Scarce Assets

The Abundance-Driven Scarcity Supercycle

Welcome to the 621 newly Not Boring people who have joined us since our last essay! Join 264,075 smart, curious folks by subscribing here:

Hi friends 👋,

Happy Thursday!

A few weeks ago in Not Boring Capital’s quarterly LP update, I wrote a small essay on scarce assets in a period of abundance. Then Thrive bought the Giants and HOF bought Bugatti and Marc Andreessen pointed out that when one thing becomes abundant, another becomes scarce, and I figured it was a good time to dive a little deeper on what is going to be a supercycle in scarce assets of all shapes and sizes (and a bear market for the easily replicable).

It is also, unofficially, the latest installment in my ongoing plea that you just be different and more you.

Let’s get to it.

Today’s Not Boring is brought to you by… Deel

Hiring globally doesn’t have to be complicated

Hiring globally can unlock growth, but local laws, payroll, and compliance often slow startups down.

Deel’s free guide breaks down what an Employer of Record (EOR) is, how startups use EORs to hire internationally without opening entities, and when it makes sense to use one so you can scale with confidence.

Scarce Assets

The playwright S.N. Behrman, in a short study of the Gilded Age English art dealer Joseph Duveen titled “Duveen,” quipped that “Duveen … noticed that Europe had plenty of art and America had plenty of money.”

Duveen made his fortune and his legend balancing that imbalance. “Joseph Duveen sold hundreds of Old Masters, for soaring prices, to American multimillionaires between the early years of the twentieth century and 1939, when he died, at the age of sixty-nine,” wrote Peter Schjeldahl in The New Yorker. He sold a Rembrandt to Carnegie partner Henry Clay Frick in 1906 for $225,000, which was absurd at the time, and the absurdity only grew. The hundreds of millions, in today’s dollars, of Frick’s money that Duveen spent on the Old Masters formed the basis for The Frick Collection.

Not to be outdone, and the whole point was not to be outdone, the Pittsburgh banker and US Treasury Secretary Andrew Mellon purchased, through Duveen, Raphael’s Cowper Madonna for $970,000 (~$21 million today) in 1929, and then, in 1936, a collection of 42 Italian Renaissance paintings and sculptures for $21 million, or half a billion today. These became core to the National Gallery of Art.

Duveen was an absolute animal, who practically spied on clients and potential clients in order to understand their psychology, their likes and dislikes, and even their trash. Per The New Yorker, “(A Duveen employee crowed that, during the years that Mellon was Treasury Secretary, ‘the contents of his wastebasket reached the train to New York in the time it took the Secretary to walk home from the office.’)”

Duveen knew the value of understanding what was priceless to someone who could afford anything with a price tag. For the newly rich of the Gilded Age, as for the wealthy of any era, that was status via scarcity, and the thing that was high-status and scarce for American millionaires back then was connection to the heritage of the old country.

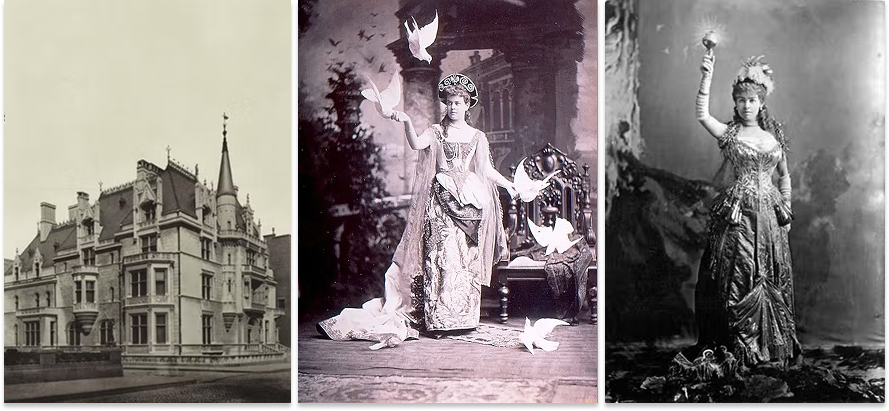

Humans are funny, and the Robber Barons’ clans had the money to be funnier than most. Alva Vanderbilt, the wife of Cornelius Vanderbilt’s grandson William, was the funniest of them all.

Despite the Vanderbilts’ gargantuan railroad and shipping fortune – the Commodore had more money than the US Treasury when he died in 1877, something like 5% of all the money in the country per The First Tycoon – they lacked social standing in New York. Caroline Schermerhorn Astor and Ward McAllister’s “Four Hundred,” instituted as a response to the meteoric rise in multimillionaires after the Civil War, defined who counted as Society. The Vanderbilts were not on the list.

So Alva did what one does. She built a French chateau on Fifth Avenue that dwarfed the street’s older townhouses, and threw the party of the century: the 1883 Vanderbilt Costume Ball. The point was to get on Astor’s list, so Alva supposedly withheld an invitation from Carrie Astor because Mrs. Astor had never called on the Vanderbilt home. To get her daughter invited, Mrs. Astor had to leave her visiting card at 660 Fifth Avenue, which meant officially recognizing the Vanderbilts. The Astors’ invitation arrived the next day.

The party cost $250,000, or $6 million in today’s dollars, but as The Museum of the City of New York writes, “as of March 27, 1883 the Vanderbilts were at the top of a new New York society that was not just limited to 400 people.”

New York City, evidently, wasn’t enough for Alva, nor for many of America’s multimillionaire class. In 1895, Alva married her daughter, Consuela Vanderbilt, to the Duke of Marlborough. Her money, his title.

By 1915, Titled Americans reported that there were 454 “Dollar Princesses,” or American heiresses who had married into European aristocracy.

