Welcome to the 1,091 newly Not Boring people who have joined us since last Thursday! If you aren’t subscribed, join 44,266 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts

Today’s Not Boring is brought to you by… BlockFi

BlockFi is a new kind of financial institution. With BlockFi, you can use cryptocurrency to earn interest up to 8.6% APY (I’ll explain how below), borrow cash against your crypto holdings, and buy or sell crypto. No minimum balances or hidden fees. Tip: signup is smoother in the mobile app. Set up your BlockFi account today, and get up to $250 in free bitcoin:

Hi friends 👋 ,

Happy Thursday / Tax Day!

Today’s post couldn’t have been timed any better. I’ve been talking to the BlockFi team for a couple of months, and we picked April 15th about a month ago. We didn’t know that Coinbase would be IPO’ing yesterday, or that I’d be so deep down the crypto rabbit hole at this point. It’s fate.

This is a Sponsored Deep Dive on a company I’ve been wanting to dig into for a long time. BlockFi offers up to 8.6% APY on deposits, which is obviously tempting and also confounding. I’ve had so many text conversations with friends that go something like, “I want to do this, but it has to be bullshit, right? How does that even work? We need you to do a Not Boring on this.”

I’m happy to report that it is not bullshit, and I have the receipts to prove it.

Let’s get to it.

Is BlockFi the Future of Finance?

Coinbase IPO’d yesterday to wild success. After touching $420.69 and going as high as $429.54, it closed at $328.28, up 31% from its reference price of $250. It peaked at a market cap of over $100 billion, and closed at $86 billion.

I’m more excited about BlockFi, though, and not because they’re sponsoring this post. It’s a more selfish reason, one that makes the sponsorship money seem like peanuts.

See, if BlockFi existed in 2013 instead of Coinbase, I probably wouldn’t even be writing this newsletter.

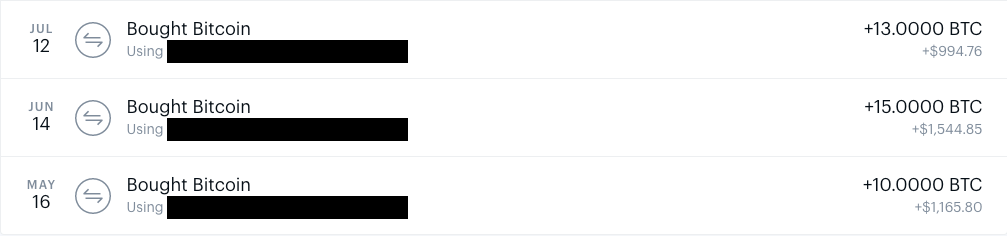

On May 16, 2013, when Coinbase was less than a year old, I set up an account and bought my first bitcoin. I forget why, but I just looked up when Union Square Ventures first invested, and that must have been it:

That was good enough for me. I bought 10 BTC on May 16th, another 15 on June 14th, and another 13 on July 12th.

That September, after quitting my job in finance, I flew my unemployed ass to Oktoberfest for a fun weekend with a few friends. On September 24th, after ten too many steins, I woke up in my Munich hotel room a little hungover and feeling dumb for spending so much on the trip and the night out... and made the stupidest financial decision of my life.

I just sold some of those silly bitcoin I’d bought, and bingo, free Oktoberfest. It felt like such an obviously responsible thing to do that three days later, I sold ten more, then I sold eight in October, five in November, and the last five in May (for a nice little 4x, I might add!).

I sold all 38 bitcoins for a total of $7,232. At current prices, those 38 bitcoins are worth $2,450,050. Gulp.

If BlockFi had been around at the time, I could have taken out a USD loan against some of those bitcoin and earned interest on the rest while they sat safely in my account. If BlockFi paid interest on bitcoin that whole time, like they do today, I’d have more than 40 bitcoin today, or over $2.6 million. Double gulp.

I’ve told you before that I’m an idiot, and I wasn’t kidding. But that’s enough self-chastising for one day. We’re here to talk about BlockFi.

Is BlockFi Legit?

BlockFi, which just announced a $350 million Series D led by Bain Capital Ventures, Pomp Investments, Tiger Global, and partners of DST Global, is building a full-fledged financial institution for crypto investors. BlockFi offers four products to retail investors:

BlockFi Interest Account (at rates up to 8.6% APY)

Trading Accounts

Crypto-Backed Loans

Credit Card

It also acts as a prime broker for institutional clients, with custody, financing, execution, and margin.

