Welcome to the 928 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 10,185 smart, curious folks by subscribing here!

Hi friends 👋,

I want to celebrate Ten k subscribers by going deep on the only company with the right name for the occasion, Tencent.

Tencent is the Chinese conglomerate behind the recently-banned WeChat, and one of the world’s most successful investment funds. There’s so much to say about this company that I’m breaking it up into two parts:

Part I (today): Tencent’s history, its business, and its portfolio, including a bonus goody for the investing nerds out there: a link to a spreadsheet I made with the current value of 102 of Tencent’s investments.

Part II (Thursday): Where Tencent is headed - it’s building new cities in China, and it’s going to be at the center of building a whole new world.

This post isn’t meant to be political or to pass value judgments. It’s just an assessment of a fascinating company that most of us know far too little about.

Favor: if you enjoy this post, please click the little heart button to like it - it helps more people discover my writing - or share it with your most Sinocurious friend.

Let’s get to it.

Tencent: The Ultimate Outsider

Tencent is the most important company that many Americans know the least about.

When President Trump signed an August 6th Executive Order banning WeChat from the United States, a lot of people said, “What’s WeChat?” Even those who knew about WeChat know very little about the octopoid company behind it.

Let’s fix that. You should leave this two-part essay with a better understanding of what Tencent does, what it owns, and why it’s one of the most significant companies in the world.

The Chinese pager-based internet service that Pony Ma launched in 1998 is now the world’s seventh most valuable company, right ahead of Berkshire Hathaway and right behind its bitter rival, Alibaba. As of Friday, Tencent is worth $628 billion.

In China, Tencent is like Facebook, Nintendo, Shopify, Netflix, Spotify, Slack, and PayPal rolled into one. Its flagship product, WeChat, has 1.2 billion users, and those users spend more time in the app every day than Americans spend on all social media apps combined. People use WeChat to message friends, shop, read the news, play games, pay for things in physical stores… pretty anything you can do on your phone, you can do on WeChat.

Tencent turned the profits from its social networking, ecommerce, and gaming cash cows into a global investment portfolio that includes many of the world’s most popular video games, the fastest-growing internet businesses in China, meaningful stakes in Tesla, Spotify, and Snap, and a portfolio of international startup unicorns second only to Sequoia’s. It even financed A Beautiful Day in the Neighborhood.

Americans don’t know much about Tencent because, in addition to being Chinese, it’s really fucking complex. It’s both one of the most profitable operating businesses in the world and one of the most ambitious investment funds. Tencent has been dubbed “The SoftBank of China” and “The Berkshire Hathaway of Tech.” Neither description does it justice. While it gets less hype, its performance puts SoftBank’s to shame. It’s going to be one of the most important companies in the world for decades to come.

Today, in Part I, I’m going to explain Tencent in four sections:

What is Tencent? An entrepreneurial story just like the ones you hear in the US, with all of the highs, lows, and near-deaths. An improbable journey from pager-based internet service to the giant holding company it is today.

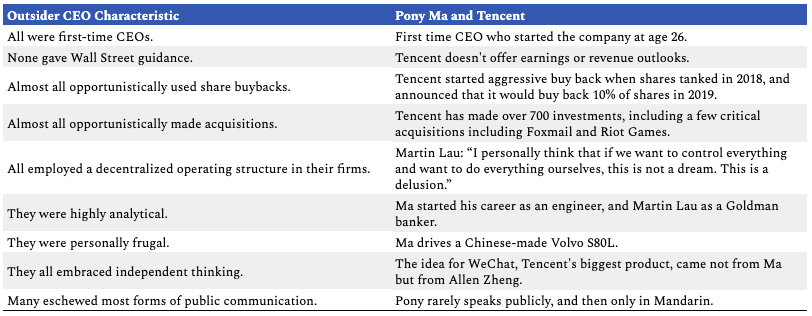

The Outsiders. William N. Thorndike’s 2012 book, The Outsiders, about eight of the most successful CEOs in US history, provides a framework for thinking about Tencent’s business. CEO Pony Ma shares all of the important characteristics with the eight that Thorndike wrote about.

Tencent’s Operating Businesses. Tencent’s core business makes money in six main ways, and each of its business units rivals in, both scope and revenue, massive, standalone public companies.

