Not Boring Capital: 2 Fund, 2 Boring

Not Boring Capital's $30M Fund II and the Value of Weird Investments

Welcome to the 1,294 newly Not Boring people who have joined us since last Monday! Join 97,780 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts (soon)

This week’s Not Boring is brought to you by… Okay, Computer.

If you like reading Not Boring, you'll love listening to Okay Computer Podcast. Every Wednesday, CNBC Fast Money's Dan Nathan is joined by a murderers row of tech investors, thinkpeople, and operators, Katie Stanton, Rick Heitzmann, Meltem Demirors, Cleo Abram, Sally Shin, Jarrod Dicker, and yours truly, Packy McCormick. We break down the biggest headlines and trends in tech investing, in public and private markets, web2 and web3, and offer our insights into how we are investing our capital. Kind of like today’s post.

This Wednesday, 01 Advisors' Adam Bain, former Twitter COO, and the guy that Kara Swisher recently referred to as "the nicest man in tech" joins his former colleague Katie, Dan, and me to discuss his outlook for 2022 and offer his take on the web2/web3 Twitter wars.

Let’s make this thing bigger than All-In. Join me and the gang by subscribing here:

Hi friends 👋,

Happy Monday! Every quarter, I send an update to the people who invested in Not Boring Capital to update them on the fund’s performance and how I see the market. Yesterday, I sent my third update. I’ve shared each of the first two, and I wanted to share this one, plus a little extra color on VC and getting weird, plus plus an opportunity to invest in Not Boring Capital.

Let’s get to it.

Not Boring Capital: 2 Fund, 2 Boring

Not Boring Capital: 2 Fund, 2 Boring

First things first: Not Boring Capital is back for Fund II, a $30M fund.

The strategy for Fund II is similar to the strategy for Fund I: invest in the best companies across verticals – web2 and web3, bits and atoms – at any stage, with a heavier concentration in earlier stages, and help them tell their stories. Maximize winners, don’t minimize losers. The average check size will just be bigger.

I picked an interesting first year to do VC. While the funding environment seems a little wild – with average valuations across stages at all-time highs, and more companies getting funded than ever before – I firmly believe that the market is a reflection of the massive opportunities still ahead, the huge number of insanely talented people starting companies, and the larger outcomes tech companies are achieving.

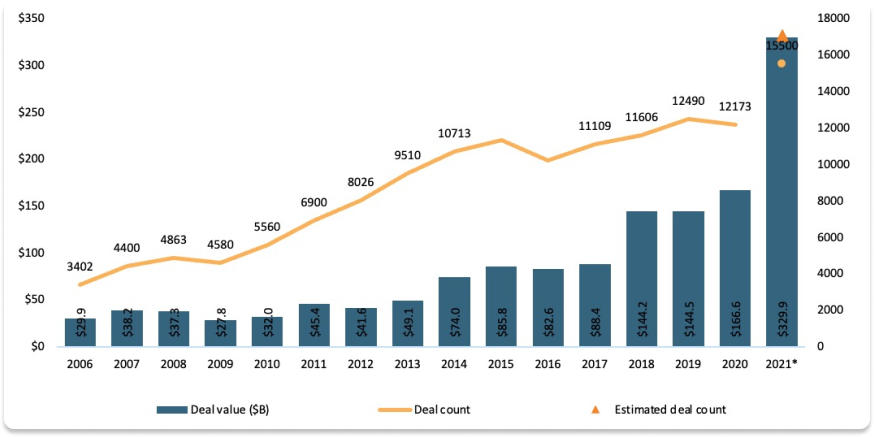

Take this chart, from Pitchbook and NVCA’s Q4 2021 Venture Monitor:

Frothy funding market, huh?

Well, maybe, but that’s not what this chart is showing. That’s actually a chart of exits by year. Total exit value grew 168% from the previous best year ever in 2020 to $774 billion in 2021… and Stripe, Bytedance, and SpaceX haven’t even IPO’d yet.

Venture funding has jumped, too, to $329.9 billion in 2021, but not by nearly as much as exits.

In fact, the 2.3x exit value to deal value ratio is the highest in any year since 2006, except for 2012, the year that Facebook went public. Investors and employees are pulling more money out than they put in by the second-widest margin ever.

Obviously, that might just mean that, fueled by low interest rates and an active money printer, the public markets are behaving as irrationally optimistically as the private ones. As rates rise, like it looks like they might, it will be interesting to see what happens to private valuations and exit opportunities. But you need to play the game on the field.

