Web3 Use Cases: Today

Jumping Back Into the Web3 Debate

Welcome to the 2,539 newly Not Boring people who have joined us since the last essay! If you haven’t subscribed, join 133,524 smart, curious folks by subscribing here:

Today’s Not Boring is brought to you by… Causal

Our mission at Not Boring is to make the world more optimistic – but optimism needs to be paired with smart planning, and that’s where Causal comes in.

Causal is a spreadsheet built for number-crunching — financial modeling, business planning, but really anything involving calculations. It's like Excel minus the arcane formulas (no more Sheet1!$E$4 or VLOOKUPs), plus live data integrations (accounting systems, CRMs, etc), and really cool shareable dashboards.

Given current market conditions, every startup needs a solid financial model to steer the ship. I've worked with the Causal team to create the Startup Suite — a set of 4 template models for early stage companies:

They've put together detailed video walkthroughs for each model in their documentation. Use one of my templates above as a starting point, or click below to just sign up for the product and start playing around:

Hi friends 👋,

Happy Thursday! I was off earlier this week celebrating my dad’s 65th birthday with the family (happy birthday, Dad!) so we’re coming at you today with the first part of a two-part essay on web3 use cases, present and future.

When I flubbed a use case argument on Cartoon Avatars a few weeks ago, I unintentionally helped spark a debate about whether crypto actually has any real use cases. It’s been fascinating to watch since, as Zach Weinberg has successfully pigeonholed people into very narrow use cases to prove that the whole thing is overhyped. My conversation with Zach has lived rent-free in my head ever since, but the more I think about it, I’m most upset with myself for walking into such a narrow debate space and conceding so much. Today, as it stands, web3 has real use cases, even if some seem silly or early or flawed.

So today and Monday, I want to walk through some of the current use cases, and then explain why I believe that over the next decade, web3 will power products, networks, and models that will impress even today’s biggest skeptics.

To be clear: I’m not here to defend crypto as a whole, or to pretend to speak on behalf of everybody involved in the space. There are people who are actually building things who are much better champions. But I do think it’s a particularly good time to step back and take stock of this last cycle’s real use cases, and to share what excites me about web3 personally.

Let’s get to it.

Web3 Use Cases: Today

(If you want to support Not Boring and own a piece of the debate, you can buy a copy this essay as an NFT on Mirror for 0.01 ETH, a real use case in itself.)

Crashes aren’t only painful because of price declines, although it’s never fun to see your account balances slashed relentlessly, day after day. Crashes are also painful because belief drains from the market as quickly as cash does. And those who never believed in the first place rush in to fill the void with a chorus of schadenfreude-laced I told you so’s.

If you felt smart a couple of months ago, you feel less smart now. If you were proud to tell people about what you’re building a couple of months ago, you’re less proud now. Nothing you’re doing has changed – you didn’t get dumber, your idea didn’t get worse – but the sentiment has shifted around you. (The opposite is true, too: if you’ve been calling the top, calling crypto a scam or a bubble, you’re feeling very smart right now.)

That’s not to say nothing is different. The market has undoubtedly changed. The prices of BTC and ETH have tumbled 76% and 69%, respectively (nice). Many alt coins are worse off than that.

A big part of it is that macro conditions have changed dramatically. After two years of COVID-induced free money, the Fed is tightening rates. Worse, the US faces 8.6% inflation and there’s doubt that hiking rates will be effective in slowing it down. Worse still, there are supply chain issues and inventory issues and a war, which is bad in its own right and also bad because it means higher food and energy prices.

Growth assets are selling off in the private and public markets, big layoffs are a daily occurrence, and inflation is hitting people hard. Real world challenges, like struggling to put gas in your car or food on your table, are more important than a pullback in asset prices.

In the world we cover in Not Boring, no sector has been harder-hit than crypto and web3. In addition to declining prices, crypto implosions have wiped out peoples’ entire life savings. First, there was LUNA and USTerra, which Jon Wu explained in Not Boring:

I’ve seen tweets in which people describe having put their life savings into Terra to earn 20% yields via Anchor without telling their significant other and lost everything. Multiple people in Korea, where Luna was based, have reportedly committed suicide. It’s worse than reckless; it’s tragic.

