Welcome to the 867 newly Not Boring people who have joined us since last Thursday! If you aren’t subscribed, join 45,133 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts

Hi friends 👋 ,

Happy Thursday!

Startup stock options are one of those things that startup employees should know a ton about but just don’t. There’s a never-ending debate in tech around whether stock options make sense for employees, or whether they’re just a way for companies to pay less cash. Even when things seemingly go really well for a company, employees’ situations are often murkier than it seems.

That’s why I was so pumped when Shanna Leonard, who runs marketing at Secfi, reached out about working together. I’ve been wanting to write about this forever.

This essay is a Sponsored Deep Dive on Secfi. For those who are new around here, that means that Secfi is paying me to write about their business. You can read more about how I pick and work with partners here.

This one is a little bit different though. The Secfi team really just wants more startup employees to know what their options are, make a plan, and not leave millions of dollars on the table. Each person I’ve spoken to there has their own personal startup equity horror story, and they want to make sure that you don’t go through the same thing. I, too, gave up cash for equity, and it was a terrible financial decision. This one is personal.

Obviously, if Secfi can help you make smarter decisions, that’s a win-win, but more thoughtfulness around employee equity is a win in itself. So we’re going to go deep on how equity works, why people don’t exercise, and what happens when they don’t.

(One note: I wanted to call this post ESOP’s Fables, but ESOPs are a public company thing more than a private company thing. But I thought it was clever, so I couldn’t not share.)

Let’s get to it.

Startup Stock Options Options with Secfi

In 2020, startup employees left $4.9 billion on the table by not exercising their pre-IPO options.

Not exercising pre-IPO means employees missed out in two major ways:

They let the typical 90 day window pass after leaving and forfeited unexercised options, either all of their options or a portion.

They stayed at the company through IPO, but didn’t exercise before the IPO and had to pay short-term capital gains or ordinary income instead of long-term capital gains because of “cashless exercising.” Costs can soar post-IPO.

That combination cost employees four point nine billion dollars. $4,900,000,000. 4,900 million. At Snowflake alone, ex-employees left 72 million options worth $1.27 billion unexercised. Ouch.

Those numbers are so big as to feel kind of meaningless, but they represent years of blood, sweat, tears, uncertainty, and financial trade-offs down the drain.

Most people who work for early stage startups take less cash compensation than they’d be able to get at a more mature company in exchange for a few things: a more fun work environment, the chance to change the world, more responsibility than they’d get elsewhere, and a host of soft benefits, but mainly, they do it for the employee stock options.

Employee stock options are the lifeblood of a startup. Options are the main way startups compete on comp with big companies like Google and Goldman that can afford to pay infinity times more cash. They offer the promise of millions and millions of dollars if things go really, really well.

When I left Bank of America Merrill Lynch and went to Breather, I took a 70% pay cut on the cash side, but I got options worth 1% of the company in exchange. Even coming from finance, I didn’t fully understand my options. I just did some hyperoptimistic expected value math (1% * $1 billion = $10 million!) and that was good enough for me.

I’m certainly not alone. Most startup employees don’t understand their options. Some don’t even know they need to exercise them or put out money at all. Because options feel like lottery tickets at the early stage, employees don’t think all that much about things like the tax implications of when they exercise, what happens if they leave the company, and all of the little details that can mean hundreds of thousands or even millions of dollars. Which is crazy, because those options can often represent, on paper, a huge percentage of their net worth.

For a group of ostensibly intelligent people, startup employees put surprisingly little thought into managing their options. These are builders. They get so immersed in their day-to-day and building great things that they lose sight of their own personal gain at times. Plus, it’s kind of taboo to talk about maximizing the value of your options when there’s real work to be done.

And most companies don’t do much to help. It’s (generally) not because they don’t want to, but because this stuff is really complicated, and so far in the future, and startups have dozens of more pressing fires to put out at any given time. In the Eisenhower Decision Matrix, employee options fall into the “important, not urgent” bucket...

UNTIL all of a sudden, your company is all over the news. It’s going to IPO. Everyone is talking about it. You did it. Finally! But, wait, what the hell happens to your options? It costs HOW much to buy them and you owe WHAT in taxes? Now, it becomes personal. And urgent.