BlockFi is building SoFi plus JP Morgan’s prime broker desk, for crypto.

There’s a race going on among everyone in the financial services space -- centralized crypto companies like BlockFi and Coinbase, neobanks like Chime and Monzo, public fintech companies like Square and PayPal/Venmo, and large brokerages and banks -- to become the financial super-app, the place that customers go for loans, credit cards, trading, insurance, cash management, and more. BlockFi has a unique wedge: a growing suite of products that earn clients high interest rates and free crypto.

The first question anyone has when they hear about BlockFi is: “What’s the catch? 8.6% APY sounds too good to be true. That can’t be legit.”

I went DEEP to understand how they do it, and it’s legit. Essentially, BlockFi arbitrages the fact that traditional finance and crypto don’t like to deal with each other.

To understand how it works, we’re going back down the crypto rabbit hole. We’ll cover topics like bitcoin, stablecoins, DeFi, and CeFi, and basis trades. You’ve probably heard the terms, but probably, like me, didn’t fully understand what they mean. We’ll change that. At the very least, we’ll all sound smarter at our next party.

There’s so much to dig into here that it’s hard to know where to start, but we’re going to try:

What Does a Bank Do?

What BlockFi Does

Stablecoins and 8.6% APY

Grayscale Bitcoin Trust

The Race to the Finance Super App

The Offer

After doing the research for this piece, I moved some of my money into stablecoins on BlockFi, and transferred all of my (much, much smaller than 2013) bitcoin holdings to BlockFi from Coinbase. Yesterday, I was on a YouTube livestream with Ben Carlson talking about the Coinbase IPO, and unprompted, he said that he’d done the same.

If you want to check it out for yourself, sign up with the Not Boring link to get up to $250 in free bitcoin when you fund your account.

If you’re still wondering what BlockFi is and how it pulls off such high rates, keep reading. There’s a lot to learn. Let’s start somewhere obvious…

What Does a Bank Do?

Banks make money in three main ways:

Net Interest Margin. Customers deposit money. Banks lend that money out to other people and businesses at a certain rate, pay depositors a lower rate, and keep the difference.

Interchange. When you use a credit or debit card at a store, the store pays your bank and its bank, typically as a percentage of the transaction and a small fixed amount.

Fees. Banks charge customers money when they overdraft, take money out of an ATM, and for all sorts of other things.

For our purposes, Net Interest Margin is the most important. It’s the spread between what banks pay on deposits and what they earn on loans. Let’s do the math on a mortgage as an example.

Right now, the Annual Percentage Yield (APY) on a standard Bank of America bank account is 0.01%. Let’s assume they can lend money to a homebuyer on a 30 year fixed rate mortgage at 3.0%. Bank of America’s Net Interest Margin is 3% - 0.01% = 2.99%.

It’s not that banks want to pay next to nothing on deposits. It’s just that with low rates across the board, banks aren’t able to pay much more and make enough net interest margin to pay for overhead and still generate enough profit to keep shareholders happy. When they could lend money at a higher rate (30-year mortgage rates were 18% in the early ‘80s), savings accounts paid higher rates too.

Banks would love to pay high interest rates on deposits. Banks compete with all of the different things you can do with your money -- buy a house, stocks, or crypto, pay off loans, travel. The higher the interest rate, the more likely you are to keep your money sitting there. More money sitting there means the banks can lend more means higher income for the banks. Given the low rates they earn from borrowers, they just can’t.1

BlockFi, however, can.

Meet BlockFi

Founded by Zac Prince and Flori Marquez in 2017, BlockFi is a crypto-native financial institution. But while BlockFi is for crypto investors, it’s not decentralized. It has over 700 employees, a headquarters in Jersey City, and is regulated. On the spectrum between a traditional financial institution (“TradFi”) and a Decentralized Finance (“DeFi”) protocol, it falls somewhere in the middle. Like Coinbase, it’s what’s known as Centralized Finance (“CeFi”).

To a client, BlockFi looks and feels like an online bank. When I set up my account, it felt very much like setting up a regular online bank account.

I signed up, verified my identity, and waited a day for everything to get approved.

Once I was in, I connected to my bank account via Plaid and deposited money via ACH.

The money hit my account instantly and BlockFi converted it to GUSD (a stablecoin).

Without me doing anything special or crypto-y, it’s now earning 8.6% APY.