Tencent’s Investment Portfolio. There’s no great public source for all of Tencent’s 700-800 investments, so I created a database of 103 of its biggest and share insights around where it invests, in which types of companies, and the unfair advantages it has as an investor.

The founding stories of Apple, Google, Microsoft, Facebook, and Amazon are canon for the type of people who read Not Boring. They’re part of modern American mythology. It’s time for us to get to know Tencent.

What is Tencent?

Note: I’ve used Julia Wu’s summary of Wu Xiaobo’s book, Matthew Brennan’s presentations, and the excellent Acquired podcast on Tencent to piece together Tencent’s history.

We’ve been conditioned to think of massive Chinese technology companies as shady, government-controlled businesses out to steal your data and try to take over the world. It might surprise you, then, that Tencent started out like a lot of US startups: as an entrepreneurial itch that one 26-year-old nerd had to scratch with the help of some friends.

Ma Huateng was born at the right time and moved to the right place. Ma was born in the Hainan province in 1971 and moved to Shenzhen when he was 13. In the late 1970s, Chinese President Deng Xiaoping designated Shenzhen as a special economic zone as part of his “reform and opening policy.” Ma, whose family name meant “horse” and whose nickname, appropriately, was Pony, grew up in the one capitalist place in communist China.

Ma was prodigiously smart. He scored high enough in college entrance exams to go anywhere in the country, but stayed close to home, attending Shenzhen University. The school didn’t have the astronomy major that Ma was most interested in, so he settled for his second choice: computer science. He was a natural.

Ma regularly won student hacking contests, and built graphical user interfaces before they were a thing in China. While interning at one of China’s leading tech companies, Ma built a stock market analysis tool with a GUI as a side project, and sold it to his employer for 50,000 Chinese Yuan (CNY), or about 3 years’ salary.

If this were a novel, the fact that Pony Ma’s first product combined tech and finance and his first taste of wealth came from an M&A transaction would be called foreshadowing.

After college, Ma spent five years at a pager company, where he was exposed to the latest technology (pagers!) and became a manager. But Ma was living a second life in the early online chatrooms. He joined the growing FidoNet community, participating in and then hosting early internet bulletin board systems, where he met future billionaires like Xiaomi’s Lei Jun and NetEase’s Ding Lei.

Inspired by Lei’s early success with NetEase (which today is worth $65 billion), in 1998, Ma left his job and convinced his friend, Zhang Zhidong, to start a company with him. They planned to combine the internet and pagers, which were popular in China at the time, to build a mobile internet on which people could send email, news, and more.

Sticking with Ma’s equestrian nomenclature, they named the company Tengxun, which means “galloping message.” Tencent is the anglicized version of Tengxun.

As Tencent was building its pager-based internet, Ma noticed the Israeli internet communication tool and Instant Messenger competitor ICQ, which sold to AOL in 1998, and decided to build a version for the Chinese market. Creatively, he called it OICQ, and built distribution and features necessary to serve customers who didn’t own personal computers, but increasingly accessed them in internet cafes.

OICQ took off, and Tencent abandoned the pager internet. Users quadrupled every three months. After nine months, OICQ hit one million users. But this was pre-AWS (or Tencent Cloud) and servers were expensive. Plus, AOL sued Tencnent to change OICQ’s name. They were running out of money, so Ma launched a dual-track process to either sell the company or raise money.

Tencent was aiming for 3 million yuan in a sale ($431k at today’s exchange rate), but the highest offer it received was for 600k yuan ($86,327). The lack of demand turned out to be a pretty lucky break. Today, it’s worth 1,454,929x its 3 million yuan asking price.

With no acquirer, Ma sold 40% of Tencent to early US-based Chinese venture investor IDG Capital and Yingke, a fund led by Chinese billionaire Li Kashing’s son, for $2.2 million. But it wasn’t out of the woods.

Soon after, AOL won its lawsuit, forcing Tencent to change the name of its flagship product. It chose QQ. Server costs continued to increase as the company crossed 100 million users with no revenue model. Tencent was back on the market. It approached Chinese search company Sohu and Yahoo! China. Neither was interested. Then, in 2001, the South African firm Naspers (literally) walked in the door and offered to invest at a $60 million valuation. So that Ma didn’t lose majority ownership, IDG sold 12.8% of its 20% and Yingke sold its entire stake for an 11x gain (not bad!), giving Naspers 32.8% of the company for $19.68 million. Today, that investment is worth $205 billion, good for a 10,436x return!

