be solved, and another product to sell. And those who solve it can build more capital-efficient businesses than their competitors, which is what counts. There is no shortage of money in the world for companies that generate predictable cash flows solving huge problems. Private credit assets under management is expected to double to $3 trillion by 2028, dwarfing venture capital by nearly an order of magnitude, and turbocharging it.

The trick is structuring your cash flows in ways that appeal to investors. Which can be complex and difficult, but that’s what makes it valuable.

Don’t be scared. Capital intensity isn’t bad, as long as you finance it right.

Thanks to William for co-writing this essay and contributing all the smart stuff, to Brett Bivens for introducing us, to the Tangible team for feedback, and to Claude for editing.

That’s all for today. We’ll be back in your inbox with the Weekly Dose on Friday. In the meantime, set your sellers up with agent swarm on Rox. We’ll

Thanks for reading,

Packy

We are going to use hard tech startups instead of Vertical Integrators throughout, because the lessons apply to any company building hardware that generates cash flows, not just the fully vertically integrated ones competing directly with incumbents.

Interesting crossover into the capex-heavy world. Coming from a renewables background a lot of this is familiar.

As you've called out, where a lot of startups die is the FOAK stage.

Have seen difficulty funding development capital at the corporate level.

Have seen hesitancy for project capital (equity or debt) for projects that nobody but the startup can operate. At that point, the risk/reward is not the same as normal project capital for "standardized" assets.

Okay, this was a fun and very interesting thesis. Having retired from a business that was primarily a service platform (not 100% SaaS, but close), with multiple rounds of financing and evaluation, and shareholder entrances and exits, before IPO, it was very interesting to read about the different ways to look at these shareholder impacts.