Titles were scarce. They weren’t making more of them. And therefore, they were desirable to a rising class of people who could buy almost anything.

As Duveen might have noted, Europe had plenty of titles and America had plenty of money.

Not so fast, says Duveen biographer Meryle Secrest, who thought Behrman’s line was overly simplistic. Whether art or titles, she writes, “Nothing would have persuaded titled Europeans, and particularly the British landed aristocracy, to part with their family heirlooms had there not been a catastrophic change of fortune in the final years of the nineteenth century.”

Why were the Europeans suddenly much poorer than they were classy? What was the catastrophe?

“Cheap food from the United States and elsewhere had wrecked the profits of European agriculture.”

The Europeans were done in by abundance, so they had to sell their Scarce Assets, which became more valuable, thanks to the wealth generated by that very same abundance. Pip pip.

Humans fucking love scarce things. Always have. The more we win from abundance, the more we want to roll the winnings into scarce things. Scarce is special.

If we are entering a period of untold abundance, expect a roaring bull market in Scarce Assets.

Macro Scarce Assets

Which is what we are seeing.

Last Friday, Josh Kushner announced Thrive Eternal, the firm’s permanent capital holding company that will concentrate in a small handful of “Iconic franchises and cultural institutions rooted in tradition, identity, and shared experience,” starting with the San Francisco Giants.

Later that same day, HOF Capital announced that it’s leading a consortium to acquire Porsche’s stakes in Bugatti Rimac and Rimac Group.

They are not making any more 143-year-old baseball teams in the technology capital of the world, nor are they making any more 117-year-old French hypercar houses.

There is an obvious story here that, despite its obviousness, is worth spelling out.

As wealth grows and concentrates, demand for a limited pool of Scarce Assets dramatically outstrips supply.

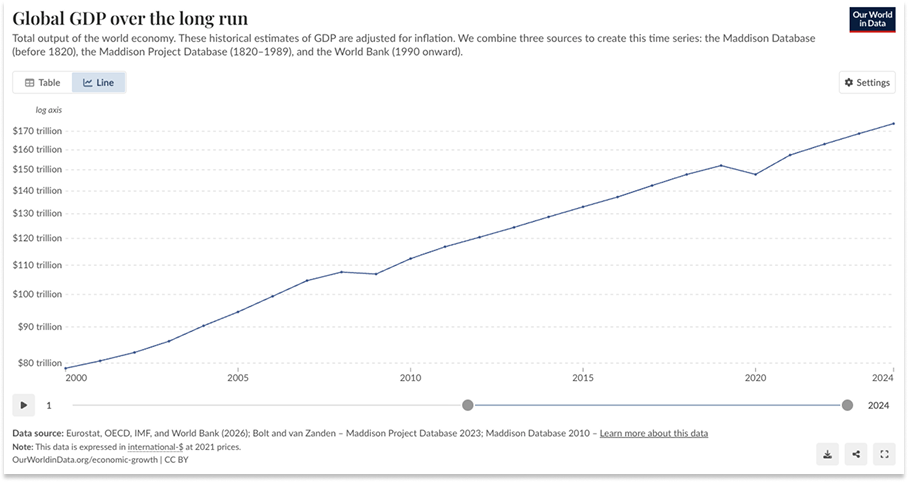

Since the turn of the millennium, global GDP has more than doubled from $78.69T to $174.28T (in 2021 Dollars), while the number of San Francisco MLB teams and Bugatti-makers has stayed flat.

GDP growth undersells the situation, though, because the composition of the growth is more relevant to our conversation. If the $100T increase in GDP was split evenly across the world’s 8.3 billion people, each person’s extra $12,048 wouldn’t mean squat for the price of the San Francisco Giants. People would be able to spend less of their money on food and more on clothes or vacations, but they wouldn’t be able to buy baseball teams.

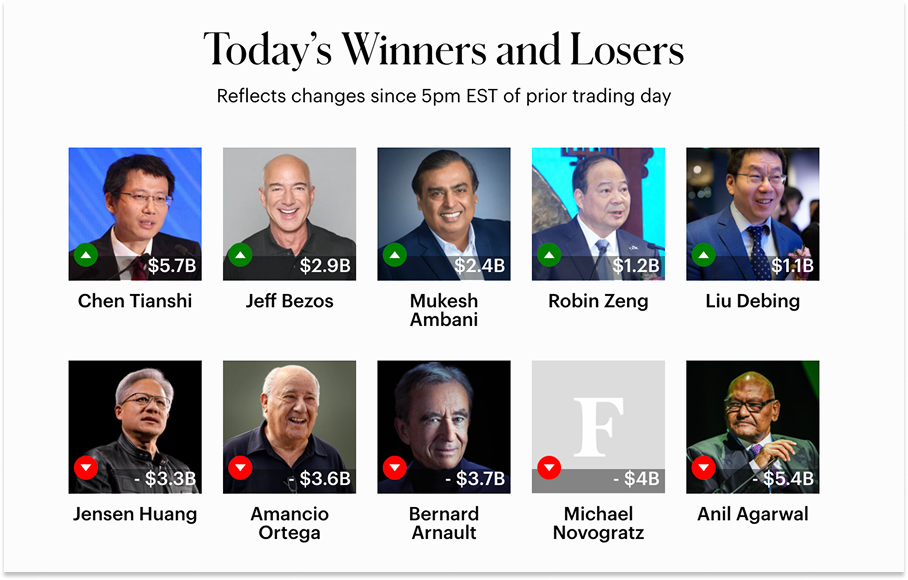

More relevant is the fact that the wealth of the world’s Top 100 wealthiest people has grown 10x in nominal terms, from $895 billion in 2000 to $7.2 trillion today. Adjusted for inflation, the world’s richest 100 people are more than 4x wealthier today than they were a quarter century ago, and their wealth has grown twice as fast as the global economy.

