Bad Analogies

Not Every Money-Burning Company is Amazon

Welcome to the 514 newly Not Boring people who have joined us since our last essay! Join 261,204 smart, curious folks by subscribing here:

Hi friends 👋,

Happy Thursday! I wasn’t planning on sending an essay this week. I wanted to give you a little time to breathe after World Models and Electromagnetism.

But then I saw someone make a bad point on the internet, and it was a particular bad point that has always bugged me, so I whipped up a short and sweet rebuttal. In short: not every company that burns a lot of money is the next Amazon. (a bit of a strawman, I admit, except this analogy keeps popping up!)

Let’s get to it.

Today’s Not Boring is brought to you by… Framer

Framer gives designers superpowers.

Framer is the design-first, no-code website builder that lets anyone ship a production-ready site in minutes. Whether you’re starting with a template or a blank canvas, Framer gives you total creative control with no coding required. Add animations, localize with one click, and collaborate in real-time with your whole team. You can even A/B test and track clicks with built-in analytics.

Launch for free at Framer dot com. Use code NOTBORING for a free month on Framer Pro.

Bad Analogies

I saw an interaction on twitter the other day that I’m not going to share here because these specific people don’t deserve to be singled out because almost everyone is guilty of something similar.

Basically, one person said, “It’s amazing that OpenAI was able to raise $122 billion when they don’t have a single business that works,” and the other person replied, “Yeah they do they have a bunch of different business lines doing billions of dollars in revenue,” and the OP responded, “Yes but none of them is profitable, they’re losing a lot of money,” and the replier replied, “You could have said the same thing about Amazon!”

Amazon’s success has done a great deal of harm to a great number of companies.

Obviously, it’s done more good. AWS is a miracle. But go with me.

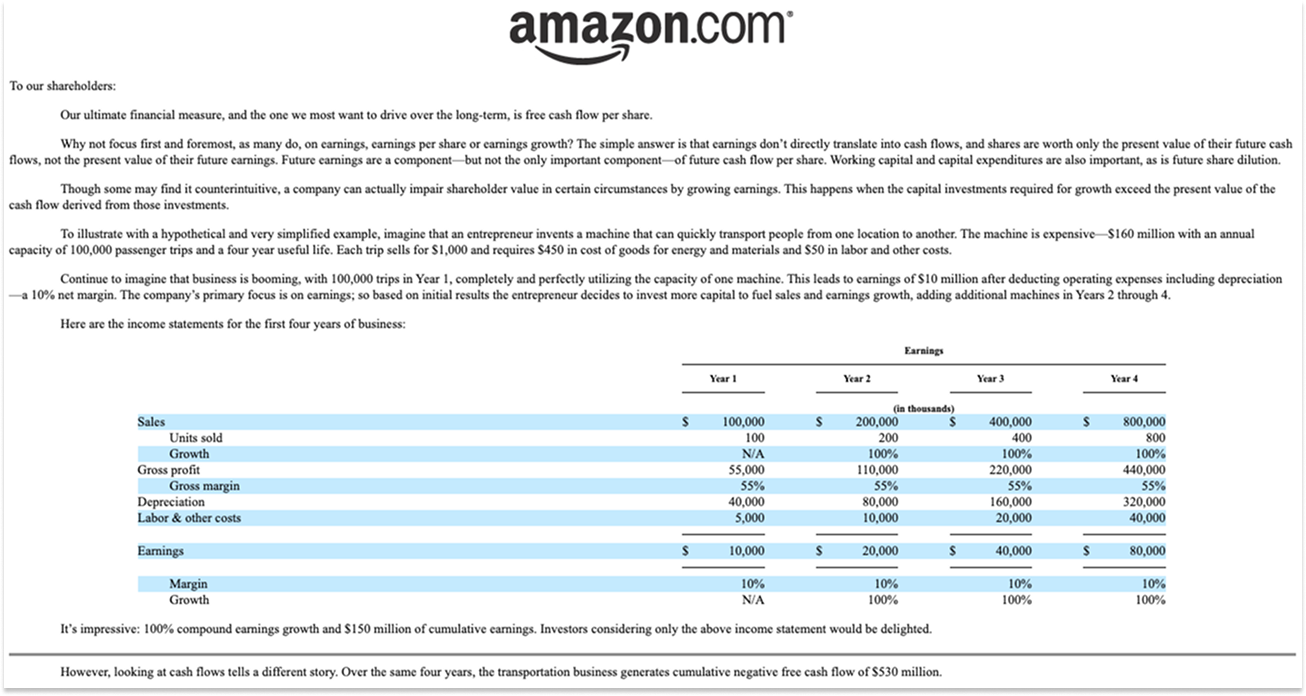

Jeff Bezos is a generational entrepreneur who came from a hedge fund and made a very calculated decision to lose money in the short term if it meant making more of it in the long term. In his 1997 Letter to Shareholders, his first as a public company CEO, he makes the trade-off he’s willing to make clear: “When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.”

