The Space Economy

Payload Space joins us to drop an in-depth S-1 for space

Welcome to the 1,582 newly Not Boring people who have joined us since last Monday! If you haven’t subscribed, join 145,467 smart, curious folks by subscribing here:

Today’s Not Boring is brought to you by… WorkOS

Building for the enterprise is typically complex, time-consuming, and distracting. Deals sometimes slip away due to strict requirements and technological demands from IT admins.

With WorkOS, startups can sell to large enterprise customers from day one. It’s a set of building blocks for quickly adding features like Single Sign-On (SAML), Directory Sync (SCIM), and Multi-Factor Authentication (MFA) with just a few lines of code.

Fast-growing B2B SaaS companies like Loom, PlanetScale, Airbase, and many others use WorkOS to abstract the integrations between dozens of identity providers. Webflow uses WorkOS to serve customers like Zendesk. Vercel leverages WorkOS to land enterprise customers like The Washington Post.

WorkOS is an API that increases your TAM. It’s free to get started and scales with you as you grow.

Hi friends 👋,

Happy Monday! Big news over here at Not Boring HQ: our daughter, Maya, was born last weekend! 🥳 Mom and baby are healthy and happy, and we’re enjoying the time together as a family.

The plan for my month of paternity leave is to bring in guest writers each week who are experts in areas that I think are going to be deeply important. Last week, we had Kevin Miao join to talk about securitization on the blockchain. Today, we’re bringing in the space cadets from Payload Space for an incredibly deep dive on the space economy, in the form of an S-1 for the industry.

They nailed it. I was giddy reading the draft that Mo Islam and Ryan Duffy sent over this week. We’ve touched on space a little bit in Not Boring, and we’ve invested in space companies like Varda and Hadrian (see deep dive), but I don’t know nearly as much as I want to about all of the progress going on in the industry. Space sounds like futuristic sci-fi, and if you’re not familiar, it’s hard to believe how vibrant and multi-faceted the space economy is today.

Plus, one of the things I’m most jealous of Dev and Maya about is that they’re almost certainly going to get to travel to space in their lifetimes. As a responsible parent, I want to know what they’re getting into.

There’s no one better at covering space than the Payload team. It’s what industry insiders read, and how I’m trying to get up to speed myself, and I’m pumped that they agreed to write a Not Boring-style deep dive for us. If you’re at all interested in the … space … and want to stay up-to-date, you need to subscribe to Payload.

5…4…3…2…1… Let’s get to it.

The Space Economy

TABLE OF CONTENTS

Prospectus Summary

Market, Industry and Other Data

Use of Proceeds

Dilution

Business (Models)

Principal Stockholders

Underwriting

Legal Matters

Risk Factors

Final Remarks

PROSPECTUS SUMMARY

Here at Payload, we try to be very judicious and sparing with our use of space clichés. We’re a B2B and B2G publisher writing for the shot-callers of space. They do not want to read a half-baked joke that “actually, this is rocket science.” They’ve heard it before. It doesn’t fly.

But today, dear readers, Payload is temporarily parting with our time-worn tradition in this prospectus summary and we’re going to let the clichés rip.

A new space age is upon us, characterized by fierce competition between superpowers and startups alike. Dozens of space unicorns are hitting escape velocity. Finally, unlike crypto, we actually are going to the Moon. Very soon.

We’re living through an age of historic firsts and massive developments, good and bad, that are happening daily in space. Just in the last few weeks, we’ve tracked the following in our daily newsletter:

On July 30, a massive Chinese Long March rocket made an uncontrolled reentry (aka tumbled back from orbit to Earth), with debris falling on Malaysia and Indonesia.

On Aug. 4, five separate launchers flew orbital missions in one day. Four of the launches were conducted by American companies, one was China’s state-owned aerospace corporation.

That same day, Blue Origin launched six people to suborbital space, including YouTuber and Dude Perfect cofounder Coby Cotton (his ticket was crowdfunded by a DAO).

SpaceX is launching its Falcon 9 at a less than weekly rate in 2022 and has refurbished and reflown some of the first-stage boosters in under a month. The company also just conducted its first static fire test of the gargantuan Super Heavy booster at its Starbase in south Texas.

Three separate launch unicorns–ABL Space Systems, Firefly, and Relativity–are poised to attempt to reach orbit for the first time in the coming weeks and months.

A wave of multibillion-dollar mergers is sweeping over the legacy satellite sector, with details emerging about two blockbuster deals that are likely to move forward.

All the while, the James Webb Space Telescope has been sending back unreal photos of our galaxy and literally letting us travel back billions of years in time.

There’s plenty more where that came from. In this essay, we’ll tell you everything you need to know about how we got here and where we’re headed.

Payload was founded on the premise that the space industry is at an inflection point. What was once monopolized by superpowers is now being privatized, with companies taking greater share of low-Earth orbit, rocket launches, and more. So, because we passionately believe in this inflection point thesis, we’ve packaged this new space primer as an S-1. It’s an intellectual exercise unpacking what taking the space industry, broadly speaking, public. Is it tech-growth stage? Yes. Is it profitable? Ehhhhh. What else do you need to know? Well, let’s dive in…

MARKET, INDUSTRY AND OTHER DATA

Space: A brief history

On Oct. 4, 1957, the Soviets launched the first artificial satellite into space. The soccer ball-sized spacecraft was named Sputnik. That word, we think, went to become one of the most famous Russian words in non-Russian tongues and English-language history books. The “Sputnik crisis” caught the West completely by surprise, clearly dividing history and the Cold War into two separate eras: “pre-Sputnik” and “post-Sputnik.”

Perceptions are everything. The New York Times had a rare three-fold headliner story on the Soviets’ successful launch. Paranoia set in among American policymakers and the general public awakened to the space age. Post-Sputnik, the perception of a Pax Americana and pacing Soviet Union gave way to a public view that the Soviets had achieved a step change not just in space. The Soviets were running up a “technology gap” over the Americans.

The race was on, with the two superpowers’ space programs kicking off a new front in the Cold War and one of the greatest technological showdowns of modern history.

Less than one month after Sputnik 1, the Soviets sent a ~1,120 lb. satellite into Earth orbit with radio transmitters, a thermal control unit, sealed cabin, and a husky-spitz mut named Laika. The Soviets hadn’t build any Earth return capabilities into Sputnik 2, so sadly, Laika didn’t make it 😓.

The pressure was on the Eisenhower administration: do something! The US delivered with Explorer 1, the Americans’ first satellite, successfully launched into space on Jan. 31, 1958, a full 119 days after the Soviets. Explorer 1 was the size of a beach ball (note: Payload only uses Earth sports balls as a metric unit for spacecraft management).

Still, congressional leaders felt that space deserved more of a federal focus–and Eisenhower established NASA in 1958 and abolished NACA (the agency’s predecessor, started in 1915). NASA’s charter was to exercise “control over aeronautical and space activities sponsored by the United States.” NASA was to handle civilian space efforts, but the Pentagon still had authority over military space programs.

Over the next three years, the Soviets and Americans worked on their space programs, but on April 12, 1961, it was the Soviets who sent the first person to space: Russian Lt. Yuri Gagarin. Mercury-era astronaut Alan Shepard became the first American to reach space (sub-orbitally) less than a month later, on May 5, 1961.

That same year, JFK set forth a national goal: “Landing a man on the moon and returning him safely to Earth within a decade.” The Americans, it should come as no surprise, were able to meet this ambitious call less than a decade later, with Neil Armstrong taking “one small step” but a “giant leap for mankind” on July 20, 1969 (nice).

As Tom Wolfe expertly chronicled in The Right Stuff, Air Force test pilots who were flying planes with rockets strapped on them in the desert would become the US’s first astronauts (part of the Mercury program). The Apollo era, though, was a high watermark for the US space program, no matter how you slice it. Astronauts were living legends and international celebrities. They drove (or, more accurately, raced) Corvettes across town in Houston. Life magazine struck a deal with the astronauts and their families to tell their stories (albeit carefully overseen by NASA handlers).

After the historic Apollo 11, the US would go on to send an additional five manned missions –Apollos 12, 14, 15, 16, and 17– and 11 men to the moon and back. Since December 19, 1972, no humans have been back to the lunar surface.

Winning the race to the Moon and inventing countless technologies out of thin air–all while using less processing power for the whole mission than an iPhone uses today–came at astronomical expense. Going to the Moon cost $283B, according to one tally. In relative terms, NASA's budget peaked from 1964 to 1966, when it consumed ~4% of all US federal government spend. That number now sits an order of magnitude lower at 0.4%.

That’s not to say that space activity dropped in the ‘70s. Companies began to launch communications satellites to carry voice, data, and eventually, TV. In 1973, the Pentagon kicked off the Global Positioning System (GPS) project. The project would take two decades to complete, with a prototype GPS bird going up 22,000+ miles above Earth in 1978 and the full constellation coming online in the mid ‘90s.

All the while, interstellar robotic probes pushed further out into the cosmos. In 1971, an American spacecraft became the first to orbit another planet (Mars). The next year, the Soviets made history by landing a spacecraft on Mars (the soft landing wasn’t so soft, as video transmission ceased from the craft after 20 seconds). They later landed not-so-softly on Venus, too. By the end of the 1970s, the US’s Voyager 1 and 2 spacecraft had sent back stunning photos of Jupiter and Saturn. The Voyagers journeyed to Neptune and Uranus (no really).

SPACE STATION

The Soviets launched the world’s first space station–Salyut 1–into low-Earth orbit (LEO) in 1971. The Soyuz 11 crew stayed aboard Salyut 1, but were killed by asphyxia due to valve failure right before reentering Earth’s atmosphere. The Salyut program would see a total of six stations launched–four for scientific research and two for military reconnaissance.

The US launched its first space station–Skylab–between 1973 and 1974. Three crews occupied Skylab for ~24 weeks, and though the microgravity lab and Earth-observing workshop was meant to last nine years, it quickly lost altitude and ultimately ended as a failure. Skylab reentered Earth’s atmosphere, and as it disintegrated, cast debris across rural regions of western Australia and into the Indian Ocean. At least nobody died?

