Tegus: The Outsiders

Meet the under-the-radar $3 billion company modernizing investment research

Welcome to the 645 newly Not Boring people who have joined us since Monday — I need to take breaks more often! If you haven’t subscribed, join 155,188 smart, curious folks by subscribing here:

🎧 For the audio version, click the play button up top or listen on Spotify or Apple Podcasts

Today’s Not Boring, the whole thing, is brought to you by… Tegus

Not Boring readers can try Tegus for free. Sign up by clicking this button to explore expert calls on hundreds of companies like Stripe, SpaceX, Meta, Anduril, Amazon, and more.

Hi friends 👋,

Happy Thursday!

As someone who uses Tegus whenever I begin researching a new company to write about, I’m really excited to bring you the first inside look at the company ever written.

It’s clear from talking to the team, and from looking at the numbers, that this is a special company that is going to be around for a long time. It’s also the perfect company to study right now, in a market that once again values free cash flow, strategic chops, and smart capital allocation.

This essay is a Sponsored Deep Dive. You can read more about how I choose which companies to do deep dives on, and how I write them here.

Let’s get to it.

Tegus: The Outsiders

It feels almost disrespectful to call Tegus a unicorn. Too fluffy.

Sure, the five-year-old company has all the markings of the mythical creature:

$3+ billion valuation as of its Series B in November 2021 (it’s since raised another round at an undisclosed valuation)

195% year-over-year ARR growth off of a very meaningful base

Over 2,500 customers

Nearly 700 employees

The company’s Series A, led by the Investment Group of Santa Barbara at a $4.5 million post-money valuation, is already one of the best venture investments I’ve come across. IGSB’s $1.5 million investment is already worth around $1 billion on paper, assuming they still hold that entire position. That’s good for a ~350% IRR as of the company’s last announced round in November 2021.

If those numbers belonged to nearly any other company, you would have heard about them on Twitter. There would be cover stories written, highlighting brother co-founders Tom and Mike Elnick.

Instead, this is the first time the Tegus story has really been told publicly. This is what you get when you search “Elnick” in Spotify podcasts:

If you’re a religious Invest Like the Best listener like I am, you’ve known about Tegus for a few years, but besides a few targeted ads, Tom and Mike have eschewed the spotlight in favor of a maniacal focus on finding genuine product market fit (PMF) with an intentionally narrow set of users.

They’ve “gone slow to go fast.” Which makes sense, because unlike the typical unicorn founders, Tom and Mike aren’t coders, they’re distance runners. And their discipline, patience, and pacing shine through in every aspect of the business.

Tegus is building the modern investment research platform for fundamental private and public market investors, starting with a novel twist on the classic expert call model, and expanding into adjacent opportunities by listening intently to customers.

Yes yes, every company says that they listen to customers, but as Tegus CFO Bob Casey put it, “If the CEO’s calendar is indicative of what’s most valuable in an organization, Tom and Mike’s calendars overwhelmingly point to customer obsession.” Before emailing me on Sunday, Casey checked Tom and Mike’s calendars for the week, and counted 14 customer calls between Monday morning and Wednesday afternoon. Casey himself has 20 customer meetings lined up when he’s in NYC next week.

That’s just one of many anecdotes that hint at Tegus’ unique approach. Learn how Tegus got here, and how it thinks and behaves today, and you’ll realize that it’s different than the typical Silicon Valley success story.

For one thing, the company is free cash flow positive, and has been for years, even before it was cool. It’s also built for the long-term, with an eye towards doing this for decades that comes through in every decision the company makes. Tom and Mike have studied Hamilton Helmer’s 7 Powers and Will Thorndike’s The Outsiders more than anyone besides maybe Ben and David at Acquired, and they’ve put the lessons to work:

7 Powers: building a business with sustainable differentiation, which leveraged counter positioning in the early days and enjoys scale economies today

The Outsiders: smart capital allocation, as evidenced by the fact that, in just five years, the company has already done a share buyback and three acquisitions, including BamSEC and Canalyst

Tegus is a business that combines the pace of a startup with the maturity of a more established company. It reminds me of the companies that fintwit loves, the ones you haven’t heard a lot about that are just spitting off cash, allocating capital wisely, with strong management teams at the helm. With markets turning, profitability and sound strategy back in vogue, and real, recurring, defensible revenue at a premium, Tegus is the perfect company for entrepreneurs and investors alike to study.

