Welcome to the 574 newly Not Boring people who have joined us since last Thursday! If you aren’t subscribed, join 32,866 smart, curious folks by subscribing here:

Hi friends 👋 ,

Happy Thursday! Today, we’re bringing back a format I love that we haven’t done for a while: the Not Boring guest post! The point of guest posts is to bring you insights and perspectives from people who know a lot more about a certain space, or have different or more nuanced takes, than I do.

Today’s guest writer, Dan Teran, fits the bill perfectly. Dan and I first met in 2014, during his time as CEO of office management platform Managed by Q, which he co-founded in 2014 and sold to WeWork in 2019. MBQ was at the forefront of applying the Good Jobs Strategy in a fast-growing marketplace startup. Harvard Business Review wrote about MBQ in 2017, saying:

Teran has focused on four things: pay, scheduling, benefits, and advancement. Employees start at $12.50 an hour. Full-time workers average 120 hours a month, and they are offered health insurance and a 401(k) plan. Employees are part owners of the company, and they get stock options.

So when Dan approached me about an essay he was writing on how food delivery platforms’ disregard for the little guy leaves them open to attack from new entrants and regulators alike, I got excited: he’s exactly the person who should be writing exactly this piece.

(Pair with: Jeremy Diamond’s excellent April piece on food delivery strategy, Feeding the Rebels.)

Dan delivered. This piece covers restaurant economics, disruption theory, the conservation of attractive profits, and the cycle of bundling and unbundling to argue that companies like DoorDash and Uber Eats are bad for restaurants, which will ultimately be bad for their own business.

Give it a read below, and check out the rest of Dan’s work on Medium.

But first, a word from our sponsor.

Today’s Not Boring is brought to you by… OpenPhone

OpenPhone is the easiest way to set up a business phone number. It’s so easy that Not Boring got a phone number before getting its own, non-Substack domain. I use OpenPhone when I have good-old-fashioned voice calls with experts and sponsors, and most importantly, to text with all of you.

Last time OpenPhone sponsored Not Boring, I asked you to text me, and kicked off dozens of great conversations. Let’s do it again. I’d love to hear what you think of the guest post format, what other guests you’d love to see, and what topics I should cover next.

So shoot me a text: 1-917-818-0620.

Plus, OpenPhone is even better for teams than for my 1-man operation. Companies big and small use it to replace Google Voice with modern software, give everyone on the team their very own business number, build custom, automated workflows, record conversations, and keep in touch with customers.

Get your team set up with a powerful and delightful business phone today:

Let’s get to it.

The Beginning of the End

By Dan Teran

The impact of the COVID-19 pandemic on third party food delivery is a Rorschach test. What you see depends on what you believe.

Some view third party food delivery operators, such as DoorDash, UberEats, and Grubhub, as heroes of the pandemic, a lifeline to restaurants, creators of employment for masses of essential workers that are responsible for slowing the spread of the virus by keeping diners safely in their homes.

Others view these firms as unscrupulous predators, draining profits from independent restaurants while undercompensating and mistreating delivery workers, all to satisfy the appetites of venture capital investors who have gambled billions of dollars on a business model that may never generate more cash than it has consumed.

Public markets have made their view known. Uber has been catapulted to all time highs, trading at over $100B market capitalization, gobbling up competitor Postmates and adjacent Drizly in alcohol delivery, while the rides business lags. DoorDash is not far behind, with a market capitalization around $60B following a successful mid-pandemic IPO, earlier this week they bought a salad robot.

All of this comes just one year after Grubhub’s CEO penned a letter to shareholders that read like a death knell for the industry, citing rising costs and “promiscuous” diners. Have the markets lost their mind, or is something fundamentally different in a post-pandemic world?

While the pandemic has driven unprecedented demand and introduced new narratives, the facts remain largely unchanged – the third party delivery industry is bad for independent restaurants, bad for delivery workers, and serves customers who are indifferent so long as their food arrives. The pandemic has brought these harsh truths irreversibly into the light, and it is for this reason that we will look back on this year not as one of good fortune for third party delivery, but as the beginning of the end.

How did we get here?

The history of business is in many ways the story of the integration and disintegration of value chains. Netscape founder Jim Barksdale famously quipped “Gentlemen, there’s only two ways I know of to make money: bundling and unbundling.”

In an integrated value chain, one firm directs many or all of the activities required to deliver value to the customer, which results in tight control over the final product and, with differentiation, higher profits. In a modular value chain, many firms compete to provide the same services, which results in greater flexibility and customization but lower profits for participating firms. I highly recommend Ben Thompson’s work on the subject for further reading, which modernizes Clay Christensen’s original work in The Innovator’s Solution.

