Status Monkeys

Analyzing NFTs as Social Networks Using the Status-as-a-Service Framework

Welcome to the 1,901 newly Not Boring people who have joined us since last Monday! Join 67,713 smart, curious folks by subscribing here:

🎧 I lost my voice a little singing too much at the wedding, audio versions will be back soon.

Today’s Not Boring is brought to you by... UserLeap

If you read to the bottom of Not Boring essays, you’re already familiar with UserLeap. Over 7,000 of you have given me feedback via the microsurveys I include in every email. It helps me make the newsletter better every week.

UserLeap is a product research platform that makes it easy to build and embed microsurveys into your product (or newsletter!) to learn about your customers in real-time. Product teams use UserLeap to gather qualitative insights as easily as they get quantitative ones, and automatically analyze the results so teams can take quick action.

Not Boring readers don’t just give me feedback through UserLeap; hundreds of you have started getting feedback from your own customers with UserLeap. We’re in good company. Teams at Square, Loom, and Retool love UserLeap, too. In fact, UserLeap knows that once teams start using the product, they don’t stop, so they’re offering a generous free plan to try it out. Sign up below to start collecting insights today.

Hi friends 👋 ,

Happy Monday!

On Saturday, Puja and I went to our first out-of-town wedding since COVID (Congrats, Coop and Liz!). We spent a lot of time in the car driving to Richmond and back, which gave me a lot of time to think up wild ideas.

Let’s get to it.

Status Monkeys

The DEAD followed me across Twitter all weekend. Not in a Haley Joel Osment way or anything, it’s just that this one avatar kept popping up everywhere:

For the uninitiated: that green guy is a CryptoPunk. CryptoPunks are 24 x 24 pixel art NFTs, of which there are, and will only ever be, 10,000. CryptoPunks, created by Larva Labs in June 2017, are OG NFTs. As new NFT projects pop up hourly, CryptoPunks are scarce and valuable by nature of their age.

So as NFT values have soared over the past couple of weeks, CryptoPunks have led the charge. The most expensive Punk sold for 4.2k ETH in March. Today it’s worth $7.57 million USD. If you want to buy your very own Punk right now, the cheapest on offer will cost you 51.85 ETH. That’s the “floor price.” You’ll get a more common Punk at that price. To buy a rare Punk, an Ape, Alien, or Zombie, like the one seen above, you’re going to have to fork over a whole lot more ETH.

A few other things to know about CryptoPunks:

Owning a Punk is a status symbol, like owning a Ferrari or an expensive handbag.

Punk owners often use the image of their Punk as their profile picture (PFP).

Displaying a Punk that you don’t own as your profile picture is frowned upon.