With Naspers’ money in the bank, the Tencent team turned its attention to monetization. In 2002, a product manager discovered the Korean company sayclub.com, which monetized by allowing users to create personalized avatars. Tencent built its own version, QQ Show, and within 6 months, the product had 5 million users paying 5 yuan (a little less than $1) per month.

As Julia Wu points out, the ability to personalize an avatar was such a hit because under communism, Chinese people had been “dull and collective” in their personal representation. Tencent also launched a “red diamond membership” for 10 yuan per month, for VIP status, monthly virtual gifts, and discounts in the QQ marketplace.

This is a really important piece to understand. In the US, as we talked about in If I Ruled the Tweets, social media monetizes through advertising. In Asia, it mainly monetizes through digital gifts, subscriptions, and purchases. To this day, “Value Added Services” generate more than 3x the revenue for Tencent than “Online Advertising.”

Avatars were big business. In 2003, Tencent hit a $100 million run rate and moved beyond messaging by building a portal, like a Chinese AOL. The team also realized that a lot of its users were chatting on QQ while playing games in internet cafes, so it added games to the QQ platform, both by acquiring small studios and building games in-house. Within a year, games added another $50 million in annual revenue.

With monetization booming, Tencent IPO’d in 2004 at a valuation of 6.22 billion HKD, or $790 million USD. Cue Motley Fool headline: if you had invested $10,000 in Tencent at its IPO in 2004, you would have $7.9 million today.

Oh, you didn’t invest in Tecent at its IPO? Damn. To be fair, it’s a very different company today than it was then, thanks to two 2005 hires: Martin Lau and Allen Zhang.

After completing its IPO, Tencent hired the Goldman Sachs investment banker who took it public, Martin Lau. Lau had the pedigree - Chinese-born, undergrad at Michigan, engineering masters at Stanford, and MBA at Kellogg - and a skillset that was complementary to Ma’s. Lau became the English-speaking face of the business, taking on a role that the shy Ma hated, and the master capital allocator. In the beginning of his tenure, Lau focused on acquiring studios to grow its scorching games business as the Chief Strategy Officer. By the next year, Ma promoted him to President.

Tencent also turned its attention to competitive threats to the portal business, including Microsoft’s increasing presence in China via MSN. To combat the threat, it acquired competitor Foxmail in 2005 to build QQ Mail. The product was successful, but more importantly, Tencent acquired the developer behind Foxmail, Allen Zhang.

With Lau and Zhang on board, Tencent grew rapidly via desktop games and the QQ platform. Its revenue jumped 15x from $200 million in 2005 to $2.9 billion in 2010. But 2011 was the year when Zhang and Lau really made their mark.

In 2010, early in the rise of mobile, Zhang noticed the popularity of Canadian messaging company called Kik, and convinced Ma to let him build a Chinese version for Tencent. The next seven years changed the trajectory of the company.

2011: Working around the clock with a small team, Zhang launched Weixin in January. English speakers know it as WeChat. (They’re actually two separate products - Weixin serves Mainland China and WeChat serves the rest of the world, but we’ll refer to the two interchangeably as WeChat.) After early competition with Xiaomi’s Mi Chat, WeChat pulled away by tapping into QQ’s existing user base, and then launching “Friends Nearby,” which was like an early version of Tinder. WeChat began adding 100k users per day.

2012: WeChat hit 100 million users. It took 433 days to hit that mark. By comparison, it took QQ ten years, Facebook 5.5 years, and Twitter 4 years. In April, WeChat launched the Moments newsfeed and Official Accounts, allowing publishers to distribute content and businesses to distribute products and services. By the end of the year, it had 300 million users.

2013: Tencent launched WeChat Pay to enable payment through the platform.

2015: WeChat crossed half a billion users.

2017: WeChat launched Mini Programs, allowing businesses to build full-functionality apps within the WeChat platform. Companies like Pinduoduo build on top of WeChat and tap into all of its customers’ existing social and professional networks. Mini Programs turn WeChat into a “super app,” and are the inspiration behind Snap Minis, which we covered in Oh Snap!. WeChat, for all intents and purposes, is the mobile operating system in China.