Skylab and Salyut walked so that the International Space Station (ISS) could run.

Jointly operated by the US, Russia, Europe, Canada, and Japan, the ISS is one of the top engineering feats of the modern age. It’s been continuously occupied since 1998, longer than tens of thousands of you reading this have been alive. Right now, as you’re reading this, there are seven people on the ISS: three Russian cosmonauts, three NASA astronauts, and one European Space Agency astronaut.

The ISS is also one of the most expensive things humans have ever built, at a cost of $150 billion (the $50 billion shuttle program is typically included in the cost of the ISS as it is here). The US footed most of the bill, and NASA shells out ~$3.1 billion a year to keep things running. All good things must come to an end, and the ISS is showing its age. The station is expected to be decommissioned and deorbited into a spacecraft graveyard in the South Pacific Ocean Uninhabited Area at the end of this decade.

SPACE SHUTTLE

Reusability is all the rage in rocket jock circles these days, but the concept is not new.

You may very well have grown up watching Space Shuttle flights. The iconic vehicle was envisioned as a revolutionary transportation system that would usher in reliable, “cheap” (or cost-effective) transit to and from LEO. The spacecraft was reusable (though the boosters that launched it were not). Reusability was a key selling point.

The shuttle became the American space program’s workhorse, and across three decades, the fleet of Columbia, Challenger, Discovery, Atlantis, and Endeavour flew 135 missions and 355 humans to space.

But the Shuttle never lived up to its dreams, and by one estimate, cost ~$1B per head to transport astronauts to the International Space Station and back. Tragically, two crews and 14 lives were also lost on the Shuttle.

The Obama administration pulled the plug on the government-run program and the Shuttle flew its final flight in June 2011. Despite the program’s budget overruns and abject dangers, the Shuttle’s final mission was an emotional moment for the nation, NASA’s rank-and-file, space buffs, and astronauts alike.

After that, Washington paid Roscosmos, Russia’s space agency, to take its crews to the space station aboard Soyuz rockets.

Skin in the game

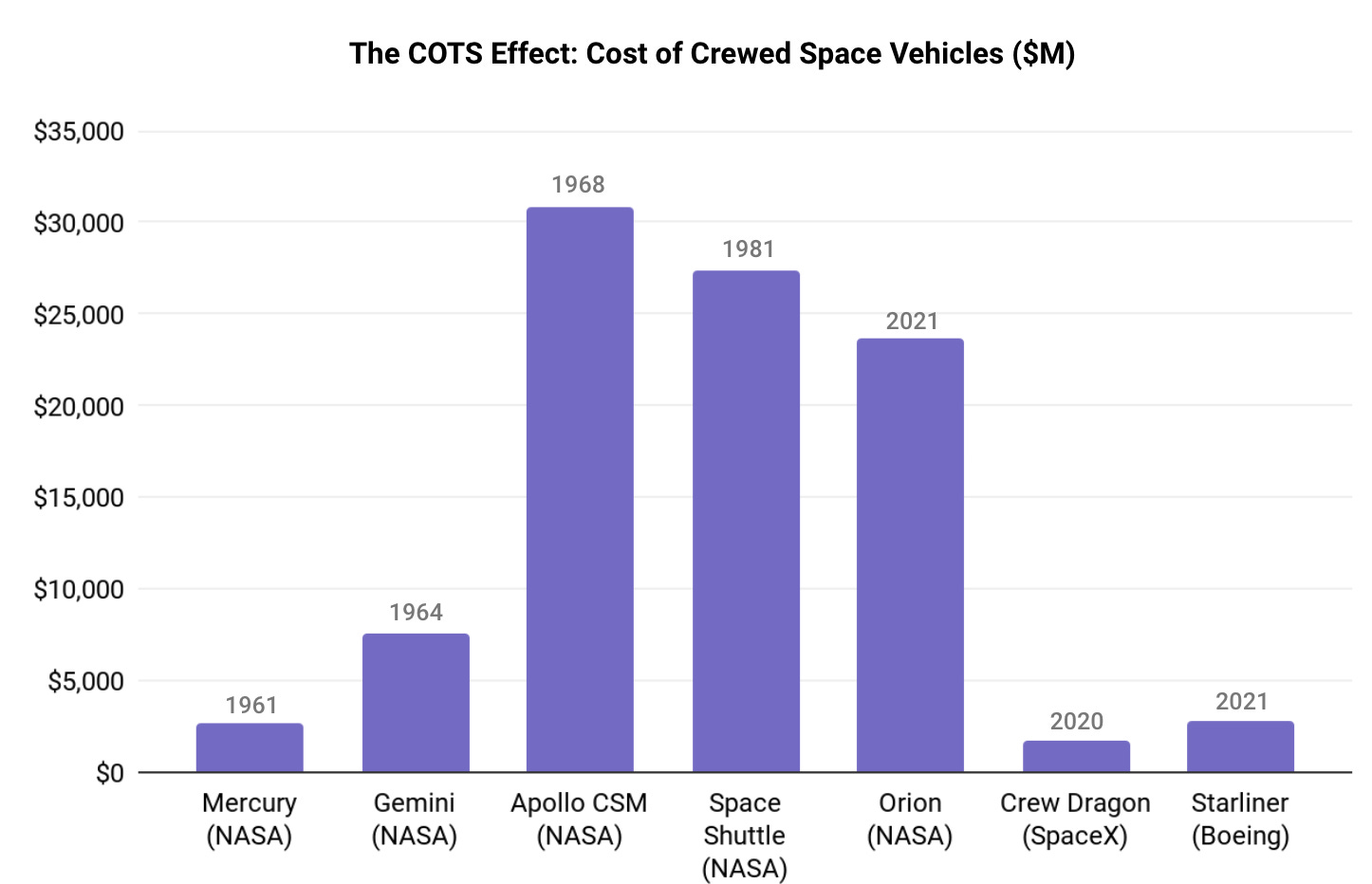

In 2005, then-NASA Administrator Mike Griffin told the private sector to buck up and challenged contractors to develop their own cargo and crew transport capabilities, configured for the specs and mission requirements of the ISS.

This would eventually lead to COTS, or Commercial Orbital Transportation Services, which may be a footnote in history but is very much a massive deal to us space nerds. The program directly paved the way for launch costs (typically measured by $/kg to orbit) to come down by an order of magnitude.

Instead of specifying the dimensions or specifications for launch vehicles and crew capsules, NASA would tell firms what it wanted and agree to pay for some of the R&D. In simpler terms, NASA went from building its own stuff to buying it as a service.

Enter SpaceX. The then-scrappy upstart got its first big break with a COTS contract in 2008 worth billions. The NASA award saved SpaceX from going under. Now, looking back with the benefit of hindsight, the deal also helped pave the way for SpaceX to become the dominant industry player that it is today.

This was a relatively new arrangement, making aerospace contractors shoulder more risk and foot the bill for development, as opposed to totally offloading it to government customers.

Fast forward to today, and the age of flippenings is upon us

Reusability would come back en vogue in 2015 when Jeff Bezos’s Blue Origin flew a rocket to space and propulsively landed it back on a launchpad in West Texas. A year later, Falcon 9 would make its first successful landing on a SpaceX droneship at sea after delivering cargo to the ISS. Over time, SpaceX has made more and more of the rocket reusable, and in South Texas, is currently working on a next-generation rocket that’s designed to be fully reusable.

SpaceX has led many of the “flippenings” of our modern space age, from pioneering reusable rockets to restoring the US’s capability to launch American astronauts to space from American soil to operating the most satellites of any entity ever in history.

Flippenings, you ask? It’s an informal term we use internally to refer to space activity that either:

A) was once monopolized by the world’s superpowers and leading space programs, where the private sector has since taken the leadership mantle,

B) improved on–or invented for the first time–by a commercial space player, or

C) is now predominantly being procured as a service from space agencies rather than developed in-house.

SpaceX isn’t the only one running up its flippening tally. For example, San Francisco-based Planet Labs, over the course of just one decade, deployed the largest Earth-observing satellite constellation ever and now images Earth daily. There’s countless other startups, legacy space players, and publicly traded companies with flippenings, both minor and mighty, on their resume.

Despite what some SpaceX maxis would have you believe, today’s space industry isn’t just SpaceX. Nor should it ever be monopolized by one player.

Why Space?

Space-for-Earth

We often see popular narratives propagated across the press and social media that say space is a pissing contest for billionaires. That is ridiculously reductive. The reality is that the vast majority of value (99+%) generated in space is not from providing joyrides to the rich. Most of the value comes from driving benefits back to Earth.

How so? Let us count but a few reasons…

Location, location, location: The US’s GPS, China’s BDS, the Eu’s Galileo, and Russia’s GLONASS provide the indispensable utility of global navigation. Looking forward, states and startups like Xona Space Systems are developing newer position, navigation, and timing (PNT) services for self-driving cars, drones, and other emerging technologies.

Bringing transparency to Earth: Since the beginning of the space age, militaries have used on-orbit reconnaissance assets to spy on enemies and frenemies alike. That’s all classified, but the advent of commercial satellite imagery has helped show the world when and where the emperor has no clothes (such as Russian war crimes in Ukraine and Chinese concentration camps in Xinjiang). This is driving the formation of a cyberpunkish sub-vertical of hiding stuff from satellites, but that’s a topic for another day.

Fighting climate change: What gets measured gets managed. To understand our changing Earth, we use remote-sensing satellites to observe it through multiple modalities. Satellites help us track greenhouse gas emissions, deforestation, sea level rise, melting polar ice caps, and so much more. And finally, here’s your fun fact of the day: you can see cow farts from space.

Earth observation (EO) for everything else: Beyond cow farts, you can use satellites for so much: detecting tax evasion, tracking illegal deforestation, inventorying earthquake and landslide damage, monitoring volcanoes, planning hyper-specific ski trips, and predicting retail earnings by counting cars in parking lots.