A lot of startup employees are going through that emotional arc right now. 2021 looks like it’s going to be even more painful for ex-employees who didn’t exercise their options (and even for current employees who will pay higher taxes if they haven’t planned properly, but it’s hard to feel too bad for them).

The year is less than four months old, and there have already been 429 IPOs on US exchanges. This time last year, there were 40. That’s a 10x increase. To be fair, a lot of the new IPOs are SPACs -- 308 SPACs have raised $99 billion via IPO already this year versus $83 billion in 248 IPOs all of last year -- but there have been some major tech IPOs already this year:

That’s an incomplete list, plus those 308 SPACs and many of last year’s 248 are lurking with bags full of money that they need to spend on taking companies public within two years.

For people who own equity in those startups, this is going to be an amazing year. Thousands of people will become millionaires for the first time, some will generate multi-generational wealth, and a few will even become billionaires. But each of those companies also has tons of former employees consumed by regret at not having purchased their options, and many others who will end up giving the government nearly as much as they take home.

Secfi wants to change that, starting by helping you get smarter on startup equity:

How Startup Equity Works

Why Employees Don’t Exercise

Options Exercise Options

Meet Secfi

The CAC Arbitrage

Secfi’s Vision

The best time to start thinking about how to handle your options was when you got your offer letter. The next best time is now.

Secfi can help. I could (and will) nerd out on this problem for hours, but Secfi is paying me and I want to make sure you check them out, so I’ll introduce you to Secfi now, then we’ll come back to them later.

Secfi is a team of equity experts 100% focused on helping startup employees understand, maximize and unlock the value of their stock options and shares. If you’re an employee at a startup, Secfi wants to make sure you’re on the right track. Really. I badly want this piece to go viral mainly because the team genuinely cares so much about helping startup employees.

So here’s an ask: if you know an employee at a unicorn startup, share this essay with them to make sure they’re thinking through things properly.

Secfi has educational resources, tools (including tax calculators), and real live people who can help you think through your equity. Secfi’s equity strategists have deep experience as financial advisors, wealth managers, investment managers and analysts, and tax professionals, and have worked with employees at the vast majority of US unicorns. They can help you.

If you have options, stop reading, check them out, and then come back:

Welcome back. Let’s learn why startup equity is great, but not as simple as it seems.

How Startup Equity Works

First things first, stock options are pretty great. A century ago, even a couple decades ago, the idea of an employee sharing in the upside with the owners of a business would have sounded absurd. When we spoke, Secfi’s CEO Frederik Mijnhardt pointed out that startup employees owning 20% of their businesses on average is a great step (but only a first step) towards minimizing wealth disparity.

Silicon Valley is built on the back of stock options. They represent a chance for employees to become capital instead of just labor. They reward people for early belief in an idea, and the hard work it takes to make that idea a reality. Without options, it would be hard for cash-poor early stage companies to attract the top talent it needs to succeed. Goldman and Google will always be able to pay more cash than any startup. But ~*options*~ are a Golden Ticket.

A major part of the allure of joining a startup is the chance to work really hard for a few years and make millions. Join a startup when it’s young, get shares in the company, help it grow into the next big thing, exit, and retire rich.

It sounds simple, but it’s so much more complex.

First, you don’t just get equity in the company. If you work at a company long enough, you earn the right to buy equity in the company. Those are called options. Just like options on public equities, they give the owner the right, but not the obligation, to buy shares in the company at a certain price. If you’re really early, that price might be $0.01 per share or $0.10 per share or some other very low number, meaning it’s mostly upside. But either way, options do not mean that you own shares in the company. You need to actively buy them.