Back to Lau. While Zhang was building WeChat, Lau was busy acquiring games, laying the foundation for the next stage of growth. Two investments in 2011 and 2012 were particularly important. In 2011, Tencent acquired 92.8% of US game studio, Riot Games, creators of League of Legends for $400 million (they acquired the remaining 7.2% in 2015). The next year, in 2012, it acquired 40% of Cary, NC-based game company, Epic Games for $330 million.

Today, Epic and Riot are two of the gems in Tencent’s gaming portfolio. League of Legends is a cornerstone of a gaming division that brought in $5.5 billion in Q2 alone. As we will explore in “Tencent’s Future,” Epic may also be the engine (pun intended) that drives the next massive phase of Tencent’s growth and puts it at the center of a new, virtual world.

Over the past decade, Lau and his team have acquired or invested in over 700 companies, funded by the massive pools of cash Tencent’s gaming division and WeChat spit off.

WeChat has over 1.2 billions users today. And those users are incredibly engaged. WeChat users in China spend an average of four hours per day in the app, more time than US users spend on all social media apps combined.

Chinese users do everything on WeChat. They communicate with friends, co-workers, and clients through WeChat. Businesses communicate with customers through Official Accounts. They can also sell things through those accounts. Thousands of businesses, including ridesharing (Didi) and food delivery (Meituan Dianping), launched on WeChat. Tencent monetizes WeChat mainly through transactions instead of ads.

So putting it all together, what is Tencent?

Tencent is a Chinese holding company that is the world leader in gaming and runs the largest messaging, social networking, and mobile payments platform in China. It uses the cash flow from those businesses to invest in the next generation of massive companies in China and around the globe. Tencent combines the diversification of an old school conglomerate with the growth and decentralization of an internet-native business into a company that may become the largest in the world.

From its roots as a product company, Tencent has become the best capital allocator of any non-investment company in the world. It’s running The Outsiders playbook to perfection.

The Outsiders

In 2012, William N. Thorndike unintentionally wrote the guide to understanding Tencent’s dominance: The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success.

In it, Thorndike explores the things that eight CEOs -- including Warren Buffett, The Washington Post’s Katharine Graham, Teledyne’s Henry Singleton, and Capital Cities’ Tom Murphy -- did differently that made them more successful than their peers.

How does he measure success?

You really only need to know three things to evaluate a CEO’s greatness: the compound annual return to shareholders during his or her tenure and the return over the same period for peer companies and for the broader market (usually measured by the S&P 500).