Spillovers: NASA regularly catalogs technology spinoffs developed for space that have now been commercialized. Examples include air filtration, autonomous navigation, EVs, flying cars, and spacesuit designs repurposed for race car drivers. Just like the loads of Formula 1 technology that make its way into passenger car production, space technology often becomes commercialized and cost-effective here on Earth.

Here’s NASA’s patent portfolio for any of you would-be founders who want to take a crack at licensing IP and trying to build something based off of these technologies.

Increased Global Instability

As hinted at above, space is the canonical example of a dual-use domain. A dual-use technology is one with both civilian and military applications (another good example here is nuclear).

Space militarization has become one of the primary technological fronts for great power competition, set against the backdrop of the Russia/Ukraine conflict and rising competition between the US and China.

In our view, for better or worse, the global race to gain an upper hand in space is only accelerating. Starting with Russia, as Quilty Analytics CEO Chris Quilty said back in March: “Space, long considered a sanctuary for international relations, turned into a source of leverage for Russia against the US and Europe.”

Launch services: Western payloads can’t fly on Soyuz, removing a ton of heavy-lift launch capacity globally. The first salvo: Russia refused to launch satellites for space-based internet provider OneWeb and held the company’s satellites hostage at its spaceport. Russia demanded that the UK government sell its stake in OneWeb. The UK refused those terms and OneWeb is now working with SpaceX (which could be considered a constellation competitor).

Spaceports: Roscosmos has suspended scientific cooperation with European partners, indefinitely delaying the launch of a European-led Mars mission. Russia has also withdrawn its staff from Europe’s spaceport and suspended all launches from the location.

Engine sales: The Pentagon was already weaning American contractors off of rockets that relied on Russian-origin technology (specifically engines). The war in Ukraine, sanctions, and geopolitical tensions hastened that phaseout, as Russia discontinued engine sales to the US (since the ‘90s, Russia has delivered 122 RD-180 engines to the US).

Cybersecurity: At the outset of the war, thousands of modems and routers made by satellite operator ViaSat were bricked by a malware hacking campaign that the US intelligence community later attributed to Moscow. The cyberattack led to partial network outages across Europe, knocking thousands of wind turbines in Germany offline. Separately, Elon Musk has said that SpaceX’s Starlink internet service, which has been indispensable for Ukrainians, has faced intense jamming in the country. Hmm…who it could be coming from?

Space stations: It seems as if the ISS could lose its safe-haven status, with geopolitical tensions between its two primary partner nations finally reaching the station. Newly installed Roscosmos chief Yuri Borisov recently announced Moscow’s intention to walk away from the ISS partnership in 2024 and commence construction on its own space station. It remains to be seen whether Russia will make good on these claims.

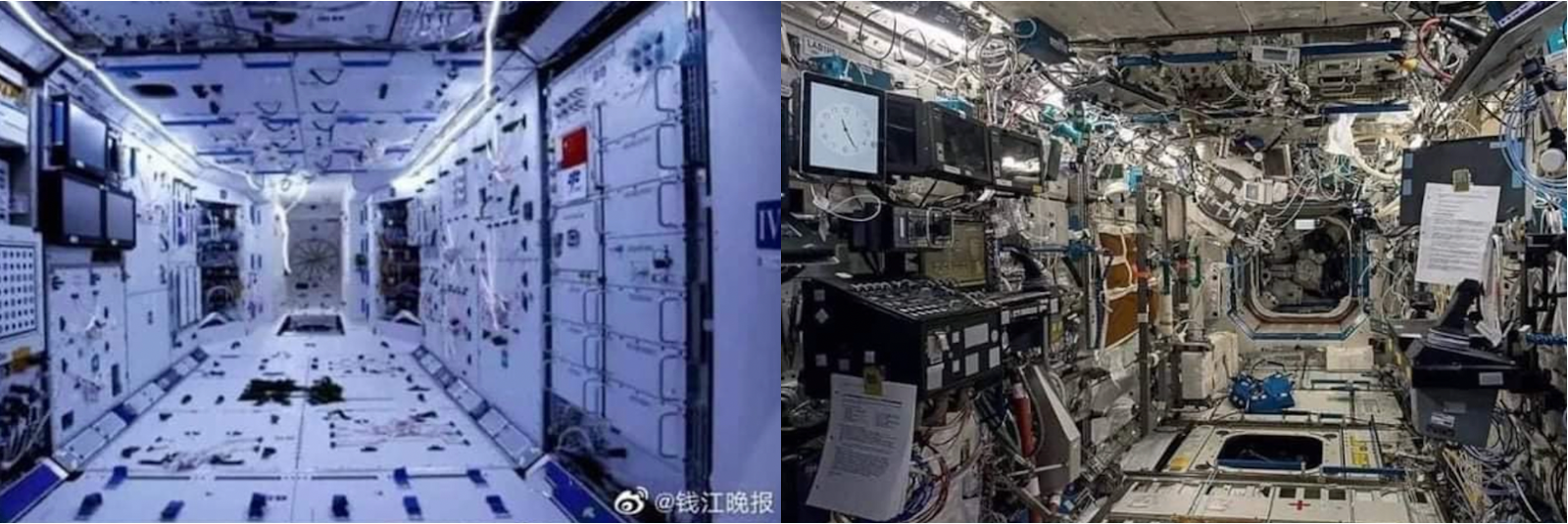

All the while, Beijing builds: The US iced China out of the ISS, leading the country to build its own space stations. China is actively building Tiangong, or “Heavenly Palace,” with the latest module going up just a couple weeks ago. Construction is slated to be completed later in 2022.

Beyond orbital outposts, China has a robust and rapidly advancing space program. China conducted more orbital launches than the US in Q3 last year, covertly demonstrated state-of-the-art hypersonic glide vehicle capabilities, and shows off new on-orbit capabilities seemingly monthly. Like Washington, Beijing views space as a warfighting domain and in the event of a conflict, would likely take measures to “blind” US birds through electronic warfare or anti-satellite kinetic (aka kaboom) capabilities.

We’d be remiss not to mention that it takes two to tango. The Pentagon is highly active in space. The US’s Space Force is a real thing. Finally, the DoD’s new Space Development Agency will be putting plenty of newfangled hardware on orbit over the next few years, from a next-gen missile-warning orbital shell of satellites to lightning-fast, laser-link battlefield combat communication constellations.

With US military planners citing off-world threats facing the US (real or perceived), it’s almost a given that the US response will involve stepped-up militarization of the space domain.

Space competition extends beyond militarization. China aims to compete with the US and West on every axis of space, from lunar settlement to Mars probes to interstellar exploration.

Seeing the primacy of space as a battleground in any future conflict, the US is pushing to maintain space leadership on all fronts, with strong bipartisan backing:

The Biden administration’s request for the NASA budget in 2023 is $26 billion, which also includes the largest request for science in the space agency’s history. Biden also wants to increase the number of personnel in the U.S. Space Force by 2,000 members to bolster US military capabilities in space.

The Artemis program, which is aiming to land U.S. astronauts on the Moon’s surface by 2025, will be the first U.S.-crewed Moon mission since Apollo 17 in 1972. The program has two key components: the Artemis Base Camp on the lunar surface; and the Gateway in lunar orbit. Each will serve as a key research base for lunar science, and a launchpad for further deep space exploration.

Federal US defense spend is up and to the right. The FY2021 DoD Budget Request projected 1.5% annual growth over the next five years. If it does not increase its budget, then by 2032 US defense spending will have been overtaken by the combined budgets of Russia and China - a scenario so politically toxic, there will be bipartisan support to overcompensate against even the risk of that happening. Many DoD officials have publicly stated that space has been identified as their most important foundational area. Globally, 2021 was a record year for government space investment, clocking in at $92B+. The share going to defense was a record 20%.

Space Race 2.0

A decade ago, the US government funded 70 percent of global space spending. Today, its share is less than 50 percent. Over 80 countries now have active space programs aiming to generate economic returns. Countries with no prior space programs are exploring opportunities in the commercialization of space. The UAE flew its first astronaut on a Russian spacecraft in 2019 and positioned a scientific satellite into Mars’ orbit earlier this year. The UAE is also working on sending an unmanned spacecraft to the Moon in 2024.

China is a true outlier in how quickly it has been able to develop space technology. Beijing launched its first astronaut into space in 2003. Since then, China became the first country to land a probe on the Moon’s farside, the second to land a rover on Mars, and the third to successfully bring lunar soil samples back to Earth. The country has also built the world’s largest telescope, deployed Beidou (a next-gen competitor to GPS), and signed an agreement with Russia to jointly build a Moon research base. China trails only the US for the number of government satellites in space (363).

What’s next? China aims to launch two megaconstellations of ~13,000 satellites, send crewed probes to the Moon’s farside for exploration and asteroid mining, and put boots on Mars by 2033. The Chinese government also estimates a $10 trillion-per-year return on investment from its planned activities in the Earth-Moon (aka “cislunar”) economic zone by 2050.

This year, China will complete construction of Tiangong, its first-ever free flying space station. Tiangong’s Tianhe-1 core module is the world’s first spacecraft powered by four ion drives, a type of electric propulsion that could dramatically reduce fuel consumption and travel time to Mars.

…all while the ISS program is suffering regular operational issues:

Recent ISS mishaps include persistent air leaks and the breakdown of a critical life-support system

Last year, the ISS flipped on its back after thrusters on a Russian module started firing after docking to the station

NASA has halted all of its spacewalks at the ISS due to safety concerns of spacesuits after water leaked into one astronaut's helmet while working outside the station. Thankfully, there may be a private solution here.

U.S. policymakers and generals are closely watching China, which has included the Moon in its Belt and Road Initiative.