Some Not Boring Capital funds will invest in bull markets, and I’m sure that others will invest through bear markets. I can’t wait. The long-term thesis – that tech will compound to unimaginable heights – remains the same in any market environment until proven otherwise, and bear market prices will be cheaper.

The trick is staying alive and being able to raise funds in any environment. To that end, I’m incredibly lucky to be backed by many of the same investors as Fund I, including many of you, along with some great new investors. The Not Boring Capital family is growing, and I want more Not Boring people involved.

The SEC imposes limits on that – like the (absurd but unfortunately hard) accredited investor rule and the rule that says you can either raise more than $10M with fewer than 100 Limited Partners (LPs, the people who invest in funds) or raise less than $10M from up to 249 LPs.

For Fund I, we hit the $9.9M cap with 133 LPs - a lot for a small fund, but not as many as I’d like!

After deploying the $9.9M Fund I in six months, I wanted to go bigger for Fund II: more money to invest, and more LPs. So I worked with the one and only Jenn Jordache at AngelList to set up a parallel fund structure – which puts all of the Qualified Purchasers ($5M+ in invested assets) in one fund and leaves more room in the $10M / 249 person fund for accredited investors.

Having that room is really important to me. I’ve asked LPs who wanted to write bigger checks to keep them smaller and turned down introductions to people who aren’t Not Boring readers.

I’ve said it before and I’ll say it again: there wouldn’t be a Not Boring Capital without all of you reading and sharing and giving feedback on Not Boring. So I want you in the fund.

You can read the memo I wrote to raise Fund II here:

The reaction for Fund I was overwhelming, and in case it is for this one too, I don’t think I’ll be able to fit everyone in, but I’ll do my best. As with last time, I’m prioritizing women and minorities traditionally underrepresented on fund cap tables, long-time Not Boring readers, and people who have backed Not Boring Syndicate deals, in that order.

Note: putting your wife’s name and your own email address to qualify as a woman will get you automatically disqualified haha. I didn’t think I’d need to say this, but over a dozen people did it last time. Kind of a Catch-22: you wouldn’t want to let anyone dumb enough to fall for that invest your money, would you?

If you’re interested in participating, and you’re an accredited investor (we need this damn rule to change), you can submit your interest here.

If you’re in, I’ll get back to you ASAP. I likely won’t be able to get back to everyone (there were 750+ submissions last time), but know that I really appreciate the trust and support.

Regardless of how many people we can get in, the other purpose of this email is to pull back the curtain on raising and running a fund.

A couple of years ago, when I worked at a venture-backed startup, I thought there was some magic Venture Capitalist (VC) knowledge that some very smart Stanford people had that the rest of us didn’t or couldn’t possess. I remember waiting for board meetings to let out so we could learn what our VCs thought about our quarter like Moses waiting for god to chisel those tablets.

Turns out, we were all pretty much the same level of idiot. But like any industry, VC has a vocabulary and shared understanding that, once you learn them, demystify the whole thing. Which is why I want to share as much of this journey as possible.

In July, in Introducing Not Boring Capital, I shared the memo that I wrote to raise the fund and my first LP Update.

In October, in Playing Solo Games, I shared my second LP Update and went deep on Not Boring Capital’s strategy as a small solo GP (one person investing the money) fund.

Today, we’ll cover two things:

Not Boring Capital LP Update III. The update that I sent my LPs last night, lightly redacted to keep private company information private.

Pushing Out On the Weirdness Curve. An unintended consequence of Not Boring Capital’s strategy is that I’m able to make weirder, riskier investments.

Without further ado…

Not Boring Capital, LP Update III

Hi Not Boring LPs 👋,

Happy new year and welcome back for Not Boring Capital, LP Update III! There are a lot of familiar faces here, and some new ones – welcome! This update is going out to LPs in both Fund I and Fund II. Not Boring Capital makes the most sense when you think about it as one (hopefully long) line of connected funds.

Let’s kick this update off with some good news, and some bad news.

First, the bad news: we’ve slowed down our pace.

After making 59 investments in Q3, we only made 48 investments out of Fund II in Q4 😉 We invested $8.4 million for an average $175k per investment.

This seems to be about the right pace for Not Boring Capital. As you’ll see below, we’ve been able to keep our bar high while investing bigger checks in more companies, even as we’ve moved our mix a little bit earlier. Over time, I expect the average check to get a little bigger (the committed pipeline for Q1 averages $290k) and the proportion of follow-ons to increase, which will keep the number of new companies in each fund from ballooning too high.

