Base Power Company

Building the Modern Power Company of the Electric Era

Welcome to the 852 newly Not Boring people who have joined us since our last essay! If you haven’t subscribed, join 225,076 smart, curious folks by subscribing here:

Hi friends 👋,

Happy Tuesday and welcome back to Techno-Industrial Tuesdays here at Not Boring!

My favorite companies are the ones that take understanding whole industries to really grok. To understand Astro Mechanica, you need to understand airlines. To understand Earth AI, you need to understand mining. As you learn the industry, you identify one or two key bottlenecks to its progress. For airlines, it’s that we’ve maxed out the capabilities of the jet engine. For mining, it’s that new discoveries are harder and more expensive to come by.

To understand Base Power Company, you need to understand power, and you come to realize that the grid is the bottleneck. Add more renewables and electrify more things, and the grid gets less stable.

That’s what Base is trying to fix, with residential batteries. It’s too early to tell if they’ll pull it off, but the strategy that Zach Dell, Justin Lopas, and the team of ex-Anduril, SpaceX, Tesla, Ramp, Blackstone, and Apple engineers and operators are executing against is sound.

Fixing the grid — really going for it with whatever tools are necessary, not just software — is one of those insanely hard problems that startups wouldn’t have dared to tackle a few years ago. I’m pumped to live in a world where they do.

We go very deep. Click here to read the whole thing online.

Let’s get to it.

Base Power Company

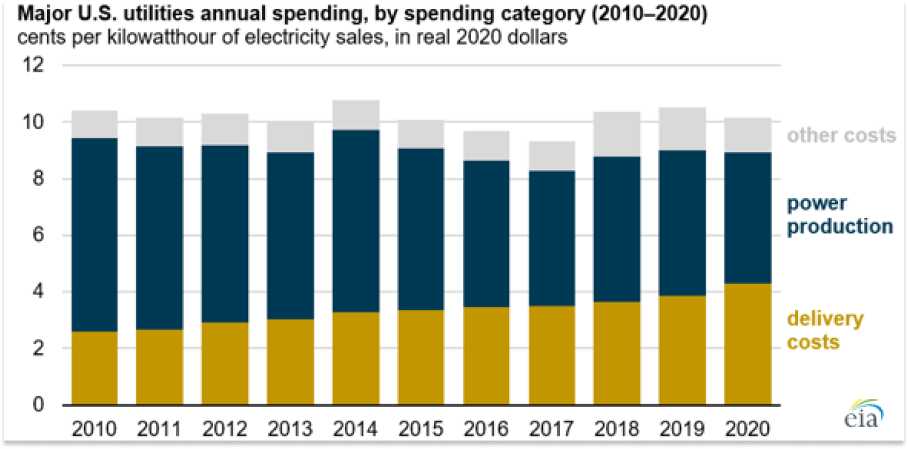

On my first call with Justin Lopas, he showed me a chart to explain why he left his job as Head of Manufacturing at Anduril to co-found Base Power Company.

This is an incredible chart. It shows that while the cost to produce electricity has fallen 33% from 6.8 cents per kilowatt hour (kWh) to 4.6 cents/kWh over the past decade, electricity is no cheaper than it was in 2010. That’s because the cost to deliver electricity has increased by 65%, from 2.6 cents/kWh to 4.3 cents/kWh.

Energy is fundamentally critical and unbelievably complex. Last year, Julia DeWahl and I spent a whole 10-episode season digging into how America can start producing nuclear energy again. But nuclear is just one generation technology, and generation (or production) is just one of the three legs of the electricity stool alongside delivery and consumption.

For the energy transition to succeed, and for the world to consume multiples more energy than we do today, all three legs need to improve.

On the production side, we need more and cheaper nuclear, solar, wind, geothermal, synthetic fuels, and other carbon-free sources of energy.

On the consumption side, we need to electrify everything we can economically electrify – from cars to heat pumps to appliances.

The good news is: both are happening!

Solar is getting unbelievably cheap, electric vehicle (EV) penetration continues to rise, and scores of incredibly smart people are working to produce electricity more cheaply and consume that cheap electricity in more ways.

The bad news is: both of those things actually make the delivery problem worse!

Delivery involves moving electrons from where they’re produced to where they’re consumed, like from a coal plant or solar farm to a home or business. There’s transmission – moving electrons over long distances from power plants to substations using high-voltage lines – and distribution – moving electrons from the substation to homes and businesses over the regular low-voltage power lines you’re used to seeing.

This whole electricity delivery system is known as “the grid.” And the grid is a bit of a mess.

It’s buckling due to four factors Construction Physics’ Brian Potter describes as, “increasing use of variable sources of electricity, decreasing grid reliability, increasing delay in building electrical infrastructure, and increasing demand for electricity.”

The bookend threats – increasing use of variable sources of electricity and increasing demand for electricity – present a particularly paradoxical problem. The more progress we make in wind, solar, EVs, and electric stoves, the more unstable the grid gets.

The power supply is increasingly variable and unreliable. The demand for power is growing and increasingly volatile. Just as everyone gets home, plugs in their Tesla, and turns on all of their shiny electric stuff, the sun sets!

With more demand for electricity, delivery gets more expensive, because transmission lines need to be sized for peak load. One solution is just to add more transmission capacity, but fixing the grid itself by modernizing or adding transmission is, like any big project in America, getting harder, slower, and more expensive to do.

This is the bottleneck standing between us and our clean, abundant energy future, and it’s the piece of the energy puzzle that has attracted the least entrepreneurial attention.

So it’s the challenge that Base Power Company plans to solve.

Base is building “the Modern Power Company of the Electric Era.”

It’s starting by deploying connected batteries across the grid in places where interconnect already exists and where the demand happens: in peoples’ homes, beginning with Texas.

Batteries can fix us. They solve electricity’s big challenge: matching electricity production and consumption. Batteries can store electricity on the cheap when the sun shines and the wind blows and discharge it whenever people want to turn on their appliances, reducing strain on the grid.

And batteries are booming. Installed storage capacity tripled from 2020 to 2021, then doubled in both 2022 and 2023. The Energy Information Agency predicts capacity will grow another 80% this year. That’s both a consequence and a cause of the fact that batteries are getting cheaper. Prices have fallen 82% over the past decade, and with more battery production, prices continue to fall.

Battery installation isn’t progressing as quickly as it could, however, thanks in part to the long interconnect queues – waiting to get connected to the grid – that are plaguing energy projects of all sorts. Most of the battery storage capacity in the US is concentrated in centralized grid-scale battery farms, which have to wait for interconnection.

But what if you go to where interconnection is freely available – customers’ homes? Residential batteries are actually ideal for a few reasons.

Justin told me to imagine the grid as a single line from the solar farm to the home and asked: “Where on the line do you put the battery?”

If you put it next to the solar farm, you go a long way towards solving the supply volatility problem.

The grid views a battery farm like a more flexible nuclear plant – reliable supply that can be ramped up or down as needed. But you still need transmission and distribution lines between the solar farm and the house to support the maximum load that the home could pull, because people will still turn on their AC and charge their EVs when they get home.

But if you slide the battery all the way over to the right and put it next to the home, you solve the supply volatility problem and the demand volatility problem.

Call that the Electric Slide.

From the perspective of the grid, it looks like the home is consistently demanding about one-quarter of its peak load. The battery charges when demand, and therefore price, is low, and discharges into the home when demand, and therefore price, is high. It smooths out the demand curve, which means less load on transmission lines.

As the demand for electricity is expected to double or triple by 2050, solving the demand volatility is crucial. If you want to really solve the grid bottleneck, you need residential batteries.

So why is the vast majority of the battery installation grid-scale (i.e. next to the solar farm in our toy example)? A lot of financial and operational reasons, it turns out.

For one thing, batteries are expensive. Customers understandably don’t want to pony up $15,000 for something that pays itself back in 12 years even after the 30% IRA tax credit.

Private equity-backed battery farms like Broad Reach (Apollo), Jupiter (BlackRock), and aypa (Blackstone) on the other hand, are happy underwriting that investment, signing offtake agreements to sell their power, and levering the hell out of it at 70-80% loan-to-value to generate high levered returns.

For another, acquiring individual residential customers is expensive compared to just putting a bunch of batteries on one piece of land.