So let’s study Tegus. Today, we’ll pull back the curtains to cover:

The Course to Tegus

Modernizing Investment Research

The Tegus Business Model

The Outsiders: Fundraising, Buybacks, and Acquisitions

When I asked Mike what he was hoping readers get out of this piece, he told me:

For a long time, we’ve been very misunderstood, and we’ve been thrilled to be misunderstood. 10 out of 10 times we would have chosen to be under the radar. But now we have 2,500 customers, and we can’t skirt through the rest of the company’s life without telling our story.

🫡 It’s time to tell the Tegus story.

The Course to Tegus

Tom and Mike Elnick grew up on Long Island with chips on their shoulders.

“We were so competitive with each other,” Mike told me, “because we wanted to prove our doubters wrong through our own competitive process.”

The result was, as the first in their family to go away to college, they ended up at an Ivy, Brown University, where they ran track and cross country. Mike went shorter, running the 800, and Tom went longer, to the 5k. They met in the middle racing the mile, where Tom bested Mike with a PR of 4:08 to his brother’s 4:12.

Whether they ran because of who they were, or whether running shaped them into who they are, the sport’s footprint is all over the brothers and the company they’ve built. “There’s this notion of ‘you gotta keep on training,’” Tom explained. “You can have a bad race, but you still have to put in your 70 miles every week.”

After school, Tom and Mike split for the first time. Tom went to work for Overbrook Management, a value oriented long/short hedge fund, as an Analyst. Mike went to expert network startup AlphaSights as one of its earliest employees. In those roles, they saw the inefficiencies of the investment research process from both sides, and it bugged them.

Not enough to start a company – they were risk-averse – but enough to start asking around. When they asked other investors about their research process, they’d get agreement that the process wasn’t as smooth as it could be, followed inevitably by a: “But that’s just the way it is.”

As competitive people, hearing “but that’s just the way it is” over and over again lit a fire and pushed them, hesitantly, into entrepreneurship. On September 11, 2015, Tom and Mike quit their respective jobs and teamed up once again, not to start a company necessarily, but to talk to as many investors about their process as possible to see if there might be a way to change the way it just was.

Modernizing Investment Research

There are many different ways to invest: quant funds, macro funds, event-driven funds, high-frequency funds, all flavors of funds. Tom and Mike were focused on speaking with investors at funds doing fundamental research, those trying to understand the businesses in which they invest more deeply than anyone else in order to develop a differentiated view on their value. As examples, current Tegus customers include ShawSpring Partners, Thrive Capital, Octahedron, Accel, Mission Holdings, Redpoint, O’Shaughnessy Asset Management, and IGSB, all funds whose investors I respect for their insightfulness.

A lot of inputs inform those funds’ views, but generally, there are three core elements that all fundamental investors focus on:

Qualitative Research: understanding how the business works

Previous Performance: using company filings to understand a business’ financials

Models: building models to analyze a business under various scenarios and assumptions

The existing process – which uses a mix of Bloomberg, CapIQ, FactSet, GLG, AlphaSights, Edgar, S&P Global, and a menagerie of other data sources – works well enough to elicit “that’s just the way it works” responses, but it’s time consuming and expensive. Analysts at investment funds are among the highest-paid professionals in the world, and they can spend up to two-thirds of their time finding, aggregating, and manipulating data. That leaves less time for analysis and creativity, the things that actually justify the big bucks.

So when Tom and Mike set out to figure out what was wrong with the process, they focused on what they believed the biggest mismatch was between how valuable something was and how painful it was to access. That mismatch was the largest in primary research, so they started by focusing on that gap first. They also loved that it was probably the hardest thing to tackle; no one who studies this space had been able to build a disruptor.

Primary research, tracking people down and asking them questions, could take a week or more between finding the right person to talk to, setting up a call, having the call, taking notes, and synthesizing them. Plus, the incumbents left a lot of room for improvement, as Mike saw first hand at AlphaSights.

The expert calls business has been around for a long time. As Byrne Hobart wrote in Tegus and the Research Stack:

Depending on how you count, it might be one of the oldest forms of financial research: if you're trying to understand what a company does, or what's happening to it right now, track down someone who knows and ask them. Phil Fisher was doing this in the 1930s and writing about it in the 1950s, and Joseph de la Vega writes about looking for rumors and insights on the Dutch East India Company.