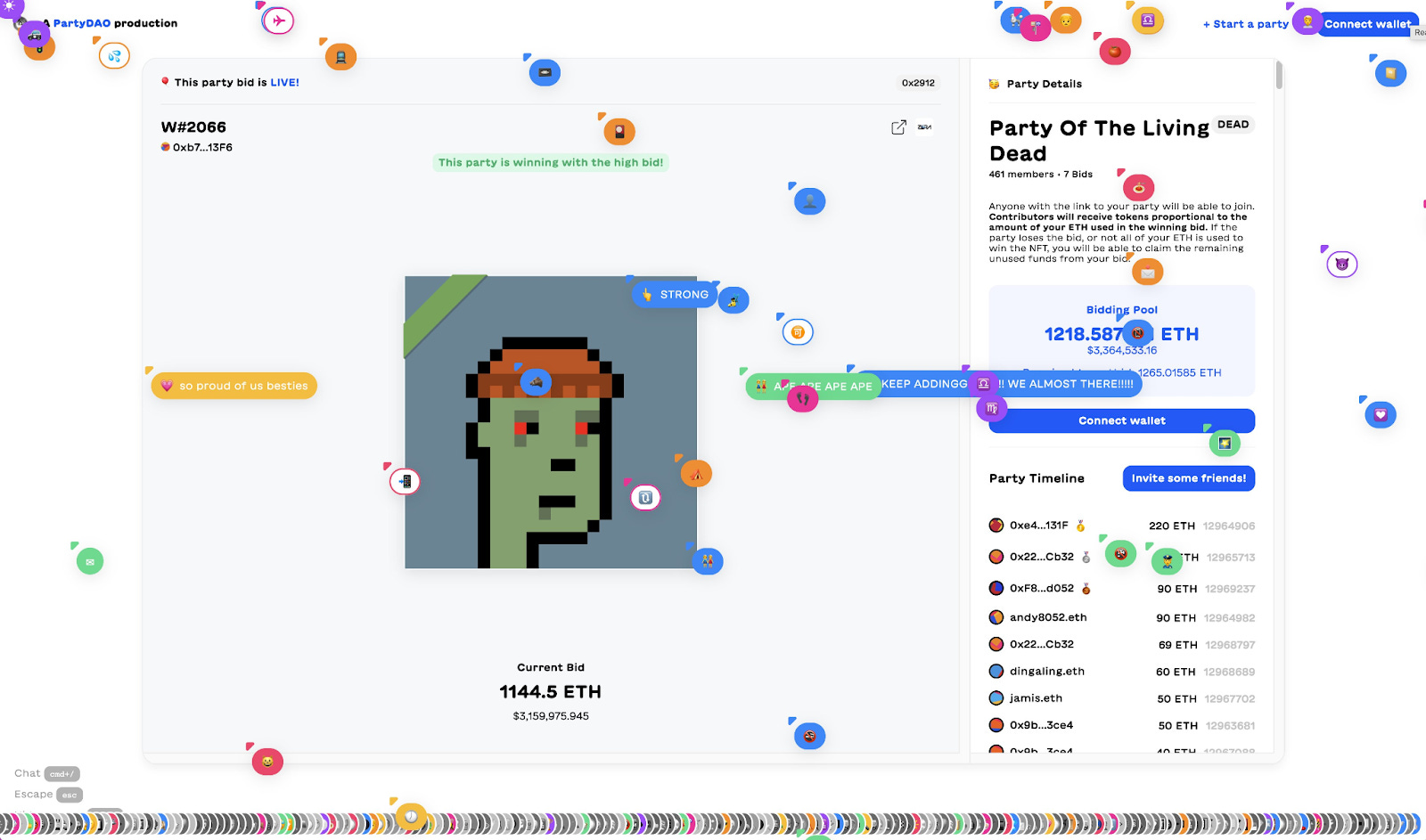

This weekend, hundreds of people changed their profile picture to that one single Zombie Punk, which sold for 1,201.725 ETH ($3.75 million) at auction on Friday. No one frowned upon so many people displaying the Punk, wearing a deconstructed party hat emoji, because they all owned it.

For Friday’s auction, 478 people joined forces on PartyBid, a new product created by Anish Agnihotri and the PartyDAO crew that lets people form teams to bid on NFTs, to pool their resources and go after the multi-million dollar Punk against rich whales. They called themselves the Party of the Living Dead. And they won.

PartyBid makes NFTs more social, with a literal party upfront and the opportunity for hundreds of people to buy, own, and manage expensive NFTs together in the back. Its social nature is obvious from its website, which feels as if Figma and Masterworks had a baby, with cursors and comments flying around the site in real-time. As Friday’s auction went on, hundreds of people, represented by moving cursors and emojis, visibly zoomed around the site. It’s hard to describe in words; you can see it in the image above, and you should check it out by visiting yourself.

Like a Zombie, NFTs were supposed to be dead. What’s going on?

I have a theory.

On Thursday night, I went on Sriram Krishnan and Aarthi Ramamurthy’s Good Time Show on Clubhouse to discuss the *Metaverse* with Gabby Dizon (YieldGuild), 3LAU, Donnie Dinch (Bitski), Jarrodd Dicker (The Chernin Group), Jon Lai (a16z), and Jesse Walden (Variant).

Not Boring readers will be very familiar with the Metaverse at this point. We’ve been talking about it for months and months. I’m guilty of tying anything that could conceivably be tied to the Metaverse to the Metaverse.

Over the past few weeks, the Metaverse has gone mainstream. Matthew Ball published his 9-part series. Satya Nadella talked about the enterprise Metaverse (sounds fun!). Zuck and Co have said “metaverse” a million times over the past couple weeks. Ben Thompson wrote a piece on the Metaverse.

NFTs will clearly play a role in the Metaverse. When everything is digital, proving that you own something and being able to bring it with you across the internet will be key. But this isn’t a Metaverse piece. It’s a social network piece.

At one point in the Good Time Show conversation, Jarrod Dicker brought up the importance of community and status in web3 and it triggered a high kid thought: NFTs tick a lot of the boxes of a successful social network from Eugene Wei’s Status-as-a-Service.

Before the full Metaverse arrives, there’s already something happening that’s bigger than jpegs. NFTs are starting to feel a lot like a new kind of social network that sits above other social networks and communities -- something of a Superverse -- and there’s no better framework to evaluate a social network than the one Wei put forth in Status-as-a-Service (StaaS).

Status-as-a-Service

(If you’ve read and internalized Status-as-a-Service, you can skip this section.)

Eugene Wei, a former product leader at Amazon, Hulu, Flipboard, and Oculus, is one of the best tech essayists on the internet. Practically everything he writes becomes canon, and Status-as-a-Service, which he wrote in February 2019, might be his greatest contribution.