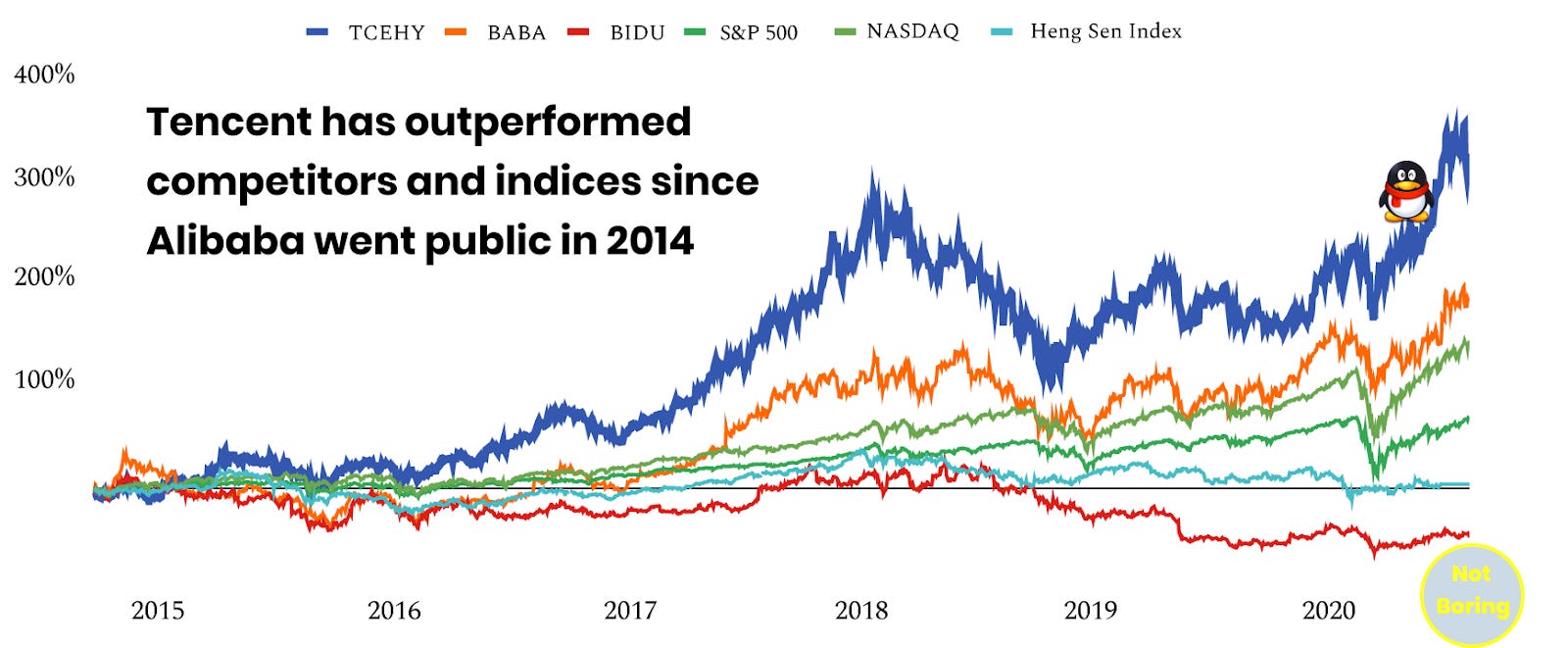

By that measure, Pony Ma has been one of the world’s most successful CEOs. Since Tencent’s biggest competitor, Alibaba, went public in September 2014, Tencent has returned 305% versus:

182% for Alibaba

-48% for Baidu

68%, 141%, and 10% for the S&P 500, NASDAQ, and Hang Sen Index, respectively.

Over the past six years, Tencent has outperformed the index that tracks the largest companies in Hong Kong’s stock market by 30x.

Why has Tencent outperformed? For the same reasons that Thorndike highlighted in The Outsiders eight years ago. Pony Ma and Tencent share the characteristics common among the most successful CEOs, and take some to extremes.

Outsider CEOs were private, ran decentralized organizations, and masterfully allocated capital to the opportunities, internal or external, with the highest potential to drive their stock’s performance. Pony Ma is the ultimate Outsider! As a result, he’s now China’s richest man with a net worth of $56.2 billion.

And the business that he built is a master class in capital allocation, as we’ll see by breaking Tencent down into its two main businesses, which often interact with each other: Operating Businesses and Investments.

