Thank God For Data Centers

These Gigavillains Are Bringing So Many Technologies Down the Learning Curve

Welcome to the 2,232 newly Not Boring people who have joined us since our last essay! Join 267,788 smart, curious folks by subscribing here:

Hi friends 👋,

Happy Wednesday!

A couple weeks ago, I asked if you wanted me to start sharing more off-the-cuff notes with not boring world subscribers, and the response was great, so we’re back. It’s a Wednesday afternoon, not my normal send time, but these are meant to be less formal and more, “I noticed something interesting, here are my quick thoughts.” This one happens to be a little longer than it is quick, but it’s one I wanted to get out for two reasons:

People hate AI Data Centers, and I think they’re wrong, even if they don’t like AI.

Because I keep hearing, reading, and seeing that AI Data Centers are funding new technologies before they’ve come down the learning curve, which might be a providentially big boon to Reindustrialization and all of the hard, physical things we want to see in the world.

It’s pretty beautiful that gaming chips that evolved from Apollo-funded integrated circuits are creating a product with so much demand that their houses can pay for all sorts of novel technologies, like the Apollo Program did.

Let’s get to it.

Today’s Not Boring is brought to you by… Deel

Hiring globally doesn’t have to be complicated

Hiring globally can unlock growth, but local laws, payroll, and compliance often slow startups down.

Deel’s free guide breaks down what an Employer of Record (EOR) is, how startups use EORs to hire internationally without opening entities, and when it makes sense to use one so you can scale with confidence.

Thank God for Data Centers

There exists a vast pool of technologies that are potentially superior to those we employ today, but which require scale and learning curves to reach their potential.

Advanced nuclear reactors are one such technology - they are more expensive than alternatives today, but manufactured at scale, and benefiting from the learning curves required to get there, may become cheaper than other generation technologies. The cost physics are on their side, and nuclear is reliable, safe, firm, and clean.

The challenge with these technologies, in normal times, is that there is little economic incentive for the buyers who would enable the scale to stick their necks out. Natural gas is cheap and abundant, and it’s not that bad for the environment, compared to coal and oil at least, and the environment is someone else’s problem, anyway. And so, in normal times, we remain stuck in local maxima without the demand to push towards global ones.

Historically, these stalemates have cracked in a couple of main ways: Alpha Products and extraeconomic Buyers of Capabilities. These are essentially the same mechanism at different scales and with different motivations.

In The Electric Slide, we discussed the role that Alpha Products played in providing the initial demand that eventually brought each layer of the Electric Stack down their respective cost-performance curves. For lithium-ion batteries, the alpha product was the Sony Handycam. For neodymium magnets and motors, it was the 3.5” hard‑disk drive. For power electronics (IGBTs / inverters), it was the variable‑frequency drive (VFD) for industrial motors. For microcontrollers (MCUs), it was the calculator. Etc.

For each of these, the new technology was advantageous enough in a specific way to the end product that it was worth paying higher costs or sacrificing on other capabilities to capture those benefits.

Alpha Products, however, typically support components that are not multi-hundred million or multi-billion dollar projects in their own right.

The role of the extraeconomic Buyer of Capabilities in the development of new technologies is even better-understood. This is the DoD or NASA, mainly, buying technologies to confer a specific advantage, almost irrespective of their cost. This category of customer cares less about price than about capability.

Theirs is an important role because it gives new technologies the opportunity to get to scale, come down the learning curve, and ultimately compete in the much larger commercial market.

For a while now, but particularly over the past couple of weeks, I’ve heard some version of the same story over and over again:

“We are still going after our long-term mission, but to fund it, we’re planning to sell to data centers.”

Today, Data Centers are increasingly serving as Buyers of Capabilities, acting as something between a government and a commercial buyer. The Data Center is the meta-Alpha Product. If you can sell them something they need, fast, they have an almost bottomless bid.

This is true for obvious things like GPUs, inference chips, and DRAM, but it’s also true for companies that you wouldn’t typically associate with AI data centers, like supersonic turbines, enhanced geothermal, modular construction, high-voltage direct current grids, solid-state transformers, silicon photonics, optical fiber, lasers, batteries, and nuclear.