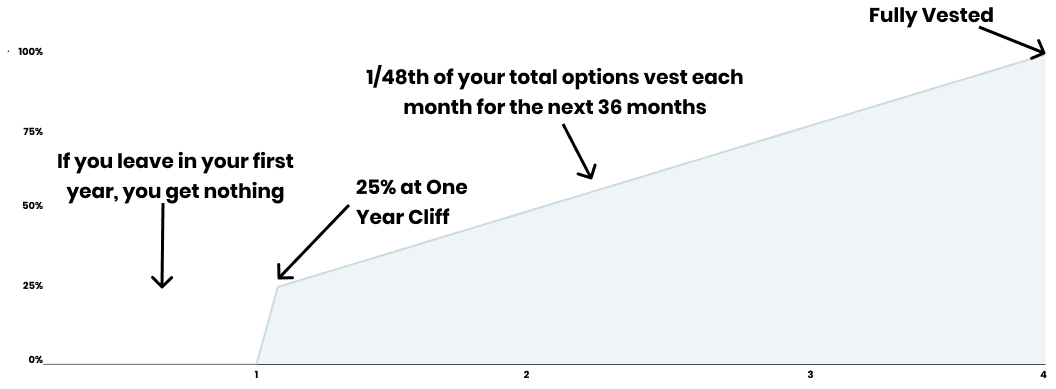

Plus, you don’t earn them all upfront. Typically, if you stay for a year, you earn a quarter of your options, and then you earn a little bit more every month for the next three years. That’s called vesting, and this particular case is the most common: four year vesting with a one-year cliff.

As those options vest, employees have the right to exercise them, or to keep them as options. Exercising means plopping down cash upfront for shares that may or may not be worth something, but it also means potential tax benefits down the line. While you’re employed, you have the option and some time to figure it out. Once you leave, you don’t.

If you leave at any point -- whether you’re fired or leave voluntarily -- you typically have 90 days to decide whether you want to exercise the portion of your options that have vested aka buy equity in the company. Some companies offer longer time periods, but after 90 days, Incentive Stock Options (ISOs) convert to Non-Qualifying Stock Options (NSOs), which come with higher taxes.

Exercising has a direct cost -- if you own 50,000 options that give you the right to buy shares at $1 per share, you have to pay $50,000. That’s a lot of cash to plop down, and if you have meaningful equity, the number may be much higher than that.

Worse, you often have to pay taxes based on the delta between your strike price (the $1 per share number) and the company’s most recent valuation (talk to a tax professional or Secfi about your specific case). This is based off something called a 409a valuation, in which an outside firm analyzes the business based on comps and ballparks what the company is worth. The better your company is doing, the higher your tax bill is going to be when you exercise, even though you might not be able to sell your shares and make any actual money for years.

Up until an actual exit, either via an IPO or an acquisition, most employees don’t know how to turn their valuable equity into cash. Even if things are looking good, they can all fall apart.

Most startups fail. Many once-hot startups end for selling for less than they raised. In those cases, employees typically get nothing for their options, even if they exercised, or worse. When WeWork filed to go public, many employees took out loans against their options to buy houses; when the IPO imploded, they were stuck with mountains of debt backed by equity whose value had collapsed 80% and many were fired from their job.

If your company is one of the lucky few that does have a successful exit, you’ve won the lottery. If you still work for the company, or left and exercised your options (bought the shares), you stand to make life-changing amounts of money. But the $4.9 billion number we started this piece with represents the fact that there are thousands of employees who left companies that ended up having successful exits but didn’t exercise, or simply never exercised pre-IPO. They had the golden ticket, and they gave it away, either completely or in chunks to Uncle Sam.

Why would they ever do that?

Why Employees Don’t Exercise

There are two ways to think about exercising options:

You can exercise your options as they vest while you’re still employed.

If you leave, voluntarily or involuntarily, you typically have 90 days to exercise.

There are different consequences for each.

Not exercising while remaining employed can mean tax consequences later, through a higher delta between your strike and current valuation and through the difference between short-term and long-term capital gains. But you still hold onto the right to exercise and to benefit from a liquidity event like an IPO or acquisition.

Not exercising after you leave means forfeiting the right to buy shares in the company, and means missing out on all of the upside in the case of a liquidity event. That sucks.

While both cases are very different -- the former means an unbelievably amazing exit becomes slightly less unbelievably amazing, the latter means a lifetime of regret -- they both have the same root causes.