Bill Gates was the world’s richest person at the turn of the millennium, with $60 billion. Today, Elon Musk and Larry Page have more money than all of 2000’s billionaires combined. The amount of money that Cambricon CEO Chen Tianshi made yesterday would rank him 60th on the 2000 list. You probably haven’t even heard of Cambricon.

Plus, more of the world’s savings sit inside of professionally managed pools of capital whose mandate is to preserve purchasing power, compound over long periods, and find assets that can’t easily be printed, copied, or competed away. Pension assets have more than tripled since the early 2000s, reaching roughly $70 trillion by the end of 2024. Private markets, a rounding error at roughly $600 billion to under $1 trillion in 2000, are now a $13 trillion to $15 trillion asset class. Sovereign wealth funds, which held roughly $1 trillion in 2000, now control something like $12 trillion to $15 trillion.

So, a much higher and more concentrated numerator (more cash) chasing a ~flat denominator (Scarce Assets).

Compounding the issue, these assets are often taken off the market altogether, shrinking the pool. Frick’s art is in The Frick Collection. Mellon’s is in The National Gallery. Thrive named its new vehicle Eternal.

So, a much higher and more concentrated numerator (more cash) chasing a decreasing denominator (Scarce Assets).

And boom goes the dynamite.

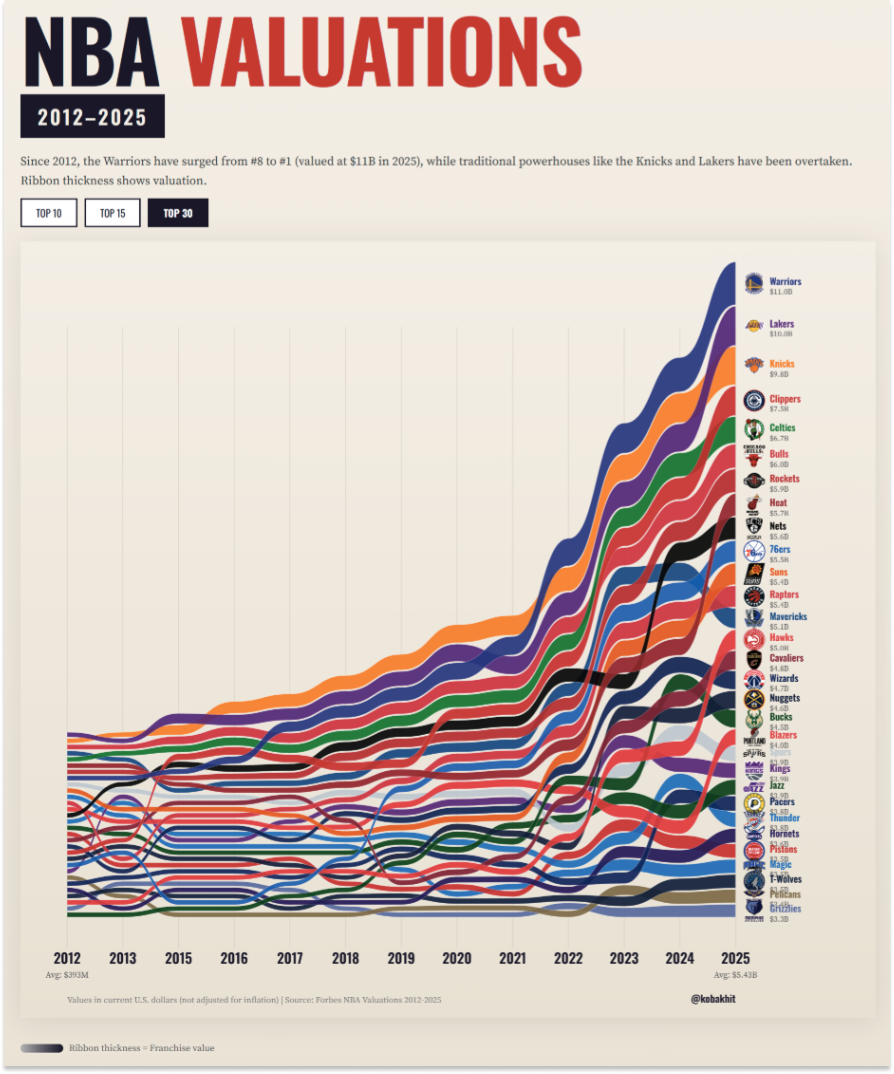

This dynamic not new. All of that concentrated capital has been putting upward pressure on major sports franchise prices for a while. Check out this NBA team value data visualization by Koba Khitalishvili.

It’s interesting to note that even within this small pool, the team that has become the most valuable ($11B) and whose value has increased the most (2,344%) is the one in San Francisco, where top-end wealth has increased the most over the time period.

Per Sportico, the total value of NFL teams grew from $190B to $228B between 2024 and 2025, and perhaps unsurprisingly, the top 10 teams’ value grew 24.3% compared to 17.8% for the bottom 22. There are levels to this, scarcity within scarcity.

I could go on. I will go on. People love wealth porn.

Last year, Vlad Doronin set the Miami-Dade record with the $120 million sale of his Star Island home, pricemogging Ken Griffin’s $107 million 2022 purchase.

That record didn’t last long. In March, Meta CEO Mark Zuckerberg purchased 7 Indian Creek, on the even more exclusive Indian Creek Island, nicknamed “Billionaires’ Bunker,” for $170 million.

Coincidentally, Zuck purchased the home from L.A.-based cosmetic surgeon Dr. Aaron Rollins. I say coincidentally, because in a previous draft of this essay, I wrote “thanks to Instagram-face, full lips and smooth skin aren’t what they used to be.” It is only fitting that someone making previously scarce “beauty” abundant would put the fruits of that commoditization to work in Scarce Assets.