Many of these technologies have the potential to be better and cheaper than the incumbent technologies they aim to replace, but they have been too expensive and unproven to compete. With backlogs in all of the traditional inputs to Data Centers, however, developers are willing to pay up for new technologies that can deliver fast, which gives them the opportunity to scale up and cost down.

For these technologies, Data Centers act as a third type of Buyer of Capabilities, a commercial analog operating on DoD-style procurement logic but commercial timescales.

Given the size of the budgets, the relative smallness of any one input’s cost relative to the overall project cost and revenue opportunity, and the speed with which Data Centers are making decisions and putting down deposits, Data Centers may meaningfully increase the odds of success of hard tech companies and Vertical Integrators more than the market realizes.

Far from being the villains they are painted as (often using misinformation and largely due to their association with deeply unpopular AI), Data Centers may be the greatest accelerant of American Reindustrialization and a built-world future that benefits all people that we’ve ever seen.

They offer dilution-free capital (real revenue on a negative working capital cycle) to fund the big vision, and more importantly, the opportunity to get to scale and down the learning curve years earlier than would otherwise have been possible. This both accelerates timelines of things that might have worked, but more slowly, and makes companies that might otherwise have died in the Valley of Death viable.

Whatever your feelings are on AI, the furor towards Data Centers is misplaced. Hell, whether or not you think we’re in an AI Bubble barely matters here. In five years, this could all fall apart, and the world will be much better off. Data Centers are funding the future where no one else will.

This isn’t the first time that people have gotten mad that something that seems frivolous is sucking up so many resources. The immediate stuff - like how much money is being spent or power is being consumed - is an easy target, while the long-term benefits are hard to see.

We Choose to Go to the Moon Not Because it is Popular

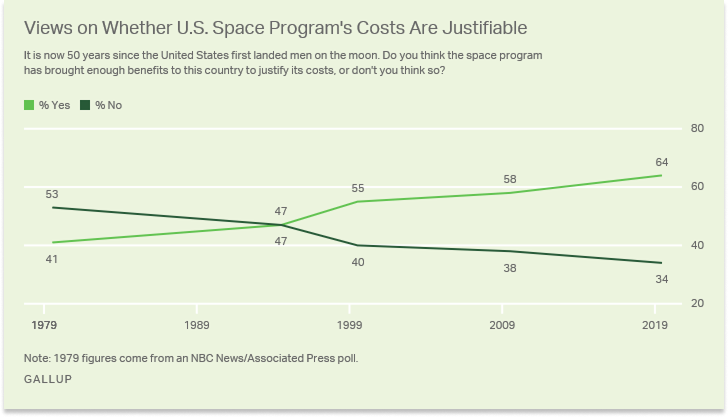

With the benefit of hindsight and distance, the Apollo mission has become one of America’s proudest accomplishments. At the time, though, not everyone loved JFK taking us to the Moon. There were too many problems on Earth to be solved to waste all that time, money, and smarts on a lunar boondoggle.

In May 1961, Gallup asked Americans, “It has been estimated that it would cost the United States 40 billion dollars-or an average of about $225 per person-to send a man to the moon. Would you like to see this amount spent for this purpose, or not?” 58% of respondents said that they would not, another 9% had no opinion, and only 33% supported the mission.

President John F. Kennedy gave his canonical “We choose to go to the Moon” speech not because it was popular, but because it was unpopular and he needed to rally support.

It didn’t work that well. In a 1964 Gallup poll that asked “Do you think the United States should go all out to beat the Russians in a manned-flight to the moon–or don’t you think this is too important?”, 66% of respondents said that they did not think it was too important, and another 8% said “Don’t know,” which amounts to the same thing. In the summer of 1965, “one-third of the nation favored cutting the space budget, while only 16% wanted to increase it.”

Even a decade after NASA pulled off the near-impossible, in 1979, only 41% of Americans told an NBC/AP poll that the benefits of the space program outweighed the costs. By 1995, that had risen to 47%, by 1999 it hit 55%, and by the 50th anniversary of the Moon Landing, in 2019, support had reached 64%.