The piece makes Not Boring seem short. It comes in at a whopping 19,825 words. If you haven’t read it, I highly recommend that you do so, but for now, I’ll summarize a few of the main points that are relevant to this piece.

Wei begins with two principles:

People are status-seeking monkeys

People seek out the most efficient path to maximizing social capital

Even though those are uncontroversial statements, Wei argues that we don’t analyze social networks through the dimension of status or social capital. Money is easier -- there are numbers, and what gets measured gets analyzed -- but, he says (emphasis mine):

Social capital is, in many ways, a leading indicator of financial capital, and so its nature bears greater scrutiny. Not only is it good investment or business practice, but analyzing social capital dynamics can help to explain all sorts of online behavior that would otherwise seem irrational.

Less than 1,000 words into his piece and two full years before NFT mania, Wei unknowingly laid the groundwork for analyzing what’s happening. NFTs blur the lines between social and financial capital, and as the media has been quick to point out, buying jpegs for thousands or millions of dollars seems irrational.

The mistake that those who dismiss NFTs make is the same that Wei argued people were making in analyzing social networks: missing the importance of social capital. Traditionally, people have used Metcalfe’s Law to explain the network effects powering social networks: “The value of a telecommunications network is proportional to the square of the number of connected users of the system (n^2).” The more users a social network has, according to Metcalfe’s Law, the more valuable it is to every new user.

The problem was, Metcalfe’s Law didn’t perfectly explain what was happening in the real world. Metcalfe’s Law alone would predict that whichever network got big first would continue to build up an increasingly insurmountable lead by being the most valuable to each new user. But Facebook took down MySpace, and Instagram and Snapchat stole younger users’ attention from Facebook. People’s preferences aren’t captured so cleanly.

It wasn’t that network effects and Metcalfe’s Law were wrong, it was just that they didn’t capture the reasons that someone might use a social network beyond pure utility, so Wei proposed a new framework for analyzing social networks’ strength that added social capital to the mix.

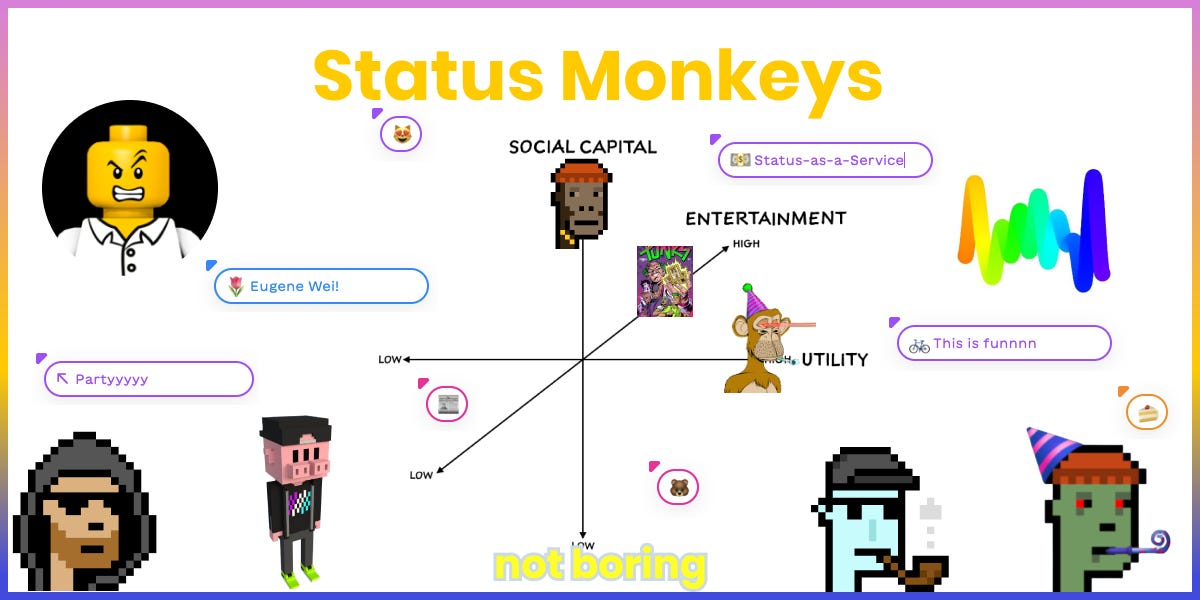

Wei evaluates social networks’ strength on three axes: Social Capital, Entertainment, and Utility. In the essay, he focused on Social Capital and Utility.

Utility is relatively easy to understand. If you can find the answer to your question on Quora or easily reach an old high school friend whose number you lost on Facebook, those products are providing you utility.

Social capital, on the other hand, is harder to define and relies on the creation of a “successful status game.” To help explain why some new social networks succeed and others fail, he used a metaphor: crypto.

