Circle & USDC: Building a Stable Platform

A Very Deep Dive on Stablecoins, USDC, and a Platform for a New Financial System

Welcome to the 778 newly Not Boring people who have joined us since Monday! If you haven’t subscribed, join 140,394 smart, curious folks by subscribing here:

🎧 This is a long one! To listen to me read it instead, head over to Spotify or Apple Podcasts.

Hi friends 👋,

Happy Thursday!

As the dust has begun to (hopefully) settle on the crypto crash, people have begun sorting through the rubble to figure out which products from this last cycle were useful and real, and which were hypes and ponzis. I’ve thrown my hat into this ring too many times, including two pieces on web3 use cases: Today and in the Future.

One category that seems to be unanimously viewed as useful, outside of the most skeptical skeptics, is stablecoins. It’s one of the use cases I highlighted a month ago. And among the stablecoins, the consensus seems to be that USDC is the stablest of them all.

Stablecoins are sneakily fascinating because they’re both a digital currency and a sort of platform on top of which new applications can be built, or old ones improved. But to achieve that promise, they need to actually be stable. A dollar-denominated stablecoin, like USDC, needs to be redeemable for a good ol’ fashioned US Dollar, every time, everywhere.

If a stablecoin can be trusted to perform that foundational obligation, then developers can begin to build financial products on modern digital rails. Sometimes, they’ll build entirely new applications, like DeFi protocols. Others, they’ll rip out pieces of old, creaky financial infrastructure and replace them with newer rails.

The revolution does not need to be total to be impactful. Circle is a case study in compromise. It’s a centralized company facilitating the growth of a decentralized financial system. It’s used by web2, web3, and web2.5 companies alike. It’s happy to sit in the background, facilitating fast, cheap, global payments and loans while others build shiny interfaces and sturdy guardrails on top.

After seeing USDC’s outperformance during the bear market – its market cap has grown as the overall market has shrunk – and seeing a lot of people I respect point to USDC as a gold standard, I decided to team up with Circle to tell the story via a Sponsored Deep Dive. You can read more about how I choose which companies to work with on Sponsored Deep Dives here. In this case, I realized that I didn’t know nearly as much about stablecoins as I should, and I was pumped that they were willing to work with me to help understand and then explain.

As always: this is not financial or investment advice. I’m an idiot, and I’m learning as I go – you would be foolish to allocate your cash based on anything I write. Do your own research. But I hope that it’s an entertaining and informative look into one of crypto’s key building blocks.

Let’s get to it.

Circle & USDC: Building a Stable Platform

(Click the link to read the full thing online)

Yes, I know. This newsletter is called Not Boring. But I’m going to start this essay off by showing you the Most Boring Chart in All of Crypto.

That’s the 1 year price chart of USD Coin (“USDC”), the fiat-backed, fully-collateralized, dollar-denominated stablecoin issued by Circle. I dare you to find me a more boring chart.

For the entire past year, as prices of other crypto assets rollercoastered up and down and up and very down, USDC hugged the $1 line tightly. 🥱

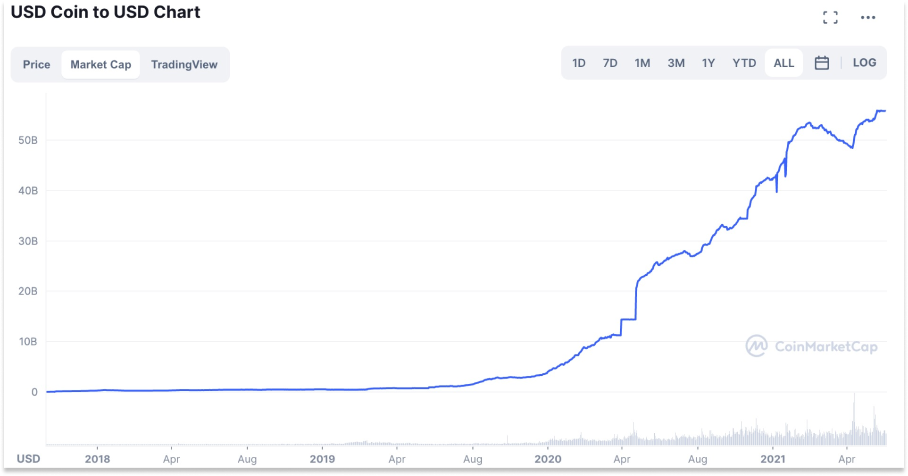

For stablecoins, boring is good. Boring is the goal. And being the most boring stablecoin results in a chart that isn’t very boring at all:

That’s USDC’s market cap since its inception in October 2018, which represents the total USDC in circulation. At the time of writing, July 20th, 2022, that number stands at $54.8 billion. Circulating USDC has more than doubled in the past year, after growing 25x between July 2020 and July 2021. Since its price is pegged to $1, increases in market cap mean that there’s more usage of USDC (the inverse is also true – the market cap declines when people redeem their USDC for Dollars).

Boring is a feature, not a bug. It’s key to Circle’s first product value proposition – digital dollars – and it’s key to Circle’s mission: To raise global economic prosperity through the frictionless exchange of financial value.

If you’ve heard of Circle, it’s likely because of USDC. That’s the company’s first killer product. Recently, it announced that it’s launching a second, Euro Coin (EUROC).

But thinking about USDC and EUROC as just stablecoins misses the company’s ambitions to become:

The platform on top of which developers build a new financial system

The digital currency of choice institutional investors leverage for trading and settlement

A tool that enables the frictionless, borderless exchange of value

It’s an ambitious bet in a competitive space, and one dogged by both valid and invalid concerns, many of which we’ll cover in this piece. Circle is trying to differentiate on trust, the necessary foundation for its ambitions. Increasingly, it seems to be working.

I didn’t give much thought to stablecoins until Luna’s UST blew up a couple of months ago. But as I’ve dug in, I’ve realized that they’re one of the most solid use cases in web3 today, and a fundamental building block in the much bigger visions entrepreneurs in the space are building towards. Once the idea of programmable, permissionless money worms into your brain, it’s hard to see where stablecoins wouldn’t provide an improvement over the status quo.

But let’s start with the basics and build up from there:

What are stablecoins?

How do stablecoin issuers generate revenue?

Why are stablecoins a valuable primitive?

How are USDC and Circle a platform?

What is Circle’s competitive advantage?

What would a new financial system built on Circle’s rails look like?

What Are Stablecoins?

If you’ve followed the crypto markets recently, you might’ve heard the word “stablecoin” and chuckled. “Stablecoin, huh?” you’d quip, “Not very … stable 😂.” It’s a funny joke.

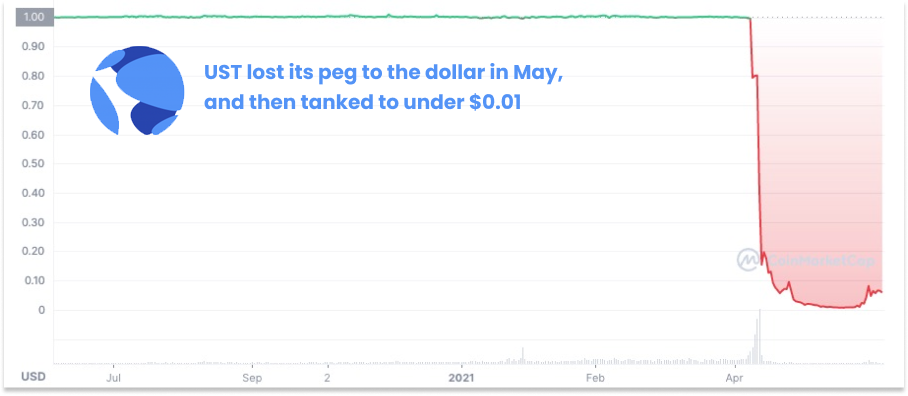

In May, UST (Terra’s stablecoin) lost its peg to the dollar (translation: it became worth less than $1). It flushed hard, bringing the entire Luna ecosystem down with it. Ultimately, it brought down crypto hedge fund Three Arrows Capital (“3AC”) which contributed to the downfall of Celsius, BlockFi, Voyager, and other Centralized Finance (“CeFi”) lenders. Friend of the newsletter Jon Wu wrote a great thread / Not Boring essay on Terra-Luna and UST, and Arthur Hayes wrote the definitive piece on the 3AC collapse in case you want to read more gory details.

