Welcome to the 974 newly Not Boring people who have joined us since last Monday! If you aren’t subscribed, join 44,858 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts (in ~30 mins)

Hi friends 👋 ,

Happy Monday! We have a special one for you today.

Back in January, I wrote a piece about Alibaba. Lillian Li, whose writing on Chinese tech I’d read and respected, but who I’d never met, DUNKED on it on Twitter.

She said that “the piece missed local context.” Which, fair. She also wrote a more complete response on her Substack, Alibaba: from growth to value.

I loved getting Lillian’s perspective -- one of the reasons I write is so people who are smarter on a particular topic share their knowledge. And when it comes to China tech, Lillian, who worked as a VC in Europe but is now based in China, is as smart as it gets. She writes a great newsletter called Chinese Characteristics. You should subscribe if you’re interested in China tech, and you should be interested in China tech:

Lillian and I got to know each other after that exchange. We decided to team up. Reprise the ol’ bull and bear schtick, but together this time. In other words, we shifted our debate method to Real-Time Engagement (I promise, this will make sense /maybe be funny in a minute).

Let’s get to it.

Today's Not Boring is brought to you by Public

As you read above, the fastest way to get smarter about investing is to put your ideas out there and get dunked on by … errr... have a conversation with other smart investors. That's why I use Public.

Public is an investing app AND a social network for talking about business trends, and the social features make it fun and easy to share ideas.

I'll be discussing today's piece on Public. Hit the link below and follow me @packym to join the conversation. Btw, if you’re looking to transfer your account from somewhere else, they’ll even cover the fees.

*Valid for U.S. residents 18+ and subject to account approval. Transfer fees covered for portfolios valued at or over $150. See Public.com/disclosures/

Agora: Bull & Bear

In 1997, two Chinese engineers joined the founding team at early video conferencing startup WebEx. A decade and a half later, each started his own company.

One, Eric Yuan, founded a company you’re all too familiar with: Zoom. The other, Bin “Tony” Zhao, founded Agora.

If you’ve joined a conversation on Clubhouse , attended a virtual event on RunTheWorld, or binged livestreams on Bilibili you’ve experienced Agora. It’s been sitting there, in the background, making sure the audio and video come through clearly.

Agora builds real-time audio and video capabilities and delivers them as a Software Development Kit (SDK) and Application Programming Interface (API) for app developers. It’s an API-first company that makes it easy for developers to add real-time video and audio into their product. Stripe for Real-Time Voice and Video Engagement, if you will. The company is so API that its ticker is API.

Agora is also a great excuse to cover a few different relevant topics:

API-first businesses and business models

Live video streaming and all of its use cases, like telemedicine and education

The audio chat wars

Because Agora sits in the background -- it’s a “picks and shovels” company -- it doesn’t care who wins as long as more people communicate, learn, heal, play, and “live real life online,” in real time.

Agora, dual-headquartered out of Shanghai and Santa Clara, went public in June last year. It was relatively quiet for its first six months as a public company, bouncing around the $3-6 billion market cap range, until investors picked up on the Clubhouse connection in January and sent shares soaring. In February, the company topped out over $12 billion before crashing after providing conservative 2021 guidance on its last earnings call.

Source: Atom Finance

Today, the company is trading at a $6.5 billion valuation on projected 2021 revenue of $182 million. It’s cheaper, but it’s not cheap. As Packy was browsing atom for its numbers, he was confused when he saw that FY21 consensus Enterprise Value (EV) / EBITDA was 4.06x. Seemed like a steal. Then he looked more closely: that’s 4.06 thousand times EBITDA.

It’s less than eight years old and still growing quickly (74% YoY revenue growth) and most of its revenue still comes from China (~80%). It’s young and fast-growing enough that whether you’re bullish or bearish on the company depends less on today’s metrics, and more on how you think about its growth potential and defensibility going forward. There’s a good case to be made on both sides, and we’re going to do just that.

Packy’s going to take the bull case, and Lillian’s going to take the bear case. Then we’ll fight it out and let you know where we end up. To get there, we’ll cover:

Agora’s History

$API’s API

China’s Livestreaming Boom

What Agora Looks Like Today

The Bull Case for Agora

The Bear Case Against Agora

Bull or Bear?

To kick it off, let’s go back to the granddaddy of online video communication: WebEx.

Agora’s History: From WebEx to YY to API

Who knows what video communication on the internet would look like today if WebEx just embarrassed its employees a little less.

Eric Yuan explained to Bessemer partner Byron Deeter, “Every time I talked to a WebEx customer, I felt very embarrassed, because I did not speak with a single happy WebEx customer.”

After fourteen years at WebEx, the last four under Cisco, which acquired WebEx in 2007, Yuan left to found Zoom in 2011. He set out to build what he couldn’t convince Cisco execs to let him build at WebEx, a new version of the product rebuilt from the ground up with customer happiness in mind.

Bin “Tony” Zhao, another WebEx founding engineer had similar feelings. After building and releasing real-time audio sessions, he said on GGV Capital’s Next Billion Podcast, “I started to regret taking that job, because I got a lot of complaints after the first release, and I realized there are some complaints that I believe I cannot solve at that time.”