Space Economy Market Size Projections

There is no consensus on how large the space economy is today. We looked at a number of estimates taken from Euroconsult, BryceTech, Morgan Stanley, and the Space Foundation to get to a ~$400B market (average) today. The good news is that each of these organizations were within about 10% of one another. However, future projections vary considerably. Estimates for the market size by the end of the decade range from UBS’ estimate of $926B to Goldman Sachs with a prediction as high as “multi-trillions” of dollars (which we assume to be $3T). US policy makers have frequently referred to the “trillion dollar space economy” in presentations designed to highlight government initiatives and encourage private sector investment in space. For those wondering what segments of the market are driving most of the growth…the general consensus tends to be satellite communications and ground equipment.

USE OF PROCEEDS

Against these historical and geopolitical backdrops, we’ll now consider how space startups get funded and what they spend money on.

Given the heavy national security bent of many space firms, the intellectual property-sensitive nature of their tech portfolios, and the fact that most business dealings are covered by NDAs, founders aren’t keen on opening the books willy-nilly. Therefore, it’d be a fool’s errand for us to try and tell you definitively what the typical cost structure of an early-stage space startup looks like.

But! We’ve spoken with 100+ space founders in the last nine months, so we’ve got more than enough anecdata to give you a directional sense of the nominal early-stage space trajectory. They tend to focus on:

Recruiting: Assembling the right founding and early technical teams is everything. When recruiting, you’re looking for the right technical chops and past hands-on experience. More often than not, that involves past gigs at rocket finishing schools (SpaceX, Blue Origin, etc.) or established contractors (Lockheed, Boeing, Northrop Gruman, etc). In these roles, hands-on sweat equity and ownership of key rocket/satellite programs come at a significant premium over your education credentials or ability to answer weird interview questions.

The MVP: The minimum viable product inherently will look a lot different than that of your typical startup. You can’t just ship something barebones and commit to quashing the bugs at a later date. The MVP = a hardware prototype. Skipping forward a few assembly, integrating, and manufacturing steps, you’ll then need to integrate and validate the MVP on-orbit. That’s already plenty expensive–and if against all odds you succeed, be prepared to spend more $$$. Deploying a constellation of production sats can be an order of magnitude (or magnitudes) more costly.

Identifying a market: The road to orbit is paved with bold product ideas in search of a market. Given the capex-intensive nature of space, successful startups have typically known from the beginning who they would sell to, where they would buy vs. build, and how, when, and where they would go to market. The art of the pivot is a little bit less graceful when you’ve already opted for a specific manufacturing technique or spent millions building one system and suddenly want to switch to another (though that could be the survivorship bias speaking).

By necessity, space companies’ founding and early teams are disproportionately (or even exclusively) technical. SG&A functions are often a can kicked down the road, and something to be backfilled once the company has shown early signs of traction. The engineer to entrepreneur pipeline is only widening, in our view.

Caveat to all the above: The description mostly speaks to hardware companies (or companies that have successfully layered software on top of their hardware). Yes, there are platforms, marketplaces, and pure software startups serving the space industry. But these are the exceptions that prove the rule. Generally speaking, space companies are enormously capital-intensive.

Moving on to more established companies, let’s quickly consider three case studies that give a glimpse of how funds are allocated across the space spectrum:

Boeing: The US industrial giant’s defense, space, and security (BDS) unit made $6.2B in the Q2 2022, good for an operating margin of 1.1% (vs. $6.9 billion, nice, and 13.9% YoY). BDS took a $93M charge for costs associated with its Starliner, its NASA-contracted crew transport system for the ISS. Starliner has been beset by software issues and delays, and as a result, affected a ~$98 billion company’s margins and earnings in a meaningful way. FWIW, Boeing did just recently successfully complete its second orbital flight test to the ISS (without a crew), so it’s looking like the US will get a new domestic taxi for the space station soon.

Starlink: SpaceX is still private and very much tight-lipped, so we can’t speak to the true economics of its Starlink unit. Last October, though, we got our hands on a Morgan Stanley note on SpaceX. The analysts base-case estimate is that Starlink’s buildout will cost ~$240 billion, burn $33 billion from 2020–2030, and become cash-flow positive in 2031. User terminals (aka the satellite dishes on homes, boats, RVs, airliners, etc) would be the most expensive line item, responsible for ~83% of all Starlink buildout costs.

DILUTION

One tool at a space startup’s disposal that is likely not available to your direct-to-consumer CPG company or run-of-the-mill B2B SaaS startup is non-dilutive financing.

Government grants offer A&D companies the opportunity to pad their war chests with non-dilutive financing, and forgo incremental rounds of equity financing. In the US, the federal government provides R&D funding to companies that meet certain criteria or hit performance milestones. A few examples:

NASA, the National Science Foundation, and other agencies provide SBIR (Small Business Innovation Research) grants for startups/SMBs with fewer than 500 employees. Startups also have the option to compete for STTR (Small Business Technology Transfer) awards.

The US Air Force provides grants through its AFWERX Challenge, which calls on industry to create solutions to specific challenges. This funding is awarded competitively.

NASA has a variety of opportunities, from grants to flight opportunities to “Tipping Point” agreements to licensing patented technologies with zero in upfront costs.

Due to the space industry’s highly skilled and productive workforce, state and local governments will also provide low-interest loans, tax breaks, and incentives to spin up or scale operations in their backyard.

Contract awards from the government are often misconstrued as subsidies. And while contracts therefore are a better fit for a conversation about business, it’s important to note that government-awarded contracts can serve as important bridge financing to help companies bring a new product to market, fund development cycles, or generally achieve more sustainable operations.

SpaceX, for example, iterated toward reusability on its workhorse rocket after the Falcon 9 was awarded a contract to supply cargo to the ISS–and before it had actually landed the rocket back on Earth in one piece.

In more recent memory, there’s an entire generation of NASA-funded, commercially developed lunar rovers that likely wouldn’t exist were it not for the NASA program providing the funding.

BUSINESS (MODELS)

Dropping costs are the common theme in our current space era. The use cases gaining traction today and tickling space nerds’ imaginations were often actually conceived of decades ago, but the cost structures never made sense and the business case couldn’t close.

The space industry has made significant progress down the cost curve, with innovations in manufacturing, propulsion, composite materials, and reusability, making it cheaper and easier than ever to reach space or operate in LEO. As new private sector startups enter the industry, the pace of innovation continues to accelerate rapidly. We’re seeing the proliferation of new business models, such as space-as-a-service, all driven by falling launch costs, better manufacturing, vertical integration, and supply chain efficiencies.

Arguably, the most important shift in space operating models has been that of the change from centralized to distributed systems, most clearly exemplified by megaconstellations.

Companies now opt for operating thousands of smallsats, versus single large and expensive individual assets with 15-year lifespans. Even large-scale infrastructure such as the ISS will be replaced by multiple private providers. More progress on mass production, additive manufacturing (3D printing), and fully reusable super-heavy (think SpaceX’s Starship) launchers could further cut costs and enable new on-orbit business models. For now, we’ll focus on a few of the models that are have captured significant investor interest and/or public mindshare:

Launch

Launch has by far seen the most disruption in the past decade compared to all other areas of the space industry. This is primarily attributed to SpaceX, which brought reusable rockets into the mainstream via the Falcon 9 and Falcon Heavy. Previously, satellite operators were limited to taking rides into orbit on expendable launch vehicles, such as the Ariane V and the Atlas V, which cost at least $150M per launch.

We see many future drivers of lower launch prices, including parts-related cost reductions, efficient refurbishments, economies of scale in production, and most importantly competition. There are many well-funded startups on their way to commercializing and scaling orbital launch capabilities. SpaceX’s Starship launch vehicle will be the next key catalyst in bringing down launch costs by another order of magnitude–by Elon Musk’s estimates, down to as little as $100 per kg.

Satellite Communications

The satellite industry is going through a renaissance period driven by lower launch costs and huge increases in performance-to-cost ratios associated with Moore’s Law. In other words, as electronics have become smaller and more capable, more powerful satellites can be packed in the same amount of payload capacity. It’s partly the reason why satellite-based data represents nearly 50% of the space economy and is growing faster than the broader industry.

The paradigm shift in cost structure has led to a massive influx of companies launching satellites into LEO. With the cost to launch and build satellites orders of magnitude lower than they ever were before, there is not only more room now to take risk, but more time allowed for demand to grow into supply. Ultimately, changes in cost structure have led to a much clearer path to long-term, widespread profitability.