Recently, the centralized DeFi (CeDeFi?) platform Celsius became insolvent…

People who put their money with Celsius expecting it to be safe are left wondering if they’ll ever get their money back, and if so, how much?

On the less explosive side of things, many companies are struggling with early tokenomic models that seem to have worked a lot better when prices only went up. NFTs have been a lot less attractive to potential buyers in this early bear market, too. OpenSea’s volume, which is representative of the larger NFT space, has plummeted in June:

The month isn’t over yet, but two-thirds of the way through, that’s a real drop. NFTs aren’t alone. The Total Value Locked (TVL) in DeFi is down 65% from a November peak of $107 billion to a current $37 billion total, according to DeFiPulse.

More shoes will undoubtedly drop. If ETH drops as much as it did in the last crash, it could end up trading in the $200s (not saying it will, but it’s not impossible). More funds will blow up. Companies and projects will go bust.

There are a lot of people on Crypto Twitter calling the bottom, calling this a generational buying opportunity, and maybe it is, but anyone pretending to know that with certainty is full of shit. One of the challenges of having money baked into the product, tradeable by anyone with an internet connection, is that it attracts a lot of grifters and false prophets.

While tech stocks (and startup valuations) and crypto prices are both down bad, there’s a big difference between the two. Even the most bearish people on tech generally are simply predicting that multiples will compress, prices will fall further, and some companies that haven’t been managed well could fail. They’re not calling for the end of tech. The crypto skeptics are loudly yelling that the whole thing was a scam all along, and that there’s no value in the space whatsoever.

While some of the vitriol is a proportionate response to the grifters who’ve been telling non-crypto folks to “have fun staying poor” or that they’re “ngmi,” a group I hope gets washed out in this bear market, the constant onslaught of skepticism from a lot of smart people (and, of course, some talentless hacks piling on) has to be making some people who are in crypto for the Right Reasons™️ question whether they should be in it at all.

So I was staring at my computer on Saturday, trying to figure out what to write in this environment, and doing what I do when I can’t think of anything – mindlessly scrolling Twitter – when I came across this tweet from my friend and Every co-founder Nathan Baschez:

Plenty of people replied with examples of people who’ve kept tweeting and writing useful things through the crash – and pointed out that what he was saying was true of equity investors, too – but the point stands. It’s easy to tweet and write when things are going well; it’s harder to do it when things are going badly and the bears are waiting to pounce on any glimmer of optimism. But if the thing that many of us have been saying the whole time – that we’re not excited by the price, we’re excited by the technological and social aspects – then now is the very best time to write about web3, when price clearly can’t be the exciting thing.

Let’s discuss some use cases.

The Debate

Over the past few weeks, Logan Bartlett’s red hot new podcast Cartoon Avatars has taken my corner of the internet by storm with a series in which Flatiron Health co-founder and Operator Partners GP Zach Weinberg debates crypto people about whether there are any real crypto use cases. The series kicked off when he wiped the floor with me in a debate over DeFi use cases a few weeks ago, and over the past two weeks, Mike Dudas and Jon Wu have tried their hands at explaining what about crypto excites them the most (more successfully than I did).

Despite the egg on my face, I’ve been a big fan of the ongoing conversation; debate is healthy, and I think it’s been useful to have to think through where the logic holds and where we’re relying a little bit more on hope. I’ll have a little Zach Weinberg asking questions in my head whenever I look at an investment now.

Over the weekend, Zach summarized his position on Twitter:

Essentially, he believes that there’s too much hype and risk relative to actual valuable use cases being created, which is particularly problematic when regular people are able to invest and/or speculate, and that the tens of billions of dollars VCs are pouring into the space could be better deployed elsewhere.

On the second half of his point, I understand the argument that dollars could be more productively deployed to other things – it would be great if VC-backed entrepreneurs could fix education, healthcare, energy, housing, infrastructure, and other critical industries. I’m investing in all of them at Not Boring Capital. But it’s also a red herring.