Is $170 million a good price for the neighborhood? How does it comp on a per square foot basis? Who gives a shit? You are asking the wrong questions. $170 million is like one AI researcher. It is less than 0.1% of Zuck’s wealth. It is about one-third of what Zuck and Priscilla committed to create better AI simulations of the human body yesterday, while I was in the middle of writing this paragraph. There is only one Indian Creek Island, and it has only so many lots, especially when you consider how many Jeff Bezos has taken off the market (three).

Take the money from The Everything Store (abundance). Roll it into Indian Creek real estate (scarcity).

And then, of course, there is art. Once used to launder class from Europe to nouveau-riche America, it is now playing the same role in the Gulf.

In November 2025, Gustav Klimt’s Portrait of Elisabeth Lederer sold at Sotheby’s for $236.4 million.

It was the highest price ever paid for modern art at auction, and the second-highest price paid at auction for any art ever after the November 2017 Christie’s sale of Leonardo da Vinci’s Salvator Mundi for $450.3 million.

While both buyers were anonymous and neither has been confirmed, the strong rumor is that Saudi Crown Prince Mohammed bin Salman (MBS) bought Salvator Mundi, and those in the know believe either MBS or Abu Dhabi purchased the Klimt. If the latter, it would reportedly be to anchor the collection at the Frank Gehry-designed Guggenheim Abu Dhabi.

Not just any country gets a Gehry-designed Guggenheim, you know.

Is Portrait of Elisabeth Lederer “worth” $236.4 million? You are missing the point. Who gives a shit? Is it even one of Klimt’s top 10 works? Artnet didn’t think so in January 2025, before the piece came to auction, but who cares. Klimts don’t go up for auction every day, and exchanging abundant dollars for scarce Klimts is a trade you do every day and twice on Sunday.

These things are like some hyperVeblen Goods - not only are they more desirable the higher the price, the high price is the entire point.

I am having a lot of fun writing this and I would love to keep going, but I have the rest of the essay to get to.

Everything we’ve covered so far fits into a bucket I’d call Macro Scarce Assets.

What I mean by that is that if the top-end of the wealth distribution keeps getting richer, the prices of these assets will keep going up. There is global competition for them. The buyers discussed in this section include multi-billionaires from the United States of America, Russia, and the Middle East.

If we want to include Asia, we might throw the $600 million wedding Indian industrialist Mukesh Ambani threw for his son Anant in 2024, the closest thing to the Vanderbilt Costume Ball this decade.

If you have the money and access, and you believe that we are embarking on the Singularity, I recommend that you buy as many Klimts, NFL Franchises, and Yellowstone Club homes as you can get your hands on.

I don’t though, sadly, so I’ve been spending a lot of time thinking about how a little guy like me might participate in the abundance → scarcity trade, and I’ve come to the conclusion that it’s everywhere.

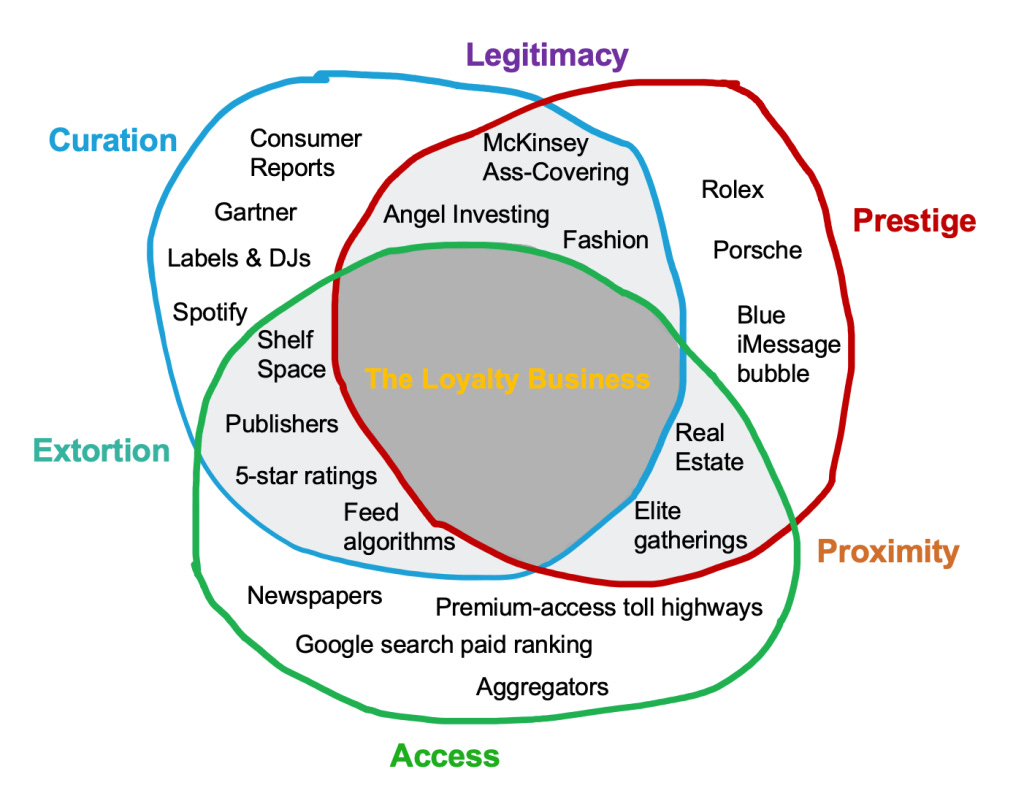

Positional Scarcity

Alex Danco, in one of my favorite essays ever, wrote: “In conditions of abundance, relative position matters a great deal.”