Today, it’s a lucrative business. When GLG filed to go public in October 2021 (it pulled the IPO in March 2022), it stated in its S-1 that the company did $589 million in revenue and $34.1 million in net income in 2020.

Typically, the way it works is that an investor wants to speak with someone with knowledge on a particular company or industry, say a recently former executive at a telecom company. They contact a firm like GLG, and GLG matches them with an expert. The expert charges GLG something like $300 per hour for their time, GLG charges the investor something like $1,000 per hour, the two parties connect, and GLG pockets a cool $700 per hour. (Numbers purely illustrative.)

That’s a lot of money for an hour, but these calls often help funds make decisions on investments in the tens or hundreds of millions of dollars, and expert calls are viewed as a cost of doing business. What’s often more painful is how long it can take to get the information you want – often a week or more. In a business in which time is literally money, that’s too long.

The Elnicks identified primary research as the hardest problem with the greatest potential gains, and they set to work figuring out how to capture those gains. They started by asking a question:

How do you modernize and streamline the information in peoples’ minds on-demand?

You could survey experts and charge investors to access their responses. Or maybe you could create a marketplace where experts sign up and investors message them directly. Those options could speed the process up, but they would do so at the cost of quality and customization.

Instead of coming up with the answer themselves, Mike and Tom started with the problem that they wanted to solve, then they hit the pavement, speaking with as many fundamental investors as they possibly could. They spent 18 months talking to potential customers before launching the first product.

In the earliest calls, they just wanted to understand the pain points. People said that the process wasn’t perfect, but it was fine, it’s just the way it was. “Sure, it’s expensive, but we’re a hedge fund. Sure, they take a while to schedule, but these are experts, they’re busy.”

So they focused in on a specific idea: what if we could get customers to generate content themselves, structure the data they generate, and then charge everyone a subscription fee to access the growing treasure trove of information?

With that reframing, the pushback got more specific. Some investors, believing that the information they gleaned from the questions they asked was proprietary, didn’t feel comfortable sharing transcripts of their calls on the platform. Then one investor said, “I’d be interested in doing this, but I’d need a lag time.” Tom and Mike asked him how much lag time he’d need, and he said two weeks. So they went back to other investors and asked if they’d feel comfortable with a two-week lag time, and many of them said yes.

Through this process, they tweaked and iterated the details until it formed a clear outline of the product. Then, they went back and met with more customers. The goal was to discover an “Over My Dead Body Product”: a product so useful to customers that if someone threatened to take it away, that’s how they’d respond.

Then one day, on one of those exploratory calls, they found something close. An investor told the Elnicks, “Send us something to sign. We’ll pay you when you launch, and we’ll start doing calls now to build up the library.”

That was huge. Getting people to nod along in agreement is one thing. Getting them to loop in their ops and legal teams to hash out and sign a contract, before a single line of code had been written, was another.

Without building a product, Tegus had started to find product-market fit. That defined an approach the company uses to this day: Sell-Design-Build.

Over the next six weeks, 40 customers signed up.

So what were they signing up for? What model emerged from those hundreds of conversations?

As one investor they spoke to told them, “Go study Costco, because this is the Costco model.”