He spends his entire 2004 Letter to Shareholders walking investors through the logic.

Earnings don’t directly translate into cash flows, and shares are worth only the present value of their future cash flows. Working capital and capital expenditures matter too, and a company can actually destroy shareholder value by growing earnings if the capital investments required exceed the present value of the cash flow derived from them.

Bezos had his hands firmly on the wheel, and a negative working capital engine at his back. There are a million little details that made Bezos’ plan work, all of which, and the connections between them, were taken into consideration. Get to scale category-by-category, starting with the ones best suited to the internet, build an unmatched distribution and logistics network, drive down prices and delivery times, get more scale, grow the distribution network, drive down prices, make the “divinely discontent” customers discontent with anything slower or more expensive than what they’d come to expect with Amazon, get them hooked on Prime, paying a subscription and ordering more, keep pressing the advantage, grow FCF per share. All the while, thanks to negative working capital, growth generated cash, cash funded more infrastructure, infrastructure enabled lower prices and faster delivery, which drove more growth.

We all know the Amazon story to some extent, right? I don’t need to go into more detail than that for now. We could tell a similar story about Facebook: they had no revenue! they didn’t even have a business model!

You could, and many have, use this to justify all manner of sins in your business, in a business in which you’ve invested, or, in the case of the AI labs, in a business that a bunch of weirdos on the internet seem to feel is their duty to defend.

I am perhaps a bit sensitive to this after spending six years pre-not boring in the same industry as WeWork. WeWork lost a lot of money, and so people compared WeWork to Amazon, and maybe there’s an argument to be made that of course you need to spend a lot of money in real estate because you need to do construction and furnish spaces and buy a lot of beer and tequila upfront but then you have this whole network of long-term leases that will generate cashflow for years to come. Bezos wasn’t afraid of spending money today for cashflow tomorrow, why should Neumann be? But we often put in offers on the same spaces as WeWork, and we had these super finely tuned underwriting models, and looking at our underwriting models versus the prices they paid to outbid us on certain spaces it was clear that no matter how optimistic your monthly revenue projections, there was just no way they were going to make money on each space. That was before you took into account the custom builds they were fronting for customers who signed two-year deals (builds that would potentially need to be redone for the next one) or the 100% commissions they were paying brokers for an entire year’s worth of revenue on any customer they brought in. Adam Neumann went on Rick Rubin recently, and it was incredible and made me like him more and even made me bullish on Flow, but even Adam Neumann admitted that he let the economics get away from him in the halcyon days of 2018 and 2019.

If you had justified a WeWork investment to yourself by analogizing to Amazon and repeating “It takes money to make money,” you would have lost it all in the 2023 bankruptcy. Maybe the cleaned up company makes a lot more sense today than the bloated one did then, I haven’t looked at it so I don’t know, but if it does, it’s certainly not because it’s like Amazon.

Of course, analogies can be a useful starting point. “This thing that I might have otherwise dismissed out of hand is probably worth a closer look, because things that have looked this obviously wrong in the past have turned out to look pretty good” is a good way to think.

Uber, too, lost a shitload of money. Uber lost way more money than WeWork. WeWork lost like $2-3 billion in its worst year. Uber burned $9.1 billion in 2022. Uber’s losses made WeWork’s look like rookie numbers.

And yet… Uber is still a publicly traded company, with a market cap hovering around $150 billion.

If you’d looked at Uber and said, “Hey, Amazon lost money too, let me take a closer look,” and then realized that Uber was burning money in actually kind of the same way that Amazon was, to get its product as close to customers as possible in order to improve the customer experience, particularly if you’d looked during the depths of 2022 when it was burning so much cash, you could have made a smart investment.