The UST situation brought to light something that was apparent to anyone who dug into the math or simply walked through the logic: not all stablecoins are created equal. Not all stablecoins are … stable.

The goal of a stablecoin is to stay pegged to its reference asset. For most stablecoins, that’s the US Dollar. So one (1) USD stablecoin – like USDC – should be worth $1. As Alex Danco wrote in 2018:

The crucial test that any stablecoin must pass for the market to actually trust it is: if a user wants to redeem their stablecoins for genuine dollars, under any reasonable circumstance, can they do so?

“Reasonable” is doing a lot of work here. People should always be able to redeem their stablecoins for genuine dollars. There are three main models stablecoin issuers pursue to make that happen:

Fiat-Backed

Cryptocurrency-Backed

Algorithmic

We’ll start last, first. Algorithmic stablecoins, like UST, aren’t backed by dollars, a basket of cryptos, commodities, or anything, really, outside of what they create themselves.

Instead of explaining this insanity myself, I’ll turn it over to the inimitable Matt Levine:

Here is how an algorithmic stablecoin works:

You wake up one morning and invent two crypto tokens.

One of them is the stablecoin, which I will call “Terra,” for reasons that will become apparent.

The other one is not the stablecoin. I will call it “Luna.”

To be clear, they are both just things you made up, just numbers on a ledger. (Probably the ledger is maintained on a decentralized blockchain, though in theory you could do this on your computer in Excel.)

You try to find people to buy them.

Luna will trade at some price determined by supply and demand. If you make it up on your computer and keep the list in Excel and smirk when you tell people about this, that price will be zero, and none of this will work.

But if you do a good job of marketing Luna, that price will not be zero. If the price is not zero then you’re in business.

You promise that people can always exchange one Terra for $1 worth of Luna. If Luna trades at $0.10, then one Terra will get you 10 Luna. If Luna trades at $20, then one Terra will get you 0.05 Luna. Doesn’t matter. The price of Luna is arbitrary, but one Terra always gets you $1 worth of Luna. (And vice versa: People can always exchange $1 worth of Luna for one Terra.)

You set up an automated smart contract — the “algorithm” in “algorithmic stablecoin” — to let people exchange their Terras for Lunas and Lunas for Terras.

Terra should trade at $1. If it trades above $1, people — arbitrageurs — can buy $1 worth of Luna for $1 and exchange them for one Terra worth more than a dollar, for an instant profit. If it trades below $1, people can buy one Terra for less than a dollar and exchange it for $1 worth of Luna, for an instant profit. These arbitrage trades push the price of Terra back to $1 if it ever goes higher or lower.

The price of Luna will fluctuate. Over time, as trust in this ecosystem grows, it will probably mostly go up. But that is not essential to the stablecoin concept. As long as Luna robustly has a non-zero value, you can exchange one Terra for some quantity of Luna that is worth $1, which means Terra should be worth $1, which means that its value should be stable.

“All of this is,” Levine writes, “quite straightforward and correct, except for Point 7, which is insane.” $UST and $LUNA rose in tandem, and they fell in tandem.

After UST’s collapse, the market for algorithmic stablecoins will likely be muted for a long time, so we don’t need to spend more time here.

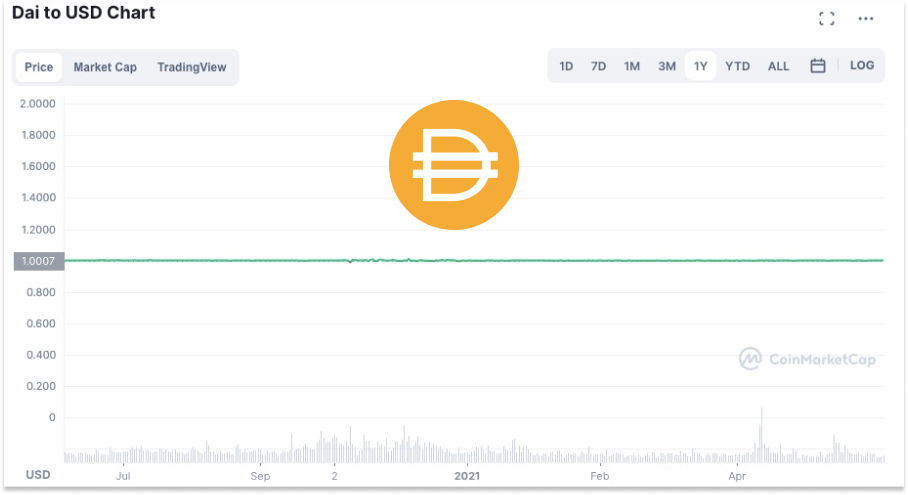

Cryptocurrency-backed stablecoins are backed by a basket of cryptocurrencies and are typically overcollateralized, meaning that the dollar value of cryptocurrencies in the reserve exceeds the dollar value of stablecoins outstanding. They achieve this by requiring each user to deposit more in another token, like ETH or BTC, than they pull out in stablecoin.

The leading example here is MakerDAO’s stablecoin, DAI, with a $7.2 billion market cap.

Here’s how it works:

A user who wants to take out a loan opens a Vault by sending ERC-20 tokens like ETH, Wrapped BTC, and USDC to the smart contract and receives DAI in return.

DAI borrowing is overcollateralized, meaning that you need to put in a higher dollar value in your ERC-20 token of choice than you take out in DAI, with higher collateral ratios depending on the volatility and liquidity of the token you deposit. Currently, ETH has a minimum collateral ratio of 170%, Wrapped BTC of 175%, and Staked ETH of 185%.

At any time, you can deposit your DAI back in and unlock the ERC-20 you’d locked up.

If, however, the price of your ERC-20 of choice drops to a point that breaks the minimum collateral ratio, Maker will liquidate you, or sell your tokens.

The disadvantage of borrowing DAI is that you need to put up a lot of collateral – currently, to borrow DAI with ETH requires a minimum collateral ratio of 170%, meaning I’d need to put in at least $17,000 worth of ETH to get 10,000 DAI. I also have to pay a Variable Annual Fee, currently at 0.50% for ETH deposits.

Plus, if the price of ETH drops to a point that breaks that ratio – in this case, if it drops even one cent – the smart contract liquidates me by selling the ETH. That could mean that you might be forced to sell at an inopportune time.

The advantage of DAI to the borrower is that it’s completely on-chain, without the need for a centralized intermediary, and works well with your existing crypto holdings. If you want to hold onto your ETH but take out a little walking around money, you can just lock up the ETH, get DAI, and use it for any of the things you might use stablecoins for.

The advantage of DAI as a protocol is that, by being overcollateralized and liquidating below certain thresholds, it can maintain stability and keep the promise that users can redeem their DAI for their ERC-20 tokens in any reasonable scenario.

As a result, even during the recent turmoil, DAI has held up well. DAI’s chart isn’t quite as boring as USDC’s, but it’s pretty boring:

At the time of writing, it’s trading at around $1.00, as designed.

There are other crypto-backed stablecoins that are pegged to the dollar, with more launching regularly, others pegged to assets besides the US Dollar, and others still that aren’t pegged to anything at all. Some just want to be reserve currencies themselves. OlympusDAO, for example, has a mix of tokens in its reserve, backing its “Future Decentralized Reserve Currency,” Ohm. If you’ve seen the (3,3) or (something, something) meme on Twitter, that comes from the game theory behind Ohm, that it’s better for everyone if everyone just stakes their Ohm and holds. Ohm has had a bumpy ride, falling from a peak of $420 to a current price of $52.