Since the Global Financial Crisis, we’ve lived in a regime of cheap and abundant capital; very few strong projects have failed for a lack of funding. In fact, as this crash in both public and private market valuations implies, investors pumped too much money into too few strong companies. There’s probably some blame to be doled out to the government for not doing things to funnel all of the excess cash to infrastructure, education, and other projects that would improve the lives of all Americans, but I don’t think there are a lot of VCs who were choosing between building new bridges or investing in DeFi protocols. LPs don’t seem to be choosing to fund web3 VCs instead of climate VCs; they’re doing both. There’s simply been more money sloshing around, and it’s the fault of the whole system, not web3 or any one industry, that we haven’t emerged from this period into this world:

There’s a related point, which is that people who could be working on solving really hard atoms challenges end up working in web3 instead. This, too, is overstated. According to a report by Electric Capital, there were 18,416 monthly active developers in web3 in December 2021. Google alone employed over 27,000 engineers the last time it reported the figure in 2016. Combined, Google and Meta employ nearly 200,000 people, and it’s pretty easy to make the argument that each marginal person at those companies contributes a lot less than each marginal developer in web3.

Back to the first part of his argument: hype and risk. I’m on the fence here. The hype isn’t unique to crypto. If you’ve been reading Not Boring for a while, you probably have this chart seared into your brain:

The Gartner Hype Cycle describes the path that practically every new technology follows. If you know of a new technology that hasn’t gone through this cycle, drop it in the comments. A technological breakthrough occurs, people think it’s going to change everything, they realize that it’s not going to change everything, and then they figure out the things it will actually change.

The tricky part about crypto versus, say, large language models or homomorphic encryption, is that regular people can easily invest in crypto projects and regular people cannot easily invest in large language models or homomorphic encryption. Compounding that trickiness is that, because people can invest in crypto projects, the people who have already invested in those projects have an incentive to try to convince other people to invest in those projects, which is why Crypto Twitter is filled with pictures of rainbow charts and confident predictions of $100k BTC, $10k ETH, and $1 DOGE. Crypto is simultaneously a technological innovation and a financial innovation. So there’s even more hype than there would be for a normal new technology, and this time, it comes with financial risk.

On the one hand, that leads to people buying at the top and overleveraging and getting rekt (although this, too, is not unique to crypto), which is bad. Let me say this loud and clear: never trade on margin if you don’t know what you’re doing and never invest more than you can lose, and do your own research, in stocks, crypto, or otherwise.

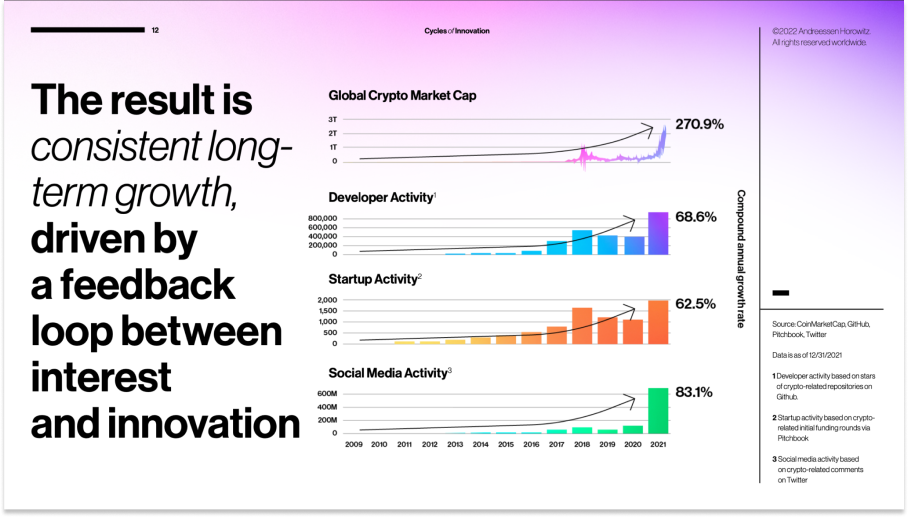

On the other hand, the enhanced hype can be productive, spurring faster iteration and innovation. In its State of Crypto Report, a16z Crypto (where I’m an advisor) explained research that they’d done showing that cyclical increases in price lead to interest in the space, which attracts new entrepreneurs who create new startups and projects, which drive the next cycle.