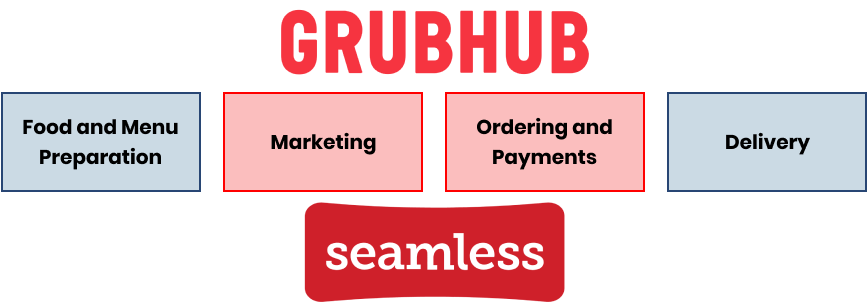

The past twenty years of the on-demand food delivery ecosystem is one long story of integration. In the interest of clarity, I’ve simplified the food delivery value chain to the steps of food and menu preparation, marketing, ordering & payment, and delivery.

In the beginning, there were a few menus in your kitchen drawer. You called to order, the restaurant took the order over the phone, prepared the food, delivered the food, and you paid in cash when they arrived. I can still remember the phone number of New World Pizza in Skillman, NJ.

The diagram below represents the value chain before third parties played a meaningful role in delivering value to the customer. All of these functions were likely coordinated by the proprietor.

The modern era of online ordering and delivery began around the year 2000, with Seamless (1999) and Grubhub (2003). In an effort to bring the menu in the drawer online, these firms created an online ordering and payment platform, and charged restaurants a commission of ~15% to receive orders through the platform. They focused on restaurants that already had in-house delivery capabilities, bringing the worlds of pizza and Chinese food online for the first time.

In 2013, Grubhub and Seamless merged and settled into life as a mature public company, seeing solid growth and consistent profits. It did not last. The very same year Doordash (2013) was founded, followed by UberEats (2014). This new breed of companies drew inspiration from the early wins of ridesharing, and adopted a similar playbook – they capitalized on broad adoption of personal mobile devices, a loose interpretation of labor laws, and mountains of venture capital to build distributed logistics networks.

These firms integrated delivery capabilities with a mobile-first online ordering and payments experience, introducing the fully integrated value chain we know today. To say nothing of the ethics or profitability of their execution, it is hard to argue with the strategic acumen of these firms in executing disruptive innovation on multiple fronts.

Clay Christensen describes two types of disruptive innovation, one in which a new entrant brings new customers into the market, and another in which a new entrant captures the low end of the market at a lower cost. These firms did both.

By integrating delivery capabilities into the food delivery value chain, restaurants that did not have delivery capabilities were now able to deliver via UberEats or Doordash, at times against their will. Nonetheless, they were successful in growing the new market by unlocking new supply and opening up new geographies.

At the same time, they executed a low end disruption to take existing market share away from Grubhub. By leveraging independent contractors rather than restaurant employees, they pitched a lower cost of delivery to restaurants. This was achieved by sharing delivery workers between restaurants, paying below minimum wage with no benefits, forcing workers to buy their own equipment, and stealing tips. This reduction in cost encouraged restaurants to fire their delivery employees and deepen their reliance on third party delivery.

The integration of the food delivery value chain has come at a cost to restaurants. In order for DoorDash and UberEats to enjoy attractive profits for themselves, they take them from restaurants. After all there is only so much profit to go around on a cheeseburger with free delivery.

Independent restaurants are all but powerless to negotiate fees, as many have relinquished their own proprietary ordering, payments, and delivery systems to work with these platforms. The platforms feel no need to negotiate, confident that if one restaurant leaves, another will take its place to satisfy a hungry diner.

It is for this reason that in 2020, when the COVID-19 pandemic hit, nearly every restaurant in America paid a 30% tariff to the third party delivery overlords, and what was already a bad deal became unbearable.

Bad to the bone

The case for the downfall of third party delivery begins and ends with the business model. Peter Drucker refers to a business model as “assumptions about what a company gets paid for.” Today’s third party delivery operators make the following assumption:

Restaurants will pay 30% of revenue for new customers, serviced by a third party delivery network.

This sounds reasonable. A few extra meals a night to new customers would better utilize existing resources and make the restaurant more profitable. A nice story, but not true.

While sales representatives from DoorDash and UberEats tell restaurateurs they are paying for new customers, in reality they know they will also be charged 30% to service existing and repeat customers, too. Industry data first shared with Expedite suggests that more than half of the orders placed on third party delivery platforms today are from repeat customers.