For a third, battery capacity is wasted on individual homes. Customers can’t arbitrage price volatility in the way a professional battery farm operator can, which means that each kW of capacity is more valuable to battery farms than it is to individual customers.

The list goes on. I know I’m throwing a lot at you for an introduction, but to understand what Base is building and why, you need to grok how multifaceted the challenge is.

To deploy batteries and fix the grid, Base can’t just build a battery; it needs to build a vertically integrated power company around batteries.

The power company needs to excel at a whole lot of things: manufacturing, finance, distributed systems, power trading, customer acquisition, consumer software, regulatory, and installation, to start. It needs to become a Retail Electric Provider (REP) itself.

Technologies are tools. The better the tools builders have, the bigger challenges they can solve. The focus should be on the challenge, not the tool. The job of the entrepreneur tackling big, physical industries is to assemble whichever combination of tools, and whichever team of people who can best wield them, is needed to do the job.

Base is one of the clearest examples of that approach that I’ve seen. It’s building a textbook Techno-Industrial, vertically integrating a number of modern tools to make a big, old market cheaper and better. It’s built a team from SpaceX, Anduril, Blackstone, and Apple, where they honed their particular crafts. And it’s a case study in Techno-Industrial strategy: how do you fit all the tools together to solve the one or two key problems that really matter?

To that end, Zach Dell, Justin’s co-founder, shared a series of memos the team has written from idea conception to Series A as he and the team started with an insight and explored the best way to turn it into a business.

“The grid is the bottleneck and batteries can unblock it” is a big insight, but it’s just a starting point.

Base is young, less than a year old. It’s well-capitalized, having raised over $60 million from investors including Thrive Capital, Altimeter Capital, and Valor Equity Partners. Antonio Gracias, who has served on the boards of Tesla and SpaceX, sits on Base’s board. Its team is stacked and its strategy is sound.

But because all of Base’s accomplishments lay in the future, it’s a perfect opportunity to analyze its strategy with a clean sheet of paper and without the benefit of hindsight. Given ideal starting conditions and a clear strategy, can a startup come to compete with monopoly utilities and fix what may be the largest and most complex machine in the world, the grid?

Only time will tell. For today, we’re going to walk through the idea maze together to understand why Base is building what it is, how, where, and what it means if they pull it off.

But we have to start with who.

Assembling a Based Team

Of the many insights that led to Base, perhaps the most important was the talent arbitrage available in the power space.

No ambitious genius wants to work for the utility. But the Anduril of Electricity? The company solving a never-ending series of interconnected hard problems to fix the trillion-dollar power market and usher in the electric future with other smart people? That’s the kind of problem smart people can’t resist.

Finding the really hard problem to solve with really smart people has been Zach Dell’s quest.

During college, he recruited a team to go to India and build anaerobic digestion systems to turn waste into compressed biogas that could be used to power stoves, lights, and fans. Before senior year, he interned at Blackstone because as the largest investment firm in the world, it seemed like the place to work with smart people and hunt for big problems. His first project proved that hunch right.

Blackstone was looking at buying a lithium mine, which meant that it had to take a view on the price of lithium, which meant that it had to take a view on battery demand. 70% of lithium goes to batteries. If you get your battery assumption right, you win. If you get it wrong, you lose. As Zach did the research, he realized that a lot of people got it wrong: as with solar solar, experts kept underestimating the exponential curve batteries were riding.

Hooked, Zach raised his hand to keep working on energy projects, and as he did, the idea that there were going to be a ton of batteries coming online stuck with him.

When he went to work at Thrive Capital after his first year at Blackstone, he kept working on energy and hardware, kept researching batteries, and met with as many battery companies as he could. He wanted to understand the best way to create and capture value from the battery wave he was convinced was coming, and he didn’t see anyone doing it the way he would.

Around the same time, Thrive made a large investment in Anduril, and Zach flew out to Costa Mesa, California to check out the factory. Naturally, Anduril’s Head of Manufacturing showed him around.

Zach and Justin hit it off.

Both wanted to start something big and both had an idea that that big thing would be in energy, although they arrived at the answer from opposite ends of the spectrum with completely different – and complementary – skill sets.

After graduating from the University of Michigan with a degree in mechanical engineering, Justin Lopas joined SpaceX as a Manufacturing Engineer before being promoted to lead Manufacturing Engineering on Falcon Thrust Structures.

His work in that role was rewarded with a one way ticket to beautiful Brownsville, Texas, where he was one of the first four people who took what would become Starbase “from an overgrown field to an operational site.” Starhopper, the R2D2-looking thing that was the first prototype of the Starship program, was his “baby.”

Working directly for Elon, Justin got a crash course in building something from nothing, but Brownsville, he realized, was not going to be his forever home. So in 2020, he joined a fledgling defense tech startup that had just raised a bunch of money after securing its first contract from Customs and Border Protection and was looking to make its first manufacturing hire to meet the demand.

As Anduril’s Head of Manufacturing, Justin grew an organization of 150 people responsible for manufacturing engineering, operations, and supply chain as the company grew from a small single-product company to a defense tech juggernaut. In announcing that the US Air Force had selected it to design, manufacture, and test production-representative Collaborative Combat Aircraft, the company tweeted that it looked forward to “delivering CCAs on schedule, within budget, and at scale.” Justin’s team laid the groundwork for that three-part promise.

By the time he met Zach in late 2022, though, Justin was starting to get The Itch. His dad was an entrepreneur – he ran his own construction company in Detroit – and Justin wanted to start his own thing too. But what was big enough to work on after SpaceX and Anduril?

He thought about the question, like he thinks about most problems, as an engineer.

GDP per Capita is the best measure of human prosperity. How do you move it?

Energy is the most directly related. There are no low-energy, rich countries.

So how do you solve energy? As we covered, the big bottleneck is the grid.

And how do you fix the grid? Well, Zach’s battery obsession might hold the key.

Over the next six months, Zach and Justin kept talking about different companies doing interesting things in hardware and energy. Eventually, the conversation turned into the two of them pitching each other energy-related startup ideas. Finally, they decided to start something together. But what, exactly?

They both knew the NewCo would have something to do with batteries, but there were a lot of battery companies. The devil was in the details.

“Justin would come up with an idea, and I’d build a spreadsheet to show him why it was a bad idea,” Zach told me. “Then I’d come up with an idea, and he’d do the same to me.”

Eventually, the duo zeroed in on the idea that would become Base and met in Austin for a week to jam on system-level implementation. “Do we do neighborhood-level batteries? Small batteries? Big ones?”

By February 2023, when Zach wrote the first memo on “Energy NewCo,” he described the play like this:

There is an opportunity to build an electrification platform for the built environment, starting with premium residential, and eventually moving downmarket into the high volume home-builders, and eventually into high rise buildings and commercial projects.

It was the classic hard tech strategy, popularized by Tesla. If batteries were expensive, then lean into that and go after the high end of the market. In this case, that meant the type of buyer who would want to add new electric appliances to their home, which Base would be happy to provide. Eventually, as battery costs fall with volume, drop prices and go after the mass market. Then, when you own a big enough network of batteries and the power to control demand, you can build a decentralized utility that balances load across the grid.

It was a start, but it wasn’t quite right. It was clear they were learning and iterating quickly, though, because by the time Zach wrote the next memo in April 2023, it had gotten a lot sharper:

We propose a vertically integrated and modern approach to an electric utility. Our model focuses on designing and selling battery packs optimized for residential homes, offering consumers the opportunity to generate, store, and sell energy. By becoming a Retail Electric Provider (REP), we can monetize installed storage assets and offer consumers competitive energy prices and real-time energy management.

We intend to move fast to take share in the residential market by offering consumers a simple, zero-downside energy solution while not financially burdening the household. A key differentiator of our product lies in the larger battery capacity, designed to maximize arbitrage opportunities.

The pieces that would become Base power were starting to snap into place. It would design and sell battery packs to homeowners. It would become an REP, meaning that it would be the company that homeowners pay their electric bill to. Importantly, instead of going premium, it would offer a zero-downside energy solution, and make money on arbitraging electricity prices. That’s the broad strokes outline of what Base is building today.

Building a vertically integrated power company that consumers love, manufacturing battery packs, offering them cheaply, and arbitraging power prices in real-time would mean building a power company with the soul and engineering chops of an Anduril or a SpaceX.