There are other promising crypto reserve currency projects, all vying to build an internet-native reserve that isn’t tied to the value of any fiat currency, but they’re different than stablecoins and outside the scope of this piece.

That brings us to fiat-backed stablecoins, like USDC.

Circle’s USDC stablecoin is the most straightforward of the major stablecoins: for every dollar of USDC in circulation, Circle holds $1 worth of straight cash and US Treasury Bills, for which there is the deepest and most liquid market of any asset in the world.

If you want to redeem 1 USDC for $1, no magic needs to happen. The dollar is sitting there, either right in the USDC reserve bank accounts at BNY Mellon and other large banks, or invested in short-term Treasuries that are easier than anything else in the world to exchange into dollars. Circle posts weekly reporting and monthly attestations on its website:

In a recent interview, Circle CFO Jeremy Fox-Geen said that Circle’s customers “could redeem all of USDC in one day. We could process those redemptions, and the only limits to the time that they would get their U.S. dollars back are the limits in the settlement systems of the fiat currency banking system itself.”

Some people – from pseudonymous Twitter accounts with 12 followers to journalist Matt Taibbi – have expressed concerns about Circle and USDC, ranging from the idea that centralized institutions cannot be trusted to issues with the structure of its agreement with BlackRock around the Circle Reserve Fund. The concerns boil down to whether or not there will always be a US Dollar available when a customer wants to redeem a USDC, which breaks down into whether Circle holds its reserve in the assets it says it does (Cash and short-term Treasuries) and whether Circle’s business operations and USDC reserves are separate.

Many of these claims seem to stem from a misunderstanding of how USDC works, how reserves are held today, and the differences between USDC and Circle itself.

Addressing the first point, whether Circle holds what it says it does, and where, and what exactly it holds, Circle has been very transparent with its holdings. In the past, it has held commercial paper, corporate bonds, municipal bonds, and Yankee CDs, but in September 2021, it moved all of its USDC reserves into cash and cash equivalents, per the 2021 Circle Examination Report by Grant Thornton.

In a blog post, the company wrote that the growth of stablecoins “has rightly brought significant federal regulatory attention” and that it would hold all USDC reserves in cash and short-duration US government treasuries “given our commitment to maintaining high standards, which in some cases go beyond those required by our regulators.”

In addition to monthly attestations and the annual audit, last week, Circle CEO Jeremy Allaire tweeted a CUSIP-level breakdown of the reserve’s T-Bill holdings:

He said that the company is working to get permission from banking partners to disclose how much it holds with each bank.

On the second, the separation between Circle’s business operations and USDC, Circle offers products that are separate from USDC, like APIs, SeedInvest, and Circle Yield. Given the recent meltdowns at Celsius, BlockFi, Voyager, and others, investors and commenters are most worried about Circle Yield, but Circle’s product is different in that it’s only available to institutional accredited investors. Currently, it offers very low rates.

Importantly, Circle’s yield product doesn’t touch its USDC reserves. Circle doesn’t lend its USDC reserves to anyone, it lets institutional accredited investors earn yields on their own USDC.

More broadly, Circle has publicly stated that its USDC reserve funds are held for the benefit of USDC token holders: “Circle does not and will not use USDC holders’ money to run its business or pay its debts. These funds are in segregated accounts.”

Further, Circle is regulated as a Money Services Business and licensed under the rules and state money transmission licenses that govern major US payment institutions including Stripe, PayPal, and Apple.

To be clear, though: everything has risk. Theoretically, in my opinion, the biggest risk to USDC is that one of its bank partners completely implodes or the US Government defaults on its debt, in which case, God help us all. But it’s important to point out that even though USDC seems to be the most stable of the stablecoins, there are always risks and people always need to be careful with their money. The S-4 that Circle and Concord Acquisition Corp. filed with the SEC in relation to a proposed SPAC deal lists 23 risks on pages 29 and 30. To be very clear: this is not investment advice and you should do your own homework.

Based on conversations with investors and others in crypto, USDC is the most trusted stablecoin in the market. As one friend who’s deep in the bowels of the crypto trading community put it, “Anyone legit in the space holding stablecoins is holding USDC.”

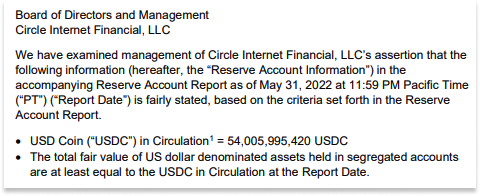

Currently, there is $54.8 billion in USDC, which means it holds cash or Treasuries worth as much via its bank and custodian partners. Every year, Circle’s reserves are audited by a leading public accounting firm, and every month, accounting firm Grant Thornton LLP attests to the fact that it has as much or more in reserves as there are USDC outstanding.

Like I said, boring. The most boring, even among fiat-backed fully-reserved stablecoins.

Tether, which issues the leading stablecoin by market cap, USDT, has come under fire numerous times over the years over concerns about what it does with the money it receives in exchange for USDT. Stripe’s Patrick Mackenzie and friend of the newsletter Alex Danco both wrote great overviews of Tether’s issues in 2019, Patrick’s here and Alex’s here. This whole 85k follower Twitter account, Bitfinex’ed, rose to prominence for calling out Tether. One of the most serious allegations against Tether is that its CFO, Giancarlo Devasini, used Tether reserves to plug a hole in crypto exchange Bitfinex’s balance sheet, which was particularly troubling both because it meant that Tether was not fully reserved, and because Devasini was a large investor in Bitfinex.

Among the more recent claims against Tether are that its reserves are partially backed by billions of dollars in Chinese commercial paper, as reported by Bloomberg (and denied by Tether), and that it lent money to other crypto companies with Bitcoin as collateral. Additionally, the company settled a lawsuit with New York’s attorney general “over allegations that they moved hundreds of millions of dollars to cover up the apparent loss of $850 million of commingled client and corporate funds” for $18.5 million.

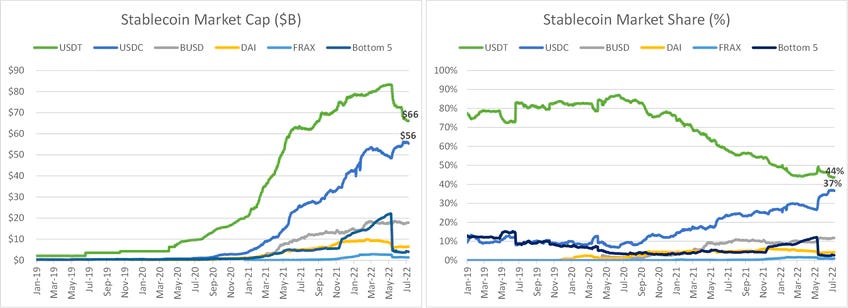

Despite the heat, and the lawsuits, and the government scrutiny, Tether has proven to be Teflon, maintaining a $65.9 billion market cap, down from a high of $83 billion achieved before UST spooked the market for all but the most stable stables.

Tether’s legitimacy has been debated ad nauseum and is out of the scope of this essay, but it’s worth noting that despite $17 billion in net outflows, Tether currently trades at $1. For his part, Jeremy Allaire said on the Bankless podcast that he believes that Tether will be around for a long time and has useful applications, particularly in Asia.

But when the job of a stablecoin is to earn trust, any hair is an impediment. At the heart of Tether’s challenges is the fact that the company is not transparent, and doesn’t disclose where its money is held or what it holds. Particularly in a market like this one, that’s not ideal.

Transparency is where Circle stands out. Largely by earning more trust, USDC is on its way toward flipping USDT as the largest stablecoin. As DeFi Surfer highlighted in Crypto’s Third Trillion Dollar Opportunity, USDC is rapidly gaining market share:

Trust is foundational for stablecoins: people need to trust that their internet dollar will get them a fiat dollar. Trust is the main reason that USDC is stealing market share from USDT, and one of the reasons that fiat-backed stablecoins remain much larger than algorithmic or crypto-backed stablecoins.