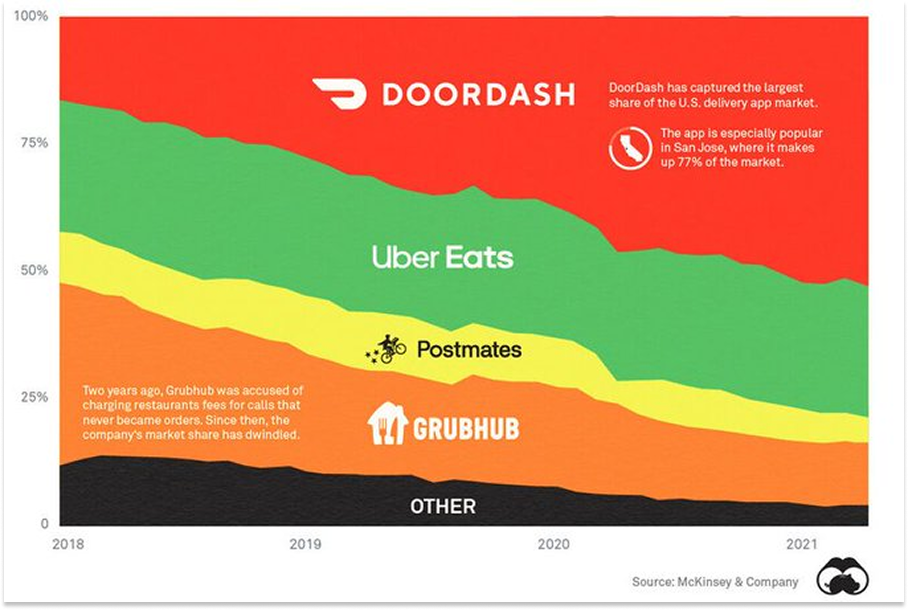

Then again, using Uber as an analogy – literally, as in Uber-for-X – has kept the startup graveyard operators in business. The one successful company that could be called an Uber-for-X is DoorDash, and it worked explicitly because the team looked at Uber, said “there’s something interesting here,” and then tuned it to fit the situation at hand. Instead of competing in dense urban markets, they took the model to underserved suburbs, where competition was lower, CACs were lower, average order values were higher, retention was higher (fewer alternatives), pickups and dropoffs were easier (stores and homes have driveways and parking lots), and then, per Dan Hockenmaier, they executed relentlessly: “They made deliveries just a little faster and more reliable every week. They scrutinized the quality of every one of their restaurants and dashers. They optimized cost out of the system and gave it back to customers in the form of Dashpass (which launched in 2018 at the start of this chart).”

So are frontier AI labs good or bad businesses? I don’t know. Smarter minds than mine are doing a lot of non-analogical work trying to answer this question. The economy depends on it.

I do know that they’re not definitely bad businesses because they’re losing money.

They are certainly generating a lot of revenue very quickly, and growing at rates that are unprecedented at their scale. Anthropic grew from a $9 billion run rate at the end of 2025 to a $19 billion run rate in February (and rumors are it went much higher in March). In announcing its $122 billion fundraise, OpenAI said, “Within a year of launching ChatGPT, we reached $1B in revenue. By the end of 2024 we were generating $1B per quarter. We are now generating $2B in revenue per month. At this stage, we are growing revenue four times faster than the companies who defined the Internet and mobile eras, including Alphabet and Meta.”

To dismiss those numbers because of a little cash burn would be just as dumb as saying that cash burn is the same as Amazon’s.

On the other hand, it’s worth looking more closely at the burn to understand what you get for it.

Amazon was a high fixed-cost business with variable revenue. The more customers it served, the cheaper each marginal customer got. Each time you ask Claude to build you an app that tells you when to do your laundry, it costs Anthropic money. Each time you ask(ed) Sora to make you a video of Sam Altman twerking, it cost OpenAI money (and scarce compute that could be used for other things), which is why they shut it down. That said, margins at both Anthropic and OpenAI are improving, and with every point in margin, that variable cost problem gets less painful.

One thing to consider is that API tokens are likely a much better business because Anthropic charges based on tokens consumed. Funnily, when I asked Claude about this, it linked me to a public artifact of research someone else had done with Claude, which said that average users of Pro and Max make Anthropic money, Heavy users of Pro and Max lose Anthropic money, and the API business (which is 70-75% of revenue) produces “50–65% gross margins on Sonnet workloads and 35–50% on Opus workloads.” Caveat emptor. This is a monster business, but I wonder how much it benefits from another bad analogy: linesofcodemaxxxxxing.