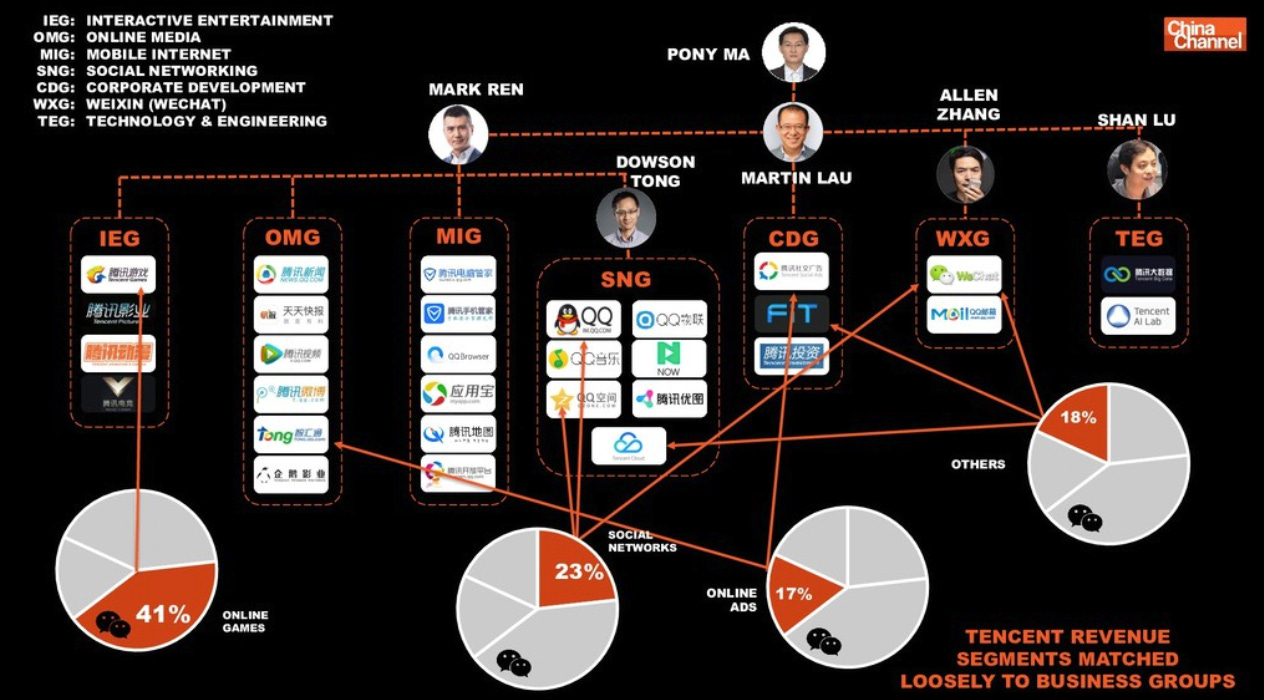

Tencent’s Core Businesses

Tencent’s core business makes money in six main ways:

Payments

Subscriptions (like video and music)

Social ads

Media ads

Games

Cloud

Here’s a breakdown of how revenue maps to business lines from a 2017 presentation by China tech analyst, Matthew Brennan:

All clear? Ok good, moving on.

JK, it’s super complex. Let’s break it down by looking at Tencent’s Q2 results, converted to USD:

Social Networks. Instead of ads, Social Networks includes Value Added Services revenue like subscriptions for video and music and in-game purchases. It has 114 million paid video subscriptions and 47 million paid music subscriptions.

Online Games. Games are Tencent’s biggest business. Tencent has 17 separate franchises that have exceeded 10 million daily active users, not including Epic Games’ Fortnite, in which it has a large, non-controlling stake.

Online Advertising - Media. It includes ads on Tecent Video’s properties, as well as in Tencent’s various other digital, news, and video media properties.

Online Advertising - Social and Others. This segment looks the most similar to US social media companies’ monetization. One of the biggest drivers is companies paying for ads in WeChat Moments, and analysts highlight the fact that WeChat still has a relatively light ad load and room to grow.

FinTech and Business Services. Tencent’s second largest segment, it includes all of TenPay, the largest online payments platform in China encompassing WeChat Pay and QQ Pay, as well as WeChat’s wealth management business. When consumers and businesses buy from businesses on WeChat, via Official Accounts and Mini Programs, the fee Tencent takes is captured here, as does the fee Tencent takes when people use WeChat Pay to pay offline and across the web.

FinTech and Business Services also includes its cloud business. Although it didn’t break cloud revenue out separately in Q2, it was a $2.4 billion business in 2019.

To give you a sense for Tencent’s scope and scale, here’s how Tencent’s business lines compare to entire industry-leading companies based on Q2 revenue.

Tencent’s Payments business is nearly as big as PayPal’s entire business, and it generated five times as much revenue as Shopify in Q2.

Its subscription revenue alone is 62% of Netflix’s.

It has some catching up to do in Social Ads, where it generates only 12% as much as the leader, Facebook, although it did generate more than 3x as much social ads revenue as Twitter.

Its small media ads business is bigger than the New York Times.

Games revenue is 64% higher than the world’s most valuable standalone gaming company, Nintendo.

Breaking cloud out of Payments and Business Services, based on last year ($600 million per quarter), it’s far behind AWS in cloud, with only 6% of the revenue.

It’s difficult to wrap your arms around Tencent, and as a result, the company likely trades at a discount to its more focused American counterparts. If you applied the same Q2 revenue multiples at which each of the businesses in the chart above is currently trading to the corresponding Tencent business segment, its operating businesses alone would be valued at $538 billion, 86% of the company’s current market cap.

And that’s before you get to the part of Tencent’s business that excites me the most, its expansive portfolio of investments.

Tencent’s Investment Portfolio

Did you know that Tencent owns 5% of Tesla, 12% of Snap, and 9% of Spotify (including a stake through Tencent Music)?

Those stakes are worth $15.4 billion, $3.9 billion, and $4.2 billion, respectively, and they barely scratch the surface.