Maintaining trust isn’t easy, though. It requires resisting temptation.

How Do Stablecoin Issuers Generate Revenue?

Let’s take a quick but very important aside to understand how stablecoin issuers generate revenue. It’s weird to think of a currency, digital or otherwise, as a business, but understanding how it works will help you understand the motivations of different stablecoin issuers.

Very simply put, the revenue formula for stablecoin issuers is $ in Reserves * Yield on $’s in Reserves.

So a useful framing to keep in mind as you read this piece is that there are two main ways that a stablecoin issuer can increase its revenue:

Grow Reserves

Generate a Higher Yield on Reserves

Growing reserves is straightforward. As a stablecoin issuer issues more stablecoins, it trades $1 from the customer for 1 dollar-denominated stablecoin that it creates. It puts that $1 in its reserve. If someone redeems, they give the $1 back in exchange for the 1 stablecoin. So you can think of this growth lever like most companies: increase usage of the product.

Generating a higher yield on reserves is a little more complicated, and this is where stablecoin issuers can get into trouble. Stablecoin issuers need to generate some yield, that’s how the business works.

Keeping every dollar in USD when redemptions are paid out in USD guarantees that there will always be a dollar available (assuming the banks you’re depositing with don’t go out of business), but bank accounts generate next to nothing.

The next-least-risky is short-duration US Treasury bonds, like 1-month and 3-Month T-Bills. The yield on 3-Month T-Bills is commonly referred to as the “risk-free rate.” Something very bad would need to happen to not be able to get your dollar back from the US Treasury.

Today, 3-Month T-Bills offer a rate of 2.29%, meaning $1 billion in reserves invested in 3-Month T-Bills would generate $22.9 million per year in risk-free* interest income. (*Nothing is really risk-free.) Not bad!

But for some, having $1 billion just sitting there earning the risk-free rate is too boring. There’s so much more money to be made! For them, there are a bunch of different ways to generate higher yields on reserves, including:

A fractional reserve model (like banks) means that you can lend each dollar more than once.

Investing reserves in riskier assets should generate higher yields on each dollar. Riskier assets might include longer duration Treasuries (like a 10-Year Treasury Bond), commercial paper, Chinese commercial paper, Yankee Deposits, DeFi, crypto-lending, and even equity or fund investments.

Pushing 25% of the reserves into even slightly riskier debt that generates something like 4% would mean an additional $4.275 million in interest income per year versus putting it all in 3-Month T-Bills, juicing revenue 19% by doing something that, in most market environments, should be totally fine.

But each basis point of additional yield comes with additional risk. The history of financial markets is full of examples of things that should have been safe in most market environments blowing up spectacularly. CeFi lenders like Voyager and Celsius were riskier than they seemed. Companies default on debt. Countries can default on their debts. During the Global Financial Crisis, the Reserve Primary Fund “broke the buck”, almost destroying the economy as investors withdrew $172 billion from money market accounts before the Fed stepped in.

Over a long enough time horizon, increasing yields on reserves is antithetical to growing $ in reserves, because increasing yields decreases the chance that there will be a dollar there when people want to redeem, which ultimately decreases trust. For pegged stablecoins, trust is paramount. Whoever engenders the most trust among investors through their actions and transparency will win through growth.

Circle has opted to grow reserves, rather than chase higher yields, in order to grow revenue.

Win trust. Grow $ in reserves. Win more trust. Become the standard that developers and financial institutions rely on to build new tools and capabilities.

Because while the value prop that 1 USDC = $1 is crucially important, it’s just the starting point. What makes stablecoins particularly compelling is their digital superpowers.

Why Are Stablecoins a Valuable Primitive?

Cryptocurrencies like BTC and ETH haven’t caught on as a medium of exchange outside of the crypto economy. The main reason is that they’re so volatile.

What consumer wants to spend 1 ETH on rent and watch the price rocket up 10% the next day? What business wants to receive 1 ETH for services rendered and watch the price fall 10% the next day?

The most obvious benefit of stablecoins relative to more volatile tokens is just that: their stability. If both parties in a transaction can reasonably assume that 1 USDC = $1, they can transact like they would in dollars.

The bigger question is why stablecoins are useful relative to good ol’ fashioned dollars, or the bank-intermediated versions thereof. To answer that, we need to start with what I think is the most fundamental thing to understand about crypto in general: crypto gives physical properties to digital assets.

Cash has some advantages over bank accounts. If you have $1,000,000 stashed under your mattress, and you need to pay a business associate $100,000, you can simply pull out a few stacks and pay them directly, right now, for free. Often, if you tried to make the same payment through a bank, you might have to pay wire fees (especially if you want the transaction to settle on the same day) or even need to physically go to the bank to sign papers. If your associate is in another country, that’s probably another fee, and it’s going to take a while. Oh, it’s Saturday? You’ll need to try again on Monday, between 9am - 4pm.

Paper cash has some obvious drawbacks, too. It doesn’t earn anything. Keeping all of that money under your mattress might make for an uncomfortable night’s sleep. If your house catches on fire, the money disappears. A robber can break into your house and steal it. More practically, to give $100,000 to your business associate, one of you is going to need to travel to the other. If you live nearby, that’s a minor headache; if you live in different countries, it becomes very impractical. And then, once you do exchange the money, you need to manually enter the transaction in your accounting software of choice.

Anyway, you know the limitations of cash. There are reasons we don’t use it much anymore. Sending wires online, or even Venmos for smaller sums, is so much more convenient than cash that people put up with the slowness, fees, and lack of control that comes with online banking.

But… there’s gotta be a better way, right?

That’s the basic thing stablecoins are trying to achieve: cash with digital superpowers.

In a great thread on the importance of stablecoins, ChainLinkGod spelled out those superpowers.

He tweeted that stablecoins are a “superior form of fiat” that are:

Programmable

Permissionless

Borderless

Low-cost

Fast settlement

Interoperable

Highly liquid

Let’s unpack each.

Programmable means that stablecoins can be coded to do certain things automatically. In a simple example, if I get my paycheck in stablecoins, a smart contract can automatically release my payment directly every two weeks (or every day, or every hour, given the low transaction costs) with just my wallet address. Some can even be sent to a DeFi lending protocol where I can earn yield, or swapped into ETH, automatically.

Permissionless means that I can send you a stablecoin, right now, with just your wallet address, without needing to go through a bank, just like cash, but digital. It also means that developers can build applications that use stablecoins without speaking to the issuer.

Borderless means that there’s no distinction between sending money to someone in your same country and another country – there’s no such thing as an “international wire” here. I saw the power of this firsthand when a few of Not Boring Capital’s LPs asked to fund their commitments via USDC because the process was so much simpler, cheaper, and faster than trying to fund internationally through their bank.

Low-cost is pretty self-explanatory, but also means that there aren’t any bank fees for holding or sending money. Today, on Ethereum, gas fees can be prohibitive for smaller transactions, but that gas fee remains constant whether you’re sending $1 or $1 million. But already, sending USDC on an Ethereum Layer 2 like Polygon – which is what Stripe does (more below) – or a cheaper L1 like Solana brings the cost down to next-to-nothing. Over time, sending money should be as cheap as sending an email.

Fast settlement means that as I send money to someone, or receive money from someone, that money is actually in my account and not in their account. If you’ve ever had pending transactions in your bank account, or received a payment that’s on the way but not yet in your account, you’ve felt slow settlement. For a good time, check out this Quora on how bank settlement works. Fast settlement, combined with features like programmability and interoperability, mean that money should be able to zip around faster than in the traditional system (at least in the US today; countries like India have better systems, and faster settlement should be coming to the US via FedNow.)

