Techbio Taxonomy

A guest post by Elliot Hershberg on 4 forces behind the shift from biotech ➡️ techbio

Welcome to the 1,524 newly Not Boring people who have joined us since last Monday! If you haven’t subscribed, join 146,991 smart, curious folks by subscribing here:

Today’s post is brought to you by … Cromatic

The biotech industry is evolving. Launching a new startup has become less capital intensive. A new generation of founders are building nimble teams, and outsourcing portions of their R&D to stay lean and focus on core scientific competencies.

Outsourcing can come with headaches. It can be challenging to decide on the right vendor, compare prices, and track project progress. While contract research organizations (CROs) are an important part of the modern biotech ecosystem, these partnerships come at a cost.

Cromatic is on a mission to help modern biotechs make the most out of outsourcing. Their vision is to develop the infrastructure necessary to make contract management a painless, daresay enjoyable, experience. Cromatic makes outsourcing easier than ever so you can focus on the science.

Cromatic is currently performing outsourcing searches for early stage biotech companies for free. Learn more here.

Hi friends 👋,

Happy Monday! Hope you’re enjoying a relaxing August. I’d like to briefly interrupt your summer holiday to let Elliot Hershberg introduce you to the future.

You met Elliot before when he wrote about Ginkgo Bioworks. While he’s not pursuing his Ph.D. in Genomics at Stanford, Elliot works with us at Not Boring Capital to discover and invest in the sci-fi-adjacent companies pushing the frontiers of biology.

Why invest in biotech, you ask? You’re not alone. One of the most frequent questions I get from LPs and potential LPs is why in the world Not Boring Capital would invest in biotech. Historically, biotech has been a very specific and separate discipline from traditional venture investing. Getting a therapeutic to market is risky at best, and even if it works, it’s incredibly cash consumptive. A small fund investing in early stage biotech is bound to be diluted to smithereens by exit time.

But Elliot’s thesis, of which I’ve become convinced over many conversations with both him and founders building in the space, is that there’s an enormous shift afoot in which biotech companies are beginning to look a lot like software companies did a decade or so ago, propelled by forces akin to the rise of AWS, founder-friendliness, and a growing ecosystem of primitives with which to build. Founders are getting closer and closer to programming atoms like software engineers program bits. The capital, and team size, needed to start and scale these businesses is declining. Multi-billion dollar outcomes and 100x returns are becoming more frequent.

The shift is so big that the category needs a new name: from biotech to techbio.

In today’s piece, Elliot synthesizes years of knowledge into a compact techbio taxonomy and describes four key shifts that are unleashing a wave of entrepreneurial energy on one of the biggest opportunities available to humanity: “tapping into the awesome power of biological growth.”

BTW, if you don’t already, you need to subscribe to Elliot’s newsletter, The Century of Biology. There’s so much exciting work being done in techbio, and there’s no better guide than a triple-threat researcher, investor, writer.

Let’s get to it.

Techbio Taxonomy

An Elliot Hershberg Guest Post for Not Boring

Sometimes new words and terminology are necessary before we can fully internalize the change taking place around us.

We needed the notion of the World Wide Web before we could truly capitalize on the promise of a global network of computers. Today, Web3 is a term that encompasses a broad set of ideas about where the Internet should go next.

An important transition is also taking place in the world of biotech. From the headline news of Google DeepMind solving protein structure prediction, to the recent completion of the human genome, the frontier of biology has become deeply integrated with AI, software, and hardware. The new generation of hybrid companies on the cutting edge of this trend are often referred to as techbio companies.1

This new intersection between bits and atoms is a really big deal. In a world where the cost of developing new drugs is increasing exponentially and healthcare takes up an unsustainable portion of our GDP, something needs to change. Beyond developing more medicines cheaper and faster, techbio could help us live longer and healthier lives in material abundance made possible through the biologization of our industrial processes.

But what actually is a techbio company? What are the defining characteristics of this new category? Here, I will attempt to contribute to the challenging and highly imperfect science of taxonomy by answering this question. With new words and terms, there needs to also be a shared understanding of what they mean.

As the first generation of techbio companies mature and the ecosystem evolves, patterns are beginning to emerge. The techbio companies of tomorrow will likely be:

Founder-led 🧑🔬🥼

Deeply integrated 🧬🖥️

Backed by new services 🔬🧪

Massive 💰🚀

It’s time to unpack each of these components. Let’s jump in! 🧬

Founder-led 🧑🔬🥼

In the world of tech, a movement focusing on “founder-led startups” would seem redundant and obvious. Of course founders lead startups, who else would? However, this wasn’t always the case. In the era before nearly all VCs touted themselves as “founder friendly” there was a very different approach to company creation and management.

Well before the existence of the YC library, AngelList, and other resources that underpin the modern startup ecosystem, VC looked very different from what it is today. In 1972, just one year after the term “Silicon Valley” was coined, Kleiner, Perkins, Caufield & Byers became the world’s largest venture capital partnership after raising an $8 million dollar fund. This new fund was born directly out of two of the most important companies in Silicon Valley history.

Gene Kleiner was one of the iconic Traitorous Eight employees who decided to leave the Shockley Semiconductor Laboratory to found Fairchild Semiconductor. His new partner Tom Perkins had learned directly from David Packard at HP. When they joined forces to start a fund, venture capital was still a nascent practice. There was no such thing as deal flow for VCs. According to Kleiner, “We just didn’t wait around for deals to come to us. You had to create the deals to be really successful.”

In practice, this meant partnering with university professors or entrepreneurs from existing large companies, and taking active management positions in the new ventures. An example of this is Tandem Computers, one of the fund’s early wins. The company sold fault-tolerant computer systems. The CEO was Jimmy Treybig, a former HP colleague. Tom Perkins served as the chairman of the company from when it was founded until a merger over 20 years later.

Obviously, a lot has changed in the 50 years since Kleiner Perkins first opened its doors on Sand Hill Road. The computer industry has exploded, giving birth to the software industry and the Web. With each generation, founders have gotten younger and companies have become more massive. While the first founders of Kleiner Perkins portfolio companies were former colleagues with deep roots in the early computer industry, the list now includes Larry Page and Sergey Brin, the brilliant young computer scientists who dropped out of their PhDs at Stanford to found Google.

The trend hasn’t stopped there. A more recent Kleiner Perkins investment is Figma, the popular design tool that Packaso McCormick uses to make graphics for Not Boring. They have delivered on their early vision of building a tool that would “allow users to creatively express themselves online.” Figma was founded by Dylan Field and Evan Wallace who met while undergrads at Brown. Dylan was awarded the Thiel Fellowship to drop out of college and work on Figma full time. A 2013 TechCrunch article covering Figma’s $3.8 million seed round summed it up nicely saying, “Children are our future, and VCs are giving them the cash to make it happen.”

A lot had to happen for tech to reach this stage. Computers had to become substantially cheaper, faster, and more widespread. An enormous amount of engineering had to happen to make computer science more accessible and standardized. Programming languages had to evolve to more closely approximate natural language, encapsulating lower level details with clever abstractions. Modern browsers are so complex that even brilliant programmers like John Carmack struggle to keep track of all of the steps involved in rendering the text you’re reading now. But browsers have a crucial property: they provide a nearly universal platform that can be used to build new platforms. The browser was the core platform that enabled two brilliant young people to launch a company providing a new platform for creative expression. It took several layers of platforms to launch The Great Online Game.

In most cases, biotech company creation looks nothing like the current paradigm in tech. Current biotech venture capital much more closely resembles the state of affairs 50 years ago when Kleiner Perkins was founded. The first generation of specialist biotech investors followed a similar playbook to the Tandem Computers days. The process involved identifying promising science from academic labs and building out a management team to commercialize it, with venture capitalists often taking an active role.

More recently, this process has been systematized by venture creation funds and companies. Some of the funds most commonly associated with this strategy are Atlas, Third Rock, and Flagship, which are all based in the Boston area. While there is variability in the mechanics between these types of funds, the core practice is the same: new companies are internally ideated, financed, and incubated within the walls of VC funds.

There are two major challenges associated with this model:

It has struggled to scale

Ownership and decision making is often delegated away from scientists

While the Web startup ecosystem has rapidly expanded, company creation in biotech has actually slowed down:

Part of this trend can be explained by the fixed scaling properties of venture creation. Any given fund can only build a finite number of new companies at a given time. It’s only possible for one fund to do the scientific ideation and team building involved in their process for a very small number of companies each year. This number can actually go down as partners saturate the number of board seats and operating roles that they can reasonably hold. Simply put, this model doesn’t have the intrinsic network effects of the Silicon Valley tech ecosystem.

The second crucial drawback is that scientists and engineers—the crucial value generators in high-tech innovation—aren’t in charge of their destiny. In tech, founders are in control of their cap table. YC companies are coached to only sell a small fraction of their company to investors early on. In biotech venture creation, VC funds take the lion’s share of equity from the start. It can be a bit like the difficult negotiation in Bad Santa, where Willie and Marcus end up giving half of their profits away to their new business partner Gin.

But the numbers can actually be even more dramatic. We’re not talking about giving up half of the equity, we’re talking about a scenario where key founding scientists can receive single digit equity percentages, if they even receive any equity at all. In a world where their work can create billions of dollars of value, many biotechnologists are capturing miniscule fractions of these returns.

The problem here isn’t just financial. Ownership has an important consequence: control over the direction of a company. A central component of venture creation is the process of building out a management team of executives who have experience bringing drugs to market. This means that scientists and engineers often don’t steer the trajectory of new companies. Leave it to the professionals! While this can be effective for executing within an existing paradigm, it doesn’t forge new ones. Google and Facebook weren’t built by former IBM executives, they were built by young programmers exploring totally different approaches to technology development and company culture. In the aftermath, we now have an existence proof for the fact that young engineers can build and lead massive generational companies.

Things are starting to change. While biotech has traditionally been the realm of only specialist investors, tech VCs have made a serious entry. These investors have brought some of the dynamics of tech entrepreneurship with them. Since making their first biotech investment in Ginkgo Bioworks (read more about that story here), YC now funds more biotech startups each year than any other investor—giving scientists a totally different option compared to the venture creation route. The software powerhouse a16z has raised several massive biotech funds, and their partners have been vocal proponents of giving scientists the reins to their own companies.

This trend is often referred to as the founder-led biotech movement.

Founder-led companies are beginning to make a real mark on the industry. The investor Tony Kulesa framed this beautifully in a recent essay, saying:

“In the past 12 months, Ginkgo Bioworks, Recursion Pharmaceuticals, AbCellera, Finch Therapeutics, SQZ Biotech — all founded and led by technical founders fresh from their academic roots — have gone public. Hot on their heels, founder-led startups at the Series A and beyond like Asimov, Biobot Analytics, Cellino, Dyno Therapeutics, GRO Biosciences, PathAI, Strand Therapeutics, Vedanta, 1910 Genetics, and many others, have raised hundreds of millions of venture capital to work on some of the most innovative frontiers in the industry. The founders of these companies are hungry and creative scientists that realized the impact of their work before others did, and now they are leading the charge to bring their innovations to the world.”

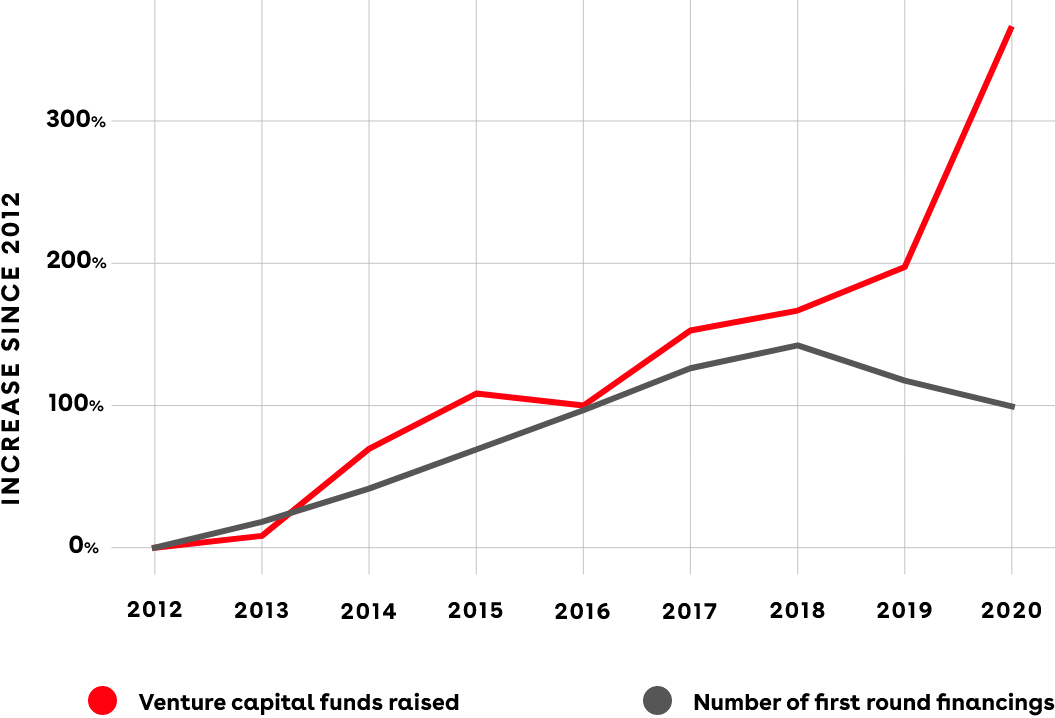

This general shift in the biotech VC ecosystem isn’t limited to just a smaller subset of anomalous companies. As the blood bath in public markets has dropped the number of biotech IPOs, emerging techbio funds have actually overtaken more traditional biotech funds at the Series A stage:

Beyond seed and series A investments, late-stage investors have also signaled a willingness to finance founder-led biotechs. Over time, this pipeline should only become more robust as some of the companies become massively successful. All of these changes have the potential to open the floodgates for a techbio revolution where company creation is accelerated, capital is more evenly distributed across more companies, and scientists are able to bring incredible new technologies out of their labs and into the market with less friction.

Here, the key take home message is that one central component of techbio actually has nothing to do with AI, software, or robots: one of the major changes is the adoption of the tech investment and company creation model where founders are at the helm.

Deeply integrated 🧬🖥️

So, what types of technologies and companies are inspiring tech investors to jump into biotech?

When people say biotech, what they normally mean is drug discovery. Startups developing drugs make up the overwhelming majority of the industry. Drug discovery companies primarily come in two flavors: asset-centric companies and platform companies. Asset-centric companies are incorporated with specific initial intellectual property (IP) for a new therapy, and focus on testing and selling that IP. Platform companies focus on a technological approach or system that should enable them to make multiple new drugs.

Many people use the term techbio to refer to platform companies, especially ones focused on using computational biology or AI-first biology approaches to make new drugs. An example of this type of company is Recursion Pharmaceuticals, which is building a massive automated lab to generate enormous amounts of molecular and imaging data to feed into AI algorithms with the goal of building maps of biology that can lead to the development of new drugs. One of the core parts of the platform is a machine vision system that automatically labels and analyzes the morphology of cells:

Okay…

Tech 🖥️✅

Bio 🔬✅

For a lot of people, these tech-enabled drug discovery platforms have become synonymous with techbio. I think that this misses the forest for the trees. While it’s true that several of the first techbio companies such as Recursion have been platform plays, the general strategy isn’t what makes techbio special.

The platform approach to drug discovery isn’t a new category defining business model that needs to be explored and then derisked by tech investors. The more traditional biotech venture creation funds actually love platform companies, and sometimes exclusively focus on this type of business model and company. These types of funds have actually delivered some of the best return profiles in all of VC by taking this focus. The Column Group, which invests in a “select group of early stage drug discovery companies with unique scientific platforms” had a 397% IRR—this is not a typo—between 2007 and 2015. This type of business model is certainly an opportunity for new cutting-edge tech to make an impact, but it isn’t the whole story.

So if platforms aren’t the special secret sauce of techbio companies, what is? I think that platforms are one example of a broader trend that I’ve come to think of as deep integration.

To reach the point of sophistication that we see now in tech, a large number of individual pieces had to be independently developed before being integrated together. Before arriving at the iPhone, we had to go from vacuum tubes to semiconductor manufactured transistors, invent haptics, develop software operating systems for mobile devices, figure out how to make wireless network protocols, lay cables across the ocean to establish a global computer network with which to connect for real-time information, and much, much more. For a long time, the state of the art in biotech has been individual molecules that we use as therapeutics, which we characterize using tools from molecular biology and lots of mice. Now, the process of mixing and matching molecular technologies and combining them with software and hardware into deeply integrated products is beginning. In this process, techbio companies are born.

I’ve been trying to understand this general process for a while. As I’ve worked in the field of genomics—a 21st century scientific discipline that combines molecular biology, computer science, and statistics—I’ve tried to build models of these compounding and intersecting areas of innovation. An example of this is the Sequencing, Synthesis, Scale, and Software model that I’ve written about which can be useful to understand how some of the major biotech breakthroughs are being combined in powerful ways. While I find it a useful model, it doesn’t exactly roll off the tongue and can be easy to forget. Because of this, I’ve tried to ask myself: what’s really going on here? What is the core underlying dynamic at work? I’ve come to view this technology stack as one example of the deep integration that is characteristic of modern techbio companies.

Let’s make this more concrete with an example of a company that’s delivered a lot of value using this tech stack. Color Health is a vertically integrated approach to delivering affordable molecular and genetic tests at scale. Color’s origin story is really interesting. One of the founders, Othman Laraki, had a troubling history of breast cancer. To better understand his own cancer risk profile, Othman decided to get genetic tests for BRCA mutations—which can lead to an increased likelihood of developing cancer.

While it is a straightforward test based on known genetics, Othman was blown away by the difficulty associated with getting his results. He had to take several trips to the Stanford academic medical center and spend thousands of dollars. As a tech entrepreneur who had sold a company to Twitter, he saw a massive opportunity. He teamed up with his previous co-founder Elad Gil (yes, that Elad Gil), a physician named Taylor Sittler, and an engineer named Nish Bhat to found Color. (side note: Nish is now a VC focused on the intersection of engineering and biology—founders in this space should check him out!)

In light of a Supreme Court ruling that lifted patent protection over genetic tests, Color set out with a tangible goal: to dramatically reduce the cost and difficulty associated with BRCA testing. To do this, they built a deeply integrated tech stack that combined DNA sequencing, software infrastructure, and process engineering:

They brought the cost of a BRCA test down from $4,000 to $250. After starting with this minimum viable product, they scaled and expanded their business outwards in an effort to offer all molecular tests in an affordable and reliable way. I’ve personally benefited from their rapid delivery of COVID test results during the pandemic. As they’ve scaled their services, Color recently raised $100M at a $4.6B valuation.

This type of story is why I think that the term techbio has value. It is meaningfully different from the traditional biotech venture creation approach. A small team of interdisciplinary founders identified a market opportunity and iterated quickly to build out an MVP. Their test was so affordable that they could sell directly to consumers, often circumventing the complexities of insurance and healthcare delivery. They raised capital from tech VC funds as they scaled, who were more receptive to their backgrounds and the substantial software involved in the product.

I highly doubt that it is possible for venture creation funds to build a business like Color. It requires a special type of entrepreneur in the driver’s seat, software and product expertise, and a mode of operation foreign to biotech VCs.

This isn’t just a one-off example. Just for this one specific combination of technologies—DNA sequencing and software—enough progress has been made in recent years that there is a huge opportunity to build a large number of massive and enduring companies. Even if we still consider just diagnostics, another unicorn is Guardant Health, which sequences DNA present in the blood and analyzes it to detect cancer at the earliest stages. Basically, it’s like Theranos, except it actually works! (This tech is extremely cool, if you’re curious you should check out a post I wrote about recent advances in this space here.)

Once you also consider recent advances in DNA synthesis and machine learning, the combinatorial space of intertwining threads starts to get really crazy. This is how you end with a company like Dyno Therapeutics that is using AI to design viruses with more optimal properties for delivering gene therapies, or Atomic AI that is using a model that resembles AlphaFold for RNA to develop new RNA therapeutics.

With a new generation of founders and investors, we are seeing a convergence of molecular and digital technologies into systems that are starting to rival the complexity and integration of the iPhone.

All of the examples that I’ve mentioned so far have been built on top of a foundation that took an enormous amount of science and engineering to create. From compounding breakthroughs in molecular technologies, to major advances in bioinformatic analysis, to modern machine learning and the hardware that it requires, there is a new level of complexity present in modern deeply integrated techbio companies.

While these new approaches are really exciting, company building isn’t just an academic or scientific exercise. Companies have to generate real and enduring value to be successful. As Chris Dixon has argued, startups need to go full stack to fully deliver on the promise of their new technology in existing industries. Tesla is an incredible example of this, having built an entire car company instead of a battery supplier for incumbent car manufacturers. This certainly also applies to deep tech.

There are many possible products and business models for cutting-edge techbio companies. There is a large space for more diagnostics and precision medicine companies like Color and Guardant to provide tremendous value and make healthcare a lot more effective. As Vinod Khosla has often said: we have a check engine light for our cars, why don’t we have one for our bodies? Drug discovery and design platforms like Recursion and Dyno have the potential to develop better medicines more quickly. Outside of medicine, full stack synthetic biology companies like Solugen are aiming to dramatically improve the efficiency of the chemical industry and flip the environmental impact by making it carbon negative. New food products like Impossible Foods and Beyond Meat are also just scratching the surface of what consumer products might be possible with synthetic biology.

For this new wave of products to really take off, there will also be another important customer to support… other scientists and companies.

Backed by new services 🔬🧪

Let’s revisit the evolution of the tech industry. What advances made it possible for two undergrads at Brown to prototype Figma, and then to scale it into a large software company with millions of users? It took a lot more moving pieces than just JavaScript and a really fast web browser.

The entire Web ecosystem has been massively accelerated by frameworks, services and providers.

The engineering required for developing new products can often be broken down into two components: the boilerplate infrastructure needed to provide standard services, and the differentiated and value generating components of the product. For Web applications, basically everybody needs to have a database and user authentication. Payment mechanisms are also important but tricky to get right. While all of these are necessary, they aren’t the core value generating features. They aren’t the tools for exploring code repositories that make Github special, or the reason that users love (and hate) Twitter.

Frameworks and services are an essential way to achieve economies of scale. This has taken a few different forms for the Web. Open-source frameworks like Ruby on Rails established standardized approaches to building production-ready web apps, and have powered products like Airbnb, Square, and Coinbase. Beyond shared frameworks, companies have emerged to provide crucial services like databases, authentication, and payment infrastructure as a service.

Here, I’m talking about the API-first ecosystem that Packy wrote about a while back. When thinking about why Shopify is so content to partner with Stripe, we arrive at the following tradeoff:

“Shopify is a really smart company. It wouldn’t tie its own hands for no good reason. Instead, it made a deliberate, strategic choice to focus on the things that it does best, and to plug in Stripe for all of the things that it does best. That’s what third-party APIs enable their customers to do.”

Basically, API providers can provide a highly valuable service to companies by taking on the responsibility for parts of the boilerplate infrastructure. This frees up companies to focus more directly on the parts of their product that are actually differentiated.

So why haven’t we seen more companies equivalent to API providers in biotech?

It’s a tough question to firmly answer, but my hypothesis is that the economics of drug discovery and the mechanics of IP have played a big part. Drugs are an extremely strange asset class. They are enormously expensive to make and test, but get the benefits of patent protection and captive markets once they are approved. In this environment, huge R&D costs have been treated as a necessary evil, and many companies reinvent the wheel and build out a lot of scientific infrastructure before spinning down after selling a single drug. For platform companies, there hasn’t been much incentive or cultural emphasis on sharing any parts of the secret sauce used to make new drugs.

So far, the provider ecosystem in biotech has consisted of companies selling scientific instruments and reagents. Examples include the DNA Sequencing giant Illumina—which effectively enabled the birth of the entire field of modern genomics—Twist Bioscience which sells synthetic DNA, and 10X Genomics which sells instruments that enable the measurement of single cells. These are all big public companies that have made a big impact on biotech, but still operate on a much lower level of abstraction than a company like Stripe.

Well, as you’ve been reading so far… The Times They Are a-Changin’ 🎶

With a new generation of founders with different technological backgrounds and exposure to software and tech, new business models are being explored. Having seen the success of software-based service providers, tech VCs have been more willing to back some of these efforts. But what is the equivalent of an API in the world of techbio?

In software, an API is a contract written in code between a client and a provider. In the life sciences, experiments or difficult manufacturing can be contracted out from companies to Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs). For example, a company can design a pre-clinical experiment (like testing a molecule in mice) and receive the data from a CRO once it has been carried out. The importance of CROs and CMOs has only grown over time, which has introduced another level of difficulty in managing and tracking all of the contracts. This is why we were super excited to back the talented team at Cromatic that is hellbent on solving this problem and letting companies get back to focusing on their core differentiated features.

The type of work that can be contracted out is starting to get pretty crazy. Synthetic biology companies can provide Ginkgo with the design specifications for new organisms, which is a move way farther up the ladder of abstraction, integrating a large number of fundamental technologies like DNA sequencing, synthesis, and design software into more complex services. Culture Biosciences is another experiment in expanding the scope of CMOs, offering a “Cloud Bioreactor Lab” which is a set of bioreactors that can be remotely controlled through a Web application. It’s interesting to note that these are both YC companies.

At Not Boring, we think that these early examples are only scratching the surface of what a full-fledged API-first techbio ecosystem could look like. We’ve now backed Melonfrost, a fast moving startup that is aiming to build an automated approach to evolving new organisms, providing scientists with an “evolutionary steering wheel, to unleash the full potential of synthetic biology.” Stay tuned for more on this team in the future. 👀

There are also other types of more conventional service providers that are emerging. For a long time, SaaS in biotech has been viewed as a fairly cursed enterprise, with a small market that has very strange dynamics. This situation has started to thaw. Benchling—another YC company with a seed round led by a16z—has built a widely used software stack for life science companies, and was valued at $6B in a recent funding round. This type of development has spurred a ton of excitement, as evidenced by communities like Bits in Bio, where hundreds of developers are exploring ways to contribute to new software for science.

All of these new services have the potential to do something very important: drive down the cost of making biological products. Cheaper drugs, foods, and chemicals. This is clearly a good thing! But ultimately, infrastructure doesn’t just decrease costs—it also makes new things possible. As USV has written about, there is often a virtuous cycle between apps and infrastructure. In the world of Web apps, new infrastructure hasn’t only made it way cheaper to build the same things we were in the 90’s, it has opened the door to totally different types of products and experiences:

For the ecosystem of techbio apps and infrastructure, we’re probably only in the first or second cycle. One of the central motivations for my life and career is to help accelerate this process. Who can even guess where this revolution will take us? Programmable cell therapies, reprogramming our cells to live longer, designing seeds that grow into buildings when we plant them on Mars? Embracing the immense generative potential of living systems will be an important part of building a healthier and more abundant future.

Whatever we end up building with techbio in the future, new services and infrastructure will play an important role in making it happen.

Massive 💰🚀

A little over a decade ago, a very thoughtful biotech VC and blogger named Bruce Booth wrote a detailed post about the Biotech Venture Capital Math Problem. The main thrust of the piece is that the return profiles of biotech are much different than tech, which dictates the optimal fund size and investment strategy necessary to be successful:

“The sad reality is that these types of “halo deal” wins just don’t happen in Life Science venture capital investing. We have great success stories in the 5x-15x range, like Amira, Avila, Enobia, Plexxikon – but 100x+ returns aren’t in the genetics of our ecosystem.”

With a stark difference in the amount of capital required in biotech, and the size of outcomes, funds have needed to compensate by making more concentrated bets to have meaningful ownership, and to stick with smaller funds. This disciplined analysis is probably worth reading and keeping in mind for tech VCs too. As AUM grows, it becomes harder to return the same multiples. VC doesn’t infinitely scale, as SoftBank has recently shown us.

While the basic equation of venture capital hasn’t changed, biotech return profiles have.

When looking at historical data in his post, Bruce pointed out that “according to BioCentury data, there have only been 17 venture-backed M&A deals from 2007-2011 with disclosed upfront payments bigger than $400M, and only a small handful of IPOs to break that valuation in their offerings.”

In recent years, we’ve seen massive acquisitions in biopharma, leading to some of the biggest multiples for biotech VCs of all time. Even a decade ago, Bruce hedged and wondered if we would more frequently see more of these large deals, saying “betting on large Black Swans in biotech may work in the future. The past isn’t predictive of the future, so maybe we’ll have a lot more Pharmasset-like exits” referring to the $11.2B acquisition by Gilead in 2011.

However, it would have been incredibly hard to predict what has started to happen in techbio. Beyond “build to buy” companies where the ideal outcome from the inception of the company is a massive pharma acquisition, many valuable life sciences companies are now being built to be enduring businesses that continue to grow over time. In just this post alone, I’ve already highlighted a handful of multi-billion dollar techbio companies.

We’ve ended up in a wild world where it costs $100 to sequence a genome, and serial tech entrepreneurs like Elad Gil are riding that wave to build precision medicine companies like Color. Recursion Pharmaceuticals isn’t looking to be acquired by a pharmaceutical company—they are looking to be a pharmaceutical company. We still don’t know how to accurately price this kind of approach, and need to validate the hypothesis that the rate of drug development will increase. But the potential opportunity for value creation at the intersection of these technologies is enormous, with some speculating that we could see an additional $9 trillion dollars in market capitalization in biopharma in the next five years alone.

We are very early in this revolution. In some ways, it mirrors the immense increase in economic freedom and earning potential that inspired Packy to predict that “within two decades, we will have multiple trillion-plus dollar publicly traded entities with just one full-time employee, the founder.”

This type of thinking begs the question: what will the first trillion dollar techbio company look like?

It may have a creative business model that doesn’t resemble anything we see today. Let’s briefly just explore one potential idea: the game studio model. In the video game industry, companies get to derive profits in two interesting ways. They sell the games they create, and they sell access to the platform they use to build the games. Epic Games does exactly this—creating popular games like Fortnite while also selling licenses to the Unreal Engine they used to make it.

This is why Epic Games has been valued at $31.5 billion. This was laid out in a news article about one of the companies financing rounds, saying

“A big reason Epic attracted $1.25 billion from venture and private equity leaders Kleiner Perkins and KKR is a bet that the gaming engine behind-the-scenes, called the Unreal Engine, that has turned Fortnite into a household name will become critical to technology across many sectors of the economy, from architecture to medical research and car manufacturing.”

So… game engineers nerded out and built such a powerful game engine that it now may be useful for designing actual buildings. This actually wouldn’t be the first time this has happened: game developers have driven a huge amount of the progress in graphics software and hardware. The GPUs that power modern AI are actually Graphics Processing Units that were first designed for PC gaming.

As people have pointed out (here and here), techbio platform companies basically resemble the game studio model. They build engines and talented teams of individuals to develop the drugs that are their ultimate product. But so far, they have only captured value from the drugs they sell themselves. What if a company also licensed part of or all of their platform to other users? This could lead to profits from both the royalties associated with platform use and from the drugs developed in-house. Now, run the basic math for a company like Epic Games that is selling multi-billion dollar drugs instead of games… 🤯

This is just one hypothetical scenario and as the wise Yogi Berra once said, “it’s tough to make predictions, especially about the future.” While it’s hard to know in advance what types of generational companies will emerge in this space, I’ve tried to lay out what I think the key ingredients will be.

Biology is rapidly accelerating and becoming an engineering discipline. New scientific and technical founders are chomping at the bit to build ambitious and enduring techbio companies. As the cost of biotech company creation steadily declines and the returns swell, new investors are backing these companies with much more favorable terms. We are now entering into a period of feedback loops between vertical products and horizontal infrastructure that has the potential to drive down the cost of engineering biology, and to open the door to totally new types of products that we currently can’t even dream of.

This is a foundational transition. If we pull this off, the future of techbio will be… massive.

Thanks to Elliot for the excellent techbio overview and Dan for editing! Subscribe to Elliot’s newsletter, The Century of Biology, to stay up to date with the techbio revolution.

That’s all for today, we’ll see you Friday morning for a Weekly Dose of Optimism!

Thanks for reading,

Packy

The term TechBio was originally coined by Artis Ventures, who has been an active investor in this space. NfX has also played a role in establishing the term.

Interesting post. Thanks for writing it, Elliot. Here are a couple of thoughts on your piece. It'd be great to learn from your reactions to them!

So, it seems that we want more founder-led biotechs that can grow quickly to massive outcomes burning relatively low capital, ideally as independent, enduring companies. Using this as a summary for what we're after:

- As much as there have been great progress in several dimensions (as you've described very well), I guess the ability to grow quickly and cheaply is a key piece that is still missing... For instance, I'd love to see stats on the costs of building a biotech over the years. Is it getting cheaper and cheaper? Have the time-to-"success" been compressed?

- Incidentally, I guess the two critical points that enable tech companies' quick and cheap growth are: (1) basically-global, almost-instant, not-strictly-gated networks (i.e. the internet, but also app stores, OSes, etc) and (2) quasi-zero marginal costs. From this point of view, it seems that biotech has a looong way still...

- Maybe an even less optimistic take is that we are not going to get much "techbio" until there are significant breakthroughs in life sciences that shift the key challenges in biotech from tech/science risk (will this solution even work?) to "merely" market risk (can we find and serve customers at some viable level of profitability?).

I do hope my comments don't sound too pessimistic. I am actually optimistic about the century of biology! Keep up the great work.

PS: Quick suggestion, instead of "deep integration", what do you think of "deep interdependence"? Isn't it more descriptive?

Is this the full article? Feels like it got cut off - or is there a part 2 coming?