Welcome to the 574 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 18,613 smart, curious folks by subscribing here!

Hi friends 👋 ,

Happy Monday!

Not Boring straddles two worlds - technology and finance. I try to bring pro-level insights to a consumer audience. Today’s essay is about what happens when those things start to blur, when technology alters finance and consumers play a larger role in shaping the markets.

It’s an early exploration of a topic that I’ll be writing a lot more about in the months and years ahead, putting thoughts down on paper so that we can debate and stress-test them together. I’d love to hear your thoughts in the comments.

But first, a word from our sponsor:

Today's Not Boring is brought to you by…

Seemingly everyone is talking about how next week’s elections will impact the markets and their investments. The fear makes sense -- historical data shows US presidential elections tend to make investors more conservative. Even my most risk-seeking, SPAC-loving friend told me that he’s going to cash until after the election. But knowledge is better than fear: do markets perform better in Democratic or Republican administrations? And most importantly, is there an ideal investment strategy during an election season?

Weathering financial uncertainty during this election is crucial for long-term financial success. Yet, it can be challenging to find a go-to source for trustworthy and unbiased insights. That’s where Zoe Financial comes in.

Read Zoe Financial’s Top 5 Investment Impacts of US Presidential Elections Here:

Software is Eating the Markets

In 2011, Netscape and a16z founder, Marc Andreesen, wrote a guest post in the WSJ titled Why Software Is Eating the World. With nine years of hindsight, he was so obviously right that it’s cliché to cite it today. I’m kind of mad at myself for typing these words right now.

Software has fundamentally altered nearly every industry. Netflix put a dent in cable’s long standing dominance, and already TikTok and Fortnite threaten Netflix. Newspapers are dying. Millions of people now earn livings in the Gig Economy or the Passion Economy. A private company, SpaceX, is doing things that NASA can’t. The list goes on.

But despite that, we operate under the assumption that financial markets are somehow different, impervious. Of course, technology has impacted finance. High-speed trading accounts for an increasingly large percentage of activity, and institutional investors will spend millions or billions on any tech that gets them a slight advantage. But if recent tech history is a guide, technology’s ultimate impact on finance will be less about further entrenching incumbents; it will empower consumers.

Consumers are participating directly in the market in greater numbers than ever before, but every analysis I’ve read treats increased retail participation as a temporary COVID-induced blip, and retail traders as irresponsible and irrational gamblers just looking to have a good time. Soon, serious people argue, things will go back to the way they were.

They may be right. But what if they’re not?

Investing in Social Status

In November, back when San Francisco was still more physical place than state of mind and most people associated Corona with lime, Alex Danco wrote an excellent post called The Social Subsidy of Angel Investing.

In it, he argued three main points:

Angel Investors in the Bay Area don’t just invest for the financial returns; they also invest for the social returns.

The social rewards of angel investing solve an important chicken-and-egg problem in early stage fundraising that financial rewards do not.

The social returns to angel investing have a strong geographical network effect, because they require a threshold density in order to kick in.

In San Francisco, owning a Ferrari wasn’t nearly as cool as owning pre-seed shares in Stripe or Uber. In some ways, startup equity behaved more like a Veblen Good -- one that paradoxically sees more demand as the price goes up -- than like an investment. How else to explain the mad dash to invest in Clubhouse at any price? A high price signaled a more competitive round, which meant more social status for getting in.

To an outsider, this might seem crazy. Why invest your hard-earned money in something that doesn’t provide the best risk-adjusted returns? When angel investors wrote checks into startups, they were really buying two things: an asset with a potential financial return and a status symbol.

As usual, Danco was prescient, but he couldn’t have predicted what happened in the year since his post.

Since the beginning of the COVID pandemic in the US in March, the economy is struggling, consumers are buying fewer things, and millions are unemployed. And yet, the stock market hovers near all-time highs. People are spending less on services and luxury items, and investing more.

There is no one way to explain everything that’s been going on, but there are a few that I like:

Low Rates + Fiscal Stimulus: Interest rates are at all-time lows, so anyone looking for yield needs to invest in stocks. Plus, the Fed has provided a backstop that makes risky assets less risky.

Tech Strength: Tech companies make up a bigger piece of the major indices than ever, and they are actually benefiting from COVID. Plus, normal people are familiar with those companies -- we use their products every day -- so they are more likely to invest in them.