Interoperable means that stablecoins can plug into any of the other web3 protocols and applications, and even into many traditional companies, seamlessly. Interoperability makes stablecoins behave a bit like platforms, which we’ll touch on shortly.

Highly liquid means that there’s enough stablecoin out there that they can easily be bought or sold. There’s over $54.8 billion of USDC alone in the system.

Obviously, there are risks as well.

For example, what happens when you send your money to the wrong address? Unless there’s someone really nice on the other end, that money is gone. What happens if you forget your seed phrase and can’t access your wallet? Money’s gone in that case, too. Wallet gets hacked? Gone. And there’s no bank on the other end to make you whole.

These are real risks for any self-custodied digital asset, and before buying, holding, or sending digital assets, you need to make sure that you’re using best practices like hot and cold wallets, sending test transactions, and never, ever clicking on a Metamask support link. It should get safer over time, as both Circle and the broader developer ecosystem are building products and infrastructure to mitigate the risks and protect users.

Back to the benefits, this being crypto, all of those pieces can combine and compose to create novel benefits. Or rather, entrepreneurs can combine those features to create novel apps that would not have been possible before.

To date, the largest use case for stablecoins has been crypto trading. Funds and individual traders use stablecoins for a bunch of reasons – instant settlement, complex trades without currency risk (needing to make a directional bet on the price of Bitcoin), access to foreign exchange, taking on leverage, and accessing the DeFi markets, where you can’t just plug in US Dollars. Plus, if you want to trade on a decentralized exchanged (“DEX”) like Uniswap, you can’t transact in USD; if you want to sell ETH, for example, for an asset that doesn’t have currency risk against the US Dollar, you’ll trade it for USDC or another dollar-denominated stablecoin.

USDC is used for all of those things, but Circle’s real ambition is to be a platform on top of which developers build novel, previously-impossible financial products.

This is probably a good place to pause for a second and give a little bit of Circle’s history. It wasn’t always a stablecoin company. Its story is a familiar one for platform and API-first companies (see: Amazon AWS & Lithic): build a consumer product, realize the infrastructure doesn’t work, build your own infrastructure, and productize the infrastructure.

Circle’s History: From Bitcoin to USDC

Circle co-founder and CEO Jeremy Allaire started the company in the early days of crypto, back in 2013, to help consumers “more easily convert, store, send, and receive digital currencies such as bitcoin.”

Allaire was already a tech veteran at the time, having founded the eponymous Allaire Corp. and online video services provider Brightcove before founding Circle.

Fun fact: after going down the internet rabbit hole in 1990, when it was largely a tool for the government and academia, Jeremy realized that there was an opportunity to commercialize it. In 1992, he wrote a proposal for the commercialization of the internet and submitted it to the Chairman of the Senate Subcommittee on Science & Technology… Al Gore. When Al Gore famously mentioned to Wolf Blitzer that he “took the initiative in creating the internet,” he did so in part based on Jeremy’s proposal.

Anyway, with Jeremy’s background and the early excitement around bitcoin, he had no trouble raising money. Per PitchBook:

2013: $9 million Series A from Breyer Capital, Accel, and General Catalyst

2014: $17 million Series B led by the same investors with Pantera Capital

2015: $50 million Series C led by Goldman Sachs & IDG Capital at a $250M valuation

2016: $60 million Series D led by IDG Capital at a $480 million valuation

2018: $110 million Series E led by Bitmain at a $3 billion valuation

Amazingly, it raised all $246 million before landing on, and announcing, what would become its killer app: USDC, which it announced in May of 2018.

Joao Reginatto, Circle’s VP Product, told me that when he joined the company seven years ago, he signed up to be the product manager for Circle’s consumer app, Circle Pay.

The plan was to build a product for people who wanted to transfer funds over blockchain rails with an app that abstracted away the complexity and provided a familiar experience. People are most familiar and comfortable with fiat currency, so they enabled Dollar, Euro, and Pound balances and transfers, on Bitcoin’s rails. In the background, they handled all of the liquidity and treasury operations, like converting dollars into BTC and back.

But by 2016, it was getting too slow to operate on Bitcoin, which was built to be P2P money, not to support apps on top. Then, they tried ETH and it wasn’t quite right, either. Then, they thought about launching their own settlement token. No go. Finally, they realized that what they needed was fiat currencies that run on blockchains.

They looked into Tether, but didn’t think they could build on top of it, so the team realized they’d need to create their own stablecoin. They brought it to the leadership team, who said, “OK! Go build a stablecoin if you don’t have the rails you need, and then we can come back to Circle Pay.”

“Then,” Joao laughed, “We never came back.”

In September 2018, Circle and Coinbase launched USDC, and in October, they announced that they’d co-founded the Centre Consortium, “a joint venture aimed at establishing a standard for fiat on the internet and providing a governance framework and network for the global, mainstream adoption of fiat stablecoins.” USDC began circulation in October 2018, and by the first day of 2019, there was $288 million USDC in circulation. To this day, Centre is jointly-owned by Circle and Coinbase and helps set the direction for the protocol, while Circle is the issuer of USDC.

Circle’s history building consumer financial products on the blockchain informed the way that they built USDC.

First, it set the tone for Circle’s regulatory and compliance stance from day one.

As Jeremy explained, one of the earliest questions he and his investors asked about operating financial services on the blockchain was, “Is this even legal?” Some first-time entrepreneurs might just let it rip, but Jeremy had already sold companies and built up a reputation, and he wanted to do it right.

He hired one of the country’s top regulatory advisory firms out of his own pocket, and they found that while there wasn’t a lot of precedent or guidance, there was some. In March 2013, the US Department of Treasury issued a six-page memo titled, “Application of FinCEN’s Regulations to Persons Administering, Exchanging, or Using Virtual Currencies.” Essentially, it said that if you act as an exchanger of money from the banking system to digital currency, you must register as a money transmitter, have Anti-Money Laundering (AML) and Anti-Terrorism policies in place, and get all the appropriate licenses.

Jeremy put it more bluntly: “The reality was, if you wanted to build a business at the intersection of the traditional and new systems, you had to be regulated or go to jail.” But instead of turning him off, Jeremy was actually intrigued by, and drawn to, a space where so much policy work needed to be done:

Something new that changes society and introduces risk needs new policy – autonomous vehicles, AI, spacecraft, genetics. Regulated spaces are hard because the implications for society are more pronounced. I wanted to work on something hard, and something that was going to be hard globally.

So from day one, they “walked in through the front door.” The company’s first non-co-founder hire was its General Counsel / Chief Compliance Officer. Starting in late 2013, Jeremy said, “We got every license we possibly could, and became the most licensed and regulated firm in crypto at the time.” Circle was the first company to receive New York’s BitLicense, and helped shape it by providing feedback. According to Joao, after Circle got the first BitLicense, other people would come to the NYC office for meetings and ask to see it, as if it were a relic.

Early on, and to this day, “doing it in a regulated way brought on a lot of ‘boo hiss’ from the crypto community, but if you want this to be mainstream, you have to do it,” said Jeremy. From the beginning, Circle’s position has been to work with regulators to be part of the dialogue, educate, and “preserve what’s important about crypto: openness, interoperability, programmability, and its inherently global nature.”

Second, starting by attempting to create consumer products on blockchain rails meant that when Circle created USDC, they built it as a platform on which other developers could build beautiful and frictionless user experiences.

From the beginning of USDC’s development, Joao “wanted to build with APIs in mind, and with scalability from the developer’s point of view.” They needed APIs to handle issuance and redemption from the beginning. As soon as the team got USDC to market in 2018, most of it pivoted immediately towards building out APIs and developer tools and documentation.

Circle was preparing for a world in which USDC powered everyday applications in web3, maybe even that it would build itself again, but it was focused on building infrastructure.