With Flex, I chose what currency I get interest paid in. So I deposited in USD, converted automatically to stablecoin, and get 8.6% interest paid out in ETH.

Then, I transferred my BTC from Coinbase. It took about two minutes, and now I’m earning 6% APY on that, in bitcoin. (Rates vary by coin deposited)

Within two days of starting the process, I now have a meaningful amount of my net worth in BlockFi. I wouldn’t recommend it if I didn’t trust it for myself. And it was easy.

That familiar bank feeling with backend crypto superpowers is by design. Early BlockFi clients were crypto natives (they had to be to use a new crypto-based product during crypto winter), but the company is making a push to attract crypto-curious clients, kind of like us. They want to be the on-ramp for millions of people to get involved with crypto.

A couple of interesting things happened in the setup process:

It Felt Like a Regular Bank. BlockFi’s on-ramp to crypto feels smooth and familiar.

Crypto Superpowers. I transferred a good chunk of money from Coinbase to BlockFi in minutes, not the hours or days it would take to send a wire or transfer money between accounts. BlockFi thinks that instant settlement gives it a big advantage over traditional financial institutions.

That combination of ease and power is working.

In early March, BlockFi announced a $350 million Series D that valued the company at $3 billion. Traditional venture/hedge funds Bain Capital Ventures, Tiger Global, and DST Global joined crypto-focused Pomp Investments as co-leads. At the time of the announcement, the company announced some eye-popping stats:

$50 million in monthly revenue, up from $1.5 million a year earlier

$15 billion in assets on the platform, up from $1 billion a year earlier

0% loss rate across its lending portfolio

50% month-over month growth

$50 million per month is an absurd amount of money for a company that’s less than four years old. It would be a great annual revenue number for a company that age. BlockFi generates revenue in three (soon to be four) ways:

BlockFi Interest Account: Earn up to 8.6% APY on stablecoin deposits, 6% on BTC, and 5.25% on ETH.

Trading Accounts: No fee trading of Bitcoin and other cryptocurrencies

Crypto-Backed Loans: Loans on crypto balances as low as 4.5% APR

Credit Card: Visa credit card with 1.5% bitcoin back on every purchase (coming soon)

These look a lot like the ways that banks make money. Let’s break down each, saving the most complex for last.

Trading Accounts

BlockFi lets clients buy and sell cryptocurrencies. The product is similar to Coinbase in that it’s a centralized and easy-to-use way to buy crypto, but there are a couple key differences.

Coinbase Offers More Currencies. Because Coinbase’s business is all about buying and selling crypto, it offers a lot more assets than BlockFi. You can buy nine assets on BlockFi, and 44 on Coinbase. While BlockFi will add more assets over time, it’s not the focus of the business. Trading on BlockFi is really about giving people a way to build up crypto deposits that BlockFi can lend out, and it only offers trading in coins that it lends.

BlockFi Has Lower Fees. Coinbase makes most of its money by charging retail traders fees. Coinbase charges normal accounts 3-4% transaction fees per trade, plus a spread on top. That drops to 0.5% plus a spread for Coinbase Pro accounts. It nets out to a 1.25-1.5% take rate on retail trades. Institutions pay much less, around 0.05%.

In Coinbase and the cryptoeconomy, Tanay Jaipuria wrote:

Over 95% of the revenue that Coinbase generates comes from transaction revenue, i.e., commissions on trades from retail and institutional clients, so let’s focus on that. Digging one level further, Coinbase’s institutional trading volume makes up about 60% of total volume. However, Coinbase makes 95% of its transaction revenue (and 90% of its total revenue) from retail trading volume.

BlockFi does not charge transaction fees, but it does take a spread on trades that averages at around 1%. It’s cheaper than Coinbase, but more expensive than exchanges like Binance and FTX that are more powerful but harder to use, particularly for people new to crypto.

Importantly, like Coinbase, FTX, Binance, Uniswap, and other exchanges, but unlike non-crypto platforms like Robinhood and PayPal, BlockFi lets you move your coins in and out.

At this point, trading is a feature on BlockFi, not a full standalone product. It’s a way to onboard people to crypto and get them earning yield.

Bitcoin Rewards Credit Card

BlockFi is launching a credit card, with Visa, that feels like a regular credit card in every way -- you can use it everywhere -- except that it gives you 1.5% back in Bitcoin whenever you use it, and up to $750 or more in bonus bitcoin rewards.