He said that new social networks are analogous to Initial Coin Offerings (ICOs) in four ways:

Each new social network issues a new form of social capital, a token.

You must show proof of work to earn the token.

Over time it becomes harder and harder to mine new tokens on each social network, creating built-in scarcity.

Many people, especially older folks, scoff at both social networks and cryptocurrencies.

It’s a really good metaphor. Take Bitcoin and Twitter.

Bitcoin issues bitcoin (BTC). Twitter “issues” followers.

Miners receive BTC for securing the network. Twitter users receive followers for tweeting witty, amusing, or mind-expanding things in under 140/280 characters.

It costs more to mine BTC now than it did earlier, and will continue to get harder until all 21 million BTC are mined. In the early days of Twitter, you could get followers by tweeting what you were eating for lunch; today, people have resorted to long threads.

This one is self-explanatory.

Neither Bitcoin nor Twitter existed fifteen years ago. Both are dominant forces today. They bootstrapped from nothing to something by rewarding early adopters, incentivizing them to do work for the network, and making it increasingly challenging to mine new tokens.

All four points are important to understand, but the most useful is the idea of proof of work in status games. If everyone who signed up for Twitter got one million followers just for signing up, there wouldn’t be any social capital in having one million followers. The fact that high follower counts are scarce makes them valuable, and the proof of work requirement enables scarcity.

Leaving Entertainment out of the equation, Wei talks about five arcs that social networks can follow, four of which are trade-offs between social capital and utility over time:

First Utility, Then Social Capital. “Come for the tool, stay for the network.” Instagram first attracted users with an easy photo editing tool and became a photo-based network on top of which people have built huge followings and businesses.

First Social Capital, Then Utility. Wei highlights Foursquare, Wikipedia, Quora, and Reddit as products that used the promise of social capital to get people to do free work that then becomes a utility for the masses.

Utility, But Not Social Capital. Messaging apps are incredibly useful for communicating with people you know, but don’t really help users build up social capital.

Social Capital, But Little Utility. Wei puts Facebook in this category, mentioning that many of his friends just stopped using Facebook with no impact on their life (This describes me too, as I suspect it describes many of you).

The fifth category, the “holy grail,” is Both Social Capital and Utility Simultaneously. To find an example, Wei goes to China’s WeChat, which combines a Facebook-like Moments feed (social capital) with a whole lot of utility, about which I wrote:

People use WeChat to message friends, shop, read the news, play games, pay for things in physical stores… pretty much anything you can do on your phone, you can do on WeChat.

WeChat created a killer combo of social capital and utility from the get-go, which hasn’t really been replicated in the West.

Even for social networks that get it right, though, Wei points out that there are two forms of asymptotes that limit growth or lead to downright collapse.

Social Asymptote #1 is Proof of Work itself. Not everyone in the world can do what it takes to gain social capital on any given social network, which creates an upper limit. I’m fascinated by TikTok, but I’ve never made a TikTok, because I’m not a great dancer and I’m just not willing to put in the work to get good at whatever the TikTok algorithm requires. TikTok is still growing absurdly fast, but if even I, who loves social networks, won’t use it, there’s a ceiling somewhere.

Social Asymptote #2 is Social Capital Inflation and Deflation.

On the inflation side, when a social network gets too successful, and there are too many people using it, the company behind it inevitably needs to introduce an algorithmic feed to handle all of the noise. Wei argues that Facebook introducing an algorithmic feed was always likely because the only scarce resource in an abundant digital world is users’ attention, so it’s necessary to deliver the things they’re most likely to engage with. It makes sense, but it was a tough break for any of the companies that relied on Facebook for a connection with their audience.

On the deflation side, social networks can get less cool as more people join. The canonical example here is what happened to Facebook when parents started joining: all the young people left for Instagram and Snapchat. Once the cool kids start leaving, the slightly less cool kids follow, then the next group, then the next, and since more of the less cool group (parents, in this case) keep joining, the cool proportion gets worse fast.

“At that point,” Wei cautions, “that product or service better have moved as far out as possible on the utility axis or the velocity of churn can cause a nose bleed.”

That’s the meat of the argument:

Social networks need to be analyzed based on more than their network effects.

There are three axes for analyses: Social Capital, Utility, and Entertainment.

New social networks are like ICOs, particularly because successful ones will use an appropriately difficult proof of work to create scarcity and status.

There are many paths social networks follow, but the best is to have high social capital and utility from the start.

There are two asymptotes that even successful social networks might hit: the proof of work ceiling and social capital inflation/deflation.

Networks that start with high social capital need to figure out how to build utility before they hit those asymptotes to survive and thrive.