The Tegus Business Model

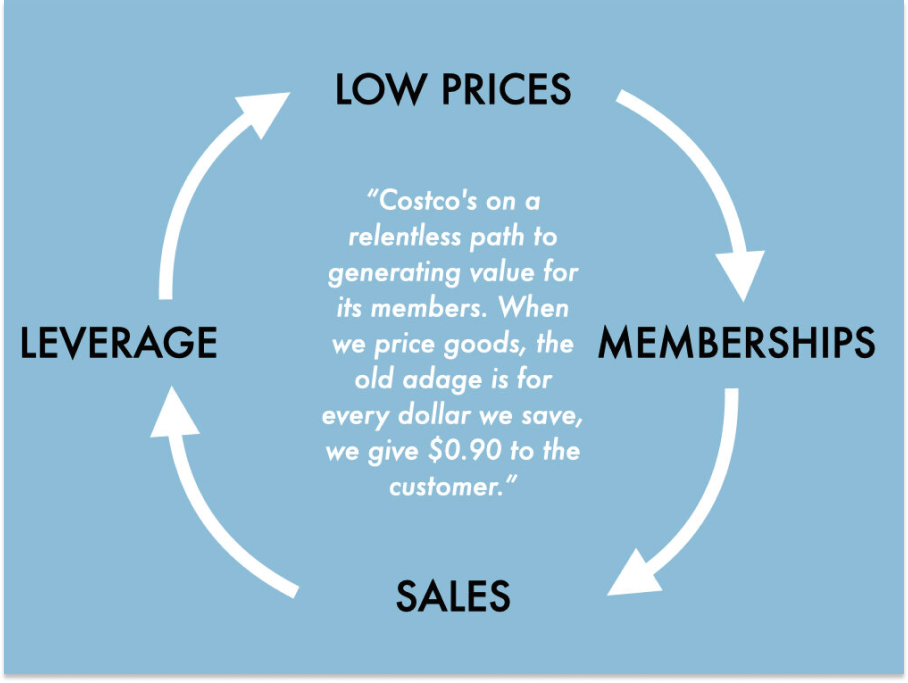

The unlock was simple in retrospect: instead of charging investors a markup on every expert call and keeping them siloed, like an expensive matchmaking service, Tegus charges investors a subscription fee to access the platform, and then lets them book expert calls at cost.

On the surface, it’s the Costco model: sell the product at breakeven, make money on the membership.

Costco’s model is a business analyst's fantasy. For those interested, this presentation by Mine Safety Disclosures, The Resilience of Costco, went viral a few years back and remains the best overview.

There are important differences between Costco and Tegus, though.

For one, Tegus doesn’t sell $1.50 hot dogs. A Tegus subscription starts at $20-25,000 per seat and grows depending on a fund’s size, and in exchange, investors pay $300-400 per call (instead of $1,000 or more) and get access to a library of transcripts for all of the calls that other investors have done through the platform.

That second point is another key difference. While Costco leverages its scale by negotiating lower prices with suppliers, which it passes on to members, to get more members, and more scale, and even lower prices, and so on, Tegus leverages its scale to build an uncatchable library of user-generated content (UGC).

When you think of UGC, you typically think of teens sharing videos on TikTok, creators dropping in-your-face content on YouTube, or influencers posting thirst traps on Instagram.

The model is brilliant, and ByteDance, Alphabet, and Meta are three of the most valuable companies in the world in large part because of it. Users create content for free, that content attracts attention, and platforms sell that attention to advertisers. In Defining Aggregators, Ben Thompson describes Google and Facebook as Super-Aggregators:

Super-Aggregators operate multi-sided markets with at least three sides — users, suppliers, and advertisers — and have zero marginal costs on all of them. The only two examples are Facebook and Google, which in addition to attracting users and suppliers for free, also have self-serve advertising models that generate revenue without corresponding variable costs.

Now, instead of aspiring influencers, imagine that you could get the best investors in the world to create content for you and pay you to do it in exchange for access to all of the other investors’ content.

That’s essentially what Tegus does. In exchange for those low per-call rates, Tegus investors and experts opt-in to sharing a transcript of their call with the entire member base, with a lag. Every call with an expert on a particular company adds to the corpus of information available to all Tegus clients about that company.

For example, if I were digging in on Shopify, I would have access to 162 transcripts of conversations with a range of experts who know about different parts of the business interviewed by investors with a financial stake in asking sharp questions.

I could read those immediately – using search and filters to quickly look for the information I was seeking – and if I found what I was looking for, I could avoid the time and expense of a call altogether. If I didn’t find exactly what I was looking for, I could schedule a call with an expert, at cost, and only ask the questions that hadn’t already been answered, in addition to new ones sparked by ideas I’d read in the transcripts.

To let you check out one of the transcripts for yourself, Tegus has opened up a free version of one of its most popular, on AWS: access it here.

All of a sudden, this $1,000/hr thing, the expert call, is just there, at no marginal cost to me. As Byrne highlights:

When there's a product that's vulnerable to commoditization, a good strategic move can be to completely commoditize it and then move on to complements. This is explicitly what Tegus is trying to do with expert calls. This basically inverts the original value proposition of expert networks: instead of a source of unique, proprietary insights, they're a source of insights that everyone has access to.

One of the key insights that Tom and Mike had – a non-obvious one at the time – is that expert calls were indeed vulnerable to commoditization. That, as Byrne put it, “they aren’t selling alpha. They’re selling beta.”