While Zach had the finance piece handled, and Justin knew manufacturing, they’d also need to get really good at software and distributed systems. The batteries would have to talk to each other, and the grid, in real-time.

Luckily, Zach’s writing was making the rounds, and through a mutual friend, it made its way to Jared Greene.

“It talked about how manufacturing was going to work, how sourcing was going to work, how capital was going to work” – the things in Justin and Zach’s respective wheelhouses – “but the network section was a to-do.”

Networking is what Jared does. When he read the memo, Jared was working at SpaceX, where he’d progressed from Simulation Engineer II to Senior Simulation Engineer to Lead Software Engineer for Laser Topology on Starlink. In that role, he built and led the team that brought the uptime of Starlink’s laser mesh network – how the satellites talked to each other – from 60% to 99%.

He quickly saw the parallel between his work on Starlink and what Base would need to do: novel deployment.

It seems counterintuitive that the most efficient way to deliver internet would be to strap a bunch of satellites onto a rocket, deliver them to low earth orbit, and beam internet down from up there. But once you have the rockets anyway, deploying in space means you’re not limited by things like land access and permits. You’re only limited by your rate of execution, which you can control.

Jared viewed Base’s effort to build a residential electricity offering as its rocket. It’s a non-trivial thing to do, but if you pull it off, you don’t need to wait in long interconnect queues, get permits, or lay transmission lines. You can scale a distributed network more quickly, limited only by your rate of execution, which you can control.

So Jared decided to talk to Zach. They Zoomed, then met up in New York, then kept talking daily for months. Finally, in August 2023, Jared agreed to join Base to head up software and engineering.

When I wrote about Varda last year, one of the things that stood out to me was that Delian realized early that the company would need to be world-class at a few things: “manufacturing in space, getting the payload back to Earth, and selling to both commercial and government customers.” So he recruited Adrian Radocea, Will Bruey, and Eric Lasker to own each of those respective capabilities.

The Base founding team is similarly assembled. Zach, as CEO, would run finance, strategy, sales, and regulatory. Justin, as COO, would own hardware and operations, the Deployment Factory. Jared would be responsible for turning the fleet of batteries into a network that trades with, and balances, the grid. And Cole Jones, a Senior Product Growth Manager on Starlink at SpaceX, would lead growth and go-to-market, bringing on customers to the REP.

Base has to be good at a lot of things, which means it needs leaders who excel in each of those things. It needs those things to work in harmony as part of a larger system, so those leaders who work together to build the machine that builds the machines.

In its Series A memo, the co-founders wrote that, before batteries or software, the first thing it needed to build was the team:

Base will acutely focus its initial efforts on hiring the best engineers & operators in the country from top hardware and software companies. Initial recruitment of top talent will set the path of the company, and will be our highest initial priority.

That prioritization seems to be paying off in the form of a stacked team.

On the manufacturing and ops side, Suzanne Dang ran procurement at SpaceX for ten years before joining Base to lead Supply Chain. Dana Paz worked on manufacturing with Justin at Anduril and runs Base’s “deployment factory”.

Base’s software team is made up of engineers from Apple, Tesla, and Ramp.

Dino Sasaridis spent 13 years at Tesla, where he worked on the original Roadster and most recently led mechanical engineering on Tesla’s Powerwall 3. He will lead engineering on Base’s battery.

“The idea is one thing,” Zach told me, “but execution is everything. You need kickass people to rally around the mission. When you go after a really big, really hard, really inspiring problem, recruiting gets easier.”

It’s a counterintuitive truth, and one of the things that attracted me to Hard Startups in the first place. As I wrote then, doing something important “helps attract and retain talent, and helps employees rally around the mission.”

The best people want to work on the hardest and most impactful problems.

They’ll have their hands full at Base.

What Base is Building

The simplest way to describe Base’s business is that it’s building a large portfolio of connected batteries with short paybacks and high cash on cash returns. That simplicity masks a whole lot of complexity.

Base Power Company is a Retail Electric Provider (REP) in Texas. It buys power from the grid and sells it to customers.

It installs a large battery – 20kWh versus 13.5 kWh for a Tesla Powerwall, increasing to 30kWh in future models – in each customer’s home. The size is designed to max out a home’s standard 240 volt 200 amp electrical capacity, which means it can provide whole home backup while supporting the grid. It also decreases install times by 50-75% by eliminating the need to install a critical loads panel, which you’d need for a smaller battery that can’t power the whole home. With larger batteries, the battery becomes the home’s single interface with the grid.

Base assembles and will soon manufacture battery packs itself, but it doesn’t make battery cells. A cell is the basic unit of a battery – the thing with the anode, cathode, and electrolyte that generates electricity through chemical reactions. A pack consists of multiple battery cells, the casing, the Battery Management System, cooling system, and connectors. It distributes and manages the power generated by the individual cells. Base believes that cells will be commoditized, and that pack assembly allows it to benefit from that commoditization and potentially integrate new cell types as better chemistries emerge.

It also manages installations itself, which it views as tightly coupled with pack assembly. It calls the whole process the Deployment Factory. Packs need to be manufactured in such a way that they’re easy to install. Modular design with no forklifts or cranes required. Connectors instead of wires that need to be cut and crimped. It’s not the way you’d design a specific battery for optimal performance, but how you’d design the whole system for optimal performance.

Base owns the battery, and customers only pay the install cost versus the nearly $20k total cost of buying a system with equivalent power. Base believes that this model is a big unlock in driving consumer adoption. Instead of asking customers to take on a decade-plus payback, Base takes it (and the upside) on itself.

Unlike customers, which can finance individual batteries at high rates, Base can build a portfolio of batteries and get cheaper asset-backed loans at the portfolio level. Unlike battery farms, it doesn’t sign offtake agreements but trades in volatile power markets, which means it can’t lever up as much as battery farms can. But because it manufactures its own batteries, it doesn’t need to pay the margins to Tesla that battery farms do, either. That said, between loans and the 30% IRA tax credits, Base expects it will be able to spend less equity on each battery and generate higher yields than it could without debt, as long as it makes money on the batteries.

To that end, because Base is an REP, it can make money by trading electricity in wholesale markets, which it believes will lower its paybacks and increase its yields. It buys power from the grid when prices are low and it sells power back to the grid when prices are high. It can do this because the battery can store the electrons it acquires cheaply and discharge them whenever they’re needed. As the team wrote in one memo, “Your home or office should run on 4am power, not 6pm power.”

Base is starting in Texas for a number of reasons. The first is that the customer pain is particularly acute in Texas, where there are 6x more outages than there were a decade ago.

Relatedly, thanks to a confluence of factors we’ll discuss, power prices in Texas are particularly volatile and getting more volatile as the state continues to lead the way in renewable generation installs. Since Base can buy low and sell high, the larger the gap between high and low, the more money it can make.

In order for all of this to work, Base is building sensors and software to aggregate demand signals from its network of connected batteries and charge and discharge electricity based on those signals. A giant fleet of software-controlled energy storage systems that Base can control should give them an edge in power trading, improve their customers’ reliability, and help improve the performance of the grid overall.

If Base is successful in power trading, it can improve its paybacks, increase its yields, and give customers savings on their electricity bills, which would allow the company to expand its battery fleet more quickly. A larger battery fleet means more signals, more profit, and a greater ability to impact the grid.

Ultimately, with a large enough fleet, Base imagines it could backwards integrate into power generation and build a modern utility with some clean sheet advantages. If you were starting a utility today, you wouldn’t build coal or gas generators; you’d build nuclear, solar, and wind. But many who have tried to compete directly with utilities on that premise have failed. Starting by owning demand, though, could give Base a cost of capital advantage: they’d already have the buyer for the power they generate.

That, the company believes, is how you build the Modern Power Company of the Electric Era.

Simple, right?

Now that we’ve covered the what, painted a picture of how all the pieces fit together, we can dig deeper into the series of why’s that led there.

Why is the grid crumbling? Why batteries? Why vertically integrate? Why a Retail Electric Provider? Why distributed? Why Texas?

We’ll start with the macro situation – with the grid and batteries – before getting into the micro of the decisions that Base is making to fix the situation and build a valuable business.

Then, once we have that, we can imagine how Base might expand from the initial market into a modern high-margin utility that fixes the grid and lets Americans use all the solar, nuclear, and wind we need to power all the EVs, AC, and electric appliances we want.

Why the Grid is Crumbling

If your goal is to solve a really big challenge, the electric grid is a worthy foe.