They call it the Crypto Price-Innovation Cycle. In each cycle, even after prices have dropped, more developers and startups remained in the ecosystem than there were before the cycle began.

Those entrepreneurs build better infrastructure and novel applications, and turn potential use cases into real ones. And that’s the crux of the debate: whether there will ultimately be use cases that justify the hype, risk, and dollars pouring in.

I believe that there will be, and I’ll lay out why, in two essays:

In this piece, I’ll talk about early but real use cases that exist today, but that make trade-offs.

On Monday, in Part II, I’ll talk about what excites me in the near-term and in the future:

There’s a wave of real use cases at the application layer on the horizon that won’t need to make the same trade-offs.

A system of permissionless innovation and composability will open the gates for unpredictable use cases (but we’ll try to predict some, anyway).

That last point – essentially “We’re still so early!” – is a bad argument on its own, but can be delicious icing on a well-thought-out cake. It’s the part that excites me the most, but I understand that it’s not enough on its own. There needs to be a road from here to there. So we’ll start with today.

The Use Cases: Today

It’s not surprising that web3 startups today seem silly or overhyped. They’re part of a long lineage.

When Facebook bought Instagram for $1 billion in 2012, some people thought it was crazy. The comments on the Dealbook article announcing the acquisition are funny in retrospect. Among the more level-headed ones – “They have not gone public yet, so they are free to value Instagram however they like” – are the familiar bubble calls:

A decade later, when Ben and David at Acquired ranked the ten best acquisitions of all-time, Facebook’s Instagram purchase ranked #1 on the list. They calculated that, at the time of recording, it contributed $153 billion to Facebook’s market cap. That’s more money than every VC combined has invested in web3 startups. And to be fair, it’s just a photo sharing app. It lets people post thirst traps, facilitates commerce, and runs a killer ad business.

A lot of the negative sentiment about the Instagram price tag was that the company didn’t make any money – not just profits, but revenue. The web2 social media model was to get a lot of users first, and then figure out how to make money. It worked for Instagram, Facebook, Snap, and others. Even Google ran that playbook, and became the business it is today thanks to its acquisition of DoubleClick; in the beginning, Google was just cool tech without a great business model.

Web3 startups take the opposite approach: a lot of money first, and then, hopefully, a lot of users. Just like it was uncertain that the prior generation of companies could transition from eyeballs to dollars, it’s uncertain that today’s web3 startups will be able to transition from dollars to eyeballs.

That’s the trade-off web3 projects are making today: financialization versus user experience.

Many web3 projects today lean too hard on the shiny new financialization levers – partially because it’s an easier way to make money, partially because that feels like the point, partially because it’s still early and great user experiences take time, and partially because the infrastructure is still being developed – but that doesn’t mean that there aren’t any use cases today. We’ll start with the most straightforward use cases: the ones where we can take what’s happening at face value without extrapolating out any further.

Today

It’s useful to look at early web3 products through the lens of Clayton Christensen’s theory of disruptive innovation.

On many dimensions and for many users, new products are worse than their incumbent counterparts, but for an overserved or ignored portion of the market, the new entrant’s offering is “good enough.” Companies that prove to be disruptive find a foothold with a small group of those overserved, ignored users, and then expand upmarket.

Disruptive products often start out looking like a toy, and it’s easy to point out their shortcomings, but those shortcomings are often fixable misdirections. The magic is in looking for the things that they do better than existing options for some users.

Today, most popular web3 products are in that early phase. They’re not perfect, but they’re “good enough” for a certain group of users. More centralized, robust, and secure products exist that do a lot of the things that web3 products do, but that don’t serve the needs of that group well. So web3 products are finding a foothold with that group. The use case proof is in the usage.

Today, as it stands, NFTs are a real use case in the way that Instagram is a real use case or art is a real use case or even gambling is a real use case. Simply, NFTs give physical properties to digital items, making them unique, ownable, and tradeable, in addition to digital properties like programmability and composability. Over time, NFTs will represent things that are more useful than the things they represent today, but even today, the collectibles use case is a real one.