Now the good news: we’ve already had our first Fund II liquidity event!

[REDACTED] $250k [REDACTED]. Our position is currently worth $3.8 million, up 15x for an IRR of around 6.7 billion % (haha, but actually).

Note: I unfortunately can’t share details on this one yet.

This one seems like a weird outlier, and it is, but I think it’s also a really good representation of the fund strategy in action. I’ll explain further below.

December was the most active month in Not Boring Capital’s long and storied nine month history. If this pace holds, we will end up deploying the fund in closer to 9 months than 12 months. Expect the capital call for the second 50% in February.

In today’s update, we’ll cover:

Fund I Review and Update

Fund II Portfolio Stats

Q1 Preview

Let’s get to it.

Fund I Review and Update

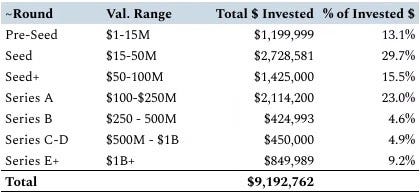

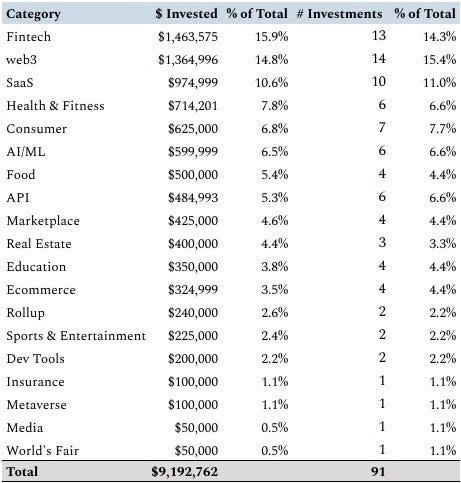

We wrapped up Fund I with 91 investments totaling $9.2M across 89 companies (two follow-ons in Fund I companies out of Fund I).

Note: $9.2M is the full amount invested from a $9.9M fund because of fees.

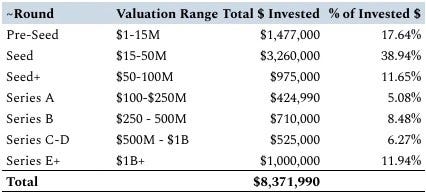

We invested most of our capital on the early side – 43% in companies valued at under $50M – but also put 19% to work in companies valued above $250M. I believe that these will provide a stable base as our riskier earlier investments take time to mature and play out.

In terms of vertical mix, it came right down to the wire, but fintech edged out web3 by dollars invested, while web3 edged out fintech by # of investments.

Ultimately, performance is what matters and returns will decide the winner. Speaking of which…

We only started investing 9 months ago, in April, and the average age of our investments is 5 months, but we’re already starting to see some early results, with ten markups (priced or SAFE) and a token offering (Braintrust). The largest markup is more than 5x higher than we invested just three months ago. Markups aren’t cash in the bank, and the market is hot, but it’s a good start.

Most of these deals haven’t been announced yet, but one has: in November, a16z led a $7M Seed in Party Round.

We’ve also seen our first markdown, but it’s one that I’m actually excited about. After struggling to raise a large round, the founder decided to recapitalize the business and refocus on product and a self-serve GTM motion. I was incredibly impressed with how he handled the whole process, and with the new plan, so we participated in the recap out of Fund II alongside existing investors. Where it shakes out is that we own a larger position in a more focused and re-energized business. More details to come in future updates when this is more public.

Lastly, we have a handful of portfolio companies somewhere between kicking off fundraising and signed term sheets.

Since Fund I is now fully deployed, this will be the last time it gets its own section, and we’ll move to having a markups section that spans funds for future updates.

Fund II Portfolio Stats

As a reminder, Fund II will be a $30M fund running a similar strategy to Fund I but with larger check sizes, more follow-ons as Fund I companies break out, and the benefit of a fund’s worth of wisdom under our belt. Here’s the memo for those who haven’t read it.