Remember when I said earlier that they’re students of 7 Powers? Well, they parlayed that insight beautifully into an early Counter Positioning strategy. In the book, Helmer describes Counter Positioning as a situation in which “A newcomer adopts a new, superior business model which the incumbent does not mimic due to anticipated damage to their existing business.”

Traditional expert networks are in the business of selling alpha. The right expert call, carefully guarded, could give an investor an edge, which that investor could use as an input to outperform the market. One-on-one, private expert calls are the crown jewel of their business, a service worthy of a 200% markup. It’s practically impossible for them to respond when doing so would mean cutting off their cash cow and having to re-tool a salesforce to reach out to a customer base who already come to the company for a particular use case, especially when most of those customers had accepted that “that’s just the way it is.”

And selling alpha can be a great business! But it’s not the business that Tegus is in. Tegus is trying to build a platform, and content is a key input to the platform.

By realizing that they could sell expert calls as beta – as knowledge that everyone in the market could access, and therefore that everyone would have to access to keep up – Tegus shifted the field of play in their favor. That would mean a bigger, stickier, more predictable business.

But as Richard Rumelt writes in my favorite strategy book, Good Strategy, Bad Strategy, strategies are made up of many chain-linked parts, each working with the rest in a way that makes the whole system stronger and harder to copy.

Tegus’ model works for Tegus because of all of the different links that chain together. Focus is a core tenet, so they’re happy saying no to customers who want private calls. They want to build a platform that customers use all day because everything they need is there. If that means saying no to lucrative private calls, so be it. And they’re quiet. One of the reasons that Tegus’ counter positioning strategy worked so well is that the team intentionally stayed so under the radar. Because as Helmer warns, “The challenger should be modest in its superiority, so as not to prompt the incumbent into overcoming bias and investing in the new business model.”

For the first five years of its life, Tegus kept quiet. They talked to customers over and over and over again. They focused on a narrow set of investors – fundamental investors focused on software businesses – to ensure that they had enough content to be useful to the customers they were trying to serve. They said “no” to countless potential customers for whom the product wouldn’t have been a perfect fit, for whom their response to its disappearance wouldn’t be “over my dead body.” They focused on free cash flow and building a sustainably differentiated value proposition for customers.

In short, they went slow to go fast.

In 2021, the pace began to pay off. What seemed like a quiet, niche product started to grow. I remember being on a call with a friend, who mentioned that Tegus had just raised at a $3 billion valuation, and I was flabbergasted. I’d spoken to Mike recently and he hadn’t mentioned anything about it. I didn’t realize how big Tegus had gotten.

“What people miss sometimes,” Tom told me, “is that when you crush one thing and crush it well, customers let you in, and adjacencies open up, and the market gets bigger and bigger, so much bigger than you think.”

After Tegus had built an “over my dead body” product in primary research, they saw that they could move into adjacent areas of the research process applying the same framework they’d used since Day 1.

The Outsiders: Fundraising, Share Buybacks, & Acquisitions

Along with 7 Powers and Good Strategy, Bad Strategy, Will Thorndike’s The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success is in my Holy Trinity of business strategy books from the past decade.

Thorndike looks at eight exceptional CEOs as judged by their ability to generate returns for shareholders over the long-term, and breaks down the traits and behaviors they share. He says that “CEOs need to do two things well to be successful: run their operations efficiently and deploy the cash generated by those operations.” Most CEOs and management books focus on the former, but Thorndike and his eight Outsiders focused on the latter: capital allocation.

Basically, CEOs have five essential choices for deploying capital–investing in existing operations, acquiring other businesses, issuing dividends, paying down debt, or repurchasing stock–and three alternatives for raising it–tapping internal cash flow, issuing debt, or raising equity.

It’s early to put Tom and Mike among the eight Outsiders. Their shareholders’ returns are spectacular, but not long-term, yet. That said, it’s clear that they think more critically, and act more decisively, about capital allocation than practically any other startup CEOs I’ve met. Even Stripe co-founder, John Collison, a fan of The Outsiders, told Patrick O’Shaughnessy:

I remember the very first time I read that book, it didn’t really resonate. And the reason why is because, “Stripe’s a small company and we’re doing one thing. I don’t get this book, we’re just working on our business.”

But Tom and Mike have been living the book’s lessons from the early days.

To whit, in 2017, when Tegus was ready to raise money, it went out to a few of its customers instead of pitching Silicon Valley VCs. Investment Group of Santa Barbara, who Mike had never heard of prior, was interested. As both sides got to know each other and developed a relationship, they realized that they were philosophically aligned. IGSB was, as a fund, what Tegus wanted to be as a company.