Lack of awareness

Uncertainty about the company’s prospects

High costs of exercising

We’ll take each in turn:

Lack of Awareness

Most startup employees simply don’t think deeply about managing their options. They often make lower salaries than they would at other jobs, savings are tight, and they don’t save up money to exercise. They often don’t even realize that exercising while employed is even an option, and don’t understand why it might be beneficial. Even while Breather was growing quickly, from a $20 million valuation to $250 million while I was there, I never once thought about exercising my options. I didn’t even realize it was a thing. (In retrospect, thank god.)

Consider yourself aware. You need to think about this. Might I suggest Secfi’s Equity Academy and Options Exercise Tax Calculator as starting points?

Uncertainty About the Company’s Prospects

Sometimes, you’re at a startup and you’re just not sure it’s going to work, or how much it’s going to work.

While you’re employed, you’re willing to pay higher taxes in the future so you don’t have to spend your hard-earned money today on an uncertain bet. They’re called options for a reason.

When you leave, you need to make a hard choice: spend my money to buy these shares now and hope that there’s a good liquidity event in the future, or forfeit most of the on-paper comp earned through years of hard work. It’s never easy to give away those options, and many people just buy so that they don’t feel regret if things do go well. But it’s expensive.

Sometimes, employees even leave, exercise their options, and then sell when given the opportunity because they think the buyer believes in the company more than they do. If you haven’t listened to my podcast with my friend Brett, he was the first employee at Drizly and sold most of his shares in the secondary market when he got the chance. He thought he was real smart, until Uber recently acquired Drizly for $1.1 billion dollars. For a raw take on what it feels like to miss out on all of that upside, give it a listen:

High Costs of Exercising

It can be really, really expensive to exercise your options. That’s because there are two costs when it comes to exercising: the direct cost and the tax bill.

The direct cost is straightforward. You own 50k options at $1, you pay $50k for the shares. That’s a lot of money, but ideally you’re doing it because you believe that what you’re buying is worth a lot more. Let’s say, for example, that the company was recently valued at $100 per share Nice! Free money!

Well… that’s where the tax bill comes in. According to Secfi’s research across 69 late-stage unicorn companies (companies valued at more than $1 billion), taxes make up 85% of the cost of exercising stock options. 🤮

Since most people are unaware they’re going to have to pay taxes, Secfi calls it the surprise factor. They call the overall expense the unaffordability factor.

I’ve seen this firsthand (unfortunately, I haven’t felt it firsthand, but close enough).

At Breather, I worked with an ex-Uber employee who needed to exercise his options within 90 days of leaving Uber to join Breather. He was early at Uber and left when they were worth $10s of billions of dollars. Pretty amazing, right? Not so fast. Exercising meant he owed hundreds of thousands of dollars in taxes, even though Uber wouldn’t IPO for another two years.

He couldn’t sleep because of the tax bill hanging over his head. He spent the better portion of a few months on calls with people he was trying to sell shares to in order to generate the cash he needed to buy his options. He asked me if I had any friends who might want to buy. Finally, he was able to find some people to buy some of his shares in the secondary market and used the proceeds to pay off the tax bill, but that meant giving up his hard-earned upside after months of stress.

It’s easy to dismiss that as a Champagne problem, but it really sucks. Upside is what your startup promised you, and why you took a pay cut in the first place. Try choosing between owing the IRS hundreds of thousands or giving up equity you earned from years of grueling work. Uber was not known for its work/life balance.

Luckily, he was able to figure it out, and he did really well when Uber IPO’d (as did the people who bought his secondary).

Selling some of your shares to cover the tax bill is just one way to exercise options. Let’s go over the full menu.

Options Exercise Options

If you have options, you have some options. Secfi not only didn’t ask me not to list other options, they actively encourage you to shop around and figure out what works best for you. Remember, the #1 takeaway here is to be educated and have a plan.

So what are the options?

Don’t Exercise. This is always an option. Particularly if you think your options are at an inflated strike price, that the company will struggle to exit, or will fail altogether, not exercising is certainly an option, and maybe the best one. I didn’t exercise when I left Breather.

Pay Out-of-Pocket. If you’ve planned ahead or happen to have enough money saved up, you can pay to exercise your options out of pocket. That’s great because it means not selling shares or owing anyone anything. Unfortunately, this option makes the most sense before the company has grown its value too significantly, and gets harder as the company gets more valuable, and therefore as the likelihood of a liquidity event increases.