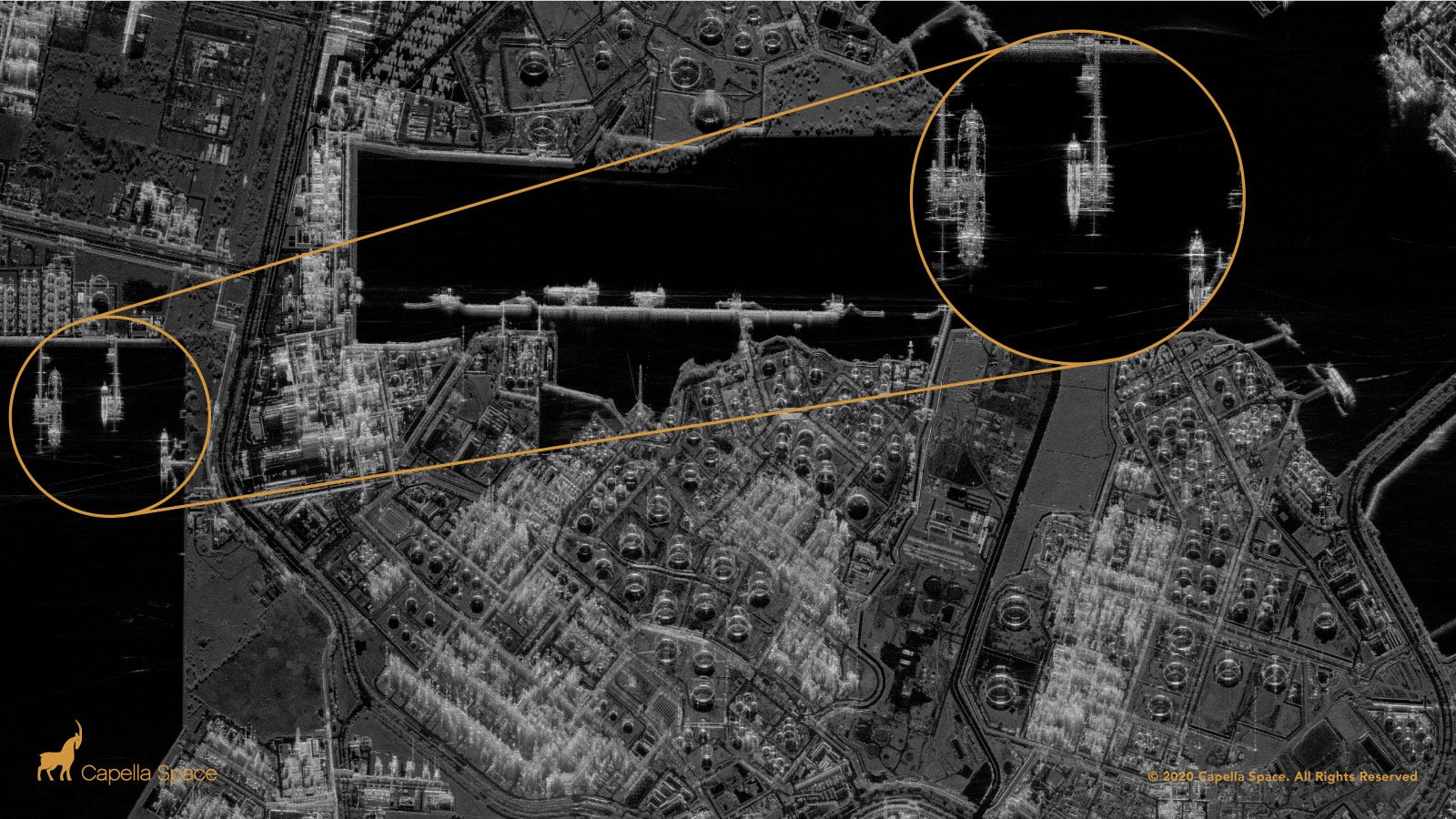

Earth Observation: Satellite Imagery

Earth observation (EO) is an umbrella term that refers to tools or technologies that measure the characteristics of air, water, and land. The data is collected from satellites, aircraft, and drones, and can provide a unique and timely source of information about Earth’s physical, chemical and biological systems. Satellite imagery is arguably the best way to understand these systems at a global scale repetitively and continuously. Not surprisingly, the US government is the largest single consumer on the planet for EO data, but that’s starting to change as the cost to acquire imagery and analytics starts to fall to price points accessible for commercial use cases. This includes everything from property insurance monitoring to mapping sites for energy infrastructure projects.

Similar to satellite communications, the “why now?” for satellite imagery is again a result of dramatic decrease in launch costs and cost performance improvements from better technology. To truly understand the scale of this, look no further than the Landsat 8, a medium-resolution EO satellite that was a collaboration between NASA and the United States Geological Survey back in 2013. The cost? 1 billion in today’s dollars. By comparison, Planet Lab’s medium-resolution SuperDove satellite costs <$300k. Now, before EO maxis start pointing out the differences in insert technical term ratio, the more important point here is that a cost-performance improvement of over 3,000x has been made for a pretty good substitute, which has significant implications for commercial use cases.

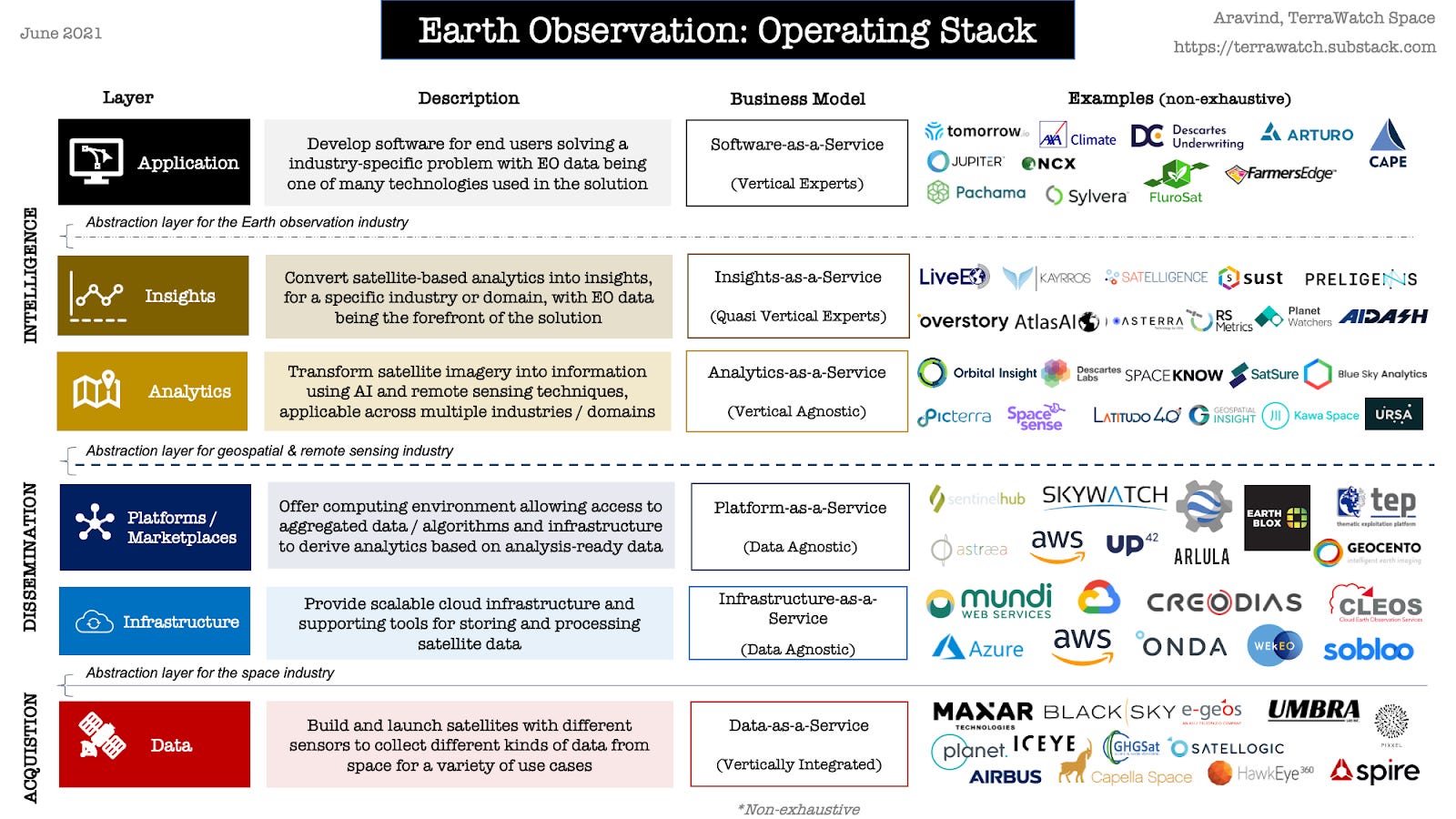

There are a few different business models when it comes to EO and satellite imagery. They are best summarized in diagram form by Aravind of TerraWatch Space, a monthly newsletter frequently touching on the evolution of the EO industry. Here’s a handy market map, courtesy of Aravind:

The industry is beginning to evolve from catering only to the defense & intelligence community to serving broader commercial use cases. As a result, more layers are evolving within the operating stack of EO:

Acquisition: This is the part of the industry that is collecting the actual data. This is the more traditional segment tied to the space industry, i.e., designing the payload (with the help of remote sensing experts) and building and launching the satellite constellations. Companies like Maxar, Blacksky, and Planet acquire the data and sell it to customers.

Dissemination: After acquisition, there has to be a way to store and process data (infrastructure: companies that charge a subscription fee service) and a way to aggregate data (platforms/marketplaces that charge on a per-use basis).

Intelligence: The final–and arguably the most important–layer is Intelligence. This is where analytics and insights are derived from raw imagery data or software developed for end users solving industry-specific problems. This is the most scalable layer of the EO operating stack and naturally lends itself to more of a SaaS-based subscription model.

Kevin Weil, president of product and business at Planet, is leading the company’s charge “up the stack.” In Ep. #0008 of our Pathfinder podcast, Weil, who formerly led product at Twitter and Instagram, described the journey up the stack into vertical-specific machine learning models and analytics products.

Space Tourism

There are two main categories of space tourism: sub-orbital and orbital. Sub-orbital flight is when a spacecraft travels above the Karman line (the 100 km altitude delineator between Earth and space) but does not reach orbital velocity. This is the type of tourism that captures most of the headlines. Blue Origin’s New Shepard and Virgin Galactic’s VSS Unity both travel up to the Karman line but never make it to orbit. Most consumers won’t really care. The reality is that to the untrained eye, reaching the Karman line effectively looks and feels like you’re in space. Blue Origin and Virgin Galactic both generate revenue by selling tickets priced between $450,000 and many millions of dollars for a few minutes in microgravity.

Orbital tourism is…you guessed it…when you travel to space and reach orbital velocity (~17,500 mph+) or the speed that an object must maintain to remain in orbit around a planet (vs sub-orbital travel at ~3,700 mph). The incredibly high speed makes orbital spaceflight much more complex technically than sub-orbital flight and therefore more expensive. Axiom Space, a company building the successor to the ISS, launched the first fully-private mission to the ISS earlier this year. The company sent four private astronauts including three paying customers to spend ten days in orbit on the ISS. The price tag? $55 million a seat.

The economics of a single flight–especially at $450,000+ for sub-orbital tourism–can be very lucrative, but the question remains as to whether companies can execute technically and scale quickly enough to cover the upfront capex of vehicle development before running out of money. Virgin Galactic is a great example of a company with a substantial backlog of customers and a product that has successfully worked, but continuous maintenance-related delays and labor constraints have put substantial stress on the company’s financial position. There will be a model here that works; the question is who will pull it off first.