One explanation is that, not having to pay the costs ourselves but getting to bask in the memory of victory, today’s Americans can of course look back and say it was worth it.

Another, though, is that over time, the real benefits, not at all obvious at the time, have become more clear.

Apollo’s critics were ultimately proven wrong, both because beating the Soviets to the Moon was awesome…

… and more directly because the absurdity of the task’s ambition coupled with the bottomlessness of its budget that they complained about were exactly the conditions needed to create terrestrially-useful innovations that would otherwise have taken much longer, or never been invented at all.

While the role that the Apollo Program played in inventing new technologies is probably overblown, it accelerated, scaled, and de-risked a lot of things that otherwise may not have gotten to sufficient scale or cost to impact our lives. Some of the technologies and products for which they served this role include:

Fireproof fabrics and flame-retardant materials (developed after the Apollo 1 fire), which made their way into firefighter suits and racing gear

Improved freeze-drying processes for food preservation

Mylar-based reflective insulation, which became the emergency space blanket

Advances in composite materials and ablative coatings

CAT and MRI imaging benefited from digital image processing techniques developed to enhance lunar photographs at JPL

Implantable cardiac pacemakers improved from bidirectional telemetry developed for astronaut biosensors

Cool suits (liquid-cooled garments) used for MS patients, burn victims, and racing drivers came directly from the spacesuit undergarment

Kidney dialysis machines used a chemical process developed to remove toxins from astronauts’ water

Black & Decker developed the technology to make cordless power tools for collecting lunar samples

NASA developed Memory foam (Temper Foam) for crash protection in seats

Water filtration using silver ions, based on the system that purified the Apollo crew’s water

Scratch-resistant lens coatings, derived from coatings developed for astronaut visors

Improved smoke detectors (the modern ionization-type was refined for Skylab, which leveraged Apollo hardware)

Even cleanroom protocols for handling lunar samples spread into pharmaceuticals and, relevant to today’s discussion, semiconductor manufacturing.

That’s just one program, albeit a very large one. If you zoom out to include the technologies that received early support from the DoD, the list includes pretty much everything that defines modern life.

The internet and TCP/IP directly, and Ethernet indirectly. Satellite communications, GPS, the inertial navigation systems that run in our phones and cars, and radio navigation. The mouse, windowing interfaces, and hypertext; the work that Doug Engelbart showed off in his “Mother of All Demos” was ARPA-funded. Public-key cryptography was invented for UK SigInt, Grace Hopper developed COBOL on the Navy’s dime, and DARPA funded the first AI labs at MIT, Stanford, CMU, and Stanford Research Institute for decades. The chips AI runs on, GPUs, and the CUDA software behind them, owe something to DARPA-funded parallel computing research. Siri’s lineage, for better or worse, through DARPA’s CALO speech recognition program at SRI. There are the more obviously military products, like the jet engine and the planes jet engines power, stealth coatings, night vision, radar and synthetic aperture radar, Lidar, ultrasound, drones, and infrared and thermal imaging. There are materials, like composites, including carbon fiber, titanium alloys, and advanced ceramics, all of which scaled through defense procurement. LEDs were funded through early signaling work, and digital photography found a buyer in early spy planes. In medicine, we have the DoD to thank for EpiPens, tourniquets, hemostatic agents like QuikClot, prosthetics, blood banking, and plasma storage. Penicillin was first mass-produced in a wartime crash program. And energy? Civilian nuclear power descended directly from Admiral Rickover’s Naval reactor program, lithium-ion battery research had defense funding, and solar photovoltaic cells were pulled forward by satellites’ unique power needs.

Military procurement is the closest thing that the United States has to a national industrial policy, and its worked. The military has funded the development of practically every general purpose technology of the past century, before the commercial market took those de-risked, cost-downed technologies and figured out how to bring them to the masses.

Of all of these, the cleanest case study and the one that maps most directly onto what’s happening in 2026, is the integrated circuit.

Minuteman, Apollo, and Moore’s Law

Fairchild Semiconductor was founded in 1957 as a transistor company, and its first big customer was the military.