In The Outsiders, Thorndike wrote, “CEOs need to do two things well: run their operations efficiently, and deploy the cash generated by those operations.”

In Q2, Tencent generated $5.4 billion in operating profit. Job 1: ✅

It’s how Tencent deploys the cash generated by those operations that’s so fascinating, though. Two of Pony Ma’s top lieutenants, President Martin Lau and Chief Strategy Officer James Mitchell, are ex-Goldman bankers. As one VC told the Financial Times: “When you put a basketball player in the room, you know what they’re going to do. If you hire Goldman Sachs bankers, you know what they are going to do.”

The analogy is a bit of a stretch, but the answer is clear: they’re going to do M&A. On its most recent earnings call, Martin Lau said:

Our M&A strategy has always been trying to invest in up and coming companies which have a great management, who have innovative products, and at the same time, they have synergies with our existing platforms. We now have more than 700 companies.

More than 700 companies!

There’s nowhere online to find all of Tencent’s biggest investments, their ownership stake, and the current value of the investments in one place… so I built it. I have only 103 of the 700 investments in there, but I think I have all the big ones, and it’s absolutely fascinating.

When you add the current value of just those 103 investments to the operating business value based on standalone business comps from the previous section, you land at a 15% higher valuation than Tencent is trading at today. The math is rough and not meant to be investment advice, but it’s helpful in thinking through how to build a complete picture of Tencent.

In Tencent’s Q2 earnings report, it mentions that the fair value of its investments in listed (public) investee companies, excluding subsidiaries (companies of which Tencent owns more than 50%), is $102.6 billion as of June 30, 2020. If you add that number to the $538 billion operating businesses value from the last section, you get $640 billion, almost exactly in line with Tencent’s current market cap of $628 billion.

So far, so good.

But that $102.6 billion is just part of the portfolio - the publicly listed non-subsidiaries. When you include investments in private companies, based on most recently announced valuations and some rough estimates, I get a current portfolio value nearly twice as big, at $187 billion. And that’s without 600 of the (likely smaller) investments that Tencent claims to have made.

Tencent is a really hard business to value accurately for a few reasons:

Just in its operating business, it does a lot of different things.

In addition to the operating business, it’s also a venture fund, a late stage fund, a private equity fund, and a hedge fund.

Startup outcomes are so unpredictable, even with Tencent’s muscle behind them.

But I have a sneaking suspicion that its venture investments are worth somewhere north of zero, so let’s take a closer look at its entire portfolio.

Where does Tencent invest?

Tencent’s investments are split fairly evenly between China and International.

Of the 103 Tencent investments I’m tracking, 54 are in China and 49 are international. Including acquired subsidiaries, the current value of investments by country break down like this:

Tencent uses the cash it generates largely in China to diversify away from China, which is particularly important given that, even with its largest companies, the Chinese government can be hard to predict. In 2018, for example, a government game review process slowed the growth of Tencent’s gaming business in the country and tanked its stock over 20%.

Just this morning, it announced an investment in French gaming company Voodoo, and gaming analyst Daniel Ahmad pointed out that Voodoo’s ad-based games would get around Chinese regulations requiring reviews of any games that monetize through in-game purchases.

What does Tencent own?

Tecent’s largest holdings include investments in some of the largest and fastest-growing gaming, music, and technology companies.

Tencent’s top 10 holdings span:

Familiar names like Tesla and Snap,

Chinese ecommerce giants Meituan Dianping, JD.com, and Pinduoduo (Turner Novak on Pinduoduo)

China’s largest digital bank, WeBank,

TikTok competitor Kuaishou,

Beike, a Chinese Zillow which just went public last week in the largest US IPO of a Chinese company since early 2018,

Sea Ltd, the Singaporean gaming, ecommerce, and payments company that looks like the Tencent of SE Asia (Julie Young on Sea)

Epic Games, the US gaming company, Fortnite creator, and owner of the Unreal Engine (Matthew Ball on Epic Games)

By my count, Tencent has 83 companies worth more than $1 billion dollars in its portfolio. 52 are unicorns, private companies worth $1 billion, which places it in the number two spot right behind #1 Sequoia Capital, which has invested in 109 according to the Hurun Global Unicorn Index, and ahead of third place SoftBank, which has 51. (In a January speech, Lau said that that company has 160 companies in its portfolio worth more than $1 billion, which would put it #1.)