Wei spends the rest of the piece giving examples and adding richness to the thesiss. Again, you should read it, but for our purposes, there are few particularly valuable tidbits that I’ll highlight:

Social capital can be used as temporary energy. “You can think of social capital accumulation incentives like these as ways to transform the potential energy of status into whatever form of kinetic energy your venture needs.”

New proof of work can lengthen the status game. Why social networks need to add new forms of proof of work to lengthen the half-life of status games, and what they can learn from gaming companies. “Casino games in Vegas pay real money to set an attractive floor on the ROI of playing. Some MMORPGs offer other benefits to players, like a sense of community, which last longer than the pure skill challenge of playing the game.”

Social capital turns into financial capital, and vice versa. “These trades allow us to assign a tangible value to social capital the way one might understand the value of an intangible asset like leveled-up World of Warcraft characters when they are sold on the open market…”

Lack of social graph portability is frustrating for users. This one is particularly germane, and highlights a main difference between traditional social networks and NFTs, so I’ll pull a big quote here:

The restrictions on porting graphs is a positive from the perspective of the incumbent social networks, but from a user point-of-view, it's frustrating. Given the difficulty of grappling with social networks given the consumer welfare standard for antitrust, an option for curbing the power of massive network effects businesses is to require that users be allowed to take their graph with them to other networks (as many have suggested). This would blunt the power of social networks along the social capital axis and force them to compete more on utility and entertainment axes.

What if you could get the benefits of a social network in a more portable, decentralized package? It’s time to turn it over to NFTs.

A Brief Recent History of NFTs

As a very quick refresher, NFT stands for Non-Fungible Token. The power of NFTs is that they make digital assets scarce. Scarcity makes digital assets valuable, like exotic cars or fine art or rare stamps are. Beeple’s Everydays would not have sold for $69.3 million if there were no way of proving that the owner bought the official version.

NFTs started in CryptoKitties in 2017, but they really got hot in early 2021 (I first wrote about them in late January). Beeple and NBA TopShot led the charge as BTC and ETH ripped to all-time highs. The newly crypto-rich did what rich people do: bought art. NFTs were met with incredulity and dismissed as toys.

Then, in April, crypto prices tanked and NFTs cooled off with them. The incredulous cooed, “See, I knew it was a bubble when people started paying millions of dollars for jpegs!”

In June, crypto site Protos was one of many blogs with an article like this one, all citing a 90% collapse in volume:

The article’s second sentence read: “NFTs peaked on May 3, when $102 million worth were sold in a single day.” The party was officially over, though: “But according to data analyzed by Protos, just $19.4 million in NFT sales were processed in the past week.”

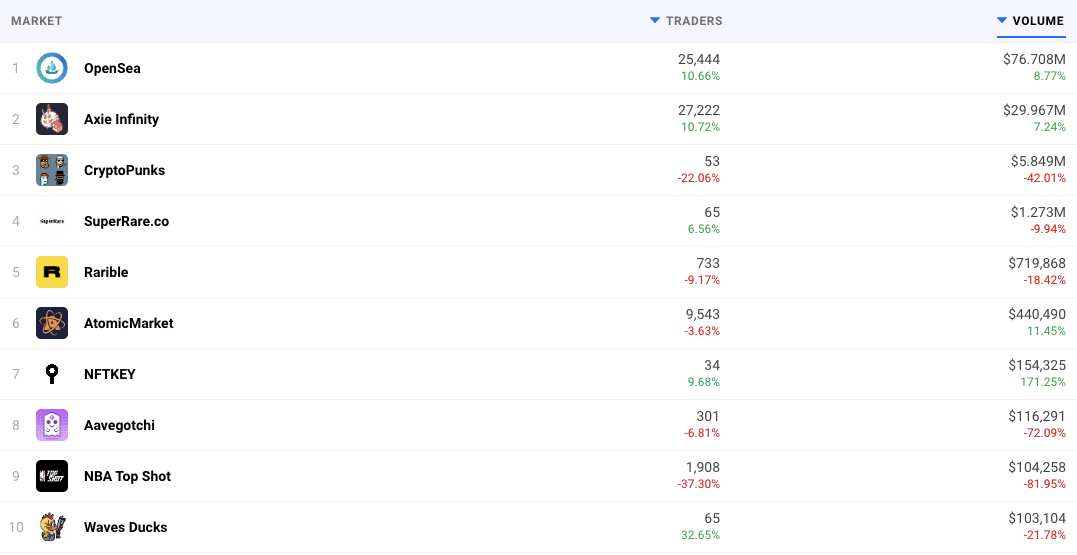

And then, over the past month or so, something funny happened. NFTs came roaring back. In just the past 24 hours, $106 million worth of NFTs from just two marketplaces -- OpenSea and Axie Infinity -- traded hands.

Over the past thirty days, according to DappRadar, the top ten NFT marketplaces did $1.86 billion in volume.