Borrow From Friends and Family. Like paying out-of-pocket, borrowing from friends and family means that you don’t need to sell shares or owe money to anyone who would repossess your home. That said, it comes with the social pressure to make sure you don’t lose your friends’ and family’s money.

Sell Secondary to Outside Parties. Like my ex-Uber friend, one way to raise the money to exercise is to sell some of your shares to other people. There are funds set up to do this, and platforms like Forge and EquityZen that will collect pools of secondary shares and match them with buyers. Or, if you own shares in Stripe or Epic, please give me a call and let’s work something out. One limitation here is that companies often limit whether or how much employees can sell on the secondary markets, another is that selling triggers capital gains tax.

Tender Offers. Sometimes, typically at Series C and beyond, companies orchestrate tender offers in which (often existing) investors make an offer to buy shares from employees to give them a little liquidity. Sounds great, but tender offers are historically underpriced. Sacra wrote a thorough piece on how and why this happens, but the long and short of it is that tender offers are typically priced at the last round’s valuation, which gets stale as hypergrowth companies grow. The longer from the last round the offer comes in, the more mispriced it is. As a result, tender offers typically only get 37% participation.

Take a Loan from a Hedge Fund or Bank Against Your Shares. There are plenty of funds out there, and even some banks, willing to lend you money to exercise your options if you’re at a later stage company with good prospects. As happened with WeWork employees, these can potentially get you into trouble if the company never gets liquidity or takes a long time to reach a liquidity event.

Of course, there’s a better way…

Meet Secfi

I remember sitting in my office and texting my friends Nick, Tucker, and Tommy the day that Secfi announced its first funding in 2018, led by Howard Lindzon’s Social Leverage. It seemed like such a good idea. We all knew (or were) people who’d been killed on their startup options in some way or another, and we were all kicking ourselves over text for not thinking of the idea first. So what does Secfi do?

Secfi is the first “pre-wealth management platform” for startup employees. They work with late stage startup employees who are in high growth mode on path to exit by doing a few things:

Educate them on what their options really mean

Help understand what it would cost to exercise them

Scenario plan

Offer non-recourse financing

This last piece is the bread and butter of Secfi’s product. Secfi will give startup employees non-recourse financing to exercise their options. It’s not a loan, but you can think of it in the same way you’d think about a loan, except that if your company never exits, you don’t owe Secfi anything. Even if your company IPOs and it doesn’t do well, and your shares are worth less than Secfi financed, you only owe the lesser amount. It’s really no-risk financing.

It starts with figuring out where your options stand, and what your options are:

Sign up for Secfi and enter information about your company and some personal details.

Access a set of tools to help you figure out the value of your shares and the costs to buy them (including taxes). They’re sophisticated. They’ll even help determine the different costs for exercising now versus waiting until an exit event. It’s fun. I sadly do not hold employee options in any unicorns, but I pretended that I did a few times.

You can (and should) do those things if you’re at all curious about the real value of your equity. If you want to secure financing to cover those costs, submit a request and they’ll get back to you with next steps. They currently work with over 80% of US unicorns, and if you work for one of those companies, 1) congrats, and 2) the process can be fast... like a few days. Here’s how that works:

Secfi determines how much financing you’re eligible for (if you have $1 million worth of options, you might be eligible for something like $250k in financing) and at what rate.

Secfi doesn’t take the risk itself. Instead, it acts as an intermediary between capital providers and employees. Last January, Secfi raised $550 million in financing from Serengeti Asset Management.

You never pay cash interest - it compounds and is taken out of your profits in the case of a liquidity event. You may pay an equity share which allows the investor to share in the upside of your equity in the case of a liquidity event.

When your company goes public or gets acquired, you pay the financing back along with the accrued fees and keep the rest of the upside yourself.

That’s it. Compared to other options, Secfi is preferable to:

Selling secondary: you keep the upside, don’t trigger capital gains, and keep your Qualified Small Business Stock (QSBS) tax treatment.

A loan in that you’re not on the hook in case things don’t go well.

Not exercising your options: you retain your chance at upside while Secfi and its capital partners take the risk.