He then grouped the different flavors of positional scarcity into categories:

What we’ve called Macro Scarce Assets mostly fit in the Prestige piece of the chart, including where it overlaps with Access to become Proximity and Curation to become Legitimacy.

Again, the useful way to think about Macro Scarce Assets is that as long as the rich get richer, they will get more valuable. “Relative position” here refers to the relative position of the asset owners versus each other based on the Scarce Assets they are able to accumulate.

But there is a different kind of scarcity that exists in relation to other assets, and moves as those assets’ relative abundance and scarcity changes. These are more specific. They are Micro Scarce Assets.

Like, when the Printing Press makes printed text cheap, handwritten text gets more valuable.

Federico da Montefeltro

In the 15th century, long before the Europeans were reduced to selling either their titles or their scarce things, Federico da Montefeltro, the Duke of Urbino, built one of the world’s greatest libraries.

Close readers will appreciate the century: it’s the same one in which Johannes Gutenberg invented the printing press. If you were a Duke looking to fill a library, I mean, what a gift!

Except that Federico da Montefeltro, the Duke of Urbino, refused to taint his shelves with even a single printed book.

His bookseller Vespasiano da Bisticci wrote, “In this library all the books as superlatively good, and written with the pen, and had there been one printed volume it would have been ashamed in such company. They were beautifully illuminated and written on parchment.”

Printed text became abundant and cheap, which made handwritten works more scarce and valuable.

The Duke attempted to do two things at once: first, as da Bisticci writes, “to do what no one had done for a thousand years or more; that is, to create the finest library since ancient times,” and second, to do it all by hand. “It is now fourteen or more years ago since he began the library,” fawned da Bisticci, “and he always employed, in Urbino, in Florence and in other places, thirty or forty scribes in his service.”

After his death, da Montefeltro’s successor dukes, the della Rovere, continued the handwritten-only tradition. “They continued to collect codices, even to have printed books copied by hand (a Borgesian touch), since only codices could enter this hallowed hall, and by the time the Library went to Rome there were 1,760 volumes.” This detail comes from Roderick Conway Morris’ coverage of the 2007 Federico da Montefeltro and His Library exhibition at the … Morgan Library.

The Morgan Library, which itself holds a Bezosian trio of Gutenberg Bibles, was built on the same impulse to collect the irreproducible in a time of abundance that motivated the Duke, and the same desire to import heritage that drove Mellon, Frick, Vanderbilt, and the other Gilded Age Industrialists. Human nature is remarkably consistent.

The da Montefeltro Library was doing something different than the Morgan Library or the Frick Collection. It was specific. When printing made text abundant and cheap, it made handwritten codices scarce and valuable.

Micro Scarce Assets

Marc Andreessen spent part of his weekend doing what he does best: memeing an idea into the mainstream through repetition. In this case, “When something becomes abundant and cheap, another thing becomes scarce and valuable.”

Macro Scarce Assets are structurally scarce: their supply is fixed or shrinking while global wealth rises. Micro Scarce Assets are relationally scarce: they become valuable because something adjacent becomes abundant. Some things can be both.

If Macro Scarce Assets are like blowing up a balloon, it just keeps getting bigger, then Micro Scarce Assets are like squeezing a balloon, the air has to move from one place to another.

Clayton Christensen nailed the Micro mechanism down most tightly in his Law of Conservation of Attractive Profits. From The Innovator’s Solution via Stratechery: “The law states that when modularity and commoditization cause attractive profits to disappear at one stage in the value chain, the opportunity to earn attractive profits with proprietary products will usually emerge at an adjacent stage.”

When one particular thing becomes abundant and cheap, this other specific thing becomes scarce and valuable.

It is an important lesson to keep in mind, one of those ideas that’s as close to a law of business physics as business gets. This is why Joel Spolsky observed that “Smart companies try to commoditize their products’ complements.” Make the thing next to you more abundant and cheaper, so you become scarcer and more valuable.

As a non-but-aspiring-billionaire, the hunt for potential Micro Scarce Assets is where I spend most of my time. These you can catch before they actually become scarce, when they’re not priced scarce.

This was basically the theme of Power in the Age of Intelligence, the hunt for companies that could use technology to capture a scarce position, expand outward from there, eat the industry, and become Scarce Assets themselves.

Real estate is one of the places this is easiest to see. The supply of land on the Earth is basically fixed, so you’re betting that demand for your particular piece of it will increase, and you can do things to make that happen.

If you’re an individual, you might build a very nice house on your land. If you’re a developer, you might put in shops and restaurants and a walkable Main Street. If you’re Japan’s JR-East, you build trains through and to the land, and then build apartments, hotels, and shops on the land, so that you can physically get more people there and convince them to stay.

If you’re Proto-Town, you buy a bunch of land 30 minutes outside of Austin, make it incredibly fast and easy to build things there, and attract a group of tenants / residents who can also build most of what the town needs, from houses to power.

On Friday, the same day that Thrive announced Eternal and HOF announced Bugatti, Proto-Town had its coming out party with that Core Memory video and a WSJ article. This is Micro Scarcity at work: as capital for hard tech and ideas about what to build become abundant, a place you’re actually allowed to build fast becomes scarce and valuable.

Land near fast-growing cities is structurally scarce, but it is more valuable to a group like Proto-Town than it would be to someone who just wanted to buy and hold, because Proto-Town can add value.

The right Scarce Asset to the right buyer basically has a scarcity-set floor and an abundance-uncapped upside.

Take the Giants purchase.