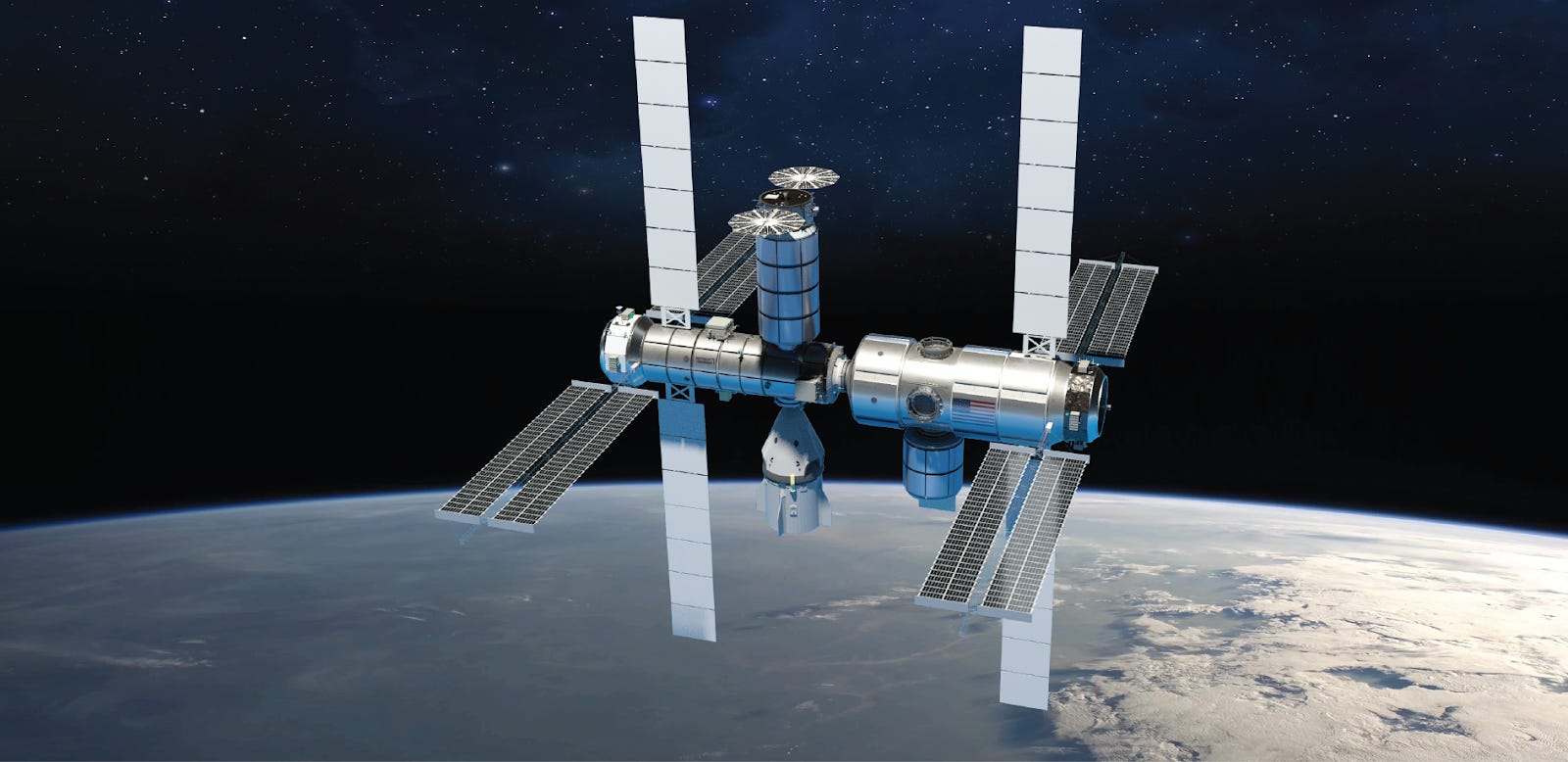

Space Stations

The NASA-led International Space Station (ISS) has been orbiting Earth since 1999 and has been continuously inhabited by astronauts since 2000. However, as the treaty between the governing nations comes to an end, and as the ISS reaches the end of its useful life, the platform will be decommissioned, leaving a significant gap in the western world's ability to operate in space.

Despite the retirement of the ISS, the US is committed to sending national astronauts to low Earth orbit (LEO), codified by a 2020 congressional directive to sustain human presence in LEO. This leaves a vast majority of the $3.8B United States Orbital Segment (USOS) budget over the course of the next decade up for grabs as the ISS approaches retirement. Also:

In 2021 alone, the US ISS budget, including launch costs, was $2.9B.

NASA forecasts a requirement of at least two astronauts to access a LEO platform at all times and is budgeting over $9B through 2025 to continue transporting crewed missions to the ISS.

The five space agencies that cooperate on the ISS increasingly rely on a platform that will be retired in just a few years time. These agencies spend $4.5B/year at the station, which is about half on productive missions and half on operations and maintenance.

So what are we trying to say here? There is a significant opportunity for a commercial provider to build a replacement and capture the revenue that will inevitably transition to the next viable platform. A number of companies have thrown their hat into the ring so far:

Axiom Space (mentioned earlier) has an advantage in that it was selected by NASA to receive the only third-party ISS port connection in 2024. In other words, Axiom modules can attach to the ISS and defer the capex needed for energy requirements by utilizing the ISS’ power supply. Axiom CEO Mike Suffrendini was recently on our Pathfinder podcast, where he laid out the company’s roadmap to reach (and fund) a free-flying space station by the end of the decade.

Blue Origin and Sierra Space plan to deliver a free-flying space station called Orbital Reef in this decade. Orbital Reef has an advantage in that it will be using Sierra Space’s upcoming Dreamchaser reusable spacecraft to ferry crew back and forth. On Pathfinder, Sierra CEO Tom Vice described the company’s transportation and space station flywheels as a platform play.

Nanoracks, in collaboration with Voyager Space and Lockheed Martin (NYSE: LMT), has formed a team to develop a free-flying commercial space station called Starlab. The basic elements of the Starlab space station include a large inflatable habitat, designed and built by Lockheed Martin, a metallic docking node, a power and propulsion element, a large robotic arm for servicing cargo and payloads, and the George Washington Carver (GWC) Science Park.

Northrop Grumman’s space station concept is centered on a modular design that borrows technology from the company’s Cygnus cargo resupply vehicle, the satellite servicing Mission Extension and Mission Robotics Vehicles (MEV and MRV), and the in-production Habitation and Logistics Outpost (HALO). This approach allows the company to minimize initial costs and allow later capabilities to be incorporated based on market needs.

Why do space station economics finally work? The ISS is a great representation of when government-backed infrastructure programs can become cost-inefficient. The headline price of the ISS was $150B ($50B of that is ascribed to the shuttle program) and it was developed in partnership with Russia, ESA, JAXA, and a few other international partners. A few reasons for the out-of-control ISS expense structure:

NASA’s development model involved large contractors maximizing for jobs in key congressional districts which dramatically increased cost inefficiencies (i.e., cost-plus).

Collaborating with international partners led to enormous cost complexity.

Government space programs are not incentivized to save money since budgets need to be spent in the year allocated regardless of inefficiencies related to doing so.

Because these new commercial players are not tied to political agendas and geopolitical dynamics, current private space station build costs are estimated to be a fraction of the original ISS. In some cases, the cost is predicted to be in the single digit percentages. The order of magnitude reduction in cost is turning space stations into viable real estate businesses in low Earth orbit.

Space Manufacturing

Another product of lower launch costs is the ability to start utilizing the microgravity of space to pursue various high-value manufacturing. Microgravity is conducive for manufacturing certain materials that cannot be disturbed in production. According to Factories in Space, there are currently over 50 companies that are developing manufacturing processes that could be carried out in space. The companies are all in different stages of development but cover a wide variety of applications, including 3D printing, food production, organic tissue growth, pharmaceuticals and raw material processing.

For space manufacturing to be a profitable business, you need to start with a high-value product where the efficiencies derived from producing the product in space creates enough added utility that customers are willing to pay a premium. Many industry experts (and VCs) believe that space manufacturing can now be done profitably because it's finally cheap enough to send raw materials up to space and finished products back to Earth.

What’d we miss?

A bunch. To break the fourth wall, because we’re writing this for a broader audience rather than the space in-group, we decided to curate some of the “sexier” space verticals. But there are many more segments that we don’t have the space to expand on, from ground infrastructure to networking technology to the thousands and thousands of fragmented parts suppliers and mom and pop machining shops around the US.

What are we watching?

Two sectors poised for big near-term breakouts, in our view, are 1) laser links and 2) edge computing.

Laser inter-satellite links are literally space lasers that speed up communications between constellations. They’re standard on the newer generation of Starlink satellites, the Pentagon is procuring them for its future constellations, and the list goes on. From Sony (yes, Sony) to a range of startups, new players are flooding into the space.

Edge computing is a rapidly growing priority for on-orbit assets. By processing data locally in LEO, satellite operators can cut out the middleman (ground stations and data centers) and deliver actionable information or intelligence with significantly less latency and lower bandwidth bills.

On a longer timeframe, we’re excited (but not necessarily bullish) on the more sci-fi-esque, batshit-crazy ideas that are still suuuper far out on the risk curve and/or still exclusively nation-state capabilities: nuclear propulsion, space-based solar power, crewed and uncrewed Mars missions, and asteroid mining,

PRINCIPAL STOCKHOLDERS

Historically, the space industry faced many structural limitations when it came to traditional venture capital and private equity. Many companies were simply not venture-scalable:

The long-cycle nature of aerospace businesses didn’t fit with the traditional 10-year fund life.

High barriers to entry does not lend itself to typical risk/return models.