Zhao didn’t have Yuan’s patience. He left in 2004 to start NeoTasks, which he describes on his LinkedIn page as: “P2p streaming technology and service provider for various companies in media, advertising, video sharing industries.”

In 2008, Zhao sold NeoTasks to Chinese streaming site YY.com and joined the company as CTO. That experience shaped what he would build at Agora.

YY during the early 2010s was China’s Second Life. The documentary called People’s Republic of Desires gives a glimpse into this brave new world where fortunes were made and lost overnight. According to Interconnected’s Kevin Xu, “Is one of the first livestreaming platforms to reach scale in China, if not the world. It is arguably one of the first instances where people were ‘living real life online.’” Like Tencent’s QQ, which was early to new forms of online monetization like avatars and digital gifting, YY was early to gifting and tipping with virtual goods and real money, a behavior that’s now common online.

The company also pushed the boundaries on real-time engagement. Xu told TechBuzz China’s Rui Ma that under Zhao, YY could handle 8 million concurrent users, and up to 100k in the same room, back in 2011. That year, it handled 421 billion voice minutes, more than Skype.

After working in B2B at WebEx, YY opened Zhao’s eyes to the potential of the consumer internet. He told GGV’s Next Billion Podcast:

I start to realize this technology is not going to be only sitting in the conference room, not only serve the purpose for people to negotiate or discuss certain business topics, it actually helped people to live online. Like they can play, they can have a party, they can sing karaoke, they can actually make friends online through video chat, audio chat. I can envision from there, people can actually live online and that’s part of the inspiration that led to Agora as well.

In 2013, realizing the opportunity to accelerate the transition to rich online experiences through real-time audio and video, Zhao left YY to start Agora. Unlike Yuan, who wanted to build a better version of the user-facing product the two built at WebEx, Zhao wanted to build products that helped developers build new user-facing products like WebEx and YY. He wanted to build APIs.

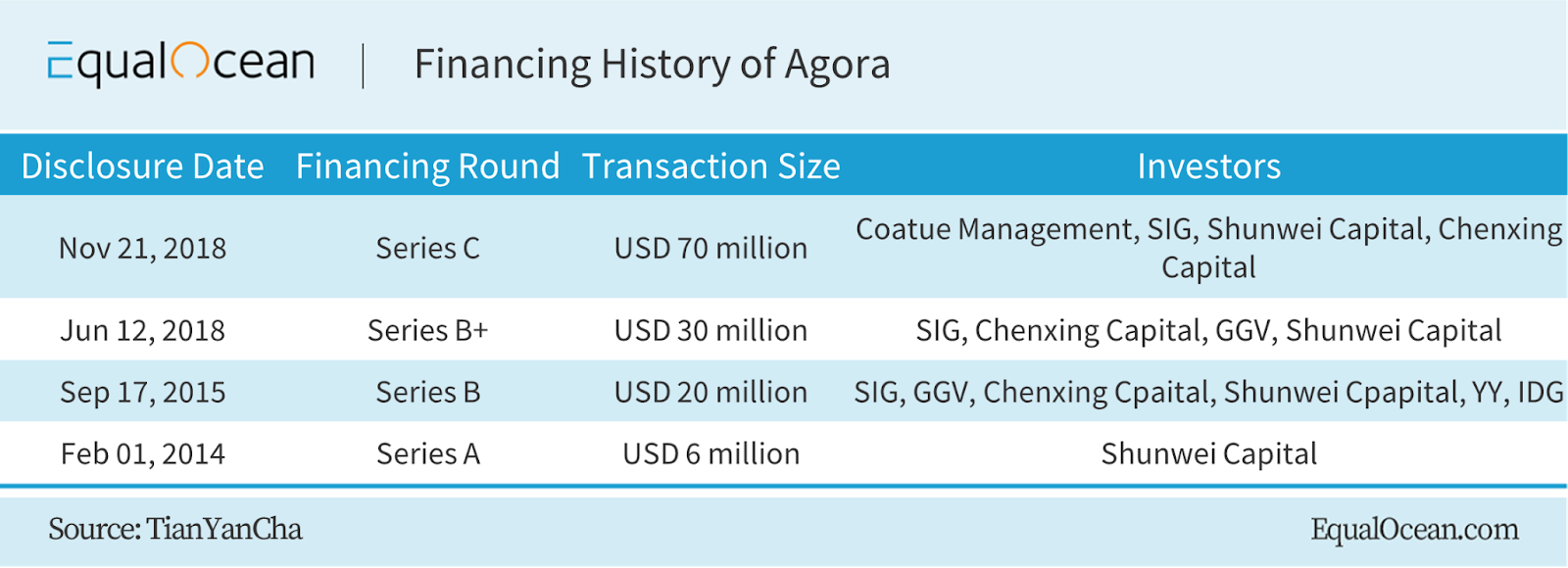

Like Yuan, Zhao’s track record made fundraising easy. He raised $6 million a couple of months after forming the company, and went on to raise $126 million from top investors including SIG, GGV, and Coatue.