The grid has been called the largest and most complex machine in the world, and for good reason. As Anna-Sofia Lesiv wrote in her excellent overview of the grid, in the US alone, it connects over 11,900 power plants, each a complex machine in its own right, over more than 160,000 miles of high-voltage power lines, and millions more miles of low-voltage distribution lines.

Maybe the best way to understand the grid is from the perspective of the power that flows through it. The journey begins at a generation facility – a nuclear plant or solar farm, for example – where various forms of energy are converted into electrical energy. Electricity is produced at low voltages, gets stepped up via transformers to high voltages, and travels from the plant through high-voltage transmission lines designed to carry it hundreds or thousands of miles. As it approaches its final destination, the power goes through a substation, where transformers step it down to lower voltages, before speeding on to low-voltage distribution lines. Once it hits your neighborhood, the power’s voltage is stepped down once more via a transformer before the power travels down one last wire to your home’s service panel (which contains the circuit breaker you need to flick when the power goes out), where it’s distributed to various circuits in your home.

The absolutely incredible thing about this whole system is just how fast everything happens. When you turn on your air conditioning, it uses power that was generated hundreds of miles away about one second ago. As Casey Handmer writes, “Transmission moves power through space (technically null space, at the speed of light).”

This is both a miracle and a curse. a16z’s Ryan McEntush explains this double-edged sword: “At all times, electricity generated must match electricity demand, or ‘load’; this is what people mean when they say ‘balance the grid.’”

Making matters more challenging, the grid has to be sized for peak load: for that really hot day every decade when everyone turns their AC all the way up all at once. There needs to be enough generation capacity to produce the load and enough transmission capacity to move it, even if it’s very infrequently used.

In an interview for Age of Miracles, Meredith Angwin, the “Grandmother of the Grid,” told us that utilities have to pay certain generation facilities to just not shut down, even if they’re not producing power, just in case they’re needed. These “capacity payments” make everyone’s electric bill higher. They’re an inelegant financial band-aid for a problem that can now be solved with technology.

Balancing the grid has always been a challenge, one often solved by picking up the phone and frantically calling generation facilities to turn production on or off ASAP, or by dumping perfectly good electricity with nowhere to go. Occasionally, when things go really wrong, there are blackouts, which cause everything from inconvenience to economic interruption to death.

But largely, for most of its life, the grid worked. Baseload power plants run consistently to meet the consistent demand for electricity, and more expensive peaker plants are dispatched as needed to meet higher periods of demand. Supply was dispatchable as-needed, and demand, while weather-dependent, was predictable.

Back in college, I interned on an energy trading desk, and every morning, the first thing I did was check the weather: if it was going to be really hot, prices would spike as more expensive peaker plants came online. But if I, as a dumb intern, knew that, it was a very predictable and largely non-threatening spike.

With the rise of renewables and the electrification of everything, that’s changed. “For most of its history, electric power generation worked like any other machine - it was turned on when it was needed, and turned off when it wasn’t,” Brian Potter wrote, “But the predictability of power generation is slowly going out the window.”

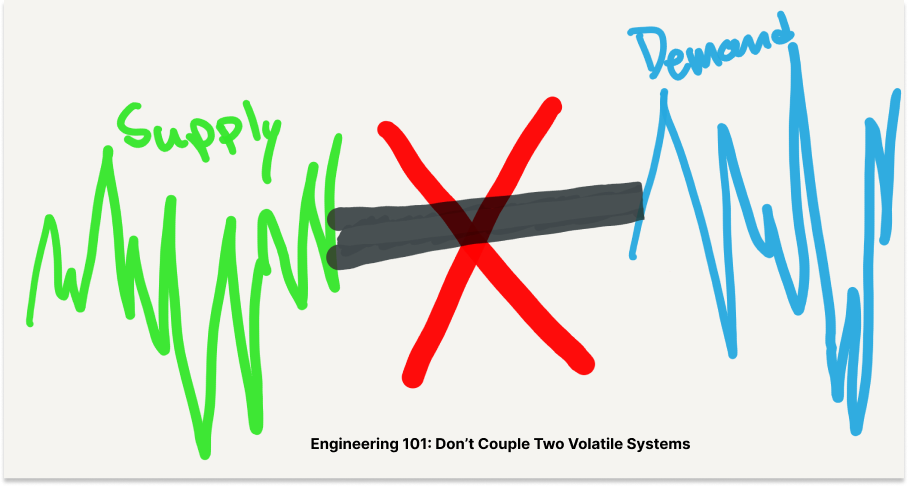

Instead of (largely) predictable supply serving (largely) predictable demand, we increasingly have volatile supply meeting volatile (and growing) demand.

“When you have a system with volatility on one end and volatility on the other,” Jared explained to me, “the basic engineering principle is: don’t couple them. Don’t force yourself to control one with respect to the other.” But that’s how we operate the grid today. Most of the time, it’s fine, but more and more frequently, it’s not.

As Brian Potter points out in The Grid, Part IV, the introduction of variable sources of electricity, like solar…

… coupled with a National Renewable Energy Laboratory-predicted tripling of electricity demand by 2050…

… means that “the grid faces several challenges that threaten its ability to distribute electric power.”

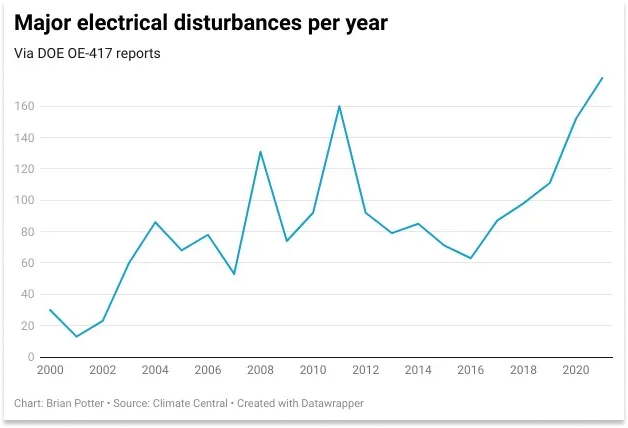

Already, outages are increasing dramatically.

Potter cites a number of factors for decreasing reliability, chief among them the rise in extreme weather conditions. Extreme weather can take down distribution lines, shut down electricity generation, and spike demand, sometimes all at once!

And it’s only going to get worse. As we rip out more coal plants, fail to build nuclear, and install more solar and wind, supply will continue to get more volatile. As we electrify our cars, heating, and appliances, demand will continue to get more volatile. But we need to do both of those things in order to avoid a climate disaster.

So what do you do?

One obvious solution which we spent a whole season of Age of Miracles covering is to build more nuclear. Nuclear is clean, firm, baseload power. It’s predictable. We should absolutely, 100% do that, and a host of startups are working to make it possible. But nuclear, as implemented in America at least, is slow to turn on and off. It can’t respond to spikes in demand. It helps solve half the issue.

Another obvious solution is just to build more transmission and distribution. But if you’ve been reading Not Boring, you know how incredibly difficult it is to build big things in America. Aside from nuclear, transmission might be the most difficult thing for us to build.

As Ryan McEntush covers, electrical infrastructure is slow and expensive to replace and build due to a witches’ brew of issues, ranging from the standard NEPA reviews to an overwhelming deluge of applications to build to run-of-the-mill supply chain issues for transformers and electrical steel. The average overhead transmission line takes more than a decade to build, seven years of which is spent in planning and permitting!

So again, what do you do?

While we’ll still need to build and replace transmission and distribution, the most pressing thing that we can do is to smooth supply and demand across time to give the grid a break.

Why Batteries?

To fix the grid, just add batteries.

Smoothing electricity supply and demand over time is what batteries were born to do. In the bluntly titled Grid Storage: Why Batteries Will Win, Casey Handmer wrote:

Here’s the key insight. Batteries and transmission are in direct competition. Both enable electricity arbitrage – the profitable repricing of a resource by matching different levels of supply and demand. Transmission moves power through space (technically null space, at the speed of light) and batteries move power through time.

What follows from that key insight is a thorough and data-driven demolition of the idea that adding more grid is the right way to fix the grid. A few highlights:

Adding 12 hours of storage to the entire US grid would not happen overnight, but on current trends would cost around $500b and pay for itself within a few years. This is a shorter timescale than the required manufacturing ramp, meaning it could be entirely privately funded. By contrast, upgrading the US transmission grid could cost $7t over 20 years.