At home, Tencent’s biggest investments are in ecommerce, and it plans to double-down on “smart retail” given the success of its WeChat Mini Programs. Abroad, almost half of the value of the portfolio is in gaming companies. In both its Chinese and international strategies, Tencent has unfair advantages, and those advantages shape what types of businesses the company invests in.

How do they do it?

China

Businesses in China run on WeChat. They can communicate with customers on Official Accounts, get distribution through group chats, build entire functioning products with Mini Programs, and accept payments through WeChat Pay. WeChat is Tencent’s unfair advantage in China. It’s the top of Tencent’s acquisition funnel.

Three of Tencent’s four largest holdings - Meituan Dianping, JD.com, and Pinduoduo - are Chinese ecommerce businesses that run on top of WeChat. Tencent uses data from WeChat to source investments, and then provides preferential placement to its investees’ Official Accounts and Mini Programs within WeChat.

For example, when Tencent invested in JD in 2014 to take on Alibaba’s Tmall, Reuters wrote:

The deal gives JD.com a headline slot on Tencent’s WeChat app that dominates China’s smartphones, an entry into eBay-style consumer-to-consumer shopping and a backer with the muscle to help it make the most of a logistics infrastructure that Alibaba lacks.

Today, Tencent’s investments in JD.com, Meituan Dianping, and Pinduoduo are worth $68.5 billion.

No one else has the transaction data or the ability to boost a company’s distribution the way that Tencent does with WeChat. This will continue to be an advantage - in just three years, there are over 1 million WeChat Mini Programs. Tencent can cherry pick the best, invest, and practically guarantee their success.

International

Whereas Tencent’s China portfolio is top-heavy with ecommerce unicorns, its international portfolio includes everything from an 86-year-old American music label, Universal Music Group, to 7-year-old Brazilian neobank, Nubank.

Its’ biggest investment category, though, is games. It owns stakes in the companies behind popular titles including League of Legends (Riot Games 100%), Fortnite (Epic Games, 40%), Clash of Clans (Supercell, 81.4%), PUBG (Bluehole, 10%), Path of Exile (Grinding Gear Games, 80%), Call of Duty, Overwatch, Starcraft, and Candy Crush (Activision Blizzard, 5%). It even owns 1.3% of Roblox, which lets kids build their own games, and 2% of Discord, a chat platform used mainly by gamers.

Tencent invests in international game companies and distributes their titles to the Chinese market. This is Tencent’s unfair advantage: companies essentially need to partner with Tencent or Alibaba to operate in China.

This is true beyond games, too. The Canadian version of Dunkin Donuts, Tim Hortons, wants to expand into China, so it recently took on an investment from Tencent. Tencent invested in Universal and Warner Music Group in part to control the licensing of their catalogs in China.

In addition to strategic investments in games and music, Tencent makes venture-style investments in fast-growing companies that have the potential to win large markets. It has shown a particular affinity for non-gaming investments in India, the only other country with as large a population as China’s. It has invested in ecommerce standout Flipkart, transportation unicorn Ola, education startup Bydu, food delivery app Swiggy, and fintech darling Khatabook, among others.

In the US, Singapore, and Indonesia, it has invested in the companies building super apps most similar to its own core product, WeChat -- Snap, Sea, and Gojek.

Tencent’s international portfolio is large, diverse, and complex, with bets at all stages, in all categories, and for all sorts of reasons. As a result, I think that investors undervalue it. But while the world catches up, Tencent keeps zooming further into the future. The real magic in the portfolio is just beginning to bloom. It’s that future that has me most excited about the company.

Tencent’s Future

We’ve gone on quite a journey today, covering Tencent’s history and what it’s up to today, including its core operating businesses and how it invests the massive profits that those businesses generate to participate in the internet’s growth at home and around the world.

In Part II on Thursday, we’ll get our crystal balls out and talk about what Tencent’s investments tell us about the future, and how the company has positioned itself to sit at the center of the next world: the Metaverse. That means we get to explore some hairier subjects, like the influence of the Chinese Communist Party, Epic’s fight with Apple, the threats to its current business and long-term mission, and much, much more.

Thanks Dan and Puja for editing, Sid for input, Turner for investment accounting help, and Julia Wu, Matthew Brennan, Ben Gilbert, and David Rosenthal for excellent background info.

Thanks for listening,

Packy