Boredom Markets: Investors are bored at home -- Bloomberg’s Matt Levine calls it the “boredom markets hypothesis” -- and not spending as much discretionary income on fun experiences and luxury goods, so they’re investing instead.

There’s another take that I haven’t heard but want to explore today:

Software is eating the markets. Flush with cash and empowered by new tech platforms that blur the lines between investment, experience, entertainment, and digital assets, a segment of consumer investors are shifting money from consumption to investment. Consumer investors expect different things from their investments than professionals do and value assets differently as a result. New technologies, regulations, social trends, and asset classes mean that this shift is here to stay, and could continue to gain momentum after COVID is gone. This time, maybe it really is different.

Like angel investments in the Bay Area, when you add social and experiential value to other asset classes like stocks, sneakers, and cryptocurrencies, price is divorced from hard math and becomes more emotional. That doesn’t mean that people are sitting at home bored and gambling; they may be making perfectly rational decisions when accounting for the many roles their investments are doing for them now.

The rise of consumer investors will alter how markets operate. To understand why and how, we’ll cover:

The State of the Market. People have a lot of savings, they can’t spend on luxury goods and experiences, and rates are historically low. Enter: more fun asset classes.

What Clayton Christensen Got Wrong. Consumers and professionals value different things in the products they buy. Why not in the investments they make?

New Technologies Breed New Spending Patterns. New platforms make investments feel more like digital goods and steal spend from non-investment categories.

Modern Platforms and Asset Classes. The platforms driving retail investment in stocks, alternative assets, venture, and crypto.

Is It Different This Time? Why the COVID-induced changes to the way we invest might persist.

Let’s start with why things are the way they are.

The State of the Market

In March, it seemed like the world was ending. Stocks plummeted 35% between late February and late March. Millions lost their jobs. Anyone deemed non-essential stayed inside. Everyone braced for a deep recession.

But then, things shifted. The Fed stepped in and lowered rates while the government pumped trillions of dollars of fiscal stimulus into the economy. While 12.6 million Americans remain unemployed and 100,000 small businesses will never reopen, the market has roared back.

Not only did public companies perform well, new ones came to market to take advantage of insatiable demand for risk assets:

Companies like Snowflake, Unity, Asana, Palantir, BigCommerce, and Lemonade IPO’d to great success.

SPACs dumped new, riskier supply onto the market, and the market is gobbling it up.

Startups are raising at ever-higher valuations, including companies that themselves offer new assets classes to yield-hungry investors.

People much smarter than me have explained why the markets are the way they are today.

Dan McMurtie called it very early in Devil’s Advocate: The Bull Case back in May.

Jesse Livermore discussed first, second, and third order causes and effects on Invest Like the Best.

Howard Marks recently wrote a letter to Oaktree’s clients called Coming Into Focus.

Their explanations go something like this:

The Fed lowered the Fed Funds rate, on which all other rates are based, to 0-0.25% on March 15th.

The Federal government learned from the 2008-2009 financial crisis and stepped in quickly to provide $3 trillion in fiscal stimulus to support a shut-down economy, which both pumped money into the system and gave investors confidence in a backstop.

Low interest rates did a lot of things:

Stimulated the economy: “Mortgage rates are so low, we should buy a house!”

Increased the discounted present value of future cashflows: everyone adjusted their models with lower discount rates, and present values shot up automatically.

Brought down demanded returns across all asset classes: when the risk-free rate is lower, people also expect lower returns on riskier assets, which drives up prices.

Forced people to search for returns in riskier assets: if returns on all asset classes come down, you need to invest in riskier assets to get the same return.

Importantly, low interest rates favor more fun assets, like art, cards, and tech stocks, over more boring ones, like bonds and value stocks. Tech stocks got a triple whammy of tailwinds:

The underlying businesses improved as everything moved online, and tech businesses like Zoom and Shopify reported massive growth.

Lower discount rates benefit every company’s valuation, but they benefit faster-growing companies the most. All else equal, if Company A has a higher proportion of its cash flow in future years than Company B, Company A’s DCF-based valuation will improve more as the discount rate drops. Tech companies, which trade profits today for growth and profits in the future, are the ultimate beneficiary of low rates.

Retail investors love investing in the tech companies they use every day, and a segment of retail investors has a lot more cash to invest.