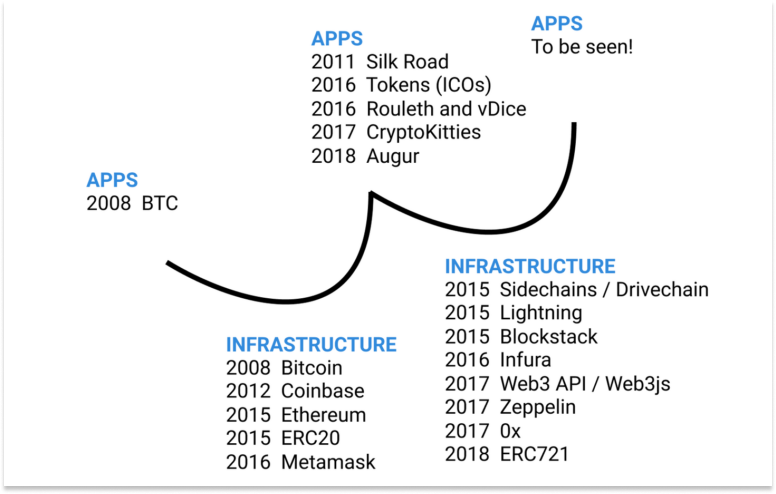

In The Myth of the Infrastructure Phase, USV’s Dani Grant and Nick Grossman described the apps-infrastructure cycle: “First, apps inspire infrastructure. Then that infrastructure enables new apps.”

A developer tries to build an app and realizes that it’s impossible or overly difficult to do with the current infrastructure, so other developers go out and build the infrastructure that would make those apps work, which opens up new possibilities for new apps, which have their own new infrastructure needs, and so on in an upward spiral. That certainly seems to apply to USDC’s development.

Circle built the infrastructure, and started working with developers who were building applications to see how USDC could help. And then suddenly, DeFi Summer happened.

The explosion in DeFi’s popularity – led by protocols like Uniswap, Compound, Aave, and Maker – created an explosion in the developer ecosystem, and interest in embedding USDC in all of the new things they were creating. DeFi developers came to Circle with ideas – “We want to wrap USDC, but make it yield-bearing,” for example – and the Circle team said, “Go for it!” Since USDC is permissionless, Circle doesn’t give or refuse permission anyway, but they were psyched to see developers building new things with their primitive.

USDC adoption has driven Circle’s meteoric rise. In May 2021, with USDC’s market cap just above $20 billion, Circle announced a $440 million funding round from Fidelity, FTX, Digital Currency Group, and more. Later that year, it signed an agreement with SPAC Concord Acquisition Corp. to take it public at $4 billion. This February, it announced that the SPAC valuation more than doubled to $9 billion, and in April, it announced a $400 million round led by BlackRock and Fidelity, as USDC’s market cap grew to $51 billion. There have been no recent announcements regarding the SPAC, and it’s possible that the deal expires before it gets to market given the current market reception of both crypto and SPACs.

Today, while DeFi activity has cooled off, Joao told me that USDC itself, with its scale, gravity, and strength during the crash, is as close as it’s been in its entire journey to behaving like a platform.

How are USDC and Circle a Platform?

When I first spoke to Jeremy, he told me that from the beginning, Circle wanted to build the http or smtp for money, protocols that are open, that anyone can connect to, but that allow for some things that http and smtp don’t, namely moving value and settling transactions.

The manifestation of that vision changed as Circle iterated its way towards product-market fit, but the vision itself remained consistent through the creation of USDC.

“When we launched USDC,” he explained, “The concept was that the best way to launch was as a protocol that anyone can build on top of.”

Circle needed to provide the dollar liquidity and market infrastructure, regulated infrastructure that connects bank money and US Treasury bonds with entities it onboards in a compliant way. Once USDC was in circulation, the combination of tokens and the protocol became a platform that anyone could build on top of.

Now, the Circle team is focused on creating better infrastructure that abstracts away a lot of the complexity for developers and users, and on expanding the suite of stablecoins it offers.

It’s weird to think of digital money as a platform, but it works.

The other day, I was on a call with Joris Delanoue, the founder of Fairmint. Today, the company lets US companies issue equity in exchange for time & effort or a cash investment. The company is web2.5 – investments on Fairmint are compliant securities and the front-end feels very web2, but in the backend, it uses USDC and smart contracts to facilitate smoother, faster, cheaper transactions.

“The USDC stablecoin is absolutely key to blurring the border between on- and off-chain,” Joris explained when my ears perked up, “It’s reliable and properly backed 1:1, and it lets us deliver a 10x better experience when dealing with (crytpo-native) securities.”

Near the end of the call, after we went through all of the progress they’d made on the product, he threw in as an aside: “Oh, and we’re actually looking at the European market now that Euro Coin launched.” That’s a big unlock from a simple coin.

That conversation was the first time that USDC’s role as a platform clicked, but Fairmint is just one example of the many companies, both web3 and traditional, that are building on top of USDC today. Party Round, a Not Boring Capital portfolio company, lets companies raise, and investors invest, in both USDC and fiat. When I asked CEO Jordi Hays why they use USDC, he pointed to demand from both founders and investors, and said that it just makes the experience smoother: “A company can raise money from 50 people in 50 countries as easily as they could raise from 50 angel investors in the US. Instant is big. Global is big. 24/7 is big.”

Established companies like Visa, MoneyGram, Twitter, and Stripe are working with USDC to facilitate crypto payments, too.

In March 2021, Visa announced that it had become the first major payments network to settle transactions in USDC, writing:

Visa’s standard settlement process requires partners to settle in a traditional fiat currency, which can add cost and complexity for businesses built with digital currencies. The ability to settle in USDC can ultimately help Crypto.com and other crypto native companies evaluate fundamentally new business models without the need for traditional fiat in their treasury and settlement workflows.

Visa’s partnership is an important stamp of approval for USDC – Visa is a $427 billion market cap global leader in moving money – and is still in the early innings, focused on settling money within the crypto ecosystem.

Stripe pushed the ball a bit further, towards non-crypto-native platforms and users. In April 2022, Stripe announced that it was introducing global crypto payouts, starting with Twitter creators, with USDC on top of Polygon. Stripe highlighted that crypto payouts will let platforms “quickly pay out to their users in even more countries, and improve their services for those who prefer crypto over traditional fiat payment methods.”

Working with established companies, which are often more conservative than their web3 counterparts, has pushed Circle to answer more sophisticated questions. Speaking with people at Stripe, it’s clear that they’re not just going to do crypto to do crypto; they need to understand how it works down to the most minute detail. Joao said that web2 and traditional payments companies are a lot more focused on questions like, “Which chain should we use? Or should we use multiple? If we use multiple, how exactly does bridging work and is it secure?”

They also have more demanding requirements. “For USDC to be an actual platform for millions of developers,” Joao highlighted, “We need to build out infrastructure that other financial platforms have.”

Circle plans to build out a lot of new infrastructure on-chain, and is particularly focused on how to raise the level of abstraction for developers. For example, Stripe is starting with Polygon, but plans to expand to more blockchains later this year:

That infrastructure should make it so easy to use USDC cross-chain that which chain a developer or user wants to use should be an implementation detail. As Joao put it, “If there’s a merchant who wants to receive USDC on Solana, but the payer is on Ethereum, we want to make that happen easily. We’ll need to abstract away things like bridges, exchanges, gas costs, and more to make it happen.”

It might also build out specific SDKs that make it easy for web2 and web3 companies to build products around USDC. “The web2 opportunity is huge.”

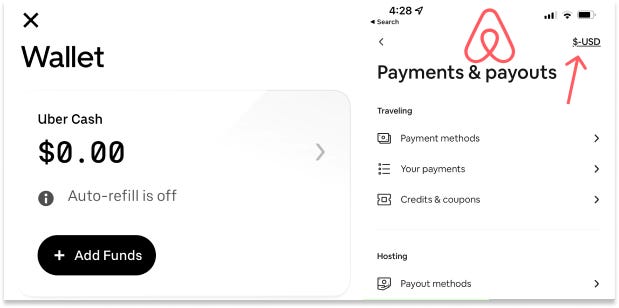

Think about the apps you use every day. Twitter, which consumes ~99.99% of my app time, is already connected to USDC via Stripe. Many of the most popular apps – like Uber and Airbnb – have wallets built-in, even though you might not think of them like that.