In the olden days, lines of code (LOC) were expensive to produce. Only a select few even knew how. There were more problems to solve than people or LOCs to solve them, so companies would create a backlog and their engineers would crank through them by producing more LOCs. The lines of code themselves were not the valuable thing; they were valuable insofar as they were used to solve problems the company needed to solve. You could look at a successful software company, see that they’d written a lot of code, and lazily analogize: LOCs are correlated with success, lines of code are themselves a goal. Goodhart’s Law strikes again.

“You gotta be tokenmaxxxxxing,” they’ll tell you. I do wonder if this part of the business slows down once the psychosis breaks and we have maxxxxed all that we can maxxxx. At some point, when you’ve gone too deep, the ghost of Jeff Bezos appears and asks you what any of these tokens you’re maxxxxing has done for your customers.

Anyway, another thing about Amazon’s business is that while they had a ton of direct competitors - Barnes & Noble, eBay, Walmart, a graveyard of dot com competitors - they had no real competition in their strategy. If Bezos was right that getting to scale category-by-category, starting with the ones best suited to the internet, building an unmatched distribution and logistics network, driving down prices and delivery times, getting more scale, growing the distribution network, driving down prices, making the “divinely discontent” customers discontent with anything slower or more expensive than what they’d come to expect with Amazon, getting them hooked on Prime, paying a subscription and ordering more, continuing to press the advantage, and growing FCF per share proved to be the winning strategy, Amazon would emerge on the other side of all that spend as the only company with all of that in place, and with the pricing power and control over the levers of profitability that come with domination.

Uber had direct competition, but it was weaker, and Uber was making a very explicit bet that scale and network effects were all that would matter. They were right, too, and emerged on the other side of all that spend as the only company with the right network in place, and with the pricing power and control over the levers of profitability that come with domination.

Could you say the same for any of the AI labs?

We don’t have to spend a lot of time answering this. There is a lot of direct competition. The strategies seem to be very similar from the outside. Sure, different companies play with targeting different end users, and maybe OpenAI will turn ads into a big business while Anthropic owns the enterprise (although it looks like OpenAI is pushing all of its resources towards competing directly for coding and enterprise), but the core strategy is spend a lot on CapEx now to build increasingly strong models and maybe God is on the other side of all of that spend.

Ask any of the polytheistic religions whether competition among the gods is any less intense. And if we’re playing gods, Google is probably Zeus. Meta is Hermes - god of commerce, god of thieves, trickster god making everyone else’s shit more expensive. Should we do DeepSeek? Sun Wukong, the Monkey God who stole and devoured the peaches of immortality until the Jade Emperor begged Buddha to intervene, and Buddha trapped him under a mountain.

Our competition is multidenominational, and everyone is fighting with basically the same weapons. Every major lab, it seems, prays at the same altar, the Altar of Scaling Laws.

But! You say. But! Recursive self-improvement! Fast takeoff! Those tokens aren’t just producing code — they’re creating a proprietary data flywheel! There will be One True God.

Maybe!

Another reason I am allergic to some of this analogizing and extrapolating is because I have done it myself. I, too, have sinned. I have analogized crypto protocols to companies that didn’t fit just right. I have written I, Exponential and Compounding Crazy. As much as you think you love a good exponential, I can assure you I love them more. So when I ever dare question whether AI might hit a ceiling before it makes us irrelevant meatbags, and am met with the inevitable, “You don’t get exponentials! This is exactly like X! Have you even seen the Tim Urban chart?!” just know that I know these tricks. I have learned their painful lessons.

Not all exponentials are created equal. Does God think forever or does he know all in an instant?