Additionally, with bonds at all-time low rates, investors can make a rational argument that they should actually diversify into more interesting asset classes like art, trading cards, real estate, and sneakers, which are now more accessible due to Reg A+ and the businesses the regulatory change has enabled. It’s hard to measure the impact of “fun” on asset prices, but across almost every consumer category, a more fun product with a better user experience will attract more dollars than a more boring one with a worse user experience. The same applies to investing.

Simultaneously, the type of people who invest in the markets already maintained their income but dramatically lowered their expenses. While personal consumption expenditures on goods bounced back to pre-COVID levels quickly -- people need to eat -- spending on services in August 2020 remained 7% below August 2019 levels, and McKinsey forecasted that the luxury goods market would drop by 35% to 39%. People are traveling less, dining out less, getting their hair cut less, and buying fewer physical status symbols. No one can see the red sole on your Louboutins when you’re on a Zoom.

As a result, retail investors have more money to spend. Disposable personal income is up 5% year-over-year (YoY) and the personal savings rate doubled from 7.3% last year to 14.1% this year! Retail investors, regular people investing their personal money, now make up 25% of trades versus 10% in 2019.

With savings accounts yielding next to nothing, people are putting that money to work in financial assets, including but not limited to stocks, not just for the potential financial gain, but because those assets themselves are filling the need for social status, connection, entertainment, and education that we’re not able to get elsewhere.

I did an informal twitter poll to see what people were doing with the money they weren’t spending:

60% of people decided to invest their money - in stocks, Bitcoin, and new alternative assets - instead of buying new things or saving it in cash. When interest rates are near-zero and inflation risk looms, investors feel the need to put money to work.

Viewed through that lens, recent investment behavior looks a lot less like crazy professional investing and a lot more like consumers buying things and experiences that also have financial upside.

What Clayton Christensen Got Wrong

It’s easy to make fun of the new wave of Robinhood-using, SPAC-buying, WallStreetBets-posting “investors.” They’re not doing the type of deep analysis traders would do, choosing to invest with the herd instead of uncovering their own hidden value gems.

One popular view of this phenomenon is that in a market like this, Robinhood is just a casino. Gamblers know the odds are against them, but they do it anyway, for the rush or the small chance of a huge return. That’s certainly part of it.

But this retail trader trend has persisted for nearly a year, around the world, and I think there’s something more to it. Retail investors value different things than institutional ones.

In What Clayton Christensen Got Wrong, one of the earliest Stratechery pieces, Ben Thompson critiqued the titular HBS professor and creator of disruption theory’s prediction that the iPod and iPhone were doomed to fail. Christensen argued that while Apple’s integrated approach makes sense in the early days of a new market, over time, as the products’ components become commoditized, a more modular approach wins out. When even modular products become “good enough,” the low-cost solution dominates the market.

What he got wrong, according to Thompson, was assuming that consumers and businesses make decisions in the same way. Specifically, Thompson highlighted three of Christensen’s flawed assumptions:

Buyers are rational.

Every attribute that matters can be documented and measured.

Modular providers can become “good enough” on all the attributes that matter to buyers.

Those assumptions largely hold for business buyers, but not for consumers. Business buyers care about getting all the features they need at the lowest possible cost. Consumers care about user experience, and how a product makes them feel.

Institutional investors still account for the vast majority of dollars traded. Even though retail traders’ share of daily average revenue trades (DARTs), according to Citadel, has more than doubled in the past year from 10% to 25%, professional investors still make 75% of trades, and make much larger trades. But if retail participation persists, 25% is still a large enough share to impact the market, and retail investors care about different things than professionals do. Like iPhone buyers and Bay Area angel investors, this new generation of retail traders is buying more than just an expected future return when they buy an asset.

Although they’re often derided as irrational, or gamblers, or YOLO traders, retail traders might be behaving perfectly rationally when you price in everything else that they’re buying: an experience, a status symbol, a digital good, belonging, entertainment, education, and more. That should mean that they have a higher willingness-to-pay than someone who attributes no value to those things.

During COVID, if some retail investors have come off as irresponsible gamblers, I’d argue that that has more to do with the software they’re using than their investing preference. Robinhood encourages gambling; it feels like a game. But new products designed with the investor-as-consumer in mind are changing that.

New Technology Breeds New Behaviors

In Audio’s Opportunity and Who Will Capture It, investor Matthew Ball wrote about technology’s impact on audio, video, and gaming. Song lengths, for example, