Welcome to the 744 newly Not Boring people who have joined us since last Monday! If you aren’t subscribed, join 33,302 smart, curious folks by subscribing here:

Hi friends 👋 ,

Happy Monday! If you’re in the US, I hope you’re enjoying some time off for President’s Day.

I like mixing it up ever so slightly on holidays. On our last US holiday, MLK Day, I wrote a longer-than-usual Not Boring Investment Memo on Antara. Today, I’m going to go the opposite way, and try to write the shortest post I’ve written in a long time.

Specifically, here’s the challenge I set for myself: explain what’s happening in the private and public tech markets in a novel way in only the space Substack gives me (no “Continue Reading” button).

As you know if you’ve been reading this, it’s a lot easier for me to write long than write short, so this was a fun exercise. I’d love to hear your feedback on the format: text my OpenPhone number at 1-917-818-0620.

But first, a word from our sponsor…

Today’s Not Boring is brought to you by… Future

Future is the 1-on-1 remote personal training app I’m relying on to get and stay in shape. I’ve been using Future since December, and I’m hooked. My coach, Alex, and I talk every day about the workouts, adjustments, how my creaky knee feels, and how I can improve my diet.

A couple of weeks ago, Future introduced Challenges, a competition to see who can complete the most workouts in 45 days. I’m battling Future CEO Rishi Mandal and fellow newsletterer Mario Gabriele, and I’m currently in last (see above, though I snuck one in this AM and am at 15). Losers owe the winner a share of Roblox, and I don’t like losing; time to pick up the pace.

If you’ve been looking to get healthier, shed a couple pounds, or get in the best shape of your life, join us on Future and get your own expert coach to guide and push you. Use the link below to Challenge me and get your first $45 days free:

Let’s get to it.

Dreams All The Way Up

It Feels Like a Bubble, But It’s Not

Tech is not in a bubble, even if it feels like it is. Compared to the biggest tech companies, the best startups and smaller public companies may actually be undervalued despite record high valuations.

In his classic A Random Walk Down Wall Street, Burton Malkiel wrote, “A blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.” Were the Princeton economist writing an updated version today, he might say, “A blindfolded monkey throwing darts at Robinhood could select a tech stock that would have doubled over the past year.”

And it’s not just public tech stocks. Private market tech company valuations have soared too, with companies raising seed rounds at $20 million pre-revenue, Series A’s at valuations in the hundreds of millions, and Series B’s worth a billion. Robinhood faced an existential crisis two weeks ago, and then raised $3.4 billion in less time than it takes me to invoice a sponsor with bill.com. It’s as if every venture capitalist has become Masayoshi Son.

It feels like frothiness that would make a barista jealous. But what if I told you that startups aren’t overvalued today? They’ve actually been undervalued for the past decade and are just catching up.

Let’s turn it over to Sir Roger Bannister to explain.

The Four-Minute Mile and the Market

In the late 1860’s, when the mile record stood at 4:36, runners around the world started seriously attempting to break the four minute barrier. Three different Walters in a row traded the record, bringing it down below 4:20 by the mid 1880’s.

Between 1942 - 1945, two Swedes, Gundar Hägg and Arne Andersson, traded the record four times, driving it down from 4:06.2 to 4:01.4, a nearly 5-second improvement in just three years. And then, nothing. The record stood, unimproved, for the next nine years, until Roger Bannister stepped up to the starting line at Iffley Road sports ground in Oxford.

Bannister took two seconds off the record, completing his mile in 3:59.4 and becoming the first person in history to break the four-minute mile.

His record stood for 46 days. John Landy smashed it with a 3:58.0. A year later, three runners broke the 4-minute mile in the same race, and today, over 1,500 people have run a competitive mile in under four minutes. Hicham El Guerrouj holds the world record with a 3:43.13 that he ran in 1999.

The moral of the story here is that there wasn’t necessarily anything physical keeping humans from breaking four minutes; it was mental. When people saw it could be done, they just kind of … did it. Bannister, through extraordinary performance, eliminated a mental barrier, and afterwards, other great but not all-time exceptional runners followed his lead.

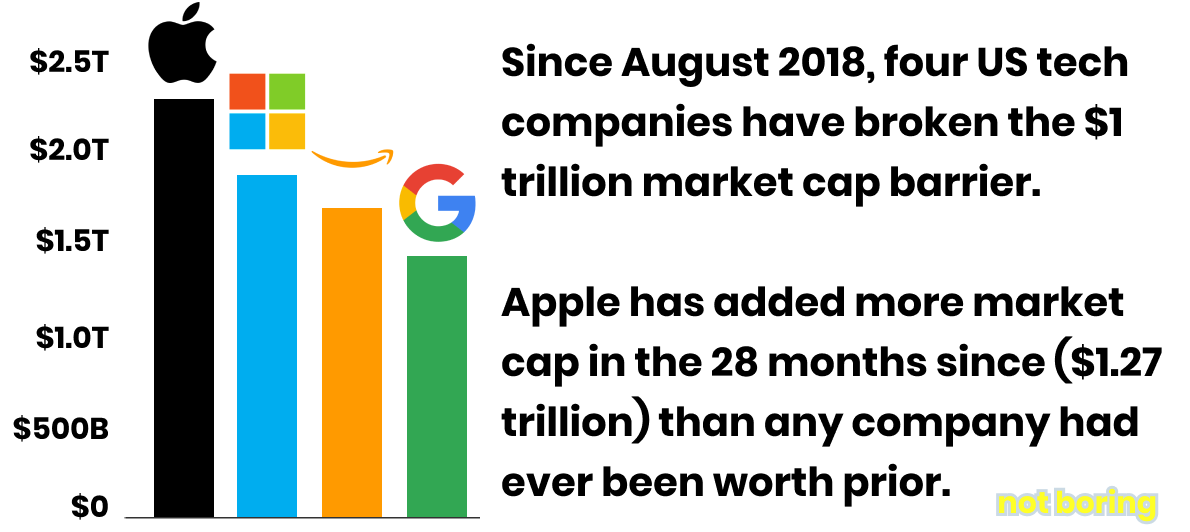

In the public markets in the 2010s, the $1 trillion market cap was the four-minute mile. As someone who owned Apple stock and options earlier in the decade, I can tell you how frustrating it was that the stock seemed to trade at a discount (sub-10x P/E ratio) simply because it was so big, despite insane profitability and growth. $1 trillion felt like a restraining wall.

Then, on August 2, 2018, an extraordinary company broke another mental barrier, when Apple became the first US company to crack the $1 trillion market cap mark.

What happened next wasn’t quite the immediate flood that Bannister unleashed, but within 16 months, by January 2020, three more companies -- Microsoft, then Amazon, then Google -- had broken $1 trillion. FAAMG had been undervalued across the board. Since Apple couldn’t break $1 trillion for psychological reasons, and it was clear that the other four weren’t as valuable as Apple, they had to be worth some discount to Apple’s artificially low market cap.

Note: FAAMG is a weird acronym for the biggest tech companies -- FB, AAPL, AMZN, MSFT, GOOG. They’re a good proxy for how big the market thinks tech companies can get.

Apple took the governor off, and today, after a wild, tech-friendly pandemic and zero interest rate policy (ZIRP) drove stocks higher, the FAAMG market caps are:

Apple: $2.273 trillion

Microsoft: $1.848 trillion

Amazon: $1.651 trillion

Google: $1.415 trillion

Facebook: $770 billion

If certain parts of the market feel bubbly, these companies don’t. They’re category-defining companies that continue to grow and innovate at a faster clip than megacaps ever have before, and they trade at very reasonable NTM EV/EBITDA multiples:

Apple: 22.0x

Microsoft: 24.8x

Amazon: 22.4x

Google: 15.4x

Facebook: 13.1x

That’s not bubbly. Poking fun at the bubble talk, Michael Batnick tweeted this chart:

That’s Amazon’s revenue, not its market cap. Insane. If Amazon keeps up that pace, $1.6 trillion will seem cheap within half a decade, which will make other numbers that seem big today seem smaller. The bar will keep getting higher.

The market caps of the FAAMG companies are the most important numbers in the market, because consciously or not, investors are pegging their private and public tech company investments against them.

Price / FAAMG Ratio

Instead of Price/Sales or Price/Earnings, high-potential tech companies are subconsciously being valued on Price / FAAMG, or a probability that those companies will become as big as today’s biggest, and it’s not crazy.

(If I’m wrong, and we actually are in a bubble that’s about to pop, this is the statement that’s going to get me roasted.)

Let me explain. Traditionally, companies are valued based on a multiple of their earnings or profits per share (Price/Earnings or P/E), or if they’re earlier in their journey and growing fast but still unprofitable, on a multiple of their revenue (Price / Sales or P/S), or a free cash flow multiple, or some other financial metric.

But today, in both private and public markets, with P/E and P/S ratios at uselessly high levels, it seems like companies are being valued on a rough probability that they can become as big as the biggest companies, which are themselves more valuable than ever before. With the $1 trillion barrier broken, and $2 trillion taken down within a year, there’s no more psychological ceiling. That’s where the seemingly crazy prices are coming from.

Now of course, this kind of valuation takes a healthy dose of optimism, and this market is ripe for dreaming, for reasons we’ve covered before:

Tech Strength. Tech companies are actually benefiting from COVID as more activity and commerce moves online.

More Cash and Envy. US personal savings rates doubled, from 7.3% to 14.1%, over the past year. People are seeing their friends get rich and want to put their savings to work.

The Fed. The Fed is printing money, and providing a backstop that makes risky assets less risky.

Rates are at all-time lows. That means money is cheap and investors are turning to equities (and alternative assets, including venture) for yield. It also means that…

Discount Rates are low. Discount rates are how investors figure out what future cash flows are worth today. We’re not there, but for illustrative purposes, a discount rate of 0% would mean that an investor values $1 billion generated in 2031 as much as $1 billion generated today.

In a structurally risk-on environment, people aren’t looking for reasons not to invest, they’re looking for justifications to invest. They want to put their money to work and they don’t want to miss out on the next $100 billion, $1 trillion, or even $2 trillion company.

I don’t think they’re wrong to think that way. In fact, relative to the biggest tech companies, the best startups and smaller cap tech companies are still undervalued compared to a decade ago.

Here’s my logic: FAAMG stocks seem to be reasonably priced and good anchors off of which everything else is pegged. FAAMG (particularly Amazon and FB) market caps have actually grown faster than startup and non-FAAMG public tech valuations. Startup and non-FAAMG valuation growth is just starting to catch up to FAAMG growth over the past year.

Startups and smaller cap tech companies are being valued based on a probability that they can become as big as the FAAMG companies (or the biggest companies in their verticals), and even at the same probability, they should be worth 5-15x as much as they were worth a decade ago, because the ceiling has risen that much.

In other words, if you think that FAAMG are reasonably valued, and you think that the probability of newer companies coming in and eventually growing as big as the biggest tech companies is about the same as it was a decade ago, startups and smaller cap tech companies are actually fairly valued or even undervalued today.

To illustrate, let’s keep it simple and look just at startup data, using post-money valuation data on US startups from Pitchbook. Here’s a chart of the growth of startup valuations versus FAAMG over the past decade:

Facebook (since its 2012 IPO) and Amazon have both smoked startup valuation growth at every stage, and only later stage valuations (Series E and beyond) have grown faster than Microsoft or Apple (Google has been a slow-grower, not even quadrupling).

Looking at average US startup valuations versus both Apple and Amazon’s market caps paint an even clearer picture. Early stage startups (Seed, Series A, Series B) are actually worth less as a percentage of Apple’s market cap than they were a decade ago. Later stage companies have grown their valuations relative to Apple, especially in the past few years, but the average Series D valuation is still only one-tenth of one percent of Apple’s market cap.

Startups at every single stage are worth less of Amazon, on average, than they were a decade ago.

With lower discount rates over the past year, it makes sense that spreads would compress: startups’ hypothetical cash flows are further in the future than FAAMG’s, so the lower the discount rate, the more startup cash flows will be worth relative to FAAMG’s. As Will Fang put it when we were discussing this idea, “When the discount rate is near-zero, time value isn’t really a thing anymore, so it's not a matter of when company x can win, but if it will eventually.”

It also makes sense that late stage is catching up more quickly than earlier stage. At the later stages, there’s a clearer picture of who will win and a clearer line of sight into what the winners’ cash flows might be than for earlier stage companies. There are also fewer later stage companies, and their averages aren’t dragged down by as many low-probability-of-success companies as earlier stage valuations.

Averages are obviously imprecise but they paint a pretty clear picture here: you can abstract away a lot of complexity by thinking about startup valuations as the probability that they can grow as large as Facebook, Amazon, Apple, Microsoft, or Google. The higher the valuations of the biggest tech companies, the higher the potential valuations of any startup.

Take Clubhouse, for example, which was recently valued at $1 billion before earning a dollar. Helllloooo bubble, amiright? Nope. $1 billion means investors are pricing in a 1/770 shot it can become the next Facebook, a 1/100 shot it’s the next Snap, or a ~1/50 shot it’s the next Twitter.

Adding credence to the P/FAAMG methodology, FAAMG haven’t only proved that companies can get really big from a market cap perspective, but also that their eventual success isn’t clear from looking at the early financials. Facebook and Amazon’s financials looked silly early on -- Facebook not monetizing for a long time, Amazon intentionally keeping itself unprofitable -- but their strategies have been proven right in the long-term. Facebook was once a laughed-at $98 million Series A with no revenue, back in 2005 when $98 million was a lot, and look at it now.

Lack of revenue or profits can’t be a disqualifying signal, as long as there’s a sensible plan to get there, eventually. PLUS, entrepreneurs now have the benefit of seeing both how those companies executed, and how they’ve talked about themselves, so they know the right things to do and say. Plus plus, the tools are better now, so it’s easier to get bigger, quicker than it was for any of the FAAMG companies.

This also works within verticals; valuations can be viewed as the probability that they become as large as the largest company in the space. That explains why some verticals get hot when its biggest companies break out, like Stripe in fintech or API-first or SpaceX in space tech.

Within a given stage, most companies will fetch a lower-than-average valuation, reflecting a lower-than-average probability that they will get massive, and a few will fetch much higher valuations, reflecting their higher probability. That makes sense, and explains the wide range of valuations within any given round. Some companies have a much higher probability of reaching FAAMG / best-in-class status than others.

Case Studies: Stripe and Shopify

The averages let us know we’re on the right track, but looking at specifics within all of that data drives the point home. One example is Twitter, which I wrote about last week. I hadn’t fleshed this idea out as fully, but wrote about the dumb idea that Twitter had a lot of room to run because other major tech companies, particularly Facebook, are worth more than 10x as much. The next day, it reported good earnings. The stock is up 26.6% since I hit send, because the narrative started to change, and investors started dreaming about its potential relative to Facebook’s. Time will tell if it gets there.

Let’s take a look at two more: Stripe and Shopify.

Stripe

Stripe illustrates how valuation in this market is dreams all the way up, because its ceiling is impacted by the very biggest companies, and it, in turn, impacts the ceiling of API-first and fintech companies at earlier stages.

Stripe is rumored to have raised at a $100 billion valuation recently, and rumors of secondary market transactions in the $125 - $150 billion price range abound. Most people I’ve spoken to about it don’t know what Stripe’s numbers look like; instead, they’re saying things like, “There’s a very good chance this is a $1 trillion+ company, the next FAAMG, so even if $150 billion feels expensive today, this could 8-15x.”

Stripe is kind of in a league of its own, without a perfect comp among FAAMG. But it has that “this could become the biggest company in the world” mystique around it. The biggest company in the world, today, is Apple at $2.27 trillion. That’s a high ceiling.

Even if it’s just Visa, with its $448 billion market cap, that’s a 3x.

With Stripe as an anchor, API-first startups are raising at big valuations. In November 2020, Checkr, which is an API-first background check company, raised at a $2.2 billion post-money valuation. In January, Check, which is building a payroll-as-a-service API, just came out of stealth and raised a $35 million Series B (led by Stripe and Thrive), which likely values it somewhere near $300 million post-money.

Those feel high for their rounds, but translate to a 1-in-45 chance that Checkr achieves what Stripe has to-date, and a 1-in-8 chance Check achieves what Checkr has, with some slight discount for time. Those seem like reasonable bets to make given that they’re two massive, perfect API-first use cases, of which there aren’t many, run by strong, experienced teams with great early traction. I’d rather invest in Checkr and Check than ten “cheaper” but worse API-first companies — you get what you pay for.

Shopify and Amazon

Shopify’s relationship with Amazon is the textbook example of P/FAAMG valuation.

Since going public in May 2015, Shopify’s stock is up over 5,000%. It’s currently trading at a 60x NTM EV / Revenue multiple and a 395.7x NTM PE ratio. Those are both very high numbers if you’re valuing Shopify based on the fundamentals, and indeed, Shopify has felt expensive at almost every point on its meteoric rise since late 2018. I made this chart back in May to describe what it’s felt like thinking about investing in SHOP:

Since then, it’s up another 90%. Crazy, right? But what if you look at SHOP’s valuation as a probability that it will become as big as Amazon?

Breaking apart SHOP’s valuation that way, there are two factors: how much has Amazon grown, and how much has the probability that Shopify becomes as big as Amazon changed?

Amazon Market Cap. Over the past five years, Amazon has grown its market cap 6.7x, from $245 billion to $1.65 trillion.

Probability SHOP Becomes AMZN. The implied probability that Shopify becomes Amazon, based on their relative market caps, has increased from 0.68% to 10.76%, not taking into account the fact that Amazon is likely to continue to get bigger as SHOP catches up.

Let’s assume Amazon’s future growth and the discount rate come out in the wash, which is conservative, and we’re left with an ~11% chance that Shopify becomes as big as Amazon. If you believe that Amazon is fairly valued, and that an 11% chance of Shopify becoming Amazon is reasonable, then Shopify’s market cap isn’t as crazy as it seems from looking only at traditional valuation metrics.

Onwards and Upwards

There’s a trope going around that since companies are raising more, earlier, at higher valuations, investors need to sit out or sacrifice returns by ignoring price to get into the hottest deals. After digging into the numbers, I just don’t think it’s true. The ceiling for these companies, as represented by the market caps of the biggest tech companies, is 5-15x higher than it was a decade ago, and should FAAMG keep growing, that ceiling may be 5-15x higher in another decade.

As I’ve been thinking about this idea, the house from the Pixar movie Up keeps coming to mind.

Startups and smaller cap tech companies are the old man’s house, FAAMG are the balloons, and Apple breaking the $1 trillion market cap threshold was the moment the house ripped away from its foundations and took flight. The balloons and the house keep floating higher, in lockstep. It makes sense for balloons to float, it feels weird for a house to float, but when you put the two together… the physics kinda work.

That said, the averages obscure the specifics, and this is different from company to company and vertical to vertical. Some areas that feel expensive are actually probably cheap, held back by the psychological barriers of investing at prices that just feel too high, while other areas might be bubbles even if the prices are lower. Some balloons will undoubtedly pop.

Take electric vehicles, a category in which there seems to be a new multi-billion dollar SPAC every day. The category will certainly grow, but the prices seem wild since they’re tied to the Tesla balloon. Tesla is a great company that may grow into its valuation, but at current multiples, it’s not as solid an anchor as FAAMG. Even if Tesla’s price proves to be right, some companies will win and some will lose, as always, but deals are pricing as if they’re all going to win. Nikola continuing to trade at an $8 billion market cap seems way out of whack -- bubbly.

Or take Gamestop, which was trading on memes, or any number of penny stocks that rocket up 200% in a day. Those are microbubbles, and I’m not arguing that they fit into this framework. But bubbles like Nikola, Gamestop, and penny stocks seem to be contained mispricings of the probability of success, or downright speculation, as opposed to systemic overvaluation.

There’s a very real chance that as FAAMG continues to grow, we don’t have a major market correction so much as micro-adjustments of each company’s probability of reaching the top. We’ll see more companies that raised at high valuations fail than ever before, but we’ll also see more companies reach the $100 billion and $1 trillion marks than ever before. Venture returns follow a power law, and that may become more extreme in the coming years.

Then again, I might look back on this essay with shame in a few years. The market could cool off or pop, FAAMG could re-rate to the lower multiples typically enjoyed by the world’s largest companies, and both public and private tech company valuations could get slashed. I expect you to call me out if that happens.

As for how to apply this? There’s not an easy framework to judge the probability that Company X becomes the next Amazon. This isn’t precise. It’s more of a sense check the next time you find yourself thinking, “It’s a bubble” or “It’s competitive out there so people are sacrificing returns to get into the hot deals or buy some growth.” Maybe there isn’t a trade-off between sitting out and being disciplined on price so much as a need for reframing what being disciplined on price means. The ceiling is higher than ever; it’s dreams all the way up.

Thanks to Ben and Ronny for data help, and to Dan for editing.

Thanks for reading, and see you on Thursday,

Packy