While third party delivery has always been a bad deal for restaurants, delivery did not represent a significant share of most restaurants business prior to 2020, and so the damage to a restaurant’s bottom line was obscured. The pandemic has brought an inconvenient truth into focus: third party delivery will kill your business if you let it, and third party delivery operators do not care.

How could third party delivery kill your business while bringing customers in the door? The model below shows a P&L for a restaurant that does ~$1M in sales annually at a 15% EBITDA margin, this would be considered very good by any standards. As you can see at the top, as third party delivery takes over more of the business, the business becomes incrementally worse. In this case, third party delivery begins to kill the business as soon as they reach 50% of revenue––sooner if you want to draw a salary, repair equipment, or pay back investors.

During the pandemic, many restaurants have gone from doing ~20% of their business through third party delivery platforms to ~80%, and watched their income statements turn from black to red, as fees ate their business alive. The message from third-party operators? Too bad.

The full model is available here so you can play with the assumptions yourself.

Unfortunately, this isn’t theoretical. The numbers above are roughly based on my friend Chef Adam Volk’s Redcrest Fried Chicken. In 2020, as his business shifted to mostly delivery he watched his previously profitable business consistently lose money, despite record sales volumes. Fortunately he was able to reduce the dependency on third party platforms before it was too late.

This is not news to sophisticated restaurant operators like Chipotle, who told investors in October that third party delivery is not profitable for them. They have something independent restaurants do not – leverage. To add insult to injury, it is a poorly kept secret that large multi-location restaurants like Chipotle, McDonalds, Shake Shack, and others pay lower fees than independent restaurants.

John D. Rockefeller used the same tactic, preferential rate agreements with railroads, to make it impossible for independent oil refiners to compete with Standard Oil. By 1880 they would refine over 90% of the oil produced in the United States and reap monopoly profits. Remember this the next time your favorite taqueria, burger joint, or pizza shop charges more for delivery – the system is calibrated to destroy them.

Arming the rebels

Drucker also notes that when firms fail to update their assumptions, they die. They die because even disruptors are open to disruption. When incumbents fail to deliver good service at a fair price to their customers, someone else will.

The initial disruptive innovation that captured the market for Doordash and UberEats was an integrated value chain from ordering to delivery. Fortunately for restaurants, the industry has come a long way. A value chain that once depended on tight integration to deliver value today stands on the precipice of becoming modularized once more, thanks to the technology enabled interfaces advanced by incumbents.

While online ordering platforms like Olo (2005), Chownow (2011), and BentoBox (2013) have been in the market for years, only recently have they emphasized integration with third party delivery capabilities, making them a substitute for third party ordering systems. This pandemic year has also brought into the public consciousness that ordering directly is the right thing to do for restaurants, and as the user experience continues to improve you can expect to see conscious diners make this easy choice.

New entrants like GoParrot (2016), Lunchbox (2019), and Bikky (2020) are combining traditional online ordering with sophisticated CRM and marketing automation that helps keep diners engaged and loyal. With this technology, restaurants can not only capture direct order volume, but convert customers from third party to first party ordering. Paying 30% of sales for a new customer is tolerable, paying 30% in perpetuity is not, and thanks to these firms it is now an option.

The next piece of the value chain to be modularized and commoditized is delivery. Charging a percentage of order value makes no sense, and is incongruous with any other logistics business. Could you imagine an e-commerce brand paying USPS 30% of their revenue to ship a package? Fortunately, the United States has a robust and competitive shipping landscape and the freedom to choose between FedEx, UPS, USPS, and DHL, driving fairly efficient competition and reasonable prices, and unexciting margins (and multiples) for these firms.

This is the likely outcome for food delivery, and the transformation is already underway. Firms like Relay and Lyft are happy to provide logistics only services, and do so for significantly lower fees. I expect to see a resurgence of locally owned and operated delivery players that can benefit from the readily accessible order APIs and continued commoditization of once proprietary fleet routing and management software.

As restaurants partner with these new entrants to optimize their businesses, the goal isn’t to kill third party platforms, but to put them in their right place and use them for what they were intended: attracting new customers on the restaurant's terms. The impact of course will put strain on their already bad economics. Whether or not these firms can survive in their current incarnation is unclear, as the economics are distorted by massive operating losses temporarily hidden by pandemic windfalls and mountains of venture capital.

It will take time for broad adoption of these new platforms, but the conversation is underway in every kitchen in America. I know this because I have seen it first hand. Redcrest Fried Chicken was able to pick up 20% of EBITDA by transitioning to a technology stack including GoParrot, Bikky, and Relay to shift repeat business away from the usual suspects. In a matter of one month they went from (5%) to 15% EBITDA, it was the matter of life and death.