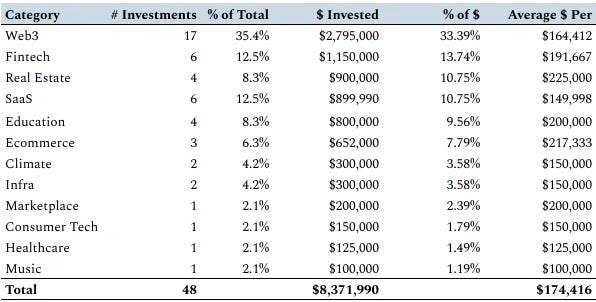

We began committing out of Fund II in early October after fully deploying Fund I, so we have one full quarter under our belt. In Q4 2021, we invested $8.4 million in 48 companies, DAOs, and protocols for an average investment of $175k.

TL;DR: Fund II is trending a little earlier stage and a little more web3 than Fund I. We are getting into deals that we want to get into, and increasingly, getting the larger allocations that we want.

We’ve been aiming to deploy 75% of our dollars in Core investments (each should be able to return the fund), 5-10% in Explore (checks to get to know earlier stage companies), and 15-20% in Growth (later stage companies that collectively should be able to return the fund once). So far, we’re right in line.

We started out with a slightly lower average check size than we’re targeting ($175k instead of a ~$250-$300k average), but our average investment size will increase over the next month. We have invested or committed $4.65M across 16 deals in Q1 2022 (most of which were committed last quarter), for an average of $290k per deal. That’s right in range for the target check size we’re aiming for for the remainder of the fund.

Stage Mix

Our investments continue to shift earlier, with over half (56%) very early, 18% early, and 26% later stage.

Here’s a look at our Fund II investments by stage today:

[Redacted Since Many Rounds Unannounced]

Now that I’m getting my feet under me and honing in on certain verticals where I’m more active and knowledgeable, I expect that we’ll continue to lean a little earlier than we did in Fund I, where both the risk and potential for returns are a little higher.

Vertical Mix

Last quarter, I wrote that, “Web3 will continue to be our biggest category for the remainder of Fund I … and certainly into Fund II.” That has certainly been the case.

Roughly ⅓ of our investments and of our dollars invested have gone into web3 startups, including projects that will decentralize and launch a token.

The fun part about investing in web3 projects is that they often build in public, with the data and progress on display for all to see. Our web3 companies have been on fire.

Instead of writing up all 48 companies – I think like 3 of you read that doc last time – I’m going to steal a page out of Shrug’s book and pick one category to focus on. This quarter, that category is, of course, web3.

web3

If you’ve been reading Not Boring, you’ll know that I’ve spent more and more time writing about web3. I’ve laid out what I think is interesting about the space broadly, and about specific large protocols, but I haven’t discussed why I think the category is compelling from a venture perspective.

It seems like every traditional fund is scrambling to become a “web3 fund.” Some of that is the investment dynamics – getting to liquidity more quickly with a token sale juices IRR. A lot of it is hype and FOMO. Maybe they saw the Uniswap returns in every crypto fund’s fundraising deck and wanted to get some of those.

For me, there are a few particularly exciting parts of web3 venture investing

The talent moving into the space and starting companies is unreal.

Tokenomics are an entirely new toolkit for entrepreneurs to play with.

Composability is magical to watch in real-time (although I’m still figuring out where value accrues and what the moats are for a lot of projects)

web3 re-opens the playing field in very big categories, and creates entirely new ones. I’ll explain, by going over some of the Q4 web3 investments that have been public about their traction.

Take music. If you were to take a traditional approach, there’s almost zero chance of building a very big business when Spotify and Apple exist. Tidal was backed by tons of big name artists and it barely made a dent. But web3 opens up new attack vectors. For example, it can help artists better price songs to fill up the dead space under the demand curve (not everyone values each song at $0.99 or some fraction of $9.99/month), form stronger connections with their biggest fans, and get paid. That’s what Sound is doing.

Sound, which lets musicians sell their songs as NFTs to their biggest fans, has been on fire in its first month. Its 5pm daily drops have become appointment internet, and it sold out its first 21 consecutive drops in under a minute each and paid out over $200k to artists (plus a 10% cut of secondary transactions, which have been very active). It would have taken 60 million streams for the artists to make that much on Spotify or Apple Music.

Sound has done all of this mostly with independent and less-well-known artists. They’re still in “pre-season.” It’s going to start getting very fun when they turn on the jets.

Or take the Metaverse. There’s a version of the future in which Facebook/Meta owns the immersive digital spaces in which we spend our time, or where Roblox grows with its users to become the metaverse of choice. There’s another in which we all create and own our own little pieces of the metaverse. That’s the world that Cyber is building.