Zoom was praised for raising so little -- $146 million -- before going public. Agora raised even less. Zoom took eight years to go public, Agora took less than seven. But while Zoom is a household name, chances are you haven’t heard much about Agora. That’s because of what it builds, and who it builds for.

$API’s APIs

Agora builds APIs and SDKs for real-time voice and video communication. It’s one of a growing number of Communications Platforms as a Service (CPaaS) companies, along with Twilio and Vonage, and more specifically bills itself as a Real-Time Engagement Platform as a Service (RTE-PaaS). (This is getting out of hand). It provides a Software-Defined Real-Time Network (SD-RTN) solution to deliver high-quality video and audio across a wide range of devices and environments. (OK, I’ll stop.)

With the acronyms out of the way, what does Agora actually do?

Like any good API-first company, Agora lets developers build some superpower into their products with a few lines of code. Stripe lets companies accept payments. Stytch lets them onboard and authenticates users. Agora lets them embed high-quality real-time audio and video.

Agora is not for static video or audio. The next YouTube, Netflix, or Spotify won’t be built on Agora. It’s for interactive, real-time video and audio, like one-to-many livestreams, audio chat rooms, or one-on-one use cases like telemedicine or tutoring.

Before Agora, and even occasionally today, companies spun up their own products by building on top of the open source WebRTC standard. WebRTC is built on the public internet, which is a “best-effort network” - it will make the best effort to deliver your data. In many cases, that best effort is not good enough, leading to laggy or glitchy video and audio. If your business relies on video and audio, you need a better solution.

That’s what Agora built. According to analyst Richard Chu:

Agora builds on this (WebRTC) with over 200 co-located data centers globally, dedicated to processing real-time audio and video data. To further improve performance, Agora uses intelligent algorithms to monitor requests and optimize data transmission paths to ensure low latency (~300ms) and resilience to packet loss (up to 70%) which ultimately translates into a superior end-user experience. This virtual overlay network is called the SD-RTN.

Agora does a ton of engineering work and spends a ton of money on co-located data centers behind the scenes to make real-time audio and video just work. The result is that someone on WiFi in Ghana and another person on 4G LTE with spotty signal in Florida can sit in the same Clubhouse room with thousands of other people and hear the conversation crystal clear.

In fact, Clubhouse was apparently built in a week on top of Agora’s voice APIs. Because Agora’s product is an SDK and over 200 specific APIs, all of which work seamlessly with a wide range of programming languages and devices, it makes something previously expensive, slow, and complicated, cheap, fast, and easy.

In fact, one Agora customer interviewed on a Tegus expert call said that his company tried to spin up its own product using WebRTC, but shifted course when they achieved only 80% reliability internationally. After building on Agora, he said that going back to WebRTC to save money is “probably not a feasible option in a way that we want to focus on what we're good at as a company.”

That’s the power of API-first businesses. As Packy wrote in APIs All the Way Down:

This is the beauty of API-first companies. They allow customers to focus on the one or two things that differentiate their businesses, while plugging in best-in-class solutions everywhere else.

Instead of wasting time trying to re-solve all of the hard technical problems, not to mention setting up 200 co-located data centers around the globe to ensure global reliability, Agora’s customers just write a few lines of code to plug in the best technology on the market, which constantly improves as Agora’s team ships updates.

Plus, Agora’s customers pay as they go, making it easy to get started.

Agora is free for the first 10,000 minutes each month, and afterwards, it charges per 1,000 minutes, with different rates for different products and quality levels.

It applies automatic volume-based discounts: free up to 10k minutes, 5% off from 100k-500k, 7% off from 500k-1mm, and 10% off from 1mm-3mm.

Putting that in perspective, assuming that Clubhouse gets the 10% discount and nothing special on top, each hour-long Clubhouse room with the max of 8,000 people in it costs $427.68.

The same room in standard video would cost $1,723 per hour, for standard quality. Premium would run you $3,883 per hour. It’s no wonder Clubhouse’s founders have said they want to keep the product-audio-only. Video is expensive!

While Agora can serve all sorts of use cases -- one-on-one telemedicine consultations, audio rooms, in-video-game chats, and more -- its bread and butter, and where it makes the most money, is on one-to-many video livestreams.

It’s hard for westerners to appreciate the magnitude of the livestreaming opportunity without experiencing it firsthand, but it’s central to the Agora thesis. Luckily, Lillian can give the local perspective.

China’s Livestreaming Boom

Saying livestreaming is big in China is akin to calling your phone a smartphone. Technically correct but so obvious it’s redundant. Since the advent of 4G and the roll-out of 5G, livestreaming and short videos are the two new mediums of the Chinese internet.

As a delivery mechanism, since 2015, livestreaming has come to encompass entertainment, education, socialisation, and, bolstered by COVID-19, commerce. In 2020, 560m people in China watched livestreams -- roughly 39% of China’s population -- and the Chinese market livestreaming e-commerce is estimated to be worth RMB 1.05 trillion ($165bn USD).

In China, livestreaming is the metaverse’s manifestation that’s eating the world. A leisurely stroll down the streets of Shanghai shows the donut light of livestreaming as a familiar fixture in boutiques. Occasionally, in particularly touristy or scenic spots, you’ll see livestreamers in the wild, talking to their fans who are flooding them with messages and gifts. In quieter cafes, students stream tutoring courses from superstar teachers. Every other night, Lillian’s mother tunes into her Chinese stock course with her favourite Key Opinion Leader (KOL) along with thousands of others on a WeChat mini-app. Whatever Chinese consumer app Lillian opens these days, be it Taobao or Pinduoduo or JD or Xiaohongshu (China’s closest equivalent to Instagram), the first prompt is to view the current livestreams for different products.

In Livestreaming monetisation models, Lillian wrote:

Livestreaming as a medium is a conflation of a product as well as as a distribution channel. It exists on a spectrum of being pure entertainment on one-side and a new go-to-market strategy on the other, with different kinds of monetisation models for each side.

While western startups have centred around the 'livestreaming as product' theme, China, with its enabling infrastructure in payment and fulfilment, have been quick to adopt livestreaming as a new distribution channel. This June's 618 Shopping Festival, saw Alibaba and JD.com report a combined total of $136.5 billion of livestreaming sales. Kuaishou surpassed 170 million daily active livestreaming shoppers in June and Pinduoduo also wants its ~500m users to start streaming as well. No longer just for small ticket items -- houses, cars, phones have all been sold during the lockdown -- livestreaming is climbing up the value chain.

Livestreaming’s journey looks a lot like our familiar Gartner Hype Cycle:

The great un-lock for China’s livestreaming industry was monetisation, but since then, it has entered the culture.

It has created an entire ecosystem of new livestreamers and the talent agencies (called Multi-Channel Networks) that spot talent and nurture them (or lure unsuspecting folks in to fleece them. New industries are grey areas).

Remember this video?

That’s a training camp for livestreamers.

Everyone is training to be the next Viya - who is essentially Oprah incarnated as a livestreamer. She can command 37m viewers (bigger than the audience for the Oscars or Game of Thrones finale) during a stream. Even Kim Kardashian had to pay a pilgrimage to the Don when she came on to Tmall to sell her KKW branded perfume. With Viya’s support, she sold out all 150,000 bottles in 1 minute. Was this a representation of one of social media’s biggest stars acknowledging her successor in the dawn of a new medium?

At this point, hopefully we’ve convinced you that livestreaming in China is big, and that livestreaming e-commerce is an established distribution channel. We should also highlight that it is also enabled by local factors in China including embedded digital payment system, robust logistics chain for next day delivery and returns, an ecosystem of Multi-Channel Networks (MCNs) cultivating talent, fandom culture which allows for a frictionless checkout and buying experience.

A lot of foundational pieces need to fall into place before the flywheel can really take-off for livestreaming e-commerce (which is a very specific form of livestreaming). This means, China’s livestreaming is not so much the future as much as a potential future for the world.

What Agora Looks Like Today

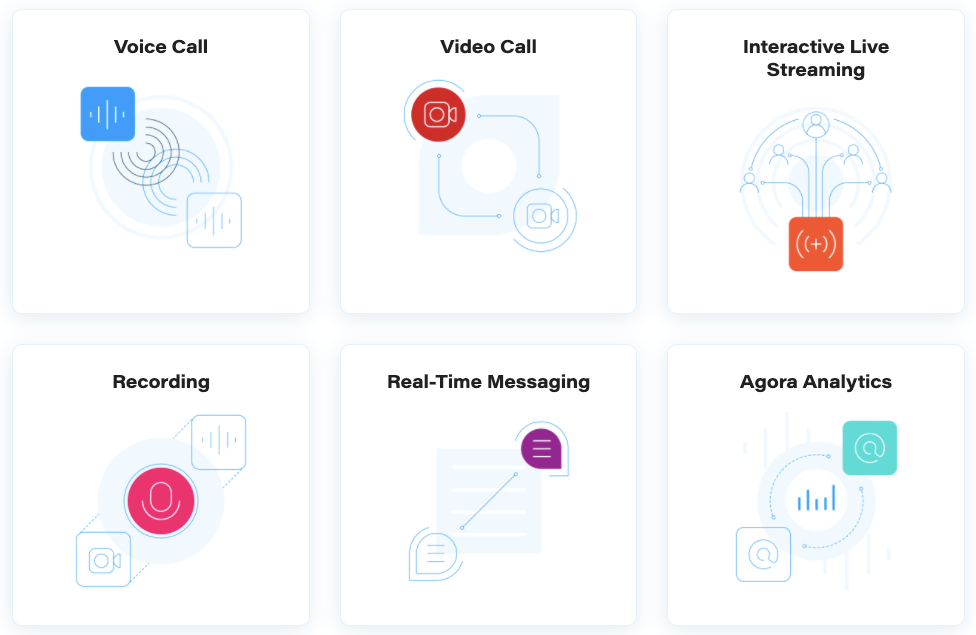

Livestreaming, and particularly livestreaming in China, has been Agora’s core focus. It’s the hardest to get right, and no one does it better than Agora for the price. But it’s beginning to diversify. Today, Agora offers the following product lines, all supported by its Real-Time Engagement platform:

As more competitors enter the space, we’re seeing an increasing verticalization and internationalisation of their product range. One focus area is education. As education moves online, and superstar teachers livestream to much larger classes than was possible physically, Agora is flexing its muscles to accommodate new needs.

At the beginning of the pandemic, the company worked with New Oriental Education, a publicly traded private education company, to bring the school online in a week, supporting classes as large as 20,000 concurrent students. It’s leaned into education heavily since. Later last year, Agora announced the release of flexible classroom, a low-code application targeting education providers. They’re augmenting the education product suite with acquisitions, including Easemob (an instant messaging API provider) and an interactive whiteboard API provider.

The company has also been on a roll in obtaining a slew of security clearances such as HIPAA, which allows them to serve the booming telemedicine market, and GDPR, which should give western companies more comfort embedding Chinese tech. The future of product for Agora will be moving towards greater localisation as it tailors their offerings to the requirements of regions outside of China.

Customers

In China, Agora focuses on education, entertainment, gaming, healthcare with emerging categories for finance, IoT, and e-commerce. As it makes an international push, it’s seeing success with customers who share those use cases, including Hallo in education, Clubhouse in entertainment, Unity in Gaming, and talkspace in telehealth.

Over the past couple of quarters, non-China revenue has grown from 20% to nearly 30%. Its Nasdaq listing and Clubhouse’s meteoric rise have no doubt helped give western customers more confidence.

Together, Agora’s customers now consume 40 billion minutes per month, or nearly half a trillion minutes annually. Those minutes translate directly into top line growth.

Financials

As its customers consume more minutes, Agora is growing tremendously quickly. Growth naturally slowed from a COVID-charged 166% in Q1 2020, but it still grew 74% YoY last quarter.

The company has solid gross margins of 60%, but they’re on a slight downtrend. As gross margins compress and SG&A and R&D expenses increase, Agora dipped back into the red for the past two quarters after being profitable in Q1 and Q2 of 2020. Those two quarters of profitability are a good sign that as top line grows, Agora can generate profits, but it has ramped up spend in R&D to continue to build its lead on the technical side and improve localisation, and SG&A to acquire more international customers.

Agora is an API-first business, which means it grows in two ways:

Acquires new customers

Existing customers’ usage expands

It tries to get into companies early and grow with them as they grow, and it’s working. Agora reported comically high 179% dollar-based net revenue expansion in 2020, meaning that the same customers spent 79% more last year than the year before on average, even accounting for any customers that churned. That’s top percentile stuff, and a testament to Agora’s stickiness.

That kind of growth and retention doesn’t come cheap. Based on Public Comps’ data, it’s the sixth most expensive company in the BVP Cloud Index at a 29.5x EV/2021 Revenue multiple.

But it’s also the fourth best based on the Rule of 40, a SaaS heuristic that says that companies are strong when their YoY revenue growth plus free cash flow (FCF) adds up to more than 40%. Agora is at 77%, behind only Zoom, Square, and Shopify among BVP Cloud companies, and right ahead of Twilio.

Agora is young, expensive, and fast-growing. It’s the only company in the BVP Rule of 40 Top 5 with a market cap under $10 billion. The next closest, Twilio, is 10x more valuable at $65 billion. Each of those companies exist in categories -- video conferencing, ecommerce, and messaging -- that are more mature than livestreaming. Can livestreaming catch up?

Agoraphilia: The Bull Case

I’m making my bull case on growth, not price. Agora is certainly expensive today.

To be an Agora bull, you need to believe three things:

Livestreaming will continue to grow

Agora has the best product in the market

It’s defensible against bigger incumbents and startups alike.

That’s it. Let’s take a look at each.

1. Livestreaming will continue to grow.

As Lillian highlighted, livestreaming is massive in China. Livestreaming ecommerce in China alone is a $165 billion market. That’s e-commerce sales via livestreaming. Market Research Future expects the livestreaming market more broadly to reach $247 billion globally by 2027, growing at a 28.1% CAGR between now and then. There are some major catalysts:

5G: As 5G rolls out, it will be cheaper, faster, and easier to create and consume livestreaming content from anywhere.

Audio Chat: Clubhouse just announced a Series C valuing the company at $4 billion, on the heels of a January Series B at $1 billion. Whether you think that’s ridiculously overvalued or not (I do for the record), it’s a good sign for Agora’s most prominent western customer, and it’s accelerating the adoption of audio chat as a feature. Twitter rolled out Spaces, Spotify acquired Locker Room to build its own Clubhouse competitor, Facebook is of course jumping in, Slack announced its own Clubhouse competitor on Clubhouse, and even fucking LinkedIn is building Clubhouse-like functionality. While these platforms are big enough to roll their own tech, even if they don’t go with Agora, they’re signaling to new companies in Agora’s target market that they, too, should be adding audio chat into their products. If audio chat is a commoditized feature, that’s a good thing for the companies that sell audio chat picks and shovels.

The Verticalization of Zoom. Zoom’s rapid COVID ascent attracted countless startups building products that take live-streaming video for granted, and embed it to create tailored experiences that solve particular user needs. JJ Oslund wrote about this trend in The Verticalization of Zoom.

All of these new video-based products fighting it out for customers is a great thing for Agora and other video APIs.

We haven’t even talked about VR, AR, and the Metaverse, but at this point, you know I’m bullish. Zhao has hinted on his ambitions in VR in particular, and Agora is already integrated in some VR education products.

There will be no shortage of demand for products that make it easy to embed real-time voice and video into products as the world continues to move online. The question is, will Agora capture that opportunity?

2. Agora has the best product in the market

We’re going to assume that most of the large players like Facebook and Twitter will build (or acquire) their own video and audio products, but that startups are not going to build for themselves. It’s too costly and time-consuming, and they’re not going to be able to match Agora.

So which product will they use?

Agora has become a go-to piece of the tech stack for companies building video streaming products. In Zoom’s Blank Check, Packy wrote:

Akarsh Sanghi, who recently launched a video streaming platform for lifestyle creators called Reach.Live out of YC, told me that all the new YC companies are building on the same stack: “React application on the client side, typescript, hasura, Postgres, WebRTC and Agora APIs for the video player.”

Agora targets companies with scale ambitions. It’s built for developers and pursues a bottoms-up go-to-market strategy. It gives away 10,000 minutes per month so that builders can try the product, and then retains them with affordable pricing and a quality experience. According to the company itself, its advantages come from the SD-RTN and 200+ global data centers, which minimize latency, its flexibility via a suite of customizable APIs, its ability to scale to millions of users, and compatibility with a multitude of development platforms and devices.

Agora is so confident in its product that it’s piloting the XLA (Experience Level Agreement), a play on an SLA that’s based on experience instead of just uptime. Customers shouldn’t have to pay for laggy video or audio just because it technically gets through. That’s a move you make if you believe you have the best experience and want to force competitors to play by your terms.

According to multiple customers interviewed on Tegus, all of whom evaluated multiple competitors for their products and whose uses range from video-game audio chat to one-to-many online video education, Agora’s advantage comes down to a combination of price, ease, scalability, and quality.

Some competitors do certain things better than Agora -- Dolby.io has more top-end audio functionality, for example -- but the sentiment is that no product works as well across video and audio, for close to the price, as Agora does.

Agora is currently used by some of the biggest livestreaming platforms in China -- YY, Momo, Bilibili, New Oriental Education, and Huya -- and as livestreaming takes off in the west, it’s well-positioned as the safe, scalable, affordable choice. “Nobody ever got fired for buying Agora.”

3. It’s defensible against bigger incumbents and startups alike.

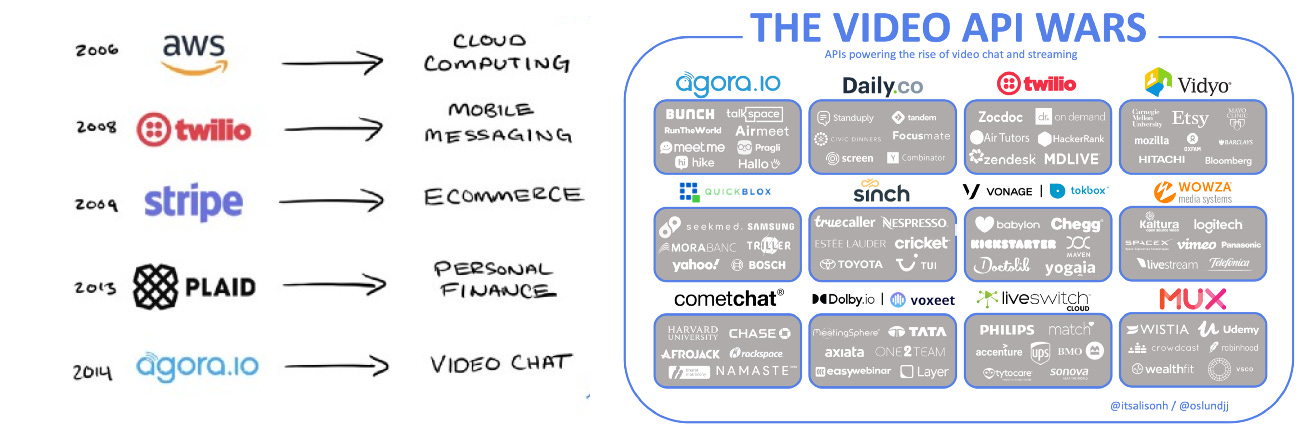

Agora is not alone. In Unbundling Zoom, Oslund expanded on that trend, highlighting the many players in the “Video API Wars.”

First, there is a wave of startups building video APIs. Hopin, one of the fastest-growing startups in history, is built on Mux, as are SoulCycle and Equinox’s streaming and on-demand classes. Not Boring portfolio company Teamflow is built on Daily, and CEO Flo Crivello told me they love it. Daily counts Y Combinator, Icebreaker, and Tandem among its clients, too. Twilio offers solutions more geared towards less price-sensitive enterprise clients who may already use Twilio’s original messaging products. There are more, as seen in the chart above, and more even beyond that.

Meanwhile, incumbents and large cloud players like AWS and Tencent Cloud have ambitions to enter the real-time engagement space.

But Agora has moats against both, starting with scale economies. Scale economies against startups make sense, and are similar to those enjoyed by any API-first first-mover: Agora’s 200+ data centers are a hard-to-replicate advantage, and it’s able to spread the costs of developing better solutions to edge cases across more customers. When the difference between excellent and terrible performance is measured in milliseconds, the little things matter.

Startup competitors will steal particular use cases like 1-1 chat or high-end audio from Agora, but I don’t think they’ll be able to catch Agora’s quality and scalability across the full suite of real-time engagement products.

Interestingly, that scale advantage extends to its battle against larger, better-funded cloud giants. One expert, an exec at a competitor, told Tegus that Tencent Cloud and AWS are limited by where their own data centers are because they’re not willing to rent from cloud competitors. Tencent will struggle to compete for customers with global audiences, for example, because it’s not willing to partner with AWS. Agora can rent from anyone, which gives it better global coverage, which gives it lower latency on calls with global participants.

Another advantage is switching costs. One customer interviewed on Tegus summed it up:

One thing I can tell you is that when it comes to price, if a company is not able to provide a model that is literally twice cheaper than Agora, it would be really hard for me to switch. Like if one of the Chinese companies says, "Hey, I can give you 100% discount from Agora's pricing," like I might consider, but if it's like 50%, like 40%, 30%, even like 20%, like the cost of switching is so high.

Finally, there’s Agora’s head-start combined with its focus. While this isn’t a traditional moat, it is an advantage. The competitor exec on Tegus said that even if the cloud giants poured a ton of resources into catching up to Agora, it would take them a year just to get to where Agora is today, by which point Agora would be another year ahead.

Outside of Amazon with AWS, where they really created the market, there are no good examples of companies shifting from a customer-facing product to a developer-focused API product and winning. I have doubts that Zoom, which is making a big push on its own APIs, will be able to effectively compete with Agora, either. In fact, I think Zoom should just buy Agora.

I’m bullish on Agora. Real-time engagement is exploding, and will become table-stakes in many products. Standalone livestreaming will continue to boom in China, and it’s already beginning to spread to the rest of the world. Agora is best-positioned to capture the opportunity, and it has moats to protect its profits as competitors enter the space. All that, and it’s only worth $6.6 billion.

Over to you, Lillian. What am I missing?

Agoraphobia: The Bear Case

So let’s go through each of Packy’s assumptions and unpack-y them.

Livestreaming’s revolution will not be global

The thrust of the bull case for Agora is that livestreaming will become as ubiquitous in the rest of the world as it has been in China. This glorious future where every dear reader will be half in the metaverse and half out. But what if this livestreaming phenomenon doesn’t become a successful Chinese export like the 2019 scooters and bike co-shares waves, but rather like that of mobile payments?

The enablers for livestreaming in China was not just the roll-out of 4G and 5G; but also effective monetisation models and payment infrastructure that made it lucrative for livestreamers, companies and platforms to focus on livestreaming. China’s payment rails and systems have not just leapfrogged their western counterparts, they are built by the tech giants like Alibaba and Tencent themselves. As such they are tech-led rather than finance-led. Will embedding frictionless payment systems within livestreams for the world be as easy as spinning up an instance of Agora?

Without a credible monetization model, livestreamers wouldn’t be incentivised to consistently livestream, and platforms wouldn’t achieve content marketplace liquidity. We’ve seen the downfall of Meerkat, Periscope and Facebook Live; why is this time going to be different? Those didn’t fail because the technology wasn’t there, but because other enabling factors were not.

But let’s assume, we’ve got 5G, we’ve cracked payment, what else? Sounds strange but the world needs to know to make livestreaming fun.

I recently tuned in to Amazon Live, and promptly shut the window after 2 minutes. It was so bland. The livestreamers didn’t know how to engage with the audience; the audience asked bad questions, there were no stickers or mini-games that made it engaging. It was all functional and no fun, and I was not going to waste my precious procrastination hours on there. I’ve noticed a similar thing on Clubhouse: people’s conversations are meandering and not that engaging. Once the shininess of listening to your favourite tech celebrity wears off, the dopamine hits are far and few in between.

All of this is to say, livestreaming the technology is here, but livestreaming as a medium is not. That will take time and deliberate UX decisions to cultivate. If not done correctly and soon, people might lose patience for the technology altogether. After all, every form of entertainment will be competing against Fortnite. Also why entertainment as the default format you ask? Because that’s the format that makes money for Agora when you are charging by the minute.

“A technology is merely a machine. A medium is the social and intellectual environment a machine creates” - Neil Postman, Amusing Ourselves to Death

I’m reminded of Eugene Wei’s seminal Status-as-a-Service blog post. He talked about how dull the early days of Twitter were, with people posting mundane life updates before tighter feedback in the form of status acquisition kicked in. This is where livestreaming is now in the West and it’s got fiercer competition for attention than Twitter had. For China, there were many years of cultural cache and user training built on tipping livestreamers, on livestreamers knowing how to perform for the camera and to engage an audience of thousands. This kind of cultural medium knowledge doesn’t spring up overnight.

Fundamentally what I’m pushing back on is saying that a technology will get adoption because it is big in China, when really we should be asking what made it catch on there in the first place.