That same chart that I showed above to highlight the slowdown in NFT sales can be interpreted more positively, too: on OpenSea alone, 1.8 million accounts have purchased $31.9 billion worth of Ethereum-based NFTs, $31.3 billion of which occurred in the last year alone.

Do some people account for multiple of those 1.8 million accounts? Sure. Is some of that volume wash trading? Sure. Is some of the art ugly? That’s in the eye of the beholder, but yes. Is a good chunk of the buying speculation? Of course.

But NFTs are a broad category, and within it, there are fascinating models emerging.

As one example, Nouns describes itself as “an experimental attempt to improve the formation of on-chain avatar communities” and an “attempt to bootstrap identity, community, governance, and a treasury that can be used by the community.” Every day for the past 347 days, one Noun has gone up for auction, and anyone in the world with enough ETH is able to participate in the bid.

The ETH from each sale goes into the Nouns DAO’s treasury, all Nouns holders become members of the DAO, and each holder gets to vote on how to allocate the growing treasury (currently at 26,568 ETH or $29.86 million) – one vote per Noun. The DAO has voted to allocate to projects ranging from sending a 3D printed Noun to the International Space Station to bringing luxury Noun sunglasses to market to donating 100 ETH to UNICEF for Humanitarian Aid Assistance in Ukraine. They’re earning real money, and allocating it collectively to off-chain recipients, occasionally to make physical products.

This week, at NFT NYC, another project, Doodles, announced a round of funding from 776, the addition of Pharrell as Chief Brand Officer, a Doodles album (produced by Pharrell) and the kickoff of Doodles 2. It seems as if Doodles is trying to build a web3 Disney.

You might think NFTs are the dumbest thing in the world, but it’s hard to argue that $31.3 billion of volume in a year doesn’t represent a real use case for some people. And OpenSea isn’t the only marketplace. The second largest, Solana-based Magic Eden, has more than 60k transactions per day and just announced a new round of funding at a $1.6 billion valuation, in this market.

Bringing it full circle, Instagram itself announced in May that it was starting to test letting creators and collectors showcase their NFTs.

NFTs are still a very young technology, but they’ve already driven a tremendous amount of volume and inspired a ton of creativity, not just in terms of art, but in terms of the technology itself. On Monday, we’ll discuss some future applications of NFTs. That said, I understand that NFTs might not satisfy a skeptic, so we’ll keep going.

Today, as it stands, decentralized exchanges (DEXes) like Uniswap are real use cases in the way that Robinhood is a real use case or the New York Stock Exchange or Chicago Mercantile Exchange or Nasdaq is a real use case. DEXes create liquidity for any number of token pairs without the need for a central party in a way that wasn’t previously possible.

Uniswap, the largest DEX, created an exchange on which anyone can show up with a wallet and trade any pair of tokens against each other, permissionlessly, without going through a central party or moving through a central order book. It all works on math, incentives, and code, and it’s working at scale. Whether you personally believe it’s good or useful to have an exchange that provides liquidity on tokens is besides the point (although I personally believe it is); the volume speaks to the fact that a lot of people find the use case valuable.

On May 24th, Uniswap announced that it had passed $1 trillion in volume in just three years (although they didn’t need to announce it; all of that data is available on-chain).

Amazingly, it’s done this with a team of about 50 people at Uniswap Labs, the company that created the protocol (Robinhood employs ~3,800). The protocol itself is governed by UNI token holders, many of whom received governance tokens in a 2020 airdrop just for using the DEX. We’ll talk more about why this is important on Monday, but as a preview, a system that lets small teams build scaled products by tapping into existing infrastructure frees a lot of people up to innovate, build different things, or work on climate. And Uniswap itself is infrastructure, which means that others can permissionlessly build on top with even fewer resources.

Uniswap might be what Zora co-creator Jacob Horne calls a Hyperstructure. From his piece by the same name:

Hyperstructures take the form of protocols that run on blockchains. Something can be considered a hyperstructure if it is:

Unstoppable: the protocol cannot be stopped by anyone. It runs for as long as the underlying blockchain exists.