Assume for a moment that AI researchers like sports, and imagine Thrive letting its portfolio companies use its newly-acquired baseball team to recruit those researchers: owner’s box, batting practice with the team, whatever. All hypothetical. The value of a top-end researcher, as set by Zuck, is somewhere in the hundreds of millions of dollars. How do you price a small edge in recruiting? Or in capital raising? Or, if Thrive is able to beat out a rival firm for a deal on the margin because it owns the Giants, and that deal ends up returning $5 billion, did they basically get paid to own the Giants?

The more uncapped your upside, the more valuable the right Scarce Asset is to you.

If this sounds silly, it was the logic for OpenAI’s acquisition of TBPN for a reported “low hundreds of millions.”

Obviously, OpenAI was not buying TBPN’s $30 million in revenue, because it stopped ads immediately. OpenAI bought a universally-beloved show hosted by two of the most commercially creative people in tech, tech media’s Scarce Asset.

The way Scarce Assets work, I doubt OpenAI had a list of ten tech media platforms with some valuation-math-based number it would pay for each. At 900 million weekly active users, ChatGPT has wider distribution than any media property in the world. What it didn’t have, which TBPN did, was likeability. OpenAI should be willing to pay almost anything for that.

More dumb math: at OpenAI’s $852 billion valuation, a 1% lower chance that the company is regulated out of existence is worth $8.52 billion. A 1% bump in its eventual public market price is worth, give or take, $8.52 billion. If there’s even a 1-3% chance TBPN helps deliver either of those 1% swings, it’s worth low hundreds of millions to OpenAI.

If that sounds silly, consider the Elon Musk Family of Companies.

A few weeks ago, I was walking around Washington Square Park with a friend and we were talking about whether Anduril would suffer the fate of recent tech IPOs like Figma and Navan if and when they go to market. My bet is that it wouldn’t, because it is a Scarce Asset.

Like the asset itself, the equity, is scarce, in a way that most post-IPO tech stocks are not.

There’s this thing I’ve noticed for a while but never put into words or numbers, that startups are incredibly sexy while they’re in the private markets, and then become pretty boring within months of IPO.

This is separate from the idea that the private markets overvalue startups and the public markets look at them clear-eyed and set the rational price. I am talking about an aesthetic thing, the butterflies you get looking at a top startup versus the ick you get looking at the same exact company on the public markets a few months later.

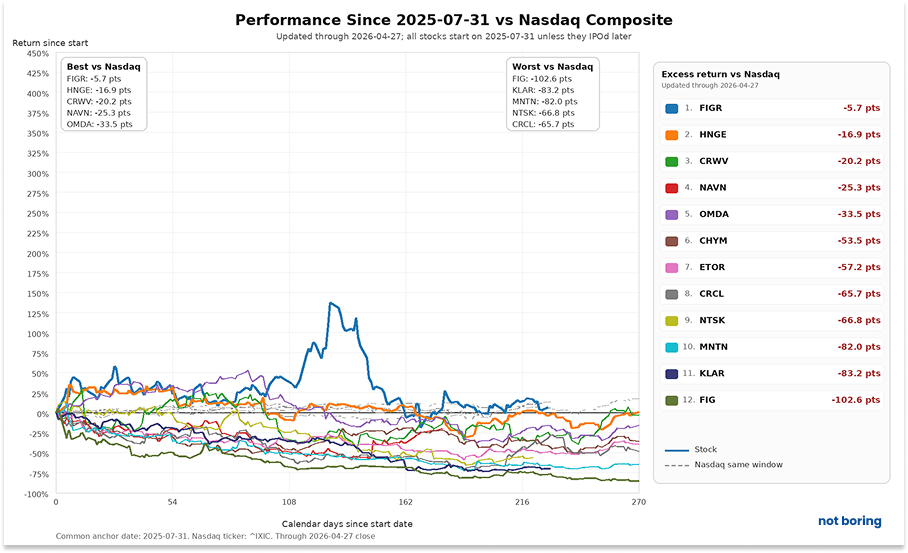

Look at the performance of the US venture-backed non-bio companies that have gone public since 2025. The chart shows their performance versus the Nasdaq Composite since Figma’s IPO day on July 31, 2025. Every single one of them has underperformed the Nasdaq over that period.

And there are a lot of good reasons for that. Maybe these companies were overvalued in the private markets. Maybe they popped too hard at IPO and their prices have floated back to reality. Maybe their earnings lag their narratives. Maybe they’ve gotten caught up in the broader SaaSpocalypse. There are a million potential reasons, but one that I haven’t heard but do believe is that they go from being relatively scarce in the private markets to undifferentiated, as assets, in the public markets.

Like, could you explain what Figure Technologies does that’s different from what Coinbase or Robinhood or eToro does? Given a whole entire universe of stocks you could own, why would you buy Navan in particular? Would you rather own Figma as your bet that software will grow, or would it make more sense to buy the basket of software companies and forget it?

In the private markets, a great startup is sexy. It’s a narrative, a secret, a status symbol, a thing you had to win your way into. Once it goes public, it becomes a ticker sandwiched between thousands of other tickers in your brokerage account, sortable by revenue multiple, gross margin, growth rate, blah blah blah. It will come up as one of 248 of companies in a screener for “software companies with 50%+ margins growing 30%+” or whatever. Even if the company hasn’t changed at all, the asset has.

The asset gets compressed down to the boring stuff. It gets Tickered.

This sounds dumb. I get that. But we are so overwhelmed by the abundance of everything that if something wants our attention, it needs to rip it from us.

I’m not commenting on any of these companies in particular, mind you, just trying to illustrate the point that as public companies with tickers, they feel less differentiated. There are other things you could put in your portfolio that could fill a similar role. There are many ways to bet on software.

If you want to bet on space, though? Well, you’re going to have to buy the SpaceX IPO.