Cyber continues to be one of my favorite places on the internet / in the ~*Metaverse*~. The world’s biggest and most visible NFT collectors showcase their collections, and build their digital worlds, with Cyber, and their recent space pods collab with RTFKT (acquired by Nike) was a huge success (the floor for a pod is currently at 0.55 ETH).

Rayan, Cyber’s founder, is based out of Morocco and has strong views about both the art world and the future of digital worlds. For example, he believes that people shouldn’t have to buy digital land from Cyber (it’s false scarcity), but that everything else – from the galleries to the art they display to the music they pipe in – should be NFTs that they own and buy from each other. As people spend more time in Cyber, it should create more demand for Sound.

I highly encourage you to check out some of the galleries from leading collectors like 6529 and Vincent Van Dough here.

Or take APIs. There’s been an interesting debate over the past few days about centralized services in web3, spurred by Signal founder Moxie Marlinspike’s post, My first impressions of web3. My stance is that most people don’t care about total decentralization, but they do want to be able to use many of the web3-native primitives like NFTs and tokens.

ThirdWeb builds APIs and SDKs on top of a new and ever-changing batch of primitives to make it easier for developers to build web3 apps. The pent-up demand was clearly there: it had a wildly successful launch in December, with 4k likes on its announcement tweet and was the #1 Product of the Month on ProductHunt.

While early hype is sometimes useful and sometimes not, seeing the strong pull from the market is important in a category like APIs and SDKs where it pays to get in early and become the entrenched default.

Lastly, take NFTs. As we’ve discussed many times in Not Boring, NFTs have exploded over the past year, with 10s of billions of dollars in volume. OpenSea was just valued above $13 billion. If you think NFTs are just funny, kinda overvalued digital art pieces, that deal alone would make you scratch your head. If you think, like I do, that art is just an easy-to-grasp, and ultimately pretty small, first use case, then there are going to be many, many multi-billion dollar businesses built around NFTs as a new asset class and primitive.

Bridgesplit, started by two genius Duke founders, Luke & Mary, is building a bridge between NFTs and DeFi, letting owners fractionalize their NFTs, create indexes, and borrow against them. That’s a pretty big opportunity with art NFTs, but a hugely important set of tools as more things become backed by NFTs. In just three months, Bridgesplit launched its devnet with over 1,500 fractionalized NFTs, signed exclusive partnerships with top Solana NFT projects including MonkeDAO, and launched a new financial primitive: Curated Indexes.

In the same vein, Abacus is an NFT appraisal protocol that’s generated strong early traction. The crowds have been shockingly accurate at appraising thousands of ETH (millions of dollars) worth of NFTs in its first couple months. In just the past two weeks, they launched Abacus Spot to provide continuous spot appraisals, and appraised these six NFTs:

We are one of the very few – if not the only – fund in the round, which was mostly made up of NFT and crypto whales, because reading Not Boring was one of the things that pushed Medici to drop out of school and go all in on web3. You can listen to the conversation I had with him on Not Boring Founders here.

We’re seeing this more often with web3 startups: people read Not Boring, jump into web3, start companies, and then reach out about investment.

The companies described above are just the ones who have been most public with their progress. We’ve also backed quieter-for-now companies and protocols including [Bunch of Companies Redacted], Parcl, and WYE Media, many of which came in through founders reading and resonating with Not Boring. Each one has big things coming, and I can’t wait to tell you more about them.

Investing in web3 seems consensus now, and prices in many cases reflect that, but there’s opportunity out the weirdness curve for learning, reputation-making, and returns.

Q1 Preview

Which brings us to Q1.

As mentioned, we’re already off to the races in 2022, having invested or committed $4.65M across 16 deals.

We’re taking some big swings in web3, including going deeper on projects that use web3 tools to help solve complex problems.

We’re making our third (and biggest) bet on an Opendoor 2.0 company – housing acquisition with a kicker to smooth demand and increase margins – after Summer and Sunbound in Q4.

We’re going to go deeper into Climate after investments in WattCarbon and Carbon Title. The Chris Sacca episode on 20VC got me fired up. I’m starting to read more (check out Ministry for the Future (realistic, near-future SciFi) and How To Avoid a Climate Disaster (Bill Gates’ plan)). Send recs and companies!

We’ll keep making risky investments, appropriately-sized.

We’ll also begin hiring a team. It’s been fun being truly solo, but we can do a lot more with a few excellent people involved. I’m already beginning to think about what Fund III might look like, and I’m getting excited about the possibilities.

Thanks for coming on this adventure with me. As always, if you have questions or feedback, feel free to reach out, and if you want to invest in Fund II, let me know!

Best,

Packy

Pushing Out on the Weirdness Curve

There’s a theme from the LP Update that I want to expand on here: taking advantage of the unique attributes of the fund to make weirder, riskier investments.

In October, I wrote a long piece about the fund strategy: Playing Solo Games. In it, I wrote a three-part diagnosis to set the stage for the strategy:

Maximize winners > minimize losers.

The rules of the game are different for a small solo fund like Not Boring Capital.

The newsletter is our unfair advantage; I need to protect time to make it good.

The rules of the game are different for a small solo fund like Not Boring Capital. In the piece, I expanded on that, explaining that we don’t lead, we don’t sit on boards, we can piggyback off of larger funds’ resources and diligence, and ultimately, that we’re structurally set up to be able to invest in a lot more of the most credible companies, and therefore, give ourselves a better chance to not miss the biggest winners.

The thing that I missed, that I want to add to the strategy for Fund II, is that Not Boring Capital’s unique attributes also mean that we can get weirder than other funds.

Earlier in this post, I wrote about a deal that turned $250k into $3.8 million in a couple of months. On the surface, the investment seemed like an anomaly, something that would be incredibly hard to replicate. But as I thought about it, the investment was a direct result of the fund strategy.

It was weird. When I told other investors about it, most of them turned it down. If it had gone wrong, I probably would have looked like an idiot. If I were only making 20, or even 50, investments out of the fund, there’s almost no chance I would have done it.

But since we’ll be making around 100 investments per fund, we have more room to get weird and make bets that others might not. We’ll have more investments go to $0 than other funds, but the hope is that we’ll catch more of the companies and projects with outlier upside returns than other funds, too.

We have a lot of advantages as a small, nimble fund with a solo GP and a non-institutional LP base. I talked about a lot of them in the last update. One of the ones I didn’t mention, but that I think is key, is that we can (and should) make riskier, weirder investments than other funds can (even if they should).

That might mean fund investments in silly-seeming DAOs. It might mean more investments in climate. It might mean things with more regulatory risk that most entrepreneurs and investors wouldn’t want to touch.

VCs have gotten a bad rap recently. I think (and I’m obviously biased here) that most of it is undeserved. At its best, VCs funnel resources to the risky projects that no other capital source could or would touch. It’s only when those weird bets pay off that it looks like the VCs were greedy all along.

Bringing up Solana has become an LP Update email tradition, but it’s illustrative here once again. In Solana Summer, I wrote about the challenge that Solana founder Anatoly Yakovenko had raising money in 2017:

It wasn’t obvious back then that this would work. One VC I spoke with showed me a calendar invite for a December 2017 coffee meeting with Anatoly to discuss the project. After the coffee, he passed. There was a lot of competition to be the next big blockchain. This VC told me, “You had Dfinity, Polkadot, Tezos, and Cosmos, all of which had lots of hype and lots of funding.”

Some crypto funds saw the vision and committed, but by the time wires were due, the crypto markets started to crumble. All of Solana’s would-be backers pulled out.

Today, with Solana’s fully diluted market cap sitting at $70 billion, one of the biggest knocks against it is that it’s VC-owned and that the VCs behind Solana are just in it to pump and dump. That’s bullshit. The bet that funds like Race Capital and Multicoin made back in 2018, in the middle of crypto winter and a sea of on-paper-stronger competitors, was so far from a sure thing as to be insanely weird and risky. Without their money, Solana may never have gotten off the ground or developed the thriving ecosystem it is today. They’ve been appropriately rewarded for being weird and right.

Even as the markets democratize, and individuals are often able to invest in web3 projects at the same time and same terms as VCs (which is an incredible development!), there’s still an important role for VCs who are willing to put their research, credibility, resources, and piles of money behind the weird, risky stuff that moves the world forward.

That’s my goal for Fund II: to push further out the weirdness and risk curves than I did in Fund I to help make the wild, amazing stuff happen.

Join me. This is going to be fun.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you next week,

Packy

Hey Packy. Is there a minimum you have in mind for an investment in the fund?

Packy - love this strategy. In many ways it's aligned with Daniel Vassallo's portfolio of small bets - which many VC's 'subscribe to' but rarely execute on as they become too vertically focused and are quick to jump on opportunities when other funds also jump. The fact that you're willing to push the boundaries and get weird is awesome. Look forward to supporting.

Adam

www.adamtank.com