Free: there is a 0% protocol wide fee and runs exactly at gas cost.

Valuable: accrues value which is accessible and exitable by the owners.

Expansive: there are built-in incentives for participants in the protocol.

Permissionless: universally accessible and censorship resistant. Builders and users cannot be deplatformed.

Positive sum: it creates a win-win environment for participants to utilize the same infrastrastructure.

Credibly neutral: the protocol is user-agnostic.

In practice, that means that Uniswap might be a protocol on top of which others are able to build new applications, like a TCP/IP or SMTP for liquidity whose community members accrue value through the threat they have (but should not, according to Horne, exercise) to flip the “fee switch” and start extracting value from the system. Instead of for-profit, Horne calls this new model “for-public.”

But we’re getting ahead of ourselves. That’s the future. We’re still talking about today.

Today, as it stands, DeFi protocols are real use cases in the same way that lending is a real use case. The most successful power a liquid, global marketplace for peer-to-peer or pool-to-peer lending and borrowing without a bank sitting in the middle adding time and cost to the process.

Protocols like Compound, Aave, and Maker let people lend or borrow against their crypto holdings. While more centralized DeFi products like Celsius have collapsed, these protocols have held up well through the downturn. Loans are overcollateralized, and when collateral drops as prices fall, the protocol liquidates borrowers. Certainly, some people feel more comfortable when there’s a person on the other side of the table who they can beg for just one more month, but for a portion of users, these protocols provide a real service. Even after the dip, Compound, Aave, and Maker have a combined $15 billion of Total Value Locked.

But, as Joe Weisenthal tweeted, a keen observer might point out that “nothing of economic value is being financed” by DeFi. That depends on your definition of economic value, but taking it to mean “real world assets,” Goldfinch is a “decentralized credit protocol for crypto loans to real businesses.” To date, over 200k borrowers have accessed credit across “India, Mexico, Southeast Asia, and more,” helping to address the very real developing world credit gap. Jia is attacking the credit gap as well, by providing blockchain-based loans to businesses in the developing world, and rewarding them with ownership for repaying loans.

Primitives that were built for internet money are now being used to support “real-world” businesses that otherwise would not be able to tap into the credit markets to grow their businesses.

Let’s keep going, to businesses that look like traditional internet businesses.

Today, as it stands, a talent marketplace like Braintrust is a real use case, in the same way that Fiverr or Upwork is a real use case. Braintrust is a minimally extractive talent network that both offers a better product and prevents against extractive take rates by using tokens to incentivize pro-network behavior. Because Braintrust is a decentralized protocol, third-parties will even be able to build their own industry- or role-specific applications on top of it.

Often, when people ask for a real web3 use case, they’re asking for an example of something that looks like a model that they’re used to or that connects to the “real world.” Braintrust, a portfolio company I wrote about in January, is my favorite example of such a use case.

Braintrust is a user-owned talent marketplace that connects high-skilled, often technical people with jobs at companies like Nike, NASA, and Porsche. The average project on the network is worth $77,630 and lasts 217 days. The money and time at stake make talent networks an ideal first use case of the user-owned marketplace model because participants have so much skin in the game.

Currently, most of the activity on the network takes place in local currency, but participants in the Braintrust ecosystem, including Talent, Clients, Connectors, and Vetters, can earn BTRST tokens for doing things that are good for the network, like screening applicants or referring candidates, and can stake those tokens for advantages in the network. Talent might stake BTRST on a certain job opening to prove their seriousness and increase their chance of getting hired, which has real monetary value, and Clients might stake BTRST to increase the visibility of their job listings to attract more Talent. Because Braintrust can use tokens to get work done and attract new demand, it can keep the take rate it charges at an industry-low 10%, making it more attractive to potential Clients and Talent.

All of that gives Braintrust small but meaningful advantages over larger incumbents, but most importantly, over the long term, user-ownership means that Braintrust won’t ultimately build up network effects and then charge more extractive fees because for that to happen, the users would have to vote to charge themselves higher fees. A user-owned co-op might also protect against extraction, but gives up flexibility and openness to do so.