Agora has the best product for specific use cases in the market and their business model is built around this

Agora was born and bred in a Chinese world of one-to-many livestreaming transmissions. Their killer feature revolves around the fast and steady scaling needs when a streamer turns on their camera and talks to thousands of viewers. Even their pricing is aligned to this model, having frequent 1:1 livestreaming convos might not break the 10,000 free minutes a month mark, but a livestreaming with a few thousands concurrent users gets you there fast.

Basically, Agora makes a lot of money when they get used for the use cases for which they were built. Other use cases are doable, but it’s not affecting the bottom line as much.

As Packy said above:

Startup competitors will steal particular use cases like 1-1 chat or high-end audio from Agora, but I don’t think they’ll be able to catch Agora’s quality and scalability across the full suite of real-time engagement products.

But what if we’re in a best-of-breed world for livestreaming and Agora’s market share gets eaten one by one by startup and enterprise competitors? And what if they are left with use cases and verticals that don’t play to their pricing strengths? I can see a world where the Zoom API takes small-scale internal enterprise conferencing, MUX takes enterprise grade quality video that gets recorded in the US, and big tech such as Twitter and Facebook will use their internal video options which they can also white label to others.

In a market where you’re competing against best-of-breed, death will come in the form of a thousand cuts. Can Agora be all things to all people in livestreaming? And if they can’t, are they getting into the verticals that allows them to maximise their revenue?

Agora’s historical strengths have been in social, gaming and education apps. They got into these apps early in China and grew with the company. Their growth, similar to the growth of other API-first companies, has been scaling with emerging companies. Have they arrived at the right time for that in the rest of the world? How many more Clubhouses can there be for Agora?

Customers who churn because they want to do it in-house

Chinese tech companies are like western tech companies but more so. By which I mean, they tend to do things by extremes. One thing they particularly love is building things in-house. For a core use case such as livestreaming, once it gets big enough, almost every Chinese tech company will have the conversation of whether to bring it house. One comparative advantage Chinese tech firms hold is that labour is cheaper, and theoretically, the thinking goes, that should lower the total cost of ownership.

I am skeptical of whether this trend will play out in the long term for Chinese firms or western firms. Twilio went through the same journey that Agora now is, and customers found the costly piece wasn’t the labour but the on-going maintenance. WhatsApp still pays Twilio hundreds of millions of dollars per year.

I don’t think that will stop them from trying in the short term. It’s interesting to note that on the customer page for Agora, heavy hitters such as Bilibili, Meituan, and Huya have disappeared during 2020. While they might come back to Agora in a few years, the churn is still a concern in the short term.

The Chinese company spectre

There is a narrative tax on being a Chinese company these days. I’m commenting on the meta-narratives and the baggage associated with China in all fields, but particularly tech.

It’s debatable whether it’s warranted but it’s definitely present and it’s not pretty. There’s increasing concerns around being a Chinese affiliated company among your buyers, among your employees and among the population at large. Zoom had to go through it as they exploded during Covid-19. Agora had to go through the public commentary cycle as Clubhouse got big.

What we also know is that private conversations are happening behind closed doors on precisely the same topics. It affects buyer’s perception and trust outside of anything that Agora does or doesn’t do (even as it has obtained ISO27001, ISO27017, ISO27018, and SOC2 Type1 certifications and passed third-party GDPR, CCPA and HIPAA compliance testing/ auditing). It’s a shame but also a reflection of our current geo-political climate onto the private economy.

How much this will affect Agora’s actual progress is hard to say, but the ambiguity is what makes it tough.

Bull or Bear?

So which is it? Bull or Bear?

Agora is in a tricky spot, full of natural tensions:

It wants to serve the broadest range of real-time engagement use cases well to appeal to the customers who need everything to just work, but faces competition from more geographically and use-case focused competitors.

It wants to expand to the west, but hasn’t made the proactive PR push that Zoom has to appease westerners security concerns.

It wants its customers to get very big, but not so big that they build in-house.

If Agora keeps growing at industry-leading rates in China while expanding to the west, the one-to-many thousands use case takes off outside of China, and Agora’s product continues to beat competitors on the combination of price and quality at scale, we might look back on $6 billion as the steal of the century in a few years.

Agora is a bet that people will live more of their lives online, and that large scale one-to-many livestreams become more common. The internet rewards the best. Instead of 10 million teachers with ten students each, the hundred best teachers will stream to a million students each. The same dynamic plays out across industries. If and when that happens, Agora is well-positioned to win.

But if competitors out-focus Agora by serving particular use cases better than it can serve those use cases as part of a broader suite, and if Agora’s not able to shake its “Chinese company” label in the West, its growth may be limited and its revenue multiple will be hard to grow into.

Ironically, Lillian is actually long $API and Packy doesn’t own any shares. Will we switch positions?

And what about you? Bull or bear? Let us know on Twitter @lillianmli & @packym.

How did you like this week’s Not Boring? Let me and Lillian know if we should do this again, and who you want to see us cover next:

Loved | Great | Good | Meh | Bad

Thanks for reading, and see you on Thursday,

Packy