This time around, it feels as if NFTs are pulling the price of ETH and BTC up, and not the other way around, as those coins’ prices rise despite the SEC’s growing interest in regulation under new Chairman Gary Gensler and potential harm from the proposed Warner-Portman Amendment to the Infrastructure Bill.

So why are NFTs back, and why might they be around for a long, long time? Let’s turn back to our friend Eugene Wei.

Investment-as-a-Status

The best place to start is where Wei himself did: with the two principles.

People are status-seeking monkeys

People seek out the most efficient path to maximizing social capital

There’s something very meta, then, about the fact that we status-seeking monkeys are turning to digital monkeys as the most efficient path to maximizing social capital.

Apes have led the charge during NFT Summer.

The #3 NFT collection over the past month is the Bored Ape Yacht Club (BAYC). Like CryptoPunks, there are only 10,000 Bored Apes.

The Bored Ape Yacht Club website calls itself “a limited NFT collection where the token doubles as your membership to a swamp club for apes.”

Unlike CryptoPunks, BAYC is brand new: it launched on April 30th. But it’s already the third most popular NFT collection, likely owing to its combination of social capital and utility. The New Yorker’s Kyle Chayka recently wrote a piece called Why Bored Ape Avatars Are Taking Over Twitter, in which XMTP founder Matt Galligan (who sports an Ape as his Twitter avatar) said, “It became a status symbol of sorts, kind of like wearing a fancy watch or rare sneakers.”

Apes are a theme, even outside the digital walls of the Yacht Club. Two of the four most expensive CryptoPunks ever, and the two most expensive sold in July, were rare Apes:

If it seems irrational that people would spend millions of dollars on pixelated jpegs of apes, well, “analyzing social capital dynamics can help to explain all sorts of online behavior that would otherwise seem irrational.”

So instead of dismissing what is very clearly becoming a real thing, let’s dig a little bit deeper and throw NFTs on Wei’s axes. We’ll even include entertainment for fun.

This is the power of valuable NFTs: they are high in social capital and utility, and moving higher in entertainment. They hit the social network trifecta.

Social Capital. NFTs are social capital with skin in the game. It’s “Investment-as-a-Status.” There are only 10,000 CryptoPunks and Apes, and within that limited set, there are some that are particularly valuable, and therefore high status. Owning a CryptoPunk or a Bored Ape, and often displaying it as your Twitter or Discord or Telegram profile pic, says something about you. They say that you were either early, or you’re rich, or you were early and now you’re rich. Using high-priced things to increase social capital is not new -- look at fine art, expensive cars, yachts, private jets, handbags, or any number of scarce things that very rich people buy to signal status. It’s just that NFTs are even more legible and public.

Utility. NFTs also have utility as investments, as tickets for access to Discord groups, and even as something that you can hang digitally on your wall. Over time, NFTs will give owners access to events and unique experiences as they evolve and infiltrate a wider audience.

Already, buying a Bored Ape gives owners access to the Bored Ape Yacht Club. NFTs like Axies provide real utility: ownership means employment for tens of thousands of people. Meebits, from CryptoPunk-creator Larva Labs, come with 3D models and animations, and could be used as characters in games.

Entertainment. Although Wei didn’t get into it (until TikTok and the Sorting Hat), most successful social networks score high on the Entertainment axis, too. TikTok is arguably as much an entertainment network as it is a social network. Ditto with YouTube. People lurk scroll Twitter for entertainment for hours every day without interacting, purely for passive entertainment. NFTs are entertaining as well: it’s fun to watch the sales, and some people are already building personas and online characters starring their Apes or Punks. Bidding on PartyBid is as much a social activity as it is an investment.

The entertainment axis for NFTs is just getting started. Punks Comic is creating comic books starring characters based on 16 Punks, with more to come. They’ll be expanding to Bored Apes soon, too.

That’s just an obvious first step. Many NFT bulls believe that there won’t be any major cultural events that aren’t memorialized as NFTs, which will play back into the events themselves, and which might change depending on what happens IRL.

So NFTs provide social capital, utility, and entertainment... how do they do against Wei’s idea that new social networks are analogous to ICOs? Given that they’re both crypto projects, that one’s almost too easy:

Each new social network issues a new form of social capital, a token. ✅

You must show proof of work to earn the token. ✅

Over time it becomes harder and harder to mine new tokens on each social network, creating built-in scarcity. ✅

Many people, especially older folks, scoff at both social networks and cryptocurrencies. ✅✅✅

There’s some nuance here.

NFTs more directly tie social and financial capital. One way to get your hands on a valuable NFT is to get in early and get your hands on something when it’s being minted, or when it’s still so early that the broader community hasn’t gotten interested. The other is just to ape in and buy one. The former is more proof of work -- figuring out which projects to back early -- while the latter may be closer to proof of stake -- putting up your ETH to back and participate in the project.