In all cases, we see a grid without storage is useless… Conversely, we see relatively small quantities of overall storage dramatically decrease the amount of generation overbuild needed. Over a wide range of wind/solar mix and battery installation, we can hit 99.99% reliability (significantly better than the pre-renewable grid) with < 10x nameplate overbuild. This is how the grid will look in the future.

Adding marginal batteries until demand saturates will generate enormous profit and value growth. Adding additional grid is just stranding assets.

Casey calls his view “unconventional, even controversial,” and arguably his “spiciest hot take on the future of energy,” but the more I’ve dug in, the more I agree with him.

Batteries aren’t a generation technology – we can’t produce more energy with batteries – but they supercharge other forms of clean generation.

As we’ve discussed, batteries are a great complement to variable generation sources like solar and wind. Solar and wind produce power whenever the sun shines and the wind blows, but people’s energy consumption doesn’t match the weather’s whims. Batteries can store power generated whenever it’s generated, and dispatch it whenever it’s needed.

But batteries are also a great complement to nuclear power. As Base wrote in a recent memo, “Nuclear has high upfront costs but very low operating costs. Load side storage helps match the consistent output of nuclear to variable load and increases the economic value of energy generated from nuclear.” Batteries make nuclear dispatchable.

In fact, they point out, batteries are a great complement to any high capex, low opex source of energy. If a plant is expensive to build but produces cheap energy thereafter, batteries can soak up all of the cheap output to be dispatched when demand calls. That allows power generation owners to amortize their capex over more demand, or to pay back their capex more quickly. Batteries make renewable energy – definitionally low opex – more competitive with fossil fuel plants, which are less expensive to build but must consistently feed fuel into the system.

Batteries are also great for the grid.

The grid is designed to carry the peak load customers are expected to demand. If demand gets spikier, grid operators need to add more transmission capacity to meet peak loads, even if most of that capacity sits unused most of the time.

Load factor is the ratio of average power demand to peak power demand over a given period. A low load factor means wasted resources. As an example, Texas’ grid is sized for 85 GW based on last summer’s peak. Currently, it’s running at a load of 48.8 GW. That’s a load factor of 57%.

Maximizing load factor means the grid can operate more efficiently. Stabilizing load factor helps to minimize fluctuations in demand, which can reduce strain on the grid and improve its overall reliability.

Batteries can help maximize and stabilize load factor by charging when demand is low, thereby increasing trough demand, and discharging when demand is high, thereby lowering peak demand.

In the short term, batteries can stabilize load factor on the existing grid, even in the face of more variable renewable energy and electrification. Over the long term, as electrification drives more demand for power, batteries can help maximize load factor and avoid expensive buildout.

Which begs the question: if batteries are so miraculous, though, why aren’t they everywhere?

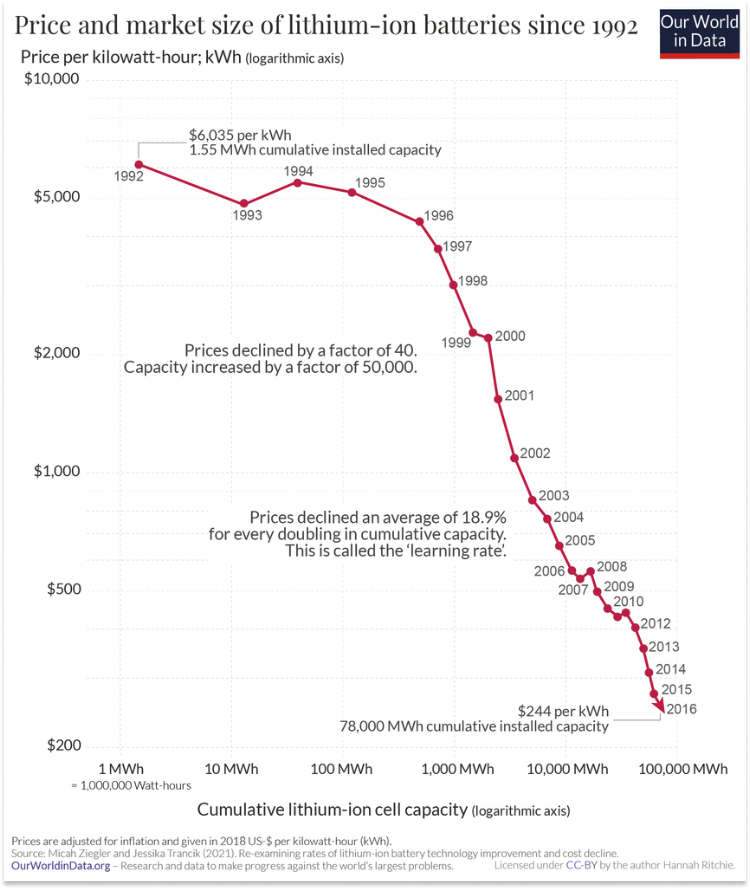

First off, give them time. Battery capacity has been growing rapidly. Between 2021 and 2023, installed capacity tripled from 5 gigawatts (GW) to 15 GW. The EIA expects capacity to double again this year to 30 GW and grow by another third the following to over 40 GW.

The biggest issue with batteries has been their cost. Beautifully, however, as we produce more of them, they get cheaper. They’re riding a learning curve. With every doubling of cumulative capacity, the price per kilowatt hour declines by 18.9%.

Last year, batteries hit a record low price of $139/kWh, down from $780/kWh in real 2023 dollars a decade earlier.

These were the trends that got Zach so excited about batteries in the first place. Batteries were growing more quickly, and getting cheaper, than most people realized.

That was the opportunity.

Why Vertically Integrate?

But what was the best way to capture the opportunity? Should you make cells? Manufacture packs? Install batteries that other people make to power electrification? Sell battery management system software that rides on batteries people have installed to build a virtual power plant? Do any or all of these things nationwide, or in a specific geography?

The answer isn’t straightforward. There are nice businesses to be built in each. But to really solve the problem, and build the biggest business, the team decided that it would have to vertically integrate and do a little bit of all of it.

So which pieces do you integrate? What do you do yourself and what do you buy off-the-shelf? Where do you start?

Building a great product is hard, but it’s relatively straightforward. Building a great vertically integrated system is endlessly complex. It’s the difference between building a solar farm and building the grid. Move one thing here, and something else changes there. Move that and something else shifts.

As more startups build vertically integrated systems versus standalone products, it’s useful to look inside Base’s process. As Zach wrote in the May 2023 Week 3 Update to the “Battery NewCo” team (emphasis mine):

Reflecting on week 3 of our Battery NewCo sprint, we have learned a lot, gone in circles on some topics, and had a good amount of ups and downs in our conviction…

One way to frame this process is that we have started with a thesis (extreme battery market growth is coming), from the thesis comes a strategy (how we are going to capture the opportunity), from the strategy comes a company structure/plan (what it should actually look like), and from that comes the team (who we need to bring together to execute on the plan). We feel very good about our thesis as outlined in our original memo. As we have talked to more players in the space, the conviction that massive battery demand is here already and coming fast has grown.

A good strategy is a high-level plan to achieve one or more goals under conditions of uncertainty, designed through recognizing the challenge (diagnosis), setting a direction to overcome it (guiding policy), and detailing steps to implement the policy (coherent actions).

The diagnosis should be the most solid, followed by the guiding policy, and then the coherent actions. And that’s what we see here.

The diagnosis – that extreme battery market growth is coming – has remained consistent since before the company was born.

Its initial hypothesis, or guiding policy, that “battery pack assembly is the most strategic part of the value chain to build around” remains the operative hypothesis. Already, the team believed that co-designing the factory and the product – the Deployment Factory – would be critical.

But as you’d expect in a good strategy, some of the coherent actions have changed as the team learns.

The Week 3 Update included three bullets with assumptions that haven’t survived further testing. I’ll share them here and come back to them later, because understanding why Base changed its mind illustrates the push and pull of building a system instead of a product:

We no longer think it makes sense to build a Retail Electric Provider (REP) to start.

We are no longer exclusively focused on Texas as an initial market for the company, even though we are still planning to build the company in Texas.

It is increasingly clear that an initial go to market focused on utility scale/commercial buyers could help us achieve scaler earlier.

Today, Base is building a REP in Texas focused on the residential market, the opposite approach to what those three bullets suggest.

To understand why the company changed its mind, we need to head deeper in the idea maze, starting with a piece that isn’t likely to change: the hypothesis around manufacturing battery packs. As we flow through the series of interconnected decisions, we can understand why Base looks the way it does today.

Why manufacture battery packs?

Today, to get off the ground quickly, Base is installing batteries manufactured by other companies. The plan, however, is to manufacture its own battery packs. It expects to roll its own out in Q4.

Why, when there are good batteries Base can buy off the shelf, would it build its own?

There’s nothing on the market that’s quite right for the system Base is building.

All of the existing residential batteries on the market are small, mainly designed to be paired with rooftop solar in order to provide backup to the specific customer’s home.

The companies that sell solar panels and batteries have built their businesses around high-margin hardware sales. As discussed earlier, residential battery adoption has been low because these batteries are expensive for consumers and take a long time to pay back.

But if the point of a system that runs on solar, battery, and electric appliances is that it’s more reliable and cheaper, Base believes that batteries should be sold with a cost saving value proposition. That requires a business model innovation – becoming a power-trading REP, as we’ll discuss – and it also requires optimizing installation.

Remember that graph from all the way at the beginning, the one that showed that even though power production was getting cheaper, power costs remain the same because power delivery is getting more expensive? There’s a similar dynamic at play here.

As batteries get commoditized, they’ll continue to get cheaper. The real bottleneck and cost driver won’t be the batteries themselves, but the costs to install them.

As Justin explained, labor time, cost, management, and the availability of enough skilled tradespeople to install batteries will be a rate-limiter on the business. There’s a shortage of electricians, and the more demand for batteries, the worse that shortage will get, leading to higher costs and longer timelines. So, like Hadrian, Base wants to expand the talent pool by simplifying the process.

Some of that can be accomplished with software and operations, things like step-by-step documentation, software checklists, and route optimization.

But most of the improvement will come from the hardware: it needs to be designed to be extremely simple to install.

“We think about installs in minutes and seconds, like a NASCAR pit stop,” Justin said. “Not days or weeks.”

So instead of thinking about installs like construction – send a bunch of parts to the home and make skilled people to build and connect the battery there – think about them like manufacturing. Do as much of the hard stuff as you can in the factory so that it’s easy as possible on-site. This is a theme that we heard from nuclear founders on Age of Miracles: to bring down costs, shift as much as possible from construction to manufacturing, where it can benefit from learning curves.

That means designing and manufacturing battery packs with installation in mind. Six easy-to-transport modules that snap together instead of one big heavy thing that requires a forklift or a crane to move. Connectors that installers can snap together like LEGO blocks instead of cutting and crimping wires.

Maybe most importantly, because the battery is larger than competitors’, it can act as the single source of power for the home, and therefore doesn’t require the installation of a separate critical loads panel like the Powerwall does. Installing a critical loads panel involves rewiring the home’s existing electrical system - switching circuits, running wire and conduit, and more. Removing that step alone will be a tremendous time and labor saver.

As Base learns from installers in the field, it can incorporate feedback into the design of the pack itself. While it benefits from learning curves in the cost of lithium-ion cells, which are certainly becoming commoditized, it can try to create its own learning curve on the pack + install piece, making the whole offering cheaper.

Plus, by controlling the hardware, Base can better integrate its firmware and software – the Battery Management System (BMS). That lets it do things to improve the battery’s performance and extend its life, better control charge and discharge, and give customers more real-time information on their batteries. It also gives them the best demand data in the market, which is crucial for balancing the grid and making money in the process.

That’s important, because Base doesn’t plan to make money by selling high-margin hardware. It’s not even going to sell the hardware.

Why a Retail Electric Provider?

Base is betting on business model innovation as much as any technical innovation.

While competitors sell high-margin hardware to customers, Base owns the batteries it installs. It only charges customers for install and takes on the risk of the battery itself. That should be a much easier financial decision for many customers.

The insight here is that the battery is more valuable to the market than it is to any one homeowner, so the market participant - Base, in this case – should own it.

It’s not a perfect analogy, but you can think of it like AWS. Instead of each company spinning up its own servers, and inevitably either wasting or running out of compute, AWS can own a ton of servers and rent them to companies as they need them. One hundred servers in an AWS datacenter are more efficiently utilized than 100 servers at 100 separate offices.

The difference is that AWS puts all of its servers in one datacenter, like battery farms do, whereas Base needs to install batteries at each of its customers’ homes in order to solve both supply and demand volatility. It then uses software to get the distributed batteries to work together.

If AWS switched the model from selling servers to selling compute, Base is switching the model from selling batteries to selling power.

To do that, it’s operating as a Retail Electric Provider. What’s that?

There are two types of electricity markets: regulated and deregulated. In regulated markets, government-regulated utilities handle the entire process of generating, transmitting, distributing, and selling electricity to customers. In deregulated markets, generation and retail sales are separated from transmission and distribution (which are still regulated), and consumers can choose among REPs who offer different plans, terms, and services.

In Brooklyn, for example, I can choose among 75 REPs who compete on terms, price, and renewable mix. If I want to pay a little more for 100% renewable energy, I can.

Instead of generating their own power, REPs purchase electricity from generators and sell it to customers for a spread. Then they handle things like billing and customer service.

Many of you reading this live in deregulated markets like New York, California, and Texas. Tell me. Do you love your REP?

Khosla Ventures’ Keith Rabois has this famous tweet laying out a formula for startup success:

It’s hard to find a market that fits that better than REPs. In Brooklyn alone, I have 75 options. I feel no love for any of them. In fact, in a survey of utility customers (broader than REP, but I think directionally correct), the highest performing utility had a very mediocre Net Promoter Score (NPS) of 44, and the worst had an NPS of -12.4. The average is 20.3. That’s a low NPS.

And the market is large. Single-family homes account for roughly 20% of US power demand, or about $200 billion in annual electricity spend. It’s not just a large market in aggregate, but one of many consumer’s biggest spending categories. In 2021, the average American household spent $121/month on electricity.

Base plans to compete with this fragmented, low-NPS mass of REPs by offering a modern consumer experience, backed by a battery.

On the experience side, Base is probably the only REP with former Apple, Tesla, and Ramp software engineers on staff. By doing table-stakes things like Apple/Google/CashApp payments, gamification of power usage, and real-time tracking and visualization, it can offer a better product experience than competitors can.

The battery, though, is the real differentiator.

Obviously, with a battery, customers get more reliable power. The Base battery will offer hours or days of backup, depending on usage. Base customers won’t have to worry about power outages, because when the power goes down on the grid, the battery will just take over. (Seeing your neighbor’s power on while yours is off during an outage is great word of mouth marketing, too).

Less obviously, but as importantly, the battery means that Base can offer customers a lower price on their electricity. The reason is counterintuitive.

Selling electricity in a deregulated market is a low-margin, high-risk business. It’s low margin because it’s competitive, and REPs have to buy from generators and sell to price-sensitive consumers. It’s high risk because prices can fluctuate wildly. For most REPs, that makes selling electricity even lower margin, because they need to hedge their risk with financial instruments for which they pay a premium.

“The hedge is a financial battery,” as Jared described it. “The battery is a technical hedge.”

Since Base can hedge with technology instead of options, it can pass the savings it would have otherwise spent on premiums back to customers.

A better product at a lower price in a large, highly-fragmented, low NPS market is a good combination if Base can pull it off.

But Base’s goal isn’t to build the world’s best REP. It wants to build one of the country’s largest and most profitable battery storage portfolios. The REP is a channel to get as many batteries as possible distributed across the state of Texas, to start, as quickly and cheaply as possible.

The core business is using those batteries to trade energy and provide ancillary services to the grid.

Why is distributed better for power trading and ancillary services?

Base plans to make money by soaking up energy when it’s cheap and discharging it when it’s expensive. If they do it right, it’s a win-win: good for the business, and good for the grid.

There are two main ways it can make money this way: power trading and grid ancillary services.

Power trading is straightforward: buy low, sell high.

Because Base is an REP, it can buy electricity at off-peak times when prices are low, and sell it back to both customers and the grid when prices are high. Power can be purchased in real-time or day-ahead markets, and owning storage capacity means that Base can purchase in the more stable day-ahead markets and sell into more volatile real-time markets (or soak up more power real-time when prices are unexpectedly low). If Base can consistently charge when prices are low and discharge when they’re high, it can make money.

Now that Base has its first REP customers, it’s kicked off trading. The image below shows that it sold power it had stored – some to customers, some back to the grid. They’re small numbers, but Base power trading is officially in business.

Grid ancillary services are things that the grid pays market participants to do in order to stabilize the grid. They include frequency regulation (charging or discharging on-demand to balance drops or spikes in grid frequency), voltage support (injecting or absorbing the power needed to support the magnetic and electric fields in transformers, electric motors, and relays), reserves (standing ready to inject power into the grid in the case of generation shortfalls), demand response (getting paid to lower usage), and ramp support and load following (quickly ramping up or down to match variability in renewable energy generation). The grid pays companies for providing these services, either directly through mechanisms like capacity payments or indirectly through markets.

If you’ve heard of the “duck curve,” it’s the phenomenon where net demand for energy from the traditional grid is low during the day when solar power is firing, and then ramps quickly when the sun sets. Even though it’s predictable, it’s tricky to get all of the traditional generating capacity fired up to meet such a sharp increase in demand. Batteries can help, as Patrick Collison points out, and the grid will pay battery operators for that capability.

Base will make money in both ways: through trading and ancillary services. But so do battery farms, and battery farms have a much simpler model.

Building out a distributed network of batteries is a hard and potentially expensive thing to do. You need to build the batteries, acquire customers one-at-a-time, and install batteries, then you need to manage those batteries, buy electricity from generators, and bill customers and handle their customer service inquiries.

Considering all that, it’s understandable that most of the big players have built centralized battery farms. If they make money by buying a bunch of batteries on leverage and paying them back by trading power and providing ancillary services to the grid, then they opt for the simplest way to put a lot of storage capacity on the grid.

But putting smart batteries next to load has advantages if you’re able to overcome the challenges.

Earlier, we discussed why residential batteries are better for the grid. Putting them next to the home solves demand and supply volatility. Importantly, residential batteries lower congestion on the grid at peak times, lowering overall power costs.

That California batteries versus duck curve chart that Patrick Collison tweeted is great, but as Ryan McEntush pointed out in response, transmission prices spike as all of those batteries discharge power onto transmission lines at once, making power even more expensive.

The price spike isn’t the batteries’ fault. Something was going to need to put a lot of power on the grid quickly. But the problem remains: the transmission costs are too damn high!

There used to be a bit on the Reply All podcast called Yes Yes No, where one co-host would read a random tweet and the other would try to figure out what it meant. Now that we’re nearly 10,000 words in, we can play a little Yes Yes No of our own:

Casey says that we need less than one order of magnitude more batteries to support California’s heavily-renewable grid. The Dude replies that we still have a transmission problem, because batteries are centralized and discharge into an overloaded grid at the same time. Casey replies that sufficient batteries solve this problem. And The Dude tells them that batteries don’t solve the problem unless you put them where the demand is, which he says is inefficient!

Putting batteries on premise is what Base is doing. It’s how you solve the grid. In the last two sections, we talked about how Base plans to handle the inefficiency by manufacturing battery packs, getting really good at install, and building a modern REP that can acquire customers efficiently. Solve the inefficiency, solve the grid.

But while the Base team wants to solve a really big challenge, they’re not doing this altruistically. They want to solve a big challenge by building a big business.

It turns out, if you can overcome the inefficiencies, building a distributed storage portfolio also has advantages for both trading and ancillary services.

It starts with better data. Because Base’s battery is the home’s interface with the grid, it knows what’s happening on its customers’ circuits in real-time. Fluctuations in demand are mainly a function of residential HVAC, and Base knows when people are turning on their air conditioners before anyone else in the market. They know what’s happening in real-time because they have a computer managing demand on every battery. Other market participants get data on a 5-minute delay. With more batteries, that should give them an increasingly unfair advantage.

Jared told me that since most of the grid was built over 50 years ago, it doesn’t have closed loop monitoring or controls. “When we talk to people about what we’re building,” he said, “the heavy-hitter question is: will you be able to get telemetry data faster than every 5 minutes? The answer is definitely yes. We’ll have sub-second data, minutes aren’t in our vocabulary.”

Another advantage is that Base will be everywhere. Battery farms spend a lot of time and money upfront figuring out where to locate their project, but the whole process - permitting, construction, interconnect – takes roughly five years to get through. The best place to put the battery farm today probably isn’t the same place it was five years ago.

Base, on the other hand, will put batteries all over the grid in different Location Marginal Pricing (LMP) and load zones. That gives it diverse exposure to different prices in different areas, and allows it to monetize congestion. They can also help financial traders hedge against transmission constraints, and get paid to do so.

As it scales its portfolio, Base will have batteries all over the grid producing real-time data and charging and discharging on-demand to respond to price signals and grid needs. While battery farms contribute to congestion by discharging all at once, Base can ameliorate and monetize congestion, which is important, because congestion pricing scales non-linearly as reserves drop, which means an opportunity for greater profits.

The same advantages that apply to trading hold for ancillary services, where Base can bid into markets for ancillary services with better data and more locational precision than anyone else, which means it should be able to offer better pricing and win more bids than competitors.

Over time and with scale, Base’s advantages compound.

As it becomes more profitable at trading, it can offer REP customers lower prices, eating more of the market more quickly and putting more batteries on the grid. At enough scale, it can work directly with utilities to provide backup power to more and more of the grid. If a utility needs to do six hours of maintenance on the system, for example, Base can say, “Great, we have eight hours worth of power, so open up your switch and we’ve got the network.”

It will take a well-orchestrated symphony of battery manufacturing, install, power trading, consumer marketing, and more to get to that point, but if it can overcome the inefficiencies of building a distributed system, then Base has a real opportunity to fix an increasingly renewable and electrified grid while building up the most profitable battery portfolio on it.

Why Texas?

Everything is bigger in Texas, and everything I just wrote is supercharged in Texas.

In that Week 3 Update, Zach wrote that Base would not start by focusing on Texas because, as an unregulated market, prices in Texas are volatile. He also wrote that Base would not build an REP, because the need to hedge would make the business more capital intensive and riskier.

But one of Base’s principles, picked up from its team’s time at SpaceX and Tesla, is “Question Assumptions.”

Like: the need to hedge power price risk would make the business more capital intensive and riskier. At some point, the team realized that batteries were the hedge, and that because of that, they’d have a built-in advantage over the competition.

Then: if you’re an REP with batteries, then price volatility can be a very good thing.

And: if you’re looking for volatility, there’s no better place to look than Texas.

When it comes to power, Texas is an island. Its grid, managed by ERCOT (Electric Reliability Council of Texas) is mostly isolated from the rest of the United States’ power grids.

While California and New York also have their own Independent System Operators, Texas is the only state whose grid isn’t interconnected with other state’s grids.

From a regulatory standpoint, that means that Texas is the only grid not federally regulated by FERC (Federal Energy Regulatory Commission). The Public Utility Commission of Texas (PUC) regulates ERCOT, particularly as it concerns electricity rates.

From a reliability standpoint, it means that Texan generators are responsible for producing the power that Texan consumers consume.

Interconnections – the physical and operational links between different power systems that allow them to transfer electricity among each other – allow other states to rely on each other to balance their grids. They can balance supply and demand across a wider range of generation capabilities, local weather conditions, and demand profiles. Texas is all on its own.

A grid is a tricky thing to manage all by yourself, made more tricky in recent years by the growing share of renewables in Texas’ generation mix. Texas is blessed by nature. It sits at the intersection of America’s Sun Belt and its Wind Belt, and as a result, it is the country’s largest wind power producer and its second largest solar producer.

It may surprise you that Texas is so big on renewables, until you realize that Texas is the most free market of all of the grids. It’s an energy-only market in which power plants are paid only for the energy they produce, and unlike in regulated markets, in which utilities can choose the source of power they provide to customers based on other factors like reliability, Texan generators compete in wholesale markets based on price. When they’re on, solar and wind have a cheaper marginal price than other power sources, so they win, at the expense of reliability.

The market makes up for this through scarcity pricing mechanisms: ERCOT introduces congestion pricing – kind of like Uber’s surge pricing – to incentivize more capacity to come online when it’s needed. It’s the only grid without a capacity market, in which generators are paid simply for being available to produce if needed, opting to ensure reliability through market signals alone.