That said, Secfi encourages startup employees to shop around and do their homework. For early employees at unicorn companies, exercising options ranks as one of the top lifetime expenses. If anything, Secfi just wants people to treat their options with the same amount of thought and care with which they treat which car to drive or which house to buy.

After shopping, many employees decide to go with Secfi. They work with employees at 80% of US unicorns and host $13 billion worth of equity options on the platform. Check out the case studies from anonymized employees at three of last years’ biggest IPOs: Airbnb, DoorDash, and Snowflake. Once your company is worth a few hundred million dollars, you should start talking to Secfi (and you should read the resources in their blog and Equity Academy before you even sign your stock option grant, or today if you’ve already signed).

Secfi almost seems too nice, and too riskless. Even I, the optimist, was a little skeptical. But that desire to help startup employees comes from two places: where Secfi comes from, and where it’s going.

Secfi was born after one of its founders got burned himself. He left his company and discovered that to exercise his $50k worth of options he would need to pay $1.8 million in taxes. He had to walk away from the options. He built a company to make sure that his experience didn’t happen to other startup employees.

In talking to Secfi’s teams and investors during this process, that mission rings loud and clear. And it’s genuine, because it’s an issue most of them went through themselves.

Frederik told me that he “had to learn the hard way that startup equity can’t just be neglected, that I couldn’t just wait to figure it out later.”

Shanna Leonard, who now runs marketing at Secfi, sold shares on the secondary market, her CPA messed up the tax calcs, and she ended up in a messy tax situation.

Martin Malloy, who runs content at Secfi, recently joined Secfi from a newly-IPO’d company after realizing that he and so many of his co-workers were unprepared to go public. He had to scramble at the last minute to avoid a massive tax bill, ended up working with Secfi to exercise his options, and then decided to join the company.

That shared experience comes through. When I asked Howard Lindzon, who led Secfi’s seed, the most underappreciated thing about Secfi, he told me: “It’s really employee-centric.” Unprompted, on a separate call, Rucker Park’s Wes Tang-Wymer, who led the A with the biggest check his fund has ever written, said “The company is incredibly employee-centric.”

Part of that comes from the Secfi’s history and its employees’ past experiences, and some of that comes from the company’s vision. In this business, being employee-centric is good business.

The CAC Arbitrage

Secfi wants to build a modern wealth management platform that serves startup employees from pre-wealth through post-IPO riches. They feel that options financing isn’t the end of the journey, but the beginning.

From that perspective, one way to look at the non-recourse financing and employee education that Secfi offers is as a customer acquisition channel that becomes profitable on the first transaction. It’s part of a newer generation of fintech startups that do well by doing good.

Broadly, there have been two waves of fintech from a customer acquisition perspective:

Companies built modern versions of old financial products and spent a ton of money to acquire customers. One very smart person told me that the problem with a lot of fintech companies is that you’re competing for customers with whoever is able to build the most optimistic Lifetime Value model. Google and Facebook are the real winners here.

Companies give benefits directly to customers upfront to acquire them more cheaply, and then add on additional services over time. Customers are the winners here.

This new model is structurally better for customers and businesses. A lot of ideas that you hear and ask “what’s the catch?” might fall into this category. The catch is that they’re paying less to Google and Facebook to acquire you. This is the holy grail in fintech (and really any business): low CAC, high LTV. Acquire a specific customer segment cheaply by owning a specific niche channel or offering highly-relevant products, and then sell them other financial products they need.

I’ve written about a few companies that work this way before:

BlockFi uses high-interest crypto deposits to acquire crypto-wealthy and crypto-curious customers, and is adding on new products like credit cards to increase LTV.

CashApp uses viral mechanics and influencer-led giveaways to acquire lower-income customers cheaply (CACs were under $5 last year) and has added products like rewards (Boost), stock trading, Bitcoin, direct deposits, business accounts, and Cash Card.

TrueAccord actually has companies send them customers for free so TrueAccord can help collect debts, and can layer on additional services that on-ramp them to the financial system.

MainStreet gets small businesses and startups the money the government owes them, and will roll out financial products that help them grow.

Ramp helps businesses save money so that they stay in business longer, grow faster, use more Ramp products, and spend more money with Ramp.