SpaceX the stock is a Scarce Asset because SpaceX the company does something rare and valuable, something that cannot easily be copied (and Elon constantly reminds people of that through his owned platform). The micro-scarce leads to the macro-scarce.

This is why, while those other companies struggle in the public markets, with a combined market cap of ~$125 billion across the twelve of them, SpaceX plans to go public at a market cap between $1.75 trillion and $2 trillion. This, despite the fact that those 12 companies combined to do roughly double SpaceX’s $15 billion in revenue last year.

The scarcity of the business and the scarcity of the asset feed back on each other.

Because the business does something rare, valuable, and defensible, and because Elon Musk knows how to use his platform to make it seem even more rare, valuable, and defensible, investors treat the stock as a Scarce Asset. Because investors treat the stock as a Scarce Asset, the company has a lower cost of capital with which to do things that make it more rare, valuable, and defensible.

And then, because the company is worth more, it can do things that have the potential to make it more valuable in reality, like ~acquiring Cursor for $60 billion. As Kevin Kwok explains, the logic for the deal is tight. It would have been harder to pull off if SpaceX were worth ~10x revenue like the other recently-public companies.

Scarce Assets have outsized value today even relative to the actual economic value their moats provide.

I think Anduril is much closer to a SpaceX than it is to a Navan. To bet on the modernization of defense, you can’t buy the Nasdaq or the DJIA or Boeing. Anduril stock, I argued, will be a Scarce Asset.

After I had that conversation with my friend, Primary’s Jason Shulman tweeted this:

It was cool to see Vertical Integrators called out as its own category, and as I wrote in Part IV of the Vertical Integrator Series, the potential to become scarce from a competitive perspective is why I like them so much: “The biggest advantage may be this: because it’s so difficult, and because the advantages you accumulate by doing a million hard things well form barriers, there will be very little serious competition awaiting on the other side of the Great Filter.”

That also means the winning Vertical Integrators have the potential to be Scarce Assets, meaning that not only will their business benefit from micro-scarcity, but they will be able to more easily attract capital thanks to macro-scarcity.

One of the things that’s interesting about Vertical Integrators is that while they share an overall approach, each one can be a unique and scarce asset. Dandy and Flock, for example, are both Vertical Integrators, but Dandy is attacking the dentistry supply chain and Flock is supplying law enforcement with better data. Each can be a Scarce Asset - the best company in its category, and the best way to bet on that category - in a way that almost no pure software company can.

This is another reason I think more value will accrue to a smaller number of companies that win their category. It’s soft and squishy and irrational, but so are we.

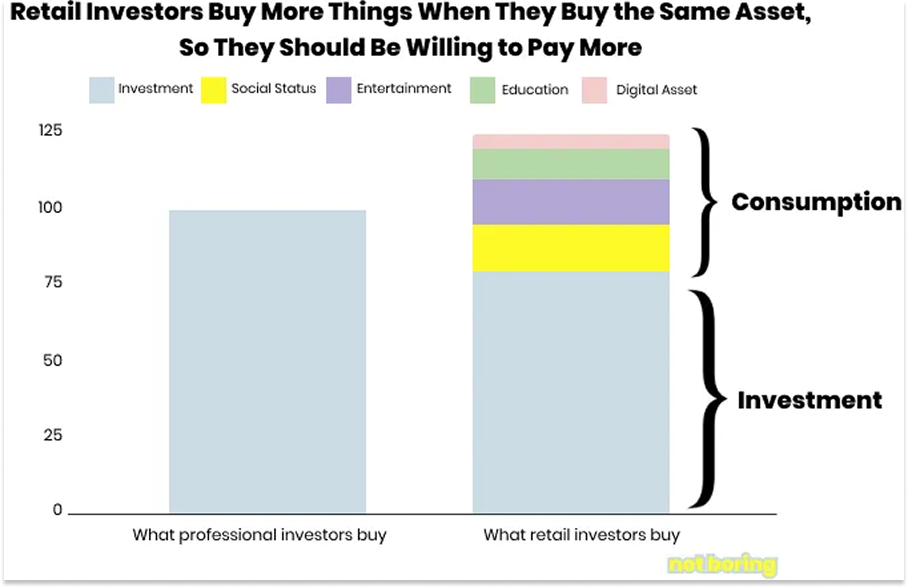

Way back in COVID times, in October 2020, to be precise, when I was sleep deprived with three-week-old Dev, I wrote this piece called Software is Eating the Markets that both holds up and doesn’t. A lot of the specific examples look very COVID in hindsight, but I think the core idea, that retail investors, like angel investors, pay for more than just future cash flows when they buy an asset, holds up.

It may not just be retail investors, either. There is so much demand for certain private companies’ secondaries and so little for others among family offices and institutional allocators that startup shares feel like Veblen Goods: there is more demand the higher the price goes. Check out Setter’s list of “the most sought-after venture-backed companies in the global secondaries market.”

This, I think, is how a market behaves when it views certain companies’ equity as Scarce Assets as opposed to purely financial instruments. If you tell someone at a party that you invested in Anthropic or SpaceX, chances are they will know what you’re talking about and perhaps even think that it’s cool! If you buy them now, even if you aren’t going to make 100x, you’ll get to live through the thrill of an IPO that everyone’s talking about with skin in the game.

People are status-seeking monkeys, Eugene Wei wrote, and still we keep underestimating it. This status-seeking shows up even in things that should be purely spreadsheet-based, like late stage investments, and even in hard-headed industrialists like Henry Clay Frick. We value what is scarce.

As more things that were traditionally scarce become abundant, we’re going to keep seeing this playing out across… everything.

Thanks to GLP-1s, skinny isn’t what it used to be. So what will be scarce when you can take a shot or a pill to look fit? As popular as marathons and fitness competitions have become, I bet they become even more popular. You can’t fake a sub-2 hour marathon.