The military was integral to market development, which imposed high barriers to entry and limited startup formation.

As costs continue to fall, technology opens up new applications and market opportunities, and commercial companies are having significant success penetrating markets that historically were difficult or near impossible to gain traction in. The investment implications for a more accessible, less expensive reach into space are significant and why you’ve seen a considerable expansion in the space investment community.

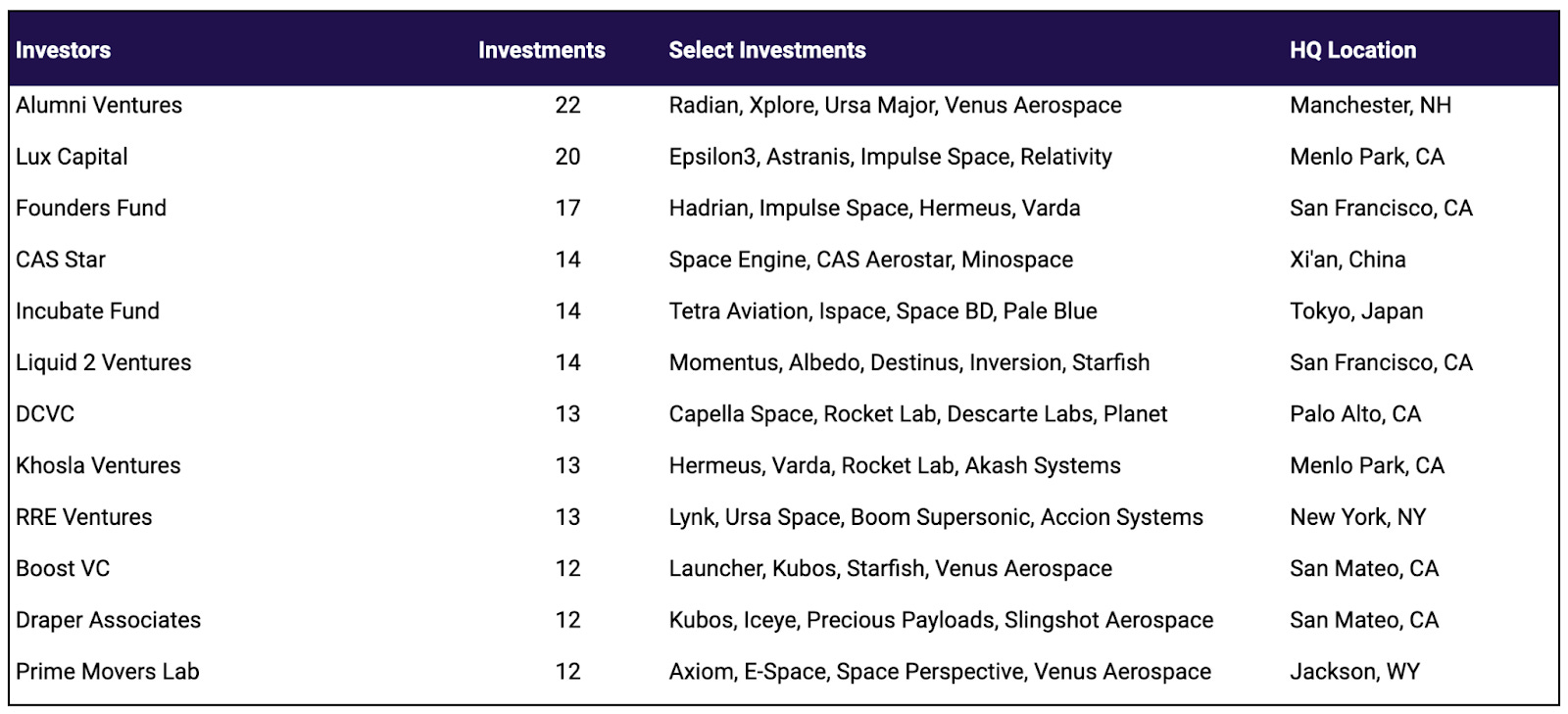

Key Venture Investors in Space (By Deal Count)

Space-Focused Investors

Among space-focused funds, NY-based Space Capital takes the crown as most active, with London-based Seraphim Capital not far behind. In the angel investor community, Dylan Taylor (CEO of Voyager), Marc Bell (CEO of Terran Orbital) and Sand Hill Angels are among the most active.

Technology Investors (with Space Thesis)

Within the broader tech investor community, Alumni Ventures, Lux Capital, and Founders Fund lead the way by deal count. Not on the list, but certainly deserving mentions:

Bessemer Venture Partners were early investors in Rocket Lab and Spire Global.

NFX has launched a space vertical with two announced investments so far: Stoke Space and Starfish.

Future Ventures was an early investor in SpaceX and Planet. Steve Jurvetson was an early adopter of the commercial space thesis, but for the time being has publicly expressed less of a desire to expand the portfolio.

Dylan Taylor’s family office, Morgan Brook Capital, has been actively investing in space for a number of years in names like Space Forge, Orbit Fab, Axiom Space, Leo Labs, Kepler Communication, and others.

Private Equity’s Role in Space

Private equity has historically been underinvested in space. We attribute that to an incompatibility issue between PE models and the nature of aerospace contracts, specifically as it relates to cash flow. One key feature in space is long-term contracts between suppliers and OEMs. These contracts supply equipment for R&D and capex-heavy programs that have over twenty-year life cycles. Yes, these contracts may offer steady and consistent cash flows, but earnings are not guaranteed…and private equity is an EBITDA multiple world.

A recent KPMG analysis highlighted that now is one of the best times for private equity to invest in aerospace & defense (A&D). Their reasons? Increased geopolitical instability, the expansion of defense capabilities away from traditional hardware toward new technologies, and increased onshoring of manufacturing and supply capability. The report goes on to highlight the opportunity in domestic supply chain consolidation. The major aerospace players have recently looked to protect their balance sheets and pause new orders, which in turn has created financial stress for the small and family-owned tiers of the aerospace supply chain. For private equity funds, this presents an opportunity to build scale from a fragmented and depressed market.

Retail & Space SPACs

The space industry was a beneficiary of the SPAC boom and correspondingly is a casualty of the SPAC bust. Nine pure play space companies went public via reverse merger in 2021. Not all space SPACs are created equal. Planet Labs and Rocket Lab made $113M and $62M last year, for example, while other publicly traded space companies made very close to $0–in other words, pre-revenue and not even remotely close to a path to profitability.

SPACs have provided retail investors (and, for a bit, the meme day traders) an opportunity to back earlier-stage companies closer to the ground floor. The financial vehicle also gave VCs the chance to reap liquidity from their space portcos, which otherwise wouldn’t have existed. While space SPACs may have been a good thing for the early investors, they’ve been punishing mom and pop investors.

YTD, the pure play space SPACs are down 36%, according to our Payload Space SPAC Index. It’s not unthinkable that we’ll begin to see companies delist, file for Chapter 11, or become acquisition targets. Some say SPACs will ultimately have a chilling effect on future industry financing, given the companies’ outlandish projections, burn rates, and unprofitable/unrealized business models.

UNDERWRITING

So, how do you close the business case? You’ve likely heard the term “hardware is hard,” which sums up the challenges of building a successful business in atoms.

Well, now acquaint yourself with “space is hard,” a commonly uttered line within the space industry. Matt Desch, the CEO of Iridium, a $5.7B publicly traded satellite operator, summed it up best to us: “Space is very hard. It’s literally very unforgiving. It always takes longer than you think, and costs more, and will disappoint you before you ever achieve success.”

Admitting that space is really hard is the first fact you must confront if you intend to invest in this industry. If you still don’t believe us, look no further than the bifurcation of performance between traditional A&D players and space SPACs in the public markets. Despite the broader market’s abysmal performance this year, traditional A&D companies are in the green. But the space SPACs are underperforming by 37%.

What's going on, and why is the underperformance so stark?

"SPAC" baggage: The word SPAC, plain and simple, has a negative connotation that not even great businesses can avoid. The De-SPAC ETF, an index that tracks the broader universe of companies that have completed SPAC mergers, is down 60% YTD.

Space is new: Pure play space companies are a new area of investing for the public markets. Most investment banks barely have research coverage for the industry (but Payload covers all of them quarterly 😎). Given the lack of analyst coverage, it's hard to see how broader markets would understand how to trade new space companies. Case in point: We’ve seen smallcap space companies trade like GameStop or AMC upon news of a launch services deal with SpaceX (which generally reflects an expense, not revenue).

Wrong time, wrong place: R&D isn't meant for public markets: They’re not where you build your first product, especially when your financial projections were based on technical milestones or TAMs that were ambitious to begin with. Fee-driven bankers led companies astray, building comp tables and valuation models that were inherently flawed.

Despite the souring market, we believe–and this is most certainly not investment advice–that significant alpha exists within both public and private markets. Again, not investment advice and DYOR. Many space SPACs are part of markets with real demand, robust pipelines, and growing backlogs. However, you must assume that these companies will have a very difficult time accessing the public markets again. For the companies that don't have a consistent working product yet, pay attention to cash balances and burn rate. You'll have to estimate whether they can get to a viable product before running out of runway.

For companies with a working product, bear in mind that there are interesting opportunities out there: SpaceX recently closed a fundraising round at a $125B valuation. Should Rocket Lab (RKLB), a vertically integrated launch service provider with a demonstrated track record of execution, really be trading at 2% of SpaceX's valuation?

And yes, SpaceX has Starlink, Starship, hypersonic point-to-point travel, interplanetary colonization, and all the other projects Elon & co. are hell-bent on tackling, but the reality is that most of those business models are currently unproven. This makes it fairly clear that there is a disconnect that can be exploited.

Anton Brevde, partner at Prime Movers Lab, recently wrote a great piece titled "2023 Will Be the Year That the New Space Bubble Pops," highlighting how "the glut of inbound capital has exacerbated the core systemic risk within New Space — the overfunding of startups with highly speculative business models at unsustainable valuations." He goes on to highlight how New Space startups have been selling to each other via the use of bookings (future revenue that is yet to be recognized) as a milestone to raise additional funds. The problem now is that capital markets have slowed down significantly.