Specifically, facing a threat from larger Soviet boosters that could launch intercontinental ballistic missiles (ICBMs) that could fit vacuum tubes, the US military, with its smaller boosters, had to invest in miniaturization, which meant transistors. Between 1958 and 1960, Fairchild’s revenue grew from $500k to $21 million, largely on the back of the Minuteman I program, for which it produced custom designs. Challenge was, as the number of transistors grew, the electronics industry ran into the “tyranny of numbers”: now that they could, engineers wanted to design circuits with thousands of components, all of which had to be wired together by hand.

So in Dallas, Texas Instruments’ Jack Kilby came up with his “monolithic idea.” “He realized that,” Carl Leonard writes, “instead of connecting separate components, an entire electronic assembly could be made as one unit from one semiconducting material by overlaying it with various impurities to replicate individual electronic components, such as resistors, capacitors, and transistors.” He had invented the integrated circuit (IC).

Three months later, in Mountain View, Fairchild co-founder Bob Noyce arrived at a similar idea from a different angle. Starting from the planar process, invented by Jean Hoerni in early 1959, Noyce realized that you could build transistors flat on a silicon wafer, with all the connections on the top surface, protected by a layer of silicon oxide. He wrote in his notebook, “In many applications now it would be desirable to make multiple devices on a single piece of silicon in order to be able to make interconnections between devices as part of the manufacturing process, and thus reduce size, weight, etc., as well as cost per active element,” and filed a patent that year.

While there are differences between the ICs they developed (Kilby’s used Geranium and Noyce’s silicon, for example), the two are credited as the co-inventor of the IC. What matters for our story is 1) the IC may not have been developed without demand from the Air Force, Army, and Navy, which were each spending real money on parallel attempts to solve it, and 2) Fairchild was now in the IC business.

In 1961, after starting at $1,000 per chip on tiny pilot runs the year before, Fairchild brought the integrated circuit to market at $120 per chip. The challenge was, no one really needed an integrated circuit, not enough to pay that price. Any electronics firm could wire together discrete transistors to do the same thing for a fraction of the price. As Britannica puts it, “a buyer had to have a serious space constraint to justify purchasing ICs.” Fortunately for Fairchild, NASA had a serious space constraint.

In early 1962, MIT’s Instrumentation Lab, which was responsible for the Apollo Guidance Computer (AGC), placed a test order for 100 ICs at $43.50 per unit. Meanwhile, getting ahead of volume and hoping to use scale to rev aerospace demand, Noyce cut the price of the IC from $120 to $15, an 87.5% drop, while still charging NASA and MIT premium prices to fund scale. “Noyce slashed prices, too, gambling that this would drastically expand the civilian market for chips, Chris Miller wrote in Chip War. “In the mid-1960s, Fairchild chips that previously sold for $20 were cut to $2. At times Fairchild even sold products below manufacturing cost, hoping to convince more customers to try them.”

Meanwhile, the government funded the gap. That November, MIT decided to go with Fairchild’s IC, or more specifically, its Micrologic computer made up of ICs. By 1963, MIT was consuming 60% of US IC production for the AGC; other military and aerospace buyers made up the rest. In a 1964 article for IEEE, Noyce wrote, “Military and space applications accounted for essentially the entire integrated circuits market last year, and will use over 95 per cent of the integrated circuits produced this year.”

In 1965, the year that Gordon Moore wrote the Cramming More Components onto Integrated Circuits paper that birthed Moore’s Law, ICs had reached cost parity with discrete components, at around $10, and were beginning to beat them. It was around this time that the Minuteman II program, which now used Texas Instruments ICs, became the technology’s largest buyer. That meant two things – 1) there were multiple large buyers of ICs and 2) there was competition – which combined caused Noyce to cut prices again, down to $2, and again, to $1. The cash coming in from Apollo allowed him to attack the commercial market with lower prices.

And it worked. By the end of the decade, America beat the Russians to the Moon, and Burroughs released the B2500 computer, the first to use ICs.

From that point forward, Moore’s Law has largely been driven by demand from the much larger and faster-moving commercial market. But the IC would not have come down the cost curve so quickly – and Moore’s Law, that self-fulfilling prophecy, may never have been coined or executed against – without the early space and military demand. It is to these Buyers of Capabilities that we owe the computer-powered world we inhabit today.