There are direct similarities, too: many people, especially older folks, will scoff.

Even I’ll admit: NFTs as a social network feels like a bridge too far.

They don’t look like social networks; if anything, they look like small communities. But the local exotic car club is a social network of sorts, as is the country club, they’re just too small to be meaningful enough for analysis. NFTs bring status signaling and social capital online at global scale. But still, if Facebook and Snapchat and TikTok and Twitter are social networks, NFTs feel like something different.

And I think they are. But that’s also the right strategy.

In Status-as-a-Service, Wei wrote a section titled Why copying proof of work is a lousy strategy for status-driven networks. Basically, using the same core proof of work mechanism as an existing social network and adding on a couple features doesn’t work because it requires the same skill to be good at each, and people are going to gravitate towards the one with more people. Bitclout, which is like Twitter but crypto, still rewards people for the same things Twitter does: saying witty, amusing, or intelligent things. The difference is, if you succeed on Bitclout, your token becomes more valuable and you make money. It’s possible that a direct exchange of social capital for financial capital is enough to get people to duplicate work or move their work to a new platform, but it’s challenging.

Instead, you need to reward an entirely new behavior. NFTs may be different enough to work, and they’re not asking people to leave their favorite existing social network. In fact, it’s better for the NFT collection and all of its holders if everyone shows off and talks about their NFTs on their favorite existing social network. The buzz could directly create more demand, or it could create indirect opportunities. If a Netflix exec sees everyone on Twitter talking about CryptoPunks, they might turn it into a show that rewards the owners. If someone at Christie’s sees everyone in the Discord they’re in talking about Art Blocks, they might put a Squiggle up for auction, bringing credibility and reach to the whole collection.

When that happens, each NFT owner (or group of owners) would build up a tremendous amount of social capital that they might bring to bear on the network. If CryptoPunks gets a Netflix show, the Punks that starred in it might become celebrities in their own right, and build up exogenous social capital that they could use on a range of social networks.

NFTs aren’t a social network in the traditional sense. There isn’t a NFT, Inc. They don’t have a home, one place where every NFT owner congregates and NFT, Inc. aggregates. Maybe OpenSea does it? Maybe it’s something like blockchain games/virtual worlds like CryptoVoxels, Decentraland, or The Sandbox. Maybe someone builds a pseudonymous social network for which owning an NFT is the price of admission, like a @harvard.edu address was for Facebook. Most likely, it’s none of the above. It’s something new: a Superverse.

I don’t mean super like “super!” I mean that NFTs might be a social network that sits above, or “super-”, the other networks.

As Wei wrote, “The restrictions on porting graphs is a positive from the perspective of the incumbent social networks, but from a user point-of-view, it's frustrating.” He said that if regulators forced social networks to make their graphs portable, it would, “blunt the power of social networks along the social capital axis and force them to compete more on utility and entertainment axes.”

What if, instead of regulation, it was a new entrant that proved the power of portability. When I wrote that, “crypto is kind of the native token for the Great Online Game,” it’s that portability that I was referring to. You can earn status in one place, own it without platform risk, and carry it with you across the internet. The same holds for NFTs, no matter which platforms rise and fall. Any social network that has profile pictures (read: all social networks) are fertile ground for NFTs to spread. Owners already display their Punk as their Twitter avatar or their RTFKT sneakers on their Instagram pictures.

And it wouldn’t just be individuals moving around. Groups of people who collectively own particular NFTs, like the Party of the Living Dead or DAOs that own NFTs could move around in packs to any new platform, using Discord as a basecamp from which to launch missions to all new territory. On new and existing platforms, members could bring the exogenous social capital that comes with owning valuable NFTs, and work as a group to build up the social capital of their NFT avatar. This thread talks about fractionalized NFTs as mini-networks, and the ability to turn 10,000 scarce assets into 10,000 scarce assets backed and promoted by hundreds of thousands or millions of people.

Wei wrote about Chris Dixon’s idea of “come for the tool, stay for the network.” NFTs make it possible to come for the tool, bring the network wherever there’s the most social and financial value.

With all of the arguments for NFTs, it’s also important to point out the obvious caveat here: the price of specific NFTs or total NFT demand could drop, maybe precipitously. Even non-bubbles have bubbly pockets. Recently, another 2017 vintage NFT collection, Ether Rocks, has seen a surge in demand, with rocks going for over $100k. Even the project’s creators call it “pet rocks on the blockchain.” The resurgence seems to be a test of just how far communities can push their power to make anything valuable.

That said, NFTs do seem to possess characteristics that make them resilient against Wei’s two asymptotes.