Brevde brings up an important point, in that the last few years we raised record amounts of capital in space, which led to speculation on products that required one or two additional layers of the space economy to develop in order to achieve business model viability. Is it a satellite imaging business that can launch and immediately generate revenue from customers? Or is it a business developing gas stations in space, requiring a robust economy of satellites that have traveled long enough to need more fuel? The companies that can generate real paying customers today are the ones that have the best chance of navigating the fundraising vacuum we're in. If you fall into the 2nd or 3rd order business model (in other words, for your business model to work, you need the proliferation of another layer of the space economy that does not exist today) and you don't have 12-18 months of runway, government contracts to bridge the gap to commercial orders will be critical.

Companies with flight heritage, proven spacecraft, clear scalability, and active operations in markets where there is real present demand—not future 2025E customers—are worthy of a second look. There are certainly diamonds in the rough.

LEGAL MATTERS

Builders are ‘gonna build. But as much as founders may want to stay heads-down on hardcore engineering and keep lawyers at arm’s length, that really isn’t an option in space. Here’s an assorted sampling of the smorgasbord of laws, rules, and regs that space players must be mindful of.

ITAR: Short for the International Traffic in Arms Regulations, this US regulatory regime covers and restricts the export of US-origin, dual-use technologies. On its face, this makes a lot of sense. The same technology powering a launch vehicle or hypersonic testbed, if it fell into the wrong hands, could be repurposed for nuclear warhead-equipped missiles.

We’ve toured rocket factories in the US, which are ITAR facilities, and the compliance there is no-nonsense and much more stringent than CYA. No smartphones and definitely no photos. As far back as 1976, the US has treated commercial satellites as defense articles.

NOAA/CRSRA: While the US greenlit commercial imagery sales decades ago, it still imposed resolution caps and plenty of other stringent caveats. Over time, the industry’s optical capabilities kept improving but they were essentially rate-limited at what they could sell. All the while, the caliber and resolution of foreign sensing and imaging constellations kept improving (and their sales teams weren’t as handcuffed).

“There’s been a lot of push from the industry for the government to loosen restrictions to increase US competitiveness,” cofounder and CEO of Albedo Topher Haddad told us.

The US put a new three-tiered licensing process into place, which was celebrated by the commercial space industry for balancing national security and economic competitive equities.

Last fall, Albedo received the first license to sell 10-cm commercial satellite imagery (meaning 10cm per pixel), taken by its future fleet of satellites in very low-Earth orbit (VLEO).

Spectrum licensing: The FCC manages and licenses the finite resource of radiofrequency signals carried over the electromagnetic spectrum. The FCC’s satellite division aims to:

Authorize as many satellite systems as possible and as quickly as possible to enable speedy satellite deployments

Cut red tape and maximize flexibility for satellite operators providing services to individual consumers and corporate customers

Optimize efficient usage of spectrum and orbital resources.

If your satellite has a radio to communicate with the ground in space, then the FCC will want authority over giving that asset the greenlight. Just last week, the commission voted unanimously to open proceedings on in-space servicing, assembly, and manufacturing (ISAM), which could pave the way for it to gain some sort of regulatory authority over microgravity factories, servicing satellites, self-assembling outposts, and space gas stations of the future.

It’s wonky stuff, but spectrum is quite the beefy arena. Space companies are constantly warring for airwaves, and their lawyers really duke it out with sharply worded barbs via FCC filing.

While we’re here…Generally speaking, space is very litigious. Everyone loves to sue everyone.

Sending stuff to space: Wanna launch? Take it up with the FAA, and specifically the Office for Commercial Space Transportation (which is weirdly abbreviated AST). The FAA licenses all US commercial launches and reentries. In recent years, the agency has streamlined its licensing process and commercial launchers are better off because of it. By the numbers…

The FAA has licensed 475 launches, 31 Earth reentries, and 46 permitted experimental launches.

21 companies currently hold active launch licenses.

14 entities hold spaceport operator licenses (see below).

Going to space? Like, yourself? Chances are you’re not, as only 637 people have been to space and it’s still quite expensive. But that first number will soon grow substantially, costs will come down, and chances are one of you reading this will go to space before the decade is out. If that’s you, though, be prepared to go through customs when you’re back on American soil.

Also, good news, finders keepers now applies to US citizens who go to space. The US Commercial Space Launch Competitiveness Act, passed in 2015, states that US citizens can keep stuff they bring back from space. It essentially extends property rights to space. ‘Merica.

Widening the aperture: As we are an American company writing for a predominantly American audience, we focus on American laws. But international laws, norms, and treaties are also pretty important.

The grandaddy of ‘em all is the Outer Space Treaty (OST), which went into force in 1967 and now has 100+ nations that have signed on. The treaty holds that any country that so desires can explore orbit, nobody has sovereign claims on certain orbits or the Moon, you can’t put WMDs in space, and so on and so forth. A few other international treaties form the bedrock of space law:

The Rescue Agreement: Like maritime law, this covenant commits countries to rescue astronauts of other nations in need, should they find themselves in sticky situations.

The Moon Agreement: If you build a base on the Moon, you gotta tell the UN, and if you’re able to extract lunar regolith or other resources, you should do so in a responsible way. The US isn’t a party to the agreement and has instead been shopping around its lunar diplomacy-focused Artemis Accords to US allies. France became the 20th country to sign on in June, and Saudi Arabia the 21st last month.

The Liability Convention: States must own up to the consequences of their spacefaring actions. Specifically, states should take full liability for damage caused by space objects and should agree to standard procedures for adjudicating and arbitrating damage claims. All the space superpowers have a pretty shitty track record here.

The Registration Convention: The UN maintains a database of objects launched into space. This is actually a great resource. The online index lists 13,450 objects. Take a gander, if you’re so inclined.

For more light reading, you can also brush up on the UN’s five declarations and legal principles, which range from broadcasting back to Earth to nuclear power sources.

Key takeaway here: Nation-states are responsible for their private sectors, including satellite launches and commercial spaceflight activities. Before the decade is out, this will apply to in-space factories, private LEO space stations, commercial rovers on the Moon, and more.

Martian law: While we’re here, we’d be remiss not to mention that perhaps as a troll, SpaceX has said it will not recognize international law on Mars. Buried in the update of a Starlink terms of service update in 2020 was the claim:

“‘For services provided on Mars, or in transit to Mars via Starship or other colonization spacecraft, the parties recognize Mars as a free planet and that no Earth-based government has authority or sovereignty over Martian activities,’ the governing law section states.”

RISK FACTORS

Investing in space involves a high degree of risk. You should consider and read carefully all of the risks and uncertainties described below, as well as the other information included in this prospectus.

Capital/Financial Risk: Companies in the aerospace industry tend to be very capital intensive. A common failure is a risk to obtain this necessary capital when needed on acceptable terms

Market Risk/Economic Viability: Demand for services such as launch for small LEO satellites and space solutions is not well established, is still emerging and may not achieve the growth potential we expect or may grow more slowly than expected.

Risk of Life: Certain business models that involve human exploration carry the risk that an accident or catastrophe could lead to the loss of human life or a medical emergency.

Environmental risk: Orbital debris growth could potentially create substantial issues for satellite operations. According to NASA there are ~500,000 pieces of debris the size of a marble or larger and ~330 million pieces of debris-about one millimeter all large enough to damage or destroy most spacecraft/satellites.

Regulatory Risk: Space is a highly regulated industry. In the US, the FAA and FCC, and internationally, the ITU, play a significant role in launch access and satellite licensing and deployment.

The FCC regulates the spectrum in the United States and the ITU regulates global spectrum. Essentially, the two organizations decide the range of spectrum that each LEO satellite constellation can operate in. They can decide not to grant licenses if certain environmental issues become more of a priority.

Competition: There is a tremendous amount of competition within certain sub verticals of the space industry. For example:

Starlink competing against the growing supply of bandwidth, including next generation GEO satellites, LEO satellites (Starlink, Telesat, Project Kuiper from Amazon and OneWeb), and 5G.

Within launch, there are over 200 launch startups globally. Though most are not viable, the operational businesses are well-capitalized and going after a finite launch market. Especially in the small launch market (<250 tons), many commentators believe the market is heavily oversupplied.

FINAL REMARKS

We are in the era of a vast mobilization of space entrepreneurs. Scientific research is moving beyond labs and universities to critical applications solving significant problems on Earth. In the near-term, the market may have grown a bit too quickly thanks to a surge in inefficient capital. There will be consolidation via acquisitions and bankruptcies (maybe they were a few years too early). Some models will require a more mature space economy or supporting infrastructure before they become profitable businesses.

However, a significant number of space startups, powered by revenue-generating business models, are addressing real-world problems: ubiquitous broadband connectivity, in-space platforms for R&D and real-time monitoring of weather, people, and critical infrastructure. And we’re just scratching the surface of what’s possible. It’s our role as media partners, investors, and concerned citizens of Earth to encourage and support these efforts, rather than dismiss the intrepid entrepreneurs and policy makers working at the forefront of innovation.

Thanks to Ryan and Mo for the deep dive into space, Rahul for making it happen, and Dan for editing! Subscribe to Payload Space to get the latest insights on the space industry.

That’s all for today, we’ll see you Friday morning for a Weekly Dose of Optimism!

Thanks for reading,

Packy

Hm, i would have expected at least one mention of PanAmSat or DigitalGlobe in the history section here. Both very quite pivotal in shaping key commercial markets for space.

Earlier on, Canadian Telesat and Western Union in US knocked the doors open for privately run comsats

Why no mention that the ISS is going to end of life early, without the participation of Russia?

Unless someone pulls heavy lifters out of their butts in the next 2 years.

Seems like all this "advancement" has been focused on space tourism or LEO as opposed to anything truly extra-orbital...