It seems to be working. When I wrote about Braintrust in January, they had facilitated $37 million in Gross Service Value (GSV). Five months later, it has doubled GSV to $74.4 million.

In a similar vein, other startups are building user-owned networks for physical world products and providing what The New York Times’ Kevin Roose describes as “normie utility.”

Helium, the focus of a February article by Roose, is a decentralized wireless network for internet of things devices, with a 5G network coming soon. It started as a long-range peer-to-peer wireless network in 2013, but failed to gain adoption. By introducing the $HNT token, which hot spot owners earn every time their hotspot is used by the network, provided a strong enough incentive for people to install the devices. Today, as it stands, there are 867,190 hotspots in the network, and HNT has a $1.25 billion market cap.

In a similar vein, Not Boring portfolio company DIMO is building a “network of drivers like you who collect and share their vehicle data to learn more about their vehicle, save money, and build better mobility applications.” Instead of getting car insurance and plugging in your insurer’s car tracking device, for example, drivers can plug in the DIMO device, share their data, and let insurers bid on their coverage. It’s possible to imagine other applications, like a decentralized Waze or fleet management products, built on top of the DIMO network. DIMO even partnered with Helium to let drivers earn rewards for verifying network coverage while driving. Ultimately, DIMO’s goal is to be a public good that makes it easier for developers to build apps for any vehicle that make mobility cheaper and more efficient.

Or take stablecoins, the simplest use case. I have international LPs in Not Boring Capital who funded their commitments using the fully collateralized stablecoin USDC because the process of sending international wires was so onerous. While many people might feel more comfortable going through a bank that can reverse errors, some people are clearly OK trading risk for convenience, particularly because they know to send a test transaction first before sending the full thing. Fintech is a very large, very real industry built on the idea that the financial rails suck, and stablecoins are one way to make sending and receiving money suck less.

While it’s possible to send money in other ways, there are clearly people and institutions who appreciate stablecoins’ value prop enough to use them instead of incumbent solutions. There’s currently $155 billion of stablecoins in circulation.

The list of use cases goes on. Just yesterday, our portfolio company Vibe Bio launched to fund cures for rare diseases with DAOs.

In an excellent post this weekend, Where are all the crypto use cases?, Evan Conrad highlighted real use cases, today, that include money not issued by a central government (“If you don't believe me,” he wrote, “then I'm happy to sell you the laptop I'm writing this on for 1,000 ETH instead of 1,000 USD”), cheap loans (Compound, Aave, Maker, and other DeFi platforms have held up well even during turbulent market conditions), Filecoin (storage that’s currently 0.0011% the cost of S3), Lab DAO, Radicle, Helium, Toucan, and Golden. These products all have real users today and are solving issues that have nothing to do with crypto itself, from finding lab space to trading carbon credits to creating a “decentralized canonical knowledge graph.”

As Conrad pointed out, smart contracts are different than blockchains, and the technology is still less than seven years old (Ethereum launched in 2015). We’re still, as they say, so early.

To be very fair though, the number of people participating in web3 is still relatively small – there are around 30 million Metamask wallets, a good proxy for self-custody and interaction with applications beyond just investing. Many of the web3 use cases meant to “onboard the next billion users,” from gamefi or play-to-earn to web3 social media, really do feel rough and early. From Axie to Stepn to Bitclout, the first attempts to build web3 versions of gaming and social products to attract millions of “normal” users gained early traction largely thanks to the financial aspects of the products. On the user experience / financialization spectrum, they’re far to the financialization side.

Now we’re wrapping up one cycle and entering a bear market. Better infrastructure is on the way. Web2 entrepreneurs and triple AAA game developers, including many senior people, have recently entered the space. And the industry has seven years of lessons under its belt.

I think the next cycle will kick off when we begin to see the fruits of those forces: when web3 projects make user experience a first-class citizen while retaining their unique advantages. Or as Christensen would say, “delivering the performance that incumbents’ mainstream customers require, while preserving the advantages that drove their early success.”

Coming Next

Whether today’s most popular web3 use cases feel silly or legitimate is a matter of opinion. Even if you fall on the “silly” side of the spectrum, that only means that you find them silly, not that they’re not real use cases.