It’s worth a quick aside on IGSB here, because their involvement speaks volumes about Tegus. Founded by Reece Duca in 1968 with $200k, the firm still manages only the partners’ capital and has no outside investors. They have an incredibly long time horizon for their investments, upwards of 30 years, add somewhere between zero and five new public and maybe one private investment per year, and spend all of their time with them.

IGSB decided to lead the round and get deeply involved in helping to build the company. Tegus was IGSB’s sole investment in 2017, and the firm’s Bob Casey joined the Board, and then joined Tegus full-time (he’s now CFO). Tegus wanted to go slow, and IGSB was fully supportive, even pushing them to think longer. The round was small: $1.5 million at a $4.5 million post-money valuation.

When I asked Tom and Mike about the young company’s maturity, they gave credit to the Board. “IGSB is as mature as it gets. A lot of it comes from insecurity, so we surround ourselves with great people.”

Whoever deserves the credit, the outcome is that they have remained maniacally focused on producing free cash flow since they earned their first revenue. That put them in a strong position. By early 2021, with the team at 115 employees and spitting off cash, in the middle of one of the frothiest bull markets in history, the company did something unusual for a young startup: it used cash from operations to buy shares back from early investors.

They were still going slow by design, and they didn’t need the cash to grow, so they took the opportunity to reduce shares outstanding, remedying a dilutive-by-current-standards Series A. Outsider lesson: “Sometimes the best investment opportunity is your own stock.”

But other investment opportunities soon popped up. By focusing on doing one thing really well, and growing strong relationships with customers, those adjacencies that Tom talked about began opening up later that year. And Tegus raised capital at the peak of the bull market, the perfect time, to take advantage of them.

In November 2021, according to Pitchbook, Tegus announced a $90 million Series B at a $3 billion pre-money valuation. Just yesterday, Patrick O’Shaughnessy shared that his fund, Positive Sum Ventures, had invested $20 million in Tegus.

Raising a round like that in a market like this is a testament to the business that Tegus has built, one that was made to thrive through any market conditions, and to its team. In his blog post, O’Shaughnessy wrote of Tom and Mike, “They fall into this rare category of maniacal entrepreneurs. Every time I speak with them—even hours into a conversation—I’m learning and taking furious mental notes.”

Raising capital is one side of the Outsiders equation; deploying it intelligently is the other. If Tegus is cash flow positive, what are they doing with all of that capital?

This is where the adjacencies started to open up.

The Series B likely closed a little earlier than November, because part of the use of proceeds was revealed the month before, in October when Tegus announced that it was acquiring BamSEC, a platform that makes it easy to find and work with company filings and earnings transcripts.

When Tegus asked customers where else they spent time, they saw that a huge chunk went to evaluating past performance and using filings to understand a company’s performance. When they evaluated the space, and weighed the “build or buy” decision, BamSEC was clearly the market leader. Nearly every banker in America uses and swears by it – another “over my dead body” product. So they decided to acquire it.

Then, this August, Tegus announced another acquisition: Canalyst.

In customer conversations, Tegus also realized that having non-GAAP reported financials is key to any investor understanding a business. When they evaluated the “build or buy” decision in that space, it was another easy buy call. Canalyst was the clear market leader, too, with the best product and highest-quality data.

Tegus’ M&A philosophy is instructive, and it goes back to Tom’s quote. They buy category leaders and are “maniacal around quality,” because customers ultimately rely on Tegus because they trust its product and data. That trust opens up more adjacencies, giving Tegus permission to build the platform out further. Buying the second-best product kills that trust. It’s just not worth it.

Thorndike wrote of the Outsiders that, “With acquisitions, patience is a virtue … as is boldness.”

In mid-2021, when Tom and Mike were starting to think about their M&A strategy, they approached a who’s-who of acquirers to learn the ropes. “One thing about working at Tegus, you eat your own dog food: you aren't afraid to pick up the phone or reach out,” Casey joked. They met with ZoomInfo CEO Henry Schuck, who has done more than a dozen acquisitions on his way to $1 billion in ARR in the past six years, and convinced him to join the Board. They spoke with Mark Leonard, the founder and president of Constellation Software, the most acquisitive software business in the world (who I think might just be Phil Jackson with a great beard):

They spoke with a handful of other highly acquisitive software leaders. They were patient, and they took the time to understand how to do it right.