Currently, those companies need to register in multiple jurisdictions and set up different banks based on where they operate. Airbnb, for example, is an e-money company in Europe and needs to hold and maintain a license to hold customer balances. Building with something like a Circle wallet SDK, they might be able to let users self-custody, top up their accounts, and spend frictionlessly with much less headache for both Uber & Airbnb, and for users.

Those are pretty straightforward examples, and there are a lot of similar opportunities to build financial products for directly or indirectly financial web2 apps, but the bigger opportunity will likely arise from all of the new companies that couldn’t have been built before.

As Circle builds out tools and infrastructure to traditional companies’ more exacting standards, developers in web3 will get access to those same capabilities, without ever needing to talk to a human at Circle. The infrastructure Circle creates, and USDC itself, are open, interoperable, and permissionless.

There are some obvious challenges that need to be solved to get to a place where stablecoin rails replace the 20th century Fortran-based infrastructure that the financial system is built on top of today. On– and off- ramps, from fiat to crypto and back, need to get smoother. There need to be more options for custody between a Coinbase account and full self-custody with an 18-word seed phrase, like Multi-Party Computation (MPC) and social recovery. Options for refundable transactions will need to be made available. Circle can build some of this into its APIs and SDKs, and the developer ecosystem as a whole will keep developing new solutions to the known challenges.

There will need to be more regional stablecoins, too, representing the Pound, Yen, and hundreds of other fiat currencies used around the world in order for stablecoins’ global potential to be realized. There, too, Circle expects to build in certain cases and partner in others.

Circle plans to keep creating new, regulated, fully-backed stablecoins and better, smoother infrastructure, creating a platform on top of which anyone with an internet connection and some skills can build. It can give those tools to developers for free while still building a massive, profitable business because of the way it makes money. It even has a venture arm, Circle Ventures, that invests in products in the ecosystem that leverage USDC in order to accelerate development in the space.

In fact, Circle is incentivized to make it as cheap, safe, and easy as possible for anyone to build on top of USDC, EUROC, and future stablecoins because Circle makes more money when more of its stablecoins are in circulation.

Circle has iterated its way into one of the best business models on the internet.

What is Circle’s Competitive Advantage?

Here’s the beauty of Circle’s business model: it charges customers nothing, which increases its scale, and makes more money as it gets bigger by investing its reserves in safe assets.

In many ways, Circle is an example of what Chris Burniske calls Protocols as Minimally Extractive Coordinators. In it, he writes: “The less extractive a protocol is in coordinating exchange, the more that form of exchange will happen.”

When dollars are converted into bits and bytes, friction and transaction costs go down. Since Circle doesn’t charge developers or users to use USDC – since it’s minimally extractive – more exchange should happen in USDC. As more exchange happens in USDC, and more USDC circulates, Circle holds conservative reserves to ensure that liquidity is always on hand to redeem USDC for a dollar at par. The portion of those reserves held in US Treasuries, I would assume, generate income for Circle, without needing to charge users or developers.

That’s why, in addition to what I believe are the team’s genuine ambitions to create a better, faster, cheaper, and more open financial system, a stablecoin company can pour resources into building out infrastructure that it gives away for free. It’s building a platform business that monetizes through interest on reserves instead of fees.

USDC is building network effects that boggle the mind, and come from two sources: the platform and the money itself.

Thinking about USDC as a platform, it has classic network effects that are somewhere between Marketplace (2-sided) and Platform (2-sided) network effects as described in NFX’s Network Effects Manual.

Without going too deep into the weeds on the differences – which come from whether supply builds for just one platform or multiple – Circle’s flywheels look like this:

First, as more developers build on USDC, USDC gains more utility (it can be used to transact in more products), which creates more demand for circulation, which creates an incentive for more developers to build on and integrate with USDC. It becomes the de facto starting point for developers and partners looking to build with stablecoins.

The second network effect comes from the money itself. Specifically, the more USDC there is in circulation, the more utility it has. A simple way to think about this is that $1 million is worthless if you’re the only person in the world who uses dollars, but very useful if everyone uses dollars.

This is classic Metcalfe’s Law: the value of a network is proportional to the square of the number of participants in the network.

The bigger and more widely used USDC becomes, the more valuable it is to everyone who uses it and to all of the developers who build on it. And because its platform is money and therefore it’s able to give away its infrastructure practically for free and monetize its reserves, Circle should be able to grow developer and user adoption faster than web2 platforms and APIs that need to charge users to build sustainable businesses.

This is Circle’s competitive advantage against tech challengers, but it might soon face a much larger competitor.

One of the perceived challenges to USDC is that the US government might issue a Central Bank Digital Currency (“CBDC”) in part to maintain the dollar’s position as the global reserve currency in an increasingly digital economy. China is going that route with the e-CNY. Circle believes that USDC and other commercial dollar-backed stablecoins give the US the best of both worlds: the innovation benefits of an open, competitive, capitalist ecosystem that also increases demand for USD as all USDC are redeemable 1:1 for USD. If you’ve been reading Not Boring, you know which approach I think makes the most sense, but it might not be either-or.

Dante Disparte, Circle’s Chief Strategy Officer and Head of Global Policy, believes that CBDCs and commercial dollar-backed stablecoins can co-exist.

“What we’re building for,” he told me, “is something cross-border versus domestic. USDC is internet-scale and designed for open, permissionless, more equitable economic activity on the internet. A CBDC is invariably domestic and transmits the risk to the taxpayer.” Earlier this month, Dante wrote Borderless money in a hot, flat, and crowded world to lay out his position in more detail, and last week, Circle’s VP of Policy & Regulatory Strategy Teana Baker-Taylor dropped a thread on the view that private and public digital money can co-exist:

Time will tell, but the government might be less of a competitor than it is a complement.

In fact, Circle’s skill and experience working with governments is its second source of competitive advantage.

In addition to the advantages that Circle gets with scale, it has a regulatory and compliance advantage over new entrants and existing competitors. Over the past nine years, it has poured resources and countless hours into building out best-in-class internal compliance, getting all of the necessary licenses to operate in the US and abroad, and working with policymakers to craft sensible legislation. It’s had to convince conservative companies like BNY Mellon, BlackRock, and Goldman Sachs, not to mention top insurance companies and auditing firms, to work with it. In doing so, and operating to a high bar, it’s established strong relationships with key players.

If it seemed fairly certain that regulators would crack down on risky stablecoins, like Luna’s UST, before the recent meltdown, it’s all but guaranteed now. It’s clear that stablecoins will be regulated, and that stablecoin issuers will be held to the highest standards. Circle is working to make sure that, as Jeremy described it, “policies don’t put the genie back in the bottle.”

In a more regulated space, Circle’s trust will be an even bigger competitive advantage, as Dante explained:

For some, the feature in stablecoins was opacity, lack of regulation, frictionlessness — all interesting during good times, but when you’re running for the exit and looking for redemption is when trust matters most. You can’t buy insurance when your house is on fire. We’ve been doing things that will increasingly become the global regulatory standard well before it was a requirement.

He believes that we’ll see thoughtful, pro-innovation regulation from the US Government and that regulators will see the importance of “same risk, same rules” in creating “more optionality in payment systems rather than disrupting and disintermediating banks.”

While the government can’t regulate math, it can and will regulate the behaviors of firms issuing stablecoins. And when it does, Circle has a near-decade-long headstart.

In order to compete with Circle, new fiat-backed stablecoin issuers will not only need to overcome its strong network effects, scale economies, and cash generation machine, they’ll need to do so while building up the compliance infrastructure, and trust, that Circle has.