The beautiful thing with these businesses is that they’re actually incentivized to be good actors. I specifically called out how nice the Ramp and MainStreet teams are in my posts on them; at the time, I didn’t realize the connection. There’s even theory to back it up.

Game theoretically, these companies are playing infinitely repeated games. Unlike single shot games, in which the preferred strategy is often to defect, to maximize for yourself in the short-term, in infinitely repeated games, the preferred strategy is cooperation.

These companies are often profitable early in the relationship because of low CACs, but they’re incentivized to keep customers happy so that they can increase their literal wallet share over time. If they mistreat customers at any point early in the journey, they would miss out on selling them the whole universe of other products on the roadmap.

That description fits Secfi to a T.

Secfi’s Vision

In Secfi’s case, they acquire a very specific set of high-value customers -- employees at valuable startups -- by educating them and offering them the best product on the market for a very acute need. There’s no better way to engender goodwill than saving or making people hundreds of thousands or even millions of dollars. Plus, increasing the number of wealthy startup employees, and minimizing the taxes they need to pay, directly increases Secfi’s total addressable market (TAM).

So far, Secfi has focused on this pre-IPO stage, on making sure that employees are smart about their options and offering non-recourse financing that lets them minimize taxes while retaining upside. That’s been a three-year Phase I.

Secfi is in this for the long-haul, and it plans to support startup employees from pre-IPO to post-IPO.

Since it works with so many startup employees across 80% of US unicorns, it will focus on adding new products to help them manage their newfound wealth. Rucker Park’s Tang-Wymer pointed out that there’s no good solution for people with between ~$3 million and $10 million in wealth -- they’re tweeners. That’s too much to just plop in Wealthfront or Robinhood, but not enough that high-end wealth managers like Citi Private Bank want to work with them.

For that band of people, the tech is insanely behind. Wealth managers who serve the ultra-wealthy never built modern tech to serve them because older high-net worth people expect white glove treatment. Without software, it’s not easy for them to come down-market and retain their margins.

By building solutions that combine software and experts, Secfi can not only serve more clients at better margins, more importantly, it can serve them in the way that they expect to be served. These are people who made their fortunes in tech; they expect to manage their wealth in a similar fashion. That may mean all sorts of things: diversification (many of these peoples’ wealth will be highly-concentrated in one stock), angel investing, charitable giving, mortgage lending, cash management, and more. Think of all the things you’d want if you woke up with $5 million in your bank account, and you have a pretty good sense of Secfi’s product roadmap.

Secfi won’t build all of this in-house; they’ll partner with companies like AngelList or AltoIRA or Wealthfront or any of the number of companies that provide specific solutions, while building where no good products exist today. They can serve as the glue between all of these products and give wealthy startup employees comprehensive tools, advice, and insights on how their whole portfolio fits together, and the tax implications of all of it.

One obvious question about Secfi is: what happens in a downturn? What happens in a world in which there’s not a multi-billion dollar IPO every week, or if companies worth billions in the private market now come back down to earth? Won’t Secfi get stuck holding the bag?

That was actually the question that Nick, Tucker, Tommy, and I had on that first text chain about Secfi. There are a couple of answers, one technical and one more broad.

Technically, Secfi’s capital partners take the underwriting risk. If they were to offer financing to too many companies that failed to exit, they could face losses. They’re compensated for that risk with interest rates and stock fees.

More broadly, though, Secfi’s bet is that the largest group of wealthy people in the coming decade will be the startup employees who took pay cuts to take a chance on early ideas, and poured their blood, sweat, and tears into making them realities. While there will certainly be cyclical downturns, the secular trend is towards more ownership in the hands of the people creating the value, and Secfi exists to serve those people. There’s over $200 billion of wealth in non-founder startup equity in the US alone, and Secfi wants to make sure that those employees keep it and manage it well.

Ultimately, Secfi’s north star is to help startup employees build wealth. That’s the catch: the better startup employees do, the better Secfi does.

If you’re a startup employee, you should make a plan today:

Ask your company to give you more education and resources

Run your situation through planning tools

Talk to Secfi

Secure the bag 💰

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Monday,

Packy

Share this post