And then they were bold.

In BamSEC and Canalyst, Tegus had identified two ideal partners to bring the fundamental investment research process into one platform:

Tegus had built a fast-growing, loved qualitative research platform.

BamSEC covered the historical performance angle, with excellent workflow software to boot.

Canalyst had become the leader in fundamental models.

In ten months, Tegus had acquired its way to owning the three main legs of the fundamental research stool. Now, Tegus is entering the next leg of the race: building the modern research platform for fundamental investors.

The products still need to be integrated, but it’s easy to imagine where it’s heading.

An analyst might start with a model on a company from Canalyst, with all inputs auditable through integrations with BamSEC. As they customize the model and tweak assumptions – the creative work of fundamental investing – they can click into transcripts of calls with experts on different pieces of the business. A former VP of Sales mentioned that the sales cycle was starting to lengthen when he left three months ago and a customer said that a competitor’s product was getting stronger? Turn the assumed growth rate down 2% and pull gross margins down 3% starting next year. If the analyst still has questions, say on a worrying uptick in COGS, she can set up a call with the former Head of FP&A, at cost.

Tegus’ hope is that by combining products with their own sustainable differentiation – Tegus in content and data, BamSEC in workflow software, Canalyst in human-in-the-loop models with clean data and unique KPIs – it can dramatically improve analysts’ jobs and build a truly sustainably differentiated product that will be best-in-class for decades to come.

As Tegus succeeds, and starts telling its story more publicly, there will be more copycats. There already are. The point of digging moats, building over my dead body products, and creating sustainable differentiation, is to put the company in a position to withstand the competition and continue to widen the lead.

To that end, I asked Mike and Tom whether, now that they had all of this content and data, they’d start using AI to pull insights out that even great analysts wouldn’t think to look for, turning more alpha into beta. They said that now that they’ve taken processes from days to hours, AI and NLP (Natural Language Processing) might help shorten them from hours to minutes, but that, as always, what they build will depend on what will make their customers’ lives easier, and on what will build sustainable differentiation for Tegus.

First things first, they’re focused on integrating BamSEC and Canalyst into one integrated product experience, so that customers don’t need to spend time and break focus by switching from product to product, so that the experience is smooth and seamless. Mike is out in Vancouver this week working with the 200-person Canalyst team in-person. Since Tom and Bob aren’t on the trip, he’ll get his own hotel room. When they travel together, they share one. There are better things than three hotel rooms to do with the money.

As they level up the company, they will, of course, continue to lean on their own product. “When we don’t know something,” Tom told me, “we go out and try to talk to the best frickin’ people to figure it out.”

The acquisitions have made Tegus even more software-focused, so the current obsession is with understanding what the best engineering organizations look like. In the past two weeks, they’ve spoken with the former CTO of GitHub, the CTO of Shopify, and dozens of other top tier engineering leaders.

With a growing organization, one in which everyone is held to a high standard and outperformers are rewarded with outsized compensation, they’re also focused on building a world-class performance management function. Snowflake’s Frank Slootman is a legend in this area, so they sent Shelly Begun, Snowflake’s CHRO, a cold message on LinkedIn. She responded, surprised because no one reaches out to her, and shared lessons with Tom and Mike. Then they talked to leaders at Netflix, at Facebook, and more.

At the end of our last call, Tom said something that captures the ethos of both the Tegus product and its culture: “You can learn almost anything.”

When a company expects to be around for fifty years, that ability to compound learning – both for itself and for its customers – might be its greatest sustainable advantage.

If you want to try Tegus for yourself, sign up with this special Not Boring link for a free trial:

Thanks to Dan for editing, and to Mike, Tom, Bob, and Jacinta for working with me on the piece!

Thanks to Dan for editing, and to Mike, Tom, Bob, and Jacinta for working with me on the piece!

We’ll be back in your inbox with the Weekly Dose of Optimism tomorrow morning!

Thanks for reading,

Packy

Interesting - wondering about the angle for experts, who seem like the one piece of the puzzle that's definitely getting the short end of the stick. Same $300 / hr, but now the transcript of your call is rendering your services increasingly useless over time. Makes sense for an expert to choose GLG given that, unless I'm missing something about how they get paid for transcript access after the fact.

Love this! Tegus is pretty epic