Thanks to AI, generic knowledge has become free and abundant. Meanwhile, prices for top-end rare physical books have jumped. Per the delightful Rare Book HUB, the cutoff to make the year’s Top 500 sales jumped from $81,250 in 2023 to roughly $120,000 in 2024, while the number of lots selling for more than $1 million rose from 12 to 29. Interestingly, the median price has decreased a bit, while the top got hot.

If we are successful in creating the abundant near-future that has been promised, the competition for Scarce Assets will continue to intensify.

There are some Scarce Assets that only a lot of money can buy, like sports teams and rare art. I bet we will see more tech billionaires, or tech companies, buy F1 teams if and as they become available.

But there are many more to be built than there are to be bought.

Unprecedented abundance will create unprecedented demand for things that cannot be made abundant.

That might mean local things: really unique restaurants, theaters, hotels. It might mean new towns altogether. I have a hunch that drones, EVs, and EVTOLs should expand local frontiers. For an enterprising new settler, it might make sense to start gobbling up cheap, buildable land where it doesn’t currently make much sense, or open up new frontiers beyond the land. You might get it wrong, you probably will. No one said scarce was easy.

It might mean personality-driven media, like TBPN, but it certainly won’t mean something that looks like TBPN. People will always want to outdo other people, but we will also like and trust each other more than we like and trust the machines.

You know what, I’m going to stop listing things.

The scarce and valuable thing you create will not come from someone else’s list.

This is the temptation, and the trap. The trap of this era of abundance will be believing that you can do great things easily, that you can create things other people truly value at the press of a button. You can’t.

All of this sounds so obvious when you write it out that I almost didn’t want to hit publish. More money buy scarce things dur dur. When all same do different har har.

But this is how almost no one is acting. People get the abundance button and they start mashing it, like those rats in that experiment, believing that the thing that is now easy for them is only easy for them, that there are no second-order effects, that the world is a static place. That maybe, hey, just for me, greatness will be easy.

Whoops. The millisecond something becomes easy, the value shoots elsewhere. Scarce is hard and hard is scarce, forever and ever, amen.

That’s all for today. We’ll be back in your inbox tomorrow with another Weekly Dose.

Thanks for reading,

Packy

Outstanding essay!

Arguably the greatest American art collectors in terms of ROI were civil servants: The Vogels. He was a high school dropout working nights as a USPS clerk sorting mail. She was as educated, Bachelor’s and Masters, and worked as a librarian. Their small apartment became a bit of a salon for yet-to-be-discovered modern artists. The Vogels purchased artworks of struggling artists, as well as encouraged them:

https://en.wikipedia.org/wiki/Herbert_and_Dorothy_Vogel

One doesn’t need to be a genius to make exceptional investments/profits in art and rare books. In fact, the ROI with rare books is much greater than stocks or real estate. Rare books and art are far easier and cheaper to maintain/store and insure than real estate.

For the record, the first printing and moveable type occurred sometime in 100-200 AD in China, where paper was invented. The Chinese characters were carved onto wooden blocks, and the ink recipe survived to this day.

Also, I think MBS purchased a painting by one of Leonardo’s apprentices: Salvador Mundi. If one studies Leonardo’s mastery of optics, prisms, water, etc., he would have painted the crystal globe’s see-through images accurately. The crystal globe is much too simplified for Leonardo’s talent and attention to detail. His Last Supper fresco is an example of Leonardo’s mastery of what the eye sees:

https://www.electrummagazine.com/2024/08/leonardos-secret-design-of-the-last-supper/

MBS hired an art expert or two to establish the provenance of Corpus Mundi. But if you pay an art expert enough, he or she is likely to tell a buyer and a seller what he/she wishes to hear.

Recommended reading: The Book: A Cover-to-Cover Exploration of the Most Powerful Object of Our Time, by Keith Houston, W.W. Norton (2016)

Leonardo da Vinci Rediscovered,

by Carmen C. Bambach, Yale University Press

“Four hundred years before Gutenberg, a Chinese commoner named Bi Sheng preempted the German. As told by Shen

Kuo, a contemporary Chinese historian:

During the reign of Qingli 1041-1048 AD), Bi Sheng, a man of unofficial position, made movable type. His method was as follows: he took sticky clay and cut in it characters as thin as the edge of a coin. Each character formed, as it were, a single type. He baked them in the fire to make them hard. He had previously prepared an iron plate and he had covered his plate with a mixture of pine resin, wax, and paper ashes. When he wished to print, he took an iron frame and set it on the iron plate. In this he placed the types, set close together. When the frame was full, the whole made one solid block of type. He then placed it near the fre to warm it. When the paste [at the back] was slightly melted, he took a smooth board and pressed it over the surface, so that the block of type became as even as a whetstone. [...] For each character there were several types, and for certain common characters there were twenty or more types each, in order to be prepared for the repetition of characters on the same page. When the characters were not in use he had them arranged with paper labels, one label for each rhyme-group, and kept them in wooden cases.

This is movable type, almost to its dictionary definition: the printing of a text from symbols on discrete blocks that can be rearranged and reused as necessary. Unfortunately, this passage contains all that is known of Bi Sheng's invention. Did he cut his letters into the surfaces of clay blocks, for example, or did he sculpt them in relief? The Chinese had a tradition of taking rubbings from engravings in stone and another of printing from wooden blocks carved in relief, leaving this most basic question unanswered.

Worse, although Shen Kuos account of Bi Sheng's system has the confident tone of an eyewitness account, no physical evidence survives to corroborate it.” — The Book: A Cover-to-Cover Exploration of the Most Powerful Object of Our Time, Keith Houston

FYI: The chapters about medieval illuminated manuscripts are fascinating (see Book of Kells).