Are the barriers to entry high? Yes. But Jeremy pointed out that there were high barriers to entry in competing with Facebook, too, before Instagram and TikTok came along. Ultimately, the company seems willing to support and partner with anyone in the space who can contribute to building a new, internet-native financial system.

What Would a New Financial System Built on Circle’s Rails Look like?

If you were to design a new financial system today, from scratch, with all of the existing technologies, how would you design it?

There’s another benefit of stablecoins, specifically fully-reserved stablecoins like USDC and DAI, that we haven’t touched upon but that’s worth highlighting: separating the payment function of money from the lending function of money.

Today, both governments and banks can create money. Governments create a certain amount, people and businesses put their money in bank accounts, and then banks can lend out multiples of that money based on reserve requirements. That’s called “fractional reserve banking,” and the amount that banks can lend out relative to deposits is dictated by the Liquidity Coverage Ratio laid out in Basel III. (If you want to have a wild time, you can read all 75 pages here.)

There are issues with a fractional reserve banking system, as seen during the Global Financial Crisis, but Basel III goes a long way towards fixing them. As with anything when I write about web3, I don’t think the benefit is in taking down big evil corporations for the sake of it, banks included. I worked at Bank of America Merrill Lynch. Great people. Instead, to me, one of the main benefits is who the value can accrue to when you remove those middlemen.

When you deposit your money at a bank, they lend it out over and over, and earn interest for doing so. I haven’t checked my account recently, but the interest is typically comically low (and they charge me a $5/mo “maintenance fee”!). The four biggest banks in the US alone – JP Morgan Chase, Bank of America, Citigroup, and Wells Fargo – generated a combined $173 billion in net interest income in 2021.

Net interest income represents the difference between the interest income a bank earns from lending and the interest it pays out to depositors. Presumably, those numbers will go up this year in a rising interest rate environment; depositors don’t care enough to move banks for a few extra basis points.

There’s nothing wrong with banks making money. It’s their job, and a lot of smart people have built out a lot of sophisticated infrastructure to do it well. But it is an opportunity for challengers. In the bull case for DeFi, that $173 billion represents the value available to be either made by lenders or saved by borrowers. The math is rough – on one side, there are a lot more banks in the world, and on the other, fully reserved means fewer loans for each dollar, among other factors – but directionally correct as a starting point.

The difference is that in this system, the net interest income should go to the people who own the dollars, not to banks. With stablecoins, anyone can plug into a DeFi lending protocol and lend money to generate returns higher than 0.01%, or whatever they’d earn in their savings account.

For this opportunity to even sniff the TradFi interest income opportunity, a lot needs to happen. For one, DeFi will need to begin to touch real world assets (RWA) like cars, small businesses, and yes, mortgages. There are a lot of challenges there, but there are also a lot of smart people working to solve them.

The technological building blocks are starting to come into place, but the biggest headwind won’t be the technology, it will be the law. City Councils will need to recognize NFT Titles. The Federal government will need to come out with clear regulation. Battles will be fought in the court. “This happened with the internet, too,” Jeremy pointed out, before the internet became the fabric of everything that it is today.

In interviews, Jeremy applauds the US government’s approach to regulating the internet. When it was first taking off, government officials talked about making people and businesses apply to be able to create a website, but luckily, they chose to let it remain open. The internet we know and love today owes a debt of gratitude to those early regulatory decisions. Today, stablecoin regulation is at the same inflection point internet regulation was at two decades ago.

Open or closed?

Government-run (Central Bank Digital Currency or “CBDC”) or commercial?

As more people begin to use stablecoins to transact and borrow and lend and get paid and do all sorts of things online, as consumers get more comfortable with the technology, it’s hard to imagine that they’ll want to go back to the way things were.

They’ll want to tap into liquid global pools of capital to borrow money to buy a house at a lower rate than they can get from a bank, instantly and permissionlessly, and they’ll want to be able to directly earn more from their money than they’re able to get from their bank account. This will likely eventually be true in the US, and it will likely be useful to people in other countries, where mortgages are harder to come by and more expensive, far sooner.

As leading DeFi protocols continue to demonstrate their sturdiness in volatile markets, and as the interfaces improve, consumers and institutions alike will get more comfortable with this online financial system. That will take time, and a lot needs to be built and worked out.

But all of the current problems are solvable problems, particularly when the goal isn’t “total decentralization,” but rather “more widespread access on smoother rails.” Some people will go full DeFi, others will work with lenders who build some pieces on USDC rails. As with Circle itself, there will be a trade-off: some centralization in exchange for a range of improvements over the current system.

As always, the most impactful innovations will likely be the ones we haven’t even dreamed up. “There are huge categories that haven’t been created or even thought of,” Jeremy said:

We have programmable money, dollars as a native data type, a protocol you can use to interact, and computation environments (smart contracts) to write code that interacts with all of that. We have transparent, open, risk-managed credit facilities on the internet. We’re getting close to the point where USDC and other stables can transact with sub-second finality for a penny or two.

What can you do with all of that? I don’t know! We’re in the very early stages of discovering what people can build.

One thing is clear: to reach mass adoption, we’ll need better interfaces. An app that Jeremy thinks we’ll see, and will need to see for widespread adoption, is a superapp like Tencent’s WeChat that combines Decentralized Identity, Decentralized Social, messaging, stablecoins, payments, the ability to interact with tokenized IP, one view of the NFTs that have utility for you (and links to the places those NFTs have utility via tokengated commerce), and more. “But in order for that product to exist,” he said, “the things that provide those services need to exist.”

USDC is just one piece of infrastructure. For Circle to achieve its mission – to raise global economic prosperity through the frictionless exchange of financial value - there will need to be advances in commerce that uses NFTs, entitlements, reputation, identity, scalable zero-knowledge technology, and more. Jeremy readily admits that the current model where people can see your transaction history is not going to work.

But he’s optimistic that we’ll get to a place where USDC is baked into a new financial and internet system that was built in and for the internet age. I agree.

There’s a popular narrative among web3 skeptics that we don’t need crypto because banks and fintechs work just fine. Why would you need to send money abroad with stablecoins when something like Wise exists? I’m a big fan of, and investor in, fintech companies. Moving money has gotten much better in the last decade.

But the skeptics’ belief is essentially that we’ve reached the end of the road when it comes to financial innovation – that the FORTRAN and COBOL-based rails work just fine, and that it’s not worth trying to build new rails on technology developed in the past decade.

That is insane to me, and ignores the history of both financial and technological innovation. Of course the financial system will be refactored – whether it takes a few years or a few decades – and it seems as if USDC will be a big part of that.

At the same time, I don’t think that stablecoins will replace banks or fintechs. Sometimes, they’ll co-exist. Increasingly, as is already happening, fintechs will build smoother, faster, cheaper, more global products on USDC rails, and provide the necessary guardrails, compliance, interfaces, and all sorts of other things that fintechs do best.

And it won’t just be fintechs. As money and banking become embedded in more of the products we use every day, and new categories of products are created with new technologies, I expect that USDC will be a core piece of more and more companies’ tech stacks. That would mean more USDC in circulation, larger USDC reserves, and more interest income for Circle, without needing to push out the risk curve.

Taking the trust-first approach, and building a platform, isn’t the fastest way to get rich. But it’s the safest, and it’s the only way to ensure that USDC lives up to its creators’ vision of raising global prosperity, a world in which Circle’s technology powers a modern, more fair financial system.

Thanks to Jesse, Peter, and the Circle team for working with me on this piece, and to Dan for editing!

That’s all for today! See you back here tomorrow for some Weekly Optimism.

Thanks for Reading, Packy

So you're telling me Circle is already a $1B+ revenue ($50B+ of USDC*.02% interest rates on 3 month T-Bills) business with super high margins? That is incredible. Stablecoins are a real product that have created a real business with real cash flow.

I've had this day Circled on my calendar for a long time...