Against Asymptote #1, Proof of Work, NFTs have the ability to add infinite new proofs of work, which Wei said can lengthen the half-life of status games. The two examples he used of games that successfully extended their lives beyond when games typically survive -- casino games in Vegas and MMORPGs -- did so because of characteristics they share with NFTs. Like casino games in Vegas, NFTs can “real money to set an attractive floor on the ROI of playing.” Like MMORPGs, NFTs’ sense of community can last longer than the pure skill challenge of playing. That said, NFTs will face an asymptote from crypto adoption and affordability. NBA TopShot and Fractional are steps in the right direction, and no doubt more innovation will come to make NFTs more accessible to a wider group of people while retaining the benefits of scarcity, or replacing scarcity with other benefits, like community.

Against Social Asymptote #2, Social Capital Inflation and Deflation, NFTs have the advantage of being decentralized. While certain platforms may present NFTs in an algorithmic feed, NFTs themselves are portable and can be used and displayed wherever the owner chooses. They’re also likely less subject to evaporative cooling since NFTs aren’t one monolithic thing -- they’re a group of smaller communities, each with their own standards. There are only 10,000 Punks, but there might eventually be thousands of DAOs or fractional ownership groups that each form their own small communities with their own standards and rules. That fractal structure should make them more resilient. Plus, thanks to proof of stake and the fact that owners choose when they sell, it’s going to cost parents a lot of time and money to take over CryptoPunks like they took over Facebook.

It’s still early. Even I, who loves this stuff, don’t own a Punk, Ape, or any other major collection. More infrastructure needs to be built, more fabric that connects disparate NFT projects. But it seems as if NFTs have the right ingredients to build a new form of social network -- a Superverse -- on top of existing networks like Twitter, Instagram, Snapchat, Discord, and TikTok, and to adapt and thrive over time.

New NFT projects can harness a potent combination of social and financial capital to get off the ground. Ownership brings social capital, utility, and entertainment. There are ever-evolving proofs of work, from figuring out the next big thing to creating brand extensions like Punks Comics to marketing particular NFTs to raise the profile of the whole collection. Punks owners have been buying up billboards in NYC, Miami, and London to spread the word. NFTs are part of the Great Online Game, and as such, the rules and opportunities are always evolving and expanding. Powerful things happen when you combine money, status, and community.

As always, I’m the first to admit that all of this sounds crazy. NFTs feel more like a fad than like a new form of social network. But thankfully Eugene Wei gave us a framework for evaluating the strength of social networks, and NFTs do shockingly well against it. There’s not much in Status-as-a-Service’s 19,825 words that would refute the idea of NFTs as social networks; in fact, nearly every section held little nuggets in support of the idea.

The next big thing will start out looking like a toy. The next big social network may start out not looking like a social network at all. The future is going to be crazier than we can predict, and a social network based on jpeg ownership certainly fits the bill.

So what’s the takeaway? What do you do with this information?

Social networks reward early adopters, and a social network with money baked in gives early believers a double-whammy. Go explore. Find an NFT that resonates with you. Join a PartyBid. Get involved. And for the love of god, don’t be one of those older folks that scoffs at NFTs.

Not Boring Jobs

Not Boring Jobs is the best place to find your dream role at a fastest-growing, not boring startup. In a little over a week, 151 of you have applied for Not Boring Jobs!

Today, I’m featuring three amazing jobs, with two non-technical options:

Two quick programming notes:

At noon EST today, I’m doing an AMA chat with Sam DeBrule on the Journal Slack. You can join here if you’d like to get in on it.

On Wednesday at 2p EST, I’m hosting a Writing Workshop with David Perell. Sign up free here.

Thanks to Dan and Puja for editing!

Disclosure: I am an idiot and don’t own the NFTs discussed today, except one Axie.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Thursday!

Packy

A great writeup as always, but wanted to push back just a bit on the idea of NFT as a status enhancing network. While I don't disagree that humans are status seeking monkeys, NFTs don't yet confer the type of social prestige that would create that social network enhancing effect.

I think it is lacking a "metaverse" that is widely used to show off that NFT token. This metaverse has to be both widely used, so that people can notice your status signalling, and it has to have some type of exclusivity (or scarcity) with the particular NFT token series . After all, NFT art seems like it can be pumped out fast. And the same art can even be reused multiple times if you have different NFTs built on different blockchains right? e.g if I purchase a NFT piece of art, how am I going to get everyone on say Facebook to realize that pixelated art avatar is worth a million bucks ? There isn't evenfunction on Facebook to support authenticating that you are the only allowed user of that NFT art...

Until something like this happens (think the Metaverse in REady Player One) I think NFT is a fad. I think it will have great functionality once the appropriate dominant metaverses are created that can leverage them

This is brilliant. Thanks for this analysis!