Of course, there are challenges, too, and it’s useful to face them head-on. This is the beauty of debate. It sharpens thinking, exposes flaws, and, when done right, helps illuminate the other side’s position. I understand where the criticism of web3 comes from better now than I did a few weeks ago, and I understand my own position better than I did then, too.

Biggie called it 25 years ago: Mo Money, Mo Problems. Baking money in from the start has attracted a lot of speculation and downright fraud that’s been distracting at best and destructive at worst.

Like the internet, crypto’s biggest challenge is that it’s full of people. People can be messy and selfish and weird and lazy and scammy. This thread captures some of the challenges well:

But crypto’s biggest opportunity, too, is that it’s full of people. People can be creative and resourceful and generous and collaborative. While there are real use cases today, what excites me most about web3 is what will happen as thousands of creative, resourceful, generous, and collaborative people build on each others’ work, and take lessons from each others’ failures, to fix shortcomings and make progress. (That’s why I love startups in general, not just web3).

Is what has been built in web3 to date worth the hype and risk? No, of course not. But innovation is a compounding process, and the next seven years will bring more useful use cases than the first seven. I believe the ultimate impact of all of this innovation will be deeply net positive, but only time will tell.

On Monday, we’ll talk about a bunch of the things I’m excited about in the short-term – social, gaming, decentralized storytelling, regenerative finance, decentralized science, tokengated commerce, decentralized identity, zero-knowledge proofs, and more – along with wilder and more meta ideas and changes that I think web3 has the potential to help unlock.

What are you most excited about? Let me know on Twitter.

Thanks to Dan for editing!

Alt Mint

Alt is something we can all agree on: it’s backed by both Not Boring Capital and Zach’s Operator Partners. Yesterday, Alt launched Alt Mint, which lets you mint NFTs backed by physical trading cards. Holders have the right to redeem their NFTs for trading cards ranging from $700 - $10,000 in value or to hold on to them for access to community benefits and rewards. Thirty Not Boring readers received VIP spots, but if you missed out, you can mint today: Mint Your Alt Mint

That’s all for today. Have a great weekend and see you Monday!

Thanks for reading,

Packy

When you write with so many buzzwords rather then layperson explanations you hinder rather then help your case. Your writing on Braintrust is a great example. Again, you hawk out "user owned" as if everyone should nod their heads when you say it.

I still can't figure out the crypto angle.

By using and referring talent to the platform, users can earn tokens. It’s never clear, however, what these tokens gate or purchase. Users on the platform may price services in terms of the token, but they’d only do so if the token has purchasing power in real terms. You write that Braintrust may offer “hints at future benefits for token holders; these might be things like educational content, free software, or coaching.” If so, the token’s price reflects the value of these services. I find it excruciatingly difficult to believe these services are worth much, so, in turn, the token isn't worth much.

You're resting the web3 use case on a tradeable loyalty program?

Good overview of use-cases, and looking forward to next chapter...

One big deficiency of Web3 though, as it stands right now, is that by definition, blockchain and all the associated Web3 infrastructure (including IPFS etc) are all based on publicly publishing the information to the entire world for transparency. In real-life, while this provides some benefits with data authenticity, etc, only some very limited use-cases can be realized on top of public information alone. Data privacy/confidentiality are necessary elements for realizing most of the use-cases with real-world utility value - with or without data authenticity.

In Web2, this data confidentiality for private information is always enforced through centralized services, and there is no equivalent model available in decentralized web3. No wonder that even Web3 services prefer centralized model for any kind of confidential or sensitive information. And in spite of degenerating to a hybrid web2/web3 model, they still suck at it, and are far worse than their web2 counterparts (including most of the wallets themselves - the supposed gateways to web3 world!).

If web3 wants to realize its true potential (which is indeed enormous!), and really get ahead of web2, this is the best time to address some of these foundational elements by adopting a decentralized model for data privacy/confidentiality (which is feasible, and even better for web2 itself). Web3 really needs to take the lead on data confidentiality in decentralized way, as its a necessity there due to its decentralization promise, rather than just a nice-to-have for centralized web2.