It is clear that UberEats and DoorDash don’t plan to stay flat footed, but they lack a strategy to win in the new reality. Both firms are promoting storefronts for restaurants to compete with pure-play ordering platforms, and DoorDash is promoting a logistics only delivery service. By entering the fray in commoditized markets within the value chain, they are undermining their own ability to reap attractive profits. In the words of Clay Christensen, “either disruption will steal its markets, or commoditization will steal its profits.”

Do you know how fast you were going?

A discussion on this topic would not be complete without acknowledging the elephant in the room, which is that restaurants and delivery workers hate these companies. I have never seen an industry so hated by its most important stakeholders. Kara Swisher boldy made this point to Uber CEO Dara Khosrowshahi on her podcast, to which he responded “I will consider it my job to have you talk to a restaurant owner who’s happy with us in the next couple of years.” Yikes.

The resentment of these companies is not idle, it matters. It matters because it is motivating hundreds of thousands of restaurants to seek out new solutions to reduce dependence on third parties, and go to great lengths to educate their customers. The email below is one example.

It also matters because public sentiment is emboldening politicians at the state, city, and soon federal level to take action to protect vulnerable populations of workers and small businesses. The gears are already in motion for 2021 to be a decisive year for legislation that will increase the cost of doing business for third party delivery operators, putting money back in the pockets of independent restaurants and delivery workers.

Lawmakers from Rhode Island to California are making moves to ban third party delivery platforms for listing restaurants without their permission. A practice that Grubhub’s own CEO described as bad for everyone, just months after they were busted for parking 29,000 domains corresponding to restaurant names in a bizarre overreach. This increases costs for restaurants because, while it feels insane to even write this, it means they have to spend time and money gathering consent from restaurants to join their platforms.

At this point most major cities (New York, Chicago, SF, DC, Seattle) have begun to impose caps on third party delivery fees in the neighborhood of 15%, some of which will expire post-pandemic, though I suspect many will not. This is a direct response to the restaurant industry’s cry for help this past year and the cold indifference from third party delivery operators, in some cases offering fee deferrals with cruel terms.

Lastly we come to the delivery workers themselves, whose treatment is frankly an embarrassment for this country. These essential workers have been left to fend for themselves in a global public health crisis without training, PPE, paid sick leave, health insurance, or workers compensation insurance. In the words of one delivery worker, they are treated like “insects.” They are not insects, they are human beings with hopes and dreams and families and they are risking their lives to bring you dinner.

Gig economy companies have gladly leaned into the leniency of a Trump Department of Labor, but I suspect the Biden Administration along with a cast of progressive mayors will help to raise the floor for how we treat workers in this country, and the cost will be borne on their employers, gig or not. I am confident that in time we will reflect on our failure to protect these workers with deep shame as an industry and as a country.

Uber CEO Dara Khosrowshahi has called these attempts at regulation “misguided”, and he might be right. However, when you consistently do the wrong thing by your customers, regulators will tell you how to run your business, and your customers will cheer them on. This is what a functioning democracy looks like.

Adapt or die

From the time I was 15 until I graduated from college, I worked on and off in food service – server, caterer, bartender, barista, you name it. One-third of Americans worked their first job in a restaurant. One-third of all Americans have a shared story of learning how to work hard with no ego, appreciating diverse perspectives, and getting a first look at how a business works.

The 500,000 independent restaurants and bars in the country are a holdout of local entrepreneurship in a world that is becoming aggregated. Independent restaurants reflect local values and culture, nourish communities, and sustain working families, employing over 11M workers. Independent restaurants to me represent the wide-eyed, bright-burning, entrepreneurial fire that is so uniquely American and is accessible to everyone. But, it is a fire that will die if it is deprived of oxygen.

I am optimistic. While some restaurant owners may lack the pedigree of their venture backed third party “partners,” restaurateurs are some of the most tenacious, resourceful, and creative people you will meet in business. They can’t unsee the damage being done to their businesses, they won’t forget the indifference of these platforms to their cries for help, and they will not take their slated disruption lying down.

The pandemic has accelerated the reimagining of independent restaurants and food creators as brands with valuable audiences and communities, and new platforms are emerging to help them to reach their customers at scale with recipes, cooking classes, frozen meals, and meal kits. I am excited for the future of independent restaurants, and hopeful that we will view the pandemic as the time that they reclaimed the power that was always theirs. As the weather warms and our nation reopens, it is third party delivery firms who will need to adapt or die.

Note from Dan: Thanks James Gettinger, Christian Lewis, Rachael Nemeth, Dave Ambrose, Sarah Quirk for encouragement and editing.

The author is an investor in Bikky, Redcrest Fried Chicken, Food Supply Co, and Mosaic Foods.

Thanks for listening,

Packy

Share this post