Something similar might be happening with Data Centers today.

Data Center Demand

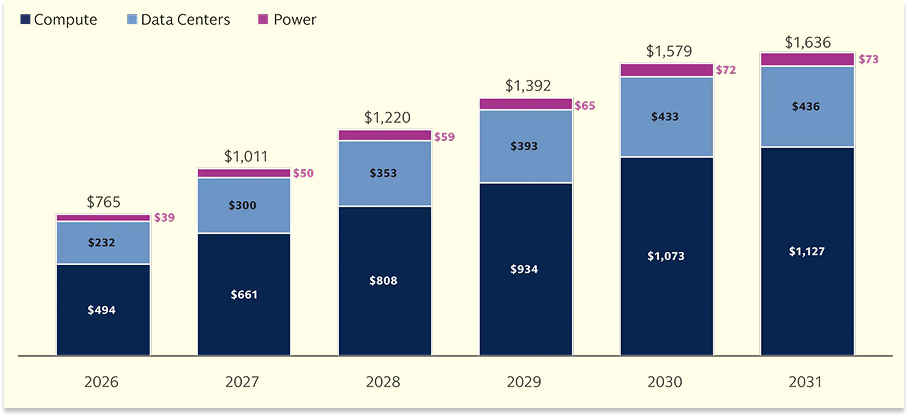

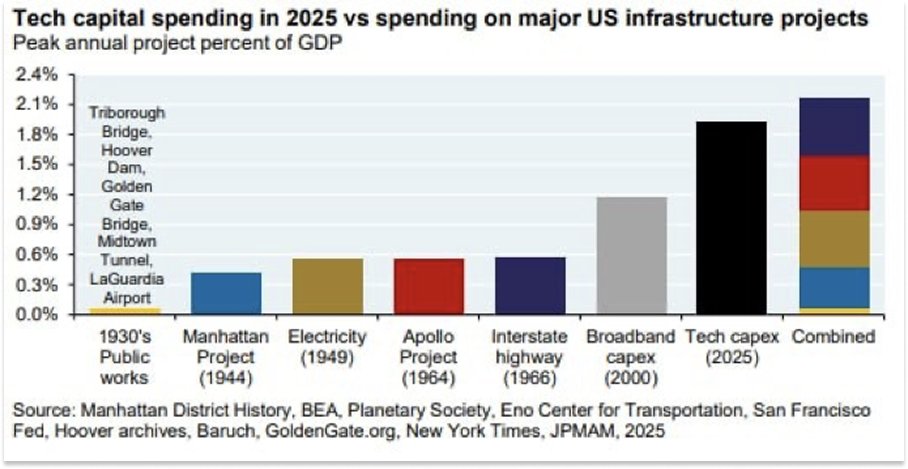

There is a sentiment floating around that we can’t build hard things in America anymore, but by any measure, modern AI data centers are hard assets to build and operate, and we are building a lot of very big ones. Western hyperscalers, labs, and neoclouds will spend something like$750 billion this year and more than $1 trillion next year building them. Goldman estimates that AI CapEx will take $7.6 trillion of capital between 2026 and 2031 across Compute, “Data Centers,” and Power.

This is an enormous amount of CapEx, absolutely, historically, any-way-you-slice-itly. With US GDP around $32 trillion, this year’s spend represents 2.4% of GDP. Assuming GDP grows by an aggressive 3% next year, AI CapEx will account for 3.1% of GDP. For context, the Manhattan Project reached 0.4% of GDP, the late-90s telecom bubble reached 1.2%, and even the Apollo Program only hit 0.4%. To find a more GDP-dominating project, you’d need to look to one of the two World Wars, the New Deal, or the Railroad Boom.

For a little more context, the $15 billion per year that Anthropic will pay SpaceX for the use of two of its Colossus data centers is roughly 60% of NASA’s entire annual budget.

Keep reading with a 7-day free trial

Subscribe to Not Boring by Packy McCormick to keep reading this post and get 7 days of free access to the full post archives.