As a result, the transition to renewables and electrified everything has been particularly bumpy in Texas, where electricity is cheaper when the getting’s good but less reliable when it isn’t. Plus, Texas has more extreme weather – very hot and very cold – than its renewable-heavy counterparts like California. As a result, last year, Texans experienced 20 hours without electricity, up 6x from three hours in 2013.

The point of a free market, though, is that while it can be messier in the short-run than a centrally-planned one, it leaves room for market-based solutions that can be better in the long-run. Base thinks it can be part of that solution, and that Texas is the ideal place for it to start.

First, because Texans are experiencing more frequent and longer outages, the battery value prop resonates with them in a way that’s hard to understand if you live in a state with a more stable grid. A more acute need paired with an economical solution should help it grow its customer base as quickly as its installation pace will allow.

Second, once those batteries are in place, they can be more profitable in Texas than they would be in other states. On Sunday morning, I pulled up GridStatus.io (which is worth checking out for a feel for how all of this works), and this is what I saw:

While each of the other ISOs real-time prices pretty closely tracked day-ahead prices (predictions made the day ahead, which are purchasable), ERCOT real-time prices ($92/MWh) had spiked far above day-ahead prices ($23/MWh). If Base charged its batteries overnight at $15/MWh real-time prices, it could have made $77 for every MWh it discharged back to the grid. And that’s actually a low spread. There are some days in the summer when you can charge for $0 and discharge for $5,000/MWh.

It doesn’t take too many days like that to pay back an ~$8,000 20kWh battery.

Base can build a big business in Texas alone, but it plans to prove the model in Texas, then move on to other deregulated markets as more renewables and electrification destabilize their grids, too.

California is an interesting next target for a battery company: because so much solar is produced in the middle of the day, Base could be paid to charge, and then discharge when prices are above zero. After deregulated markets, it can partner with utilities in regulated markets as they too shift to more renewables, and their customers electrify more of their energy consumption.

By cutting its teeth in Texas, Base believes it can become one of the most sophisticated Virtual Power Plant (VPP) operators in the market. Then, it can compete with companies like Tesla, Sunrun, and Sunnova in regulated markets, where they currently partner with existing utilities to run VPPs. Base thinks that by flipping the model - from selling hardware to selling power – it can win against the companies who have failed to aggregate much demand due to lack of customers willing to pay.

Or, Base hopes, by showing that deregulated energy markets can work really well in Texas, it can convince other states to adopt regulatory frameworks more similar to the Lone Star State’s. To be fair, Texas’ deregulated energy-only market has been a mixed bag. In 2021, Winter Storm Uri left millions of Texans without power for days and left the whole market shook.

But if Base is right, and it can prove it in Texas, it might show that renewables, free markets, and batteries offer a combination of low-prices and reliability that regulated systems can’t match.

As former PUC Commissioner Will McAdams said on the Energy Capital Podcast:

We've doubled our battery capacity. We will double it again very soon. And batteries are right at home in what's going on right now. It has been an invaluable resource and will be a critical resource managing through the seasons that we're soon to see with the amount of load growth patterns that we have today. And so every energy company in the world is either looking at Texas or has invested capital in Texas to some degree.

But that’s a long way away. For now, Texas will keep Base busy for a long time. There are 11 million homes in the state, increasingly powered by renewable energy, with a quarter of a million electric vehicles to plug in at the end of each day, growing to half a million with haste. If Base can fix Texas’ grid, it can fix ‘em all. And in the process, it can build up one of the largest and most profitable battery storage portfolios in the country.

The Base Business Model

We just covered a lot of complexity to arrive back at a business model that’s really quite simple:

building a large portfolio of connected batteries with short paybacks and high cash on cash returns.

Building storage portfolios is a good business no matter how you slice it, so good that Casey Handmer used an exclamation point when he wrote: “Indeed, while new solar farms take 5-20 years to pay for themselves, battery plants are so lucrative they’re often profitable by year two – which is unheard of in the energy infrastructure space!”

Broad Reach, which was founded in 2019, was acquired for $1 billion in equity value in 2023, at just four years old, and with only 350 MW of storage in operation (with another 880 MW under construction). Now that batteries are getting cheaper, renewables are getting more plentiful, and demand for electricity is picking up, building a profitable portfolio of batteries is easier than it’s ever been.

But to build the most profitable portfolio, and one that alleviates the grid’s challenges, Base believes that you need to do a whole lot of hard things, at once, in such a way that the whole system works in a way that no competitor can match.

You need to manufacture batteries, and design a whole Deployment Factory, optimized to lower the cost of the whole installation at scale.

You need to offer the batteries as part of a larger REP offering, and offer them at install cost (taking on the cost of the battery yourself) in order to increase adoption.

You need to turn that adoption into a distributed network of batteries that produces demand signals in real-time, and can charge and dispatch on-demand in order to profitably trade power and offer ancillary services to the grid.

And you need to start in Texas, the most isolated and volatile grid in America, in order to create, and capture, the most value.

To make it more clear, let’s look at that ERCOT summer 2023 chart again.

In a purely financial market, an arbitrage like that would get traded away within minutes, maybe seconds.

But batteries aren’t a purely financial market. Accessing the arbitrage requires a lot of hard engineering, manufacturing, distribution, sales, and software.

If you can pull all of that off, you have the arbitrage practically to yourself as long as you can keep competitors at bay.

To that end, and I will bang this drum until my face turns blue, digging a moat is key.

“The moat,” Zach told me, “is ‘hard.’”

Each of the high-level things that Base does has a thousand sub-steps, and a small team of talented people within the company tasked with making sure they’re executed in lockstep. With each coherent action they pull off, the moat against would-be competitors deepens.

Manufacturing its own batteries means it won’t need to pay a margin to battery companies like the battery farms do. Using those batteries to offer better reliability and cheaper prices than other REPs means it should be able to acquire customers more cheaply, and retain them longer. Adding more batteries to the grid gives Base more data in more locations than anyone in Texas, and a greater ability to profit on that data. Continuing to hire world-class engineering talent in an industry that traditionally hasn’t means that they can keep doing all of those things better and faster than a competitor can.

That’s the plan, at least.

Today, Base is officially online in Texas, serving a handful of homes with third-party batteries and REP service, powered by Base’s software. It’s aiming to ramp up to dozens installs by the end of Q2. In Q4, it will roll out v1 of its own Base-manufactured batteries, which will speed up installation and improve Base’s responsiveness to the grid’s needs. As it installs, it’s learning and adjusting. HOA’s are proving to be trickier than expected, but they’re figuring it out.

For now, Base is financing batteries off of its own balance sheet. In the months ahead, it needs to grow the portfolio and prove out the economics of its batteries so that it can secure asset-backed loans to fuel its growth. Building a portfolio that appeals to lenders means that Base can unlock a lower cost of capital, which means more batteries and more profits, and ultimately even lower costs of capital. The moat widens.

Combine the balance sheet of a PE-backed storage portfolio with the engineering and operational chops of a SpaceX in a trillion-dollar market, and you’re in business.

That said, Base is trying to build a power company on hard mode, and there are a lot of challenges – real and surmountable – ahead. Let’s go through them.

The Arguments Against Base

The simplest reason that Base might fail is the same as its moat if it succeeds: it’s hard.

That should be painfully obvious at this point. Manufacturing batteries is hard. Installing them is hard. Acquiring customers is hard. Convincing them to pay for a big battery on the side of their house is hard. Power trading is hard. Distributed software is hard. Financing a portfolio of individual batteries with no offtake agreements is hard. Each thing that Base has to do individually is hard, and the model depends on all of them working together. That’s why hiring has been the highest priority, but even with the best people, getting all of this right will be hard. That’s obvious.

But there are more nuanced arguments for why Base might not work, or might not be needed, and I asked the team about them. They range from dumb to smart.

The dumb argument is that we won’t need batteries if we just add a bunch of nuclear, which we should. There are a few reasons this one doesn’t hold up.

The first is that adding new nuclear capacity is really hard. With Vogtle 4 online, there are no new large-scale nuclear projects in the pipeline. We should do everything we can to change that – and I’m particularly excited about hyperscalers adding nuclear to power AI datacenters – but we can’t rely on nuclear as our only hope.