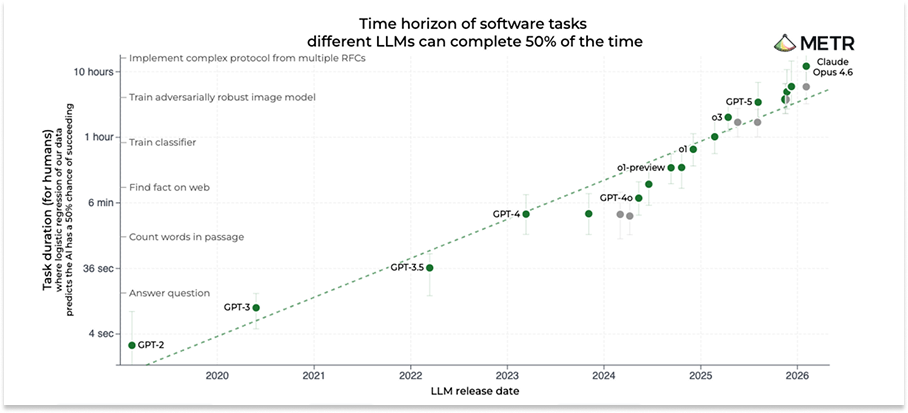

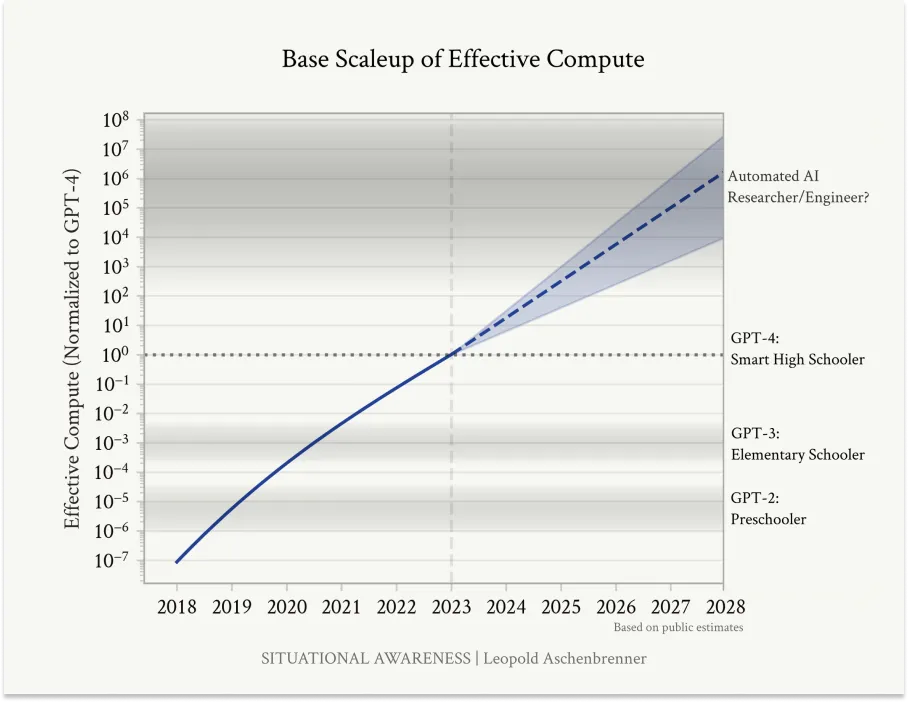

I have been pushing back against Leopold’s assertion that believing ASI will come soon after 2027 “doesn’t require believing in sci-fi; it just requires believing in straight lines on a graph” since he first tweeted it. (to be fair, he’s made billions more dollars than me in the interim.)

Just this week, METR’s Joel Becker wrote a post attempting to provide an intuition for the “Straight lines on graphs” argument. The point is that even if it doesn’t make sense, the line will continue to go up. We’ll figure out ways. But my point is that even if the models can think longer, it doesn’t mean that we will birth God. I think we’re going to end up with really excellent software, which is great, instead of an all-knowing and all-loving AI.

AND, more relevant to the Amazon discussion, if each lab’s model can think longer and get smarter at roughly the same rate, without any clear runaway winner, then the situation is not analogous to Amazon, or even Uber, who ate short-term pain for long-term strategic solitude.

I don’t mean to pick on the AI labs, I don’t even think they themselves are the ones perpetrating this malanalogous thinking, it’s just that they’re the only thing anyone is talking about so they are the richest source of bad analogies. And I really don’t know how it’s going to play out. There is a chance we wake up in a decade and OpenAI and Anthropic are the most valuable companies in the world. There is also a chance that they are the AOLs of this whole thing. There’s a chance that the biggest business in a decade is the one that bought all the cheap tokens after the crash, the way Rockefeller bought all the excess rail capacity worth buying.

AOL and Rockefeller are analogies, too, huh? Avoiding them is hard, because they truly are useful starting points. They’re so easy to reach for, in fact, that on their own, they are at best consensus and at worst dangerous.

It’s the work you do from those starting points that will decide whether you end up the next Hummer Winblad or the next J.P. Morgan. (damnit)

That’s all for today. If you liked what you read, join us in not boring world:

We’ll be back in your inbox tomorrow with a Weekly Dose.

Thanks for reading,

Packy

Fantastic read.

And a good John D Rockefeller analogy is always appreciated

the wework one always bothered me too. the amazon defense only works if the losses are funding a compounding structural advantage. wework was burning money on buildouts with no real defensibility on the other side. the economics were just bad.