This one is straightforward. Credit card providers earn an annual fee and interchange, and it’s up to them to use it in a way that attracts customers and strengthens the business. Traditionally, that’s meant points, miles, or cash back. In Ramp’s Double-Unicorn Rounds, I wrote that instead of points:

...it rewards them with better software. Better software drives more usage, which drives more revenue, which drives better software, and so on. The faster the flywheel turns, the further ahead Ramp pulls.

The same principle is at play here. Instead of points or cash back, BlockFi gives people bitcoin. It seems like a minor distinction, but it’s potentially massive, for two reasons.

One, they’re rewards that can increase in value over time. If you’re bullish on bitcoin, then you believe the rewards you earn will be worth more in the future. You’re getting long bitcoin every time you buy anything. (Of course, they can also go down over time).

Two, bitcoin rewards are an on-ramp. There are a lot of people who don’t want to spend their hard-earned cash buying bitcoin, or feel uncomfortable depositing money in an account and trading it for bitcoin. Those same people might be happy to just get free bitcoin for doing something they’d be doing anyway. Once they do, it kicks off BlockFi’s money flywheel:

Earn bitcoin

Bitcoin automatically deposited in BlockFi account, BlockFi lends it out

Client earns 6% on bitcoin holdings in bitcoin, building up the stack

Client can take USD loans against that bitcoin

The bitcoin credit card is an on-ramp, a way to get the next 15 million people to dip their toes in crypto. It’s an on-ramp to BlockFi, too, and likely a low CAC one - who doesn’t want free bitcoin? Once clients are in the ecosystem, BlockFi can monetize them in all sorts of ways as it builds out more financial institution functionality.

Crypto-Backed Loans

There’s this tension in crypto: thousands of people have made millions of dollars by buying and hodling bitcoin, ETH, and other coins. On-chain, they’re very wealthy. But to actually use that wealth to buy things, they need to sell coins. That’s a problem, because selling triggers capital gains taxes in the US, and because most crypto-wealthy believe bitcoin will only keep going up in value over time. Historically, doing anything but hodling has caused major regret.

The internet is littered with cautionary tales. See: my ~$2.5 million Oktoberfest experience, or even more painfully, Bitcoin Pizza. On May 22, 2010, programmer Laszlo Hanyecz bought two pizzas from Papa John’s for 10,000 BTC. At the time, those 10,000 BTC were worth $41. Today, they’d be worth $645 million.

The examples are painful and comical, but it’s a genuine problem: there’s nearly $1.2 trillion in wealth tied up in a currency that people don’t feel comfortable spending.

BlockFi solves that by offering USD loans collateralized by bitcoin at rates as low as 4.5% APR.

BlockFi is able to offer competitive rates while protecting its downside by holding onto your bitcoin (or ETH, Litecoin, or PAXG) as collateral. Loans start at a 50% Loan to Value (LTV), meaning that you need to put up bitcoin that are worth twice as much as you’re borrowing. If you want a $100k loan, you need to put up 3.12 BTC, currently worth $200k.

If the price of bitcoin crashes, that gives BlockFi a 50% cushion. If the price drops below certain thresholds, it will ask borrowers to post more collateral. In the worst case scenario, it can liquidate some of your bitcoin to cover the loan. That said, even in the sharp drawdown in March 2020, it didn’t have to liquidate any clients, while DeFi protocols like Maker did. That’s good, because selling into a massive selloff is typically the worst thing you can do.

This highlights an important and obvious distinction between DeFi and CeFi: CeFi companies have teams of real people who can proactively work with clients to get ahead of issues before getting to the point at which a liquidation needs to occur. Protocols have dashboards and warning signs, but not customer support and risk teams whose job it is to avoid catastrophe.

Everything is a trade-off. DeFi protocols typically have lower fees and are more open and transparent. Many people believe in “not your keys, not your coins,” the idea that if you keep your coins in a centralized account, you don’t really control them. (Balaji made this point in an excellent Tim Ferriss Show interview.) Plus, one person’s comfort in having people on the other side is another’s discomfort in having people on the other side.

For BlockFi’s target customers and institutional partners, though, the trade-off can be worth it. BlockFi has a 0% loss ratio on loans. It’s the lower risk option.

BlockFi Interest Account

Up to this point, everything feels pretty normal: no-fee trading, credit cards with 1.5% back, and collateralized loans at 4.5% APR are things we’re used to. BlockFi just does it all with crypto.

The BlockFi Interest Account is normally where people start to give me quizzical looks, because BlockFi offers up to 8.6% APY on stablecoins and 6% APY on bitcoin. That’s an insanely high rate, and it makes a huge difference. Over 30 years, $100k at 8.6% APY turns into $1,188,214. At the standard 0.01% APY I earn at Bank of America, it turns into $100,300.

Obviously, there is no free lunch, and there is especially no free lunch over thirty years.

The biggest risk with BlockFi is that its accounts are not FDIC insured. If BlockFi gets totally wiped out, your money is gone. There’s a trade-off: for accepting more risk, you earn higher interest.

BlockFi takes that risk very seriously. Watch this video with the company’s Chief Risk Officer Rene van Kesteren, a former Managing Director in Equity Structured Finance at Bank of America Merrill Lynch, to understand how they think about it.

Still… 8.6% is a lot. It beggars belief. I didn’t understand it at all, which is why I wanted to write this piece in the first place, to dive in and see if I could figure it out and explain it. Here goes.

Stablecoins and 8.6% APY

Remember from earlier that banks want to pay high interest rates. It attracts deposits, which enable more lending, which makes more money. A lot of challenger banks will even pay unsustainably high rates on deposits as a customer acquisition cost (CAC) in the form of a bonus rate on top. Those are typically limited to some period of time, like the first six months, after which you go back to earning normal APY.

BlockFi is not a bank (technically, it’s a secured non-bank lender), but it makes money like one. It’s able to offer 8.6% APY on stablecoin deposits and 6% on BTC not as an introductory offer, but because it is able to make a lot more than that on its loans.

According to crypto research and media firm The Block, BlockFi was running a 10% average weighted APR on its retail loans in early 2021. That leaves plenty of room for 8.6% APY on stablecoins, especially when blended with lower rates on other assets.

These rates are not directly tied to crypto prices; most of BlockFi’s life has been during a bear market. They’re based on the availability of arbitrages. Hedge funds can generate high, nearly-riskless returns on certain trades if they can get leverage, and banks won’t make the loans, so funds are happy to pay BlockFi rates that make 8.6% APY accounts possible.

The main arbitrage is something called a basis trade.

A basis trade is the purchase of an underlying asset and the sale of a related derivative, like a future. You make money on a basis trade as the price of the underlying asset and the derivative converge.

In this case, bitcoin futures, which trade on traditional commodities exchanges like the Chicago Mercantile Exchange (CME) or smaller futures exchanges like Deribit, trade at a significant premium to the “spot” price of bitcoin, which is the price that you’d pay if you went into the market right now and bought bitcoin.

When a commodity’s futures price is higher than the spot price, it’s called contango. Typically, contango occurs when investors believe the price of something will be worth more in the future than it is today. In the oil markets, for example, that could happen if people expect a very cold winter in a few months, and want to lock in a price. With normal commodities like oil, you’re OK paying a premium on the futures because owning the futures means you don’t have to take delivery of actual barrels of oil and store them somewhere until the winter.

Bitcoin, of course, costs practically nothing to hold, and yet, at the time of writing, June BTC futures are trading at a 46.4% premium to spot on Deribit.

A hedge fund can buy bitcoins today at $63k and sell an equal amount of futures contracts for $67.5k, sit there while time passes, and collect the difference. Bloomberg’s Joe Weisenthal gives the example of December futures trading on the CME at $63,000 last Friday while Bitcoin was at $58,300. In either case, the ~45% annualized return comes from rolling 3m futures four times per year.

Weisenthal wrote, “What this means is in theory (I stress, *in theory*) you could go long spot bitcoin, while shorting the December future, and if you just wait for the two to converge, that’s an easy 8% in 12 months.” (Note: I think he meant an easy 8% in eight months).

That is (again, in theory) free money, a riskless trade2. Hedge funds love finding riskless trades. They can borrow tons of money, “lever up,” and make way more than 8%. And the 8% number is relatively low. JP Morgan rate derivatives strategist Josh Younger put out a report last Friday saying that the “June CME contract was offering a 25% annualized yield relative to spot.”

Normally, when there’s nearly free money lying around, it doesn’t stick around for too long. It gets “arbitraged away.” In this case, that would mean enough people borrow money to buy bitcoin, and enough people sell the futures contract, that the spread between the two compresses to next to nothing.

But in this case, that’s not really happening, for a couple reasons:

What Institutions Can Buy. Some big, traditional financial institutions can’t really go to Binance or even Coinbase to buy large amounts of bitcoin, but they’re very used to buying commodities futures on the CME, so they buy up futures, bidding up the price.

Who Lends Money for Crypto Trades. Arbitrageurs want to borrow to lever up on the trade in a big way, but banks don’t like to lend money for crypto trades.

That’s BlockFi’s opportunity.

As Matthew Leising wrote in Bloomberg:

Some of the largest non-bank firms in cryptocurrency including BitGo, BlockFi, Galaxy Digital and Genesis are stepping up to meet investor demand for dollars amid a long-standing weariness by banks to lend to individuals or companies associated with Bitcoin and other digital assets. In this case, they’re lending to hedge funds that need cash to buy Bitcoin for a trade that is almost guaranteed to pay out at annualized returns that have recently hit 20% to 40%.

Banks won’t lend to hedge funds on a free money trade because it stinks of crypto, and neither they nor their shareholders want anything to do with crypto (for now). BlockFi, which is crypto-native and understands the market as well as anyone, is more comfortable with the risk and is very willing to lend hedge funds the money for the basis trade at the right price.

Banks won’t lend to BlockFi to turn around and lend to hedge funds to make the basis trade, so where does BlockFi get the money to lend? You guessed it. Deposits. Specifically, stablecoin deposits.

Wait, what are stablecoins?

Stablecoins are cryptocurrencies that peg their value to some external reference, often USD. They allow funds to dollar denominate trades on the blockchain. The best explanation I’ve come across is that stablecoins are just tokenized dollars. In the case of one of the most popular, USD Coin, “tokenizing USD into USDC is a three-step process:

1) A user sends USD to the token issuer's bank account.

2) The issuer uses USDC smart contract to create an equivalent amount of USDC.

3) The newly minted USDC are delivered to the user, while the substituted US dollars are held in reserve.”

Stablecoins are regular dollars that are compatible with the blockchain, and are typically backed by actual dollars in an account. They’re important here because hedge funds need them to make sure the basis trade is actually delta neutral. If the trade is dollar-denominated, meaning prices are all quoted in dollars, they’re not taking currency risk, or a directional bet on where bitcoin ends up.

That’s why BlockFi is able to pay 8.6% on stablecoin deposits. (They automatically turn your USD into stablecoins when you deposit money via ACH). BlockFi lends out stablecoin deposits to hedge funds to lever up on the basis trade. If hedge funds are able to pay BlockFi 15% because they’re making 40%, BlockFi can afford to pay depositors 8.6%.

This trade won’t last forever, and the 8.6% rate will likely come down in the long run, although it’s been stable at 8.6% for many months. A few things may happen to tweak the trade in the short-term:

Demand for bitcoin and bitcoin futures may decline. There is historically high bitcoin demand right now, and if that decreases, there will be less premium on the futures, which means less juice to be arbed.

Bitcoin ETFs. Bitcoin ETFs are coming -- there are three in Canada already. That will have opposing impacts on the trade. On the one hand, it will make it easier to run the trade, which would mean more demand for dollar-denominated loans. On the other, it will decrease the demand for futures, which may tighten the spread and make the trade less profitable. It will be interesting to watch where that nets out.

More Lenders Come Into the Space. Over time, assuming crypto keeps getting bigger and more legitimized, new startups, existing competitors, decentralized protocols, and big banks will all compete to lend money against crypto trades. In a low-rate environment, companies don’t just let other companies take all of the juicy yield for themselves. As the supply of dollars available to run the arb increases, rates come down.

That said, even if the basis trade goes away, BlockFi is still able to earn more than 8.6% by lending out dollars for crypto-backed loans, and there’s still a massive gap between what people want to borrow to buy crypto and what they’re able to borrow:

It will take some time for the basis trade to get arbitraged away, and crypto is still the wild west. New opportunities are popping up all of the time that a crypto-native financial institution like BlockFi is better equipped to understand and move quickly on than traditional ones.

Grayscale Bitcoin Trust

Even today, the basis trade is just one of the things BlockFi does in order to pay out seemingly-too-good-to-be-true rates. The rates aren’t based on any one specific trade, but on BlockFi’s ability to accumulate and lend crypto assets for which there’s more demand than supply. Stablecoins are the most in-demand because they’re needed to dollar denominate all sorts of trades, but BlockFi offers competitive rates on 10 crypto-assets.

Rates are based on how much BlockFi can generate by lending each type of asset out, which is based on supply and demand. Putting one BTC or ETH in if you have them pays out 6%, but it tiers down to a more standard 0.5% from there as you deposit more because there isn’t as much demand to borrow bitcoin or ETH.

While stablecoin rates have remained consistent, bitcoin APY’s on BlockFi have come down recently as the most profitable trade -- Grayscale -- went away.

There are all sorts of reasons someone might want to borrow bitcoin, including shorting (although there’s not much demand for that today outside of hedging), but the biggest was to arb the Grayscale Bitcoin Trust premium to NAV.

The Grayscale Bitcoin Trust (GBTC) is one of the few indirect ways (i.e. not owning bitcoin) for people to get bitcoin exposure. It holds bitcoin in a trust, and then sells shares in the trust in the stock market. Like futures, GBTC traded at a premium to the Net Asset Value (NAV) of bitcoin it held because people could buy it more easily, in ways that they were used to, than bitcoin itself. I can buy shares of GBTC in my Schwab account or 401k. To many, that feels safer, and it comes with tax advantages. (AltoIRA lets you own crypto in your IRA directly, FYI.) As a result, GBTC has traded in a 5% - 30% premium to NAV range over the past couple of years.

Institutions took advantage of that premium. The way GBTC works is that people and institutions can put Bitcoin in the Trust, keep it there for six months, and then get GBTC shares which they could turn around and sell to retail buyers at that 5-30% premium.

Same story: nearly riskeless trade, borrow bitcoin to exploit it, profit. 5-30% premium in six months meant 10-60% annualized returns, boosted by margin.

In order to borrow bitcoin, they turned to BlockFi. BlockFi generated strong yield from the trade, which they gave to depositors in the form of high yields on bitcoin.

Over the past couple of months, though, the GBTC premium turned into a discount as buyers got new ways to get bitcoin exposure indirectly: like Tesla and Square, which hold BTC on the balance sheet, Microstrategy, which holds so much bitcoin on its balance sheet it’s essentially a BTC ETF, and three Canadian Bitcoin ETFs, launched in the past couple months, already have $1.3 billion in assets under management. BlockFi itself launched its own Bitcoin Trust.

More supply for the same indirect bitcoin demand meant lower GBTC prices. With no premium, and a discount in its place, the demand to borrow bitcoin to put in the trust went away. As a result, BlockFi lowered its bitcoin APY.

The Grayscale illustrates two things: that BlockFi’s rates may come down over time, but also that it has a diversified enough business that it’s not reliant on any one trade at a given time. As long as there are new, legitimate trades that investors want to borrow crypto to put on, BlockFi will be able to generate enough yield to pay out above-market interest on deposits.

The question is: can it expand from that wedge into the full suite of financial institution services faster than competitors can get comfortable with crypto?

The Race to Become the Finance Super App

A smooth and familiar interface, crypto-backed loans, and legit high interest rates have propelled BlockFi to dizzying heights in less than four years: $50 million in monthly revenue with $15 billion in deposits and a $3 billion valuation. According to The Block, BlockFi was already profitable entering 2021. But this is just the early stage of BlockFi’s master plan to reimagine what a modern financial institution looks like on crypto rails.

In its report, BlockFi Company Intelligence, The Block wrote:

From one perspective, BlockFi can be viewed as one of the world's largest crypto-native neobanks: part non-bank crypto-secured (collateral) lender, part digital asset depository institution. But even that framing provides an incomplete picture.

What BlockFi is building, according to its CEO Zac Prince, is a lot like a crypto-native SoFi plus the prime brokerage desk of a large bank like JP Morgan.

SoFi started with student loans as its wedge into a young, underserved customer base, and has expanded what it can offer those customers. Today, in addition to student loans, SoFi offers cash management, a credit card, stock and crypto trading, personal loans, home loans, auto loan refinancing, credit tracking, and life insurance. SoFi, which invested in BlockFi’s seed round, recently announced a merger with one of Chamath Palihapitya’s SPACs (IPOE). It’s currently trading around a $13 billion market cap.

Similarly, BlockFi started with crypto loans as its wedge to attract a wave of newly wealthy crypto investors who were underserved by the market to make deposits. They’ve added no-fee trading and a credit card, and will continue to roll out new product lines. It’s not hard to imagine cash management, stock trading, wealth management, mortgages, and all of the financial services that crypto holders might need, all built on crypto rails.

Now, it’s trying to expand its addressable market by building more on-ramps that make it easy for crypto curious people to get involved in the space. An 8.6% APY is one way to pique peoples’ interest, but credit cards and other products that let people easily earn and grow their crypto holdings without feeling like they’re dealing with crypto will unlock new client bases.

But the race is on.

As a public company with an $86 billion market cap, Coinbase is undoubtedly going to expand its offering to try to infiltrate more of its customers’ financial lives. It already launched bitcoin-backed loans last August.

DeFi is still confusing and hard to use, but it’s improving rapidly and attracting more people beyond the hardcore crypto community. Projects like Aave and Compound offer lower fees and more decentralization than BlockFi.

Non-crypto companies like Square, Fidelity, Monzo, Robinhood, Mastercard, PayPal/Venmo, and even SoFi are moving into BlockFi’s space:

Square said 1 million customers bought Bitcoin in January, and it holds over 3,000 bitcoin on its balance sheet

Robinhood said that 9.5 million people traded crypto on its app in Q1

PayPal lets customers buy, sell, and hold crypto

PayPal’s Venmo will let people pay each other in crypto

Mastercard is supporting crypto on its network

Visa built a crypto API that it’s piloting with neobanks.

The list goes on, and new runners are entering the race every day. Many of these companies have more robust financial services offerings than BlockFi, and are betting that adding crypto into the mix is enough to retain existing users and attract some new ones.

BlockFi’s bet is that crypto, or at least digital currency, is just better than the existing financial system in a lot of ways that have nothing to do with decentralization, and that CeFi, which combines the benefits of centralization and digital money, is the winning combo.

Software is eating the world, and at some point, they think crypto will eat the way we store and exchange money by building money directly into the infrastructure itself.

If that turns out to be wrong, or in a more extreme case, if bitcoin crashes and BlockFi’s clients and counterparties explode, BlockFi could struggle, and there’s no FDIC to back up its deposits.

But if that’s true, if crypto is fundamental to building better financial products, then BlockFi’s wedge and singular focus on crypto will be an advantage versus incumbents and startups that try to add it on after the fact. Robinhood, for example, doesn’t even let users transfer crypto outside of the app. If people accept that money moves more easily and equitably on crypto rails, bolt-on solutions built for speculation won’t cut it.

If they’re right, and CeFi wins, the battle may end up being BlockFi vs. Coinbase. BlockFi board member Anthony “Pomp” Pompliano believes that BlockFi’s decision to start with deposits gives it a clearer path to product expansion, drawing on Robinhood vs. Square:

Robinhood remains a brokerage-focused business. They have tried to scale by adding new products (crypto trading, cash accounts, etc), but that appears to be a much more difficult road than originally anticipated. Square on the other hand has been able to build a serious ecosystem of products that includes payment infrastructure, point-of-sale technology, CashApp, Bitcoin brokerage, and fractional share brokerage for public equities.

The not-so-subtle implication is that Coinbase is Robinhood and BlockFi is Square, and that BlockFi can build Coinbase before Coinbase can build BlockFi.

Coinbase’s IPO just adds fuel to the fire. More companies will enter the space. Spreads will get arbitraged away. Yields will compress.

8.6% APY won’t last forever, but if BlockFi can build a robust suite of financial services with crypto tools for an expanding base of crypto owners, it has a shot at building a lasting institution in a competitive and lucrative space.

The Offer

BlockFi is offering Not Boring readers up to $250 in free bitcoin for opening up and funding an account. I did it myself, and it was smooth and easy. That said, do your own diligence, read reviews. You probably shouldn’t put all of your money in BlockFi. I put less than 10%.

If you own crypto and want to earn on or borrow against your holdings, or if you’re just curious and want the easiest on-ramp to earning and growing your crypto holdings, check it out:

Thanks to Dan for editing, and to the BlockFi team - Russell, Chris, and Shayne.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading, and see you on Thursday for a special edition.

Packy

Couple of reasons why banks rates are low: 1. Front end rates are anchored by the fed funds rate which is 0.25-0.5% now. Deposits from retail clients are basically overnight unsecured lending to the bank which is why they’re near 0%; 2) Liquidity trap from years of low interest rates. Borrowers are not borrowing not because they don’t want to but because they already are saddled with debt. Corp debt is high, consumer debt is high. There is just no more room to borrow more.

Theoretically not free money. You could lose money on a long spot vs short 3m futures trade if the contango steepens, which tends to happen in a bull market. "Delta neutral" is more accurate. If you’re going to put on this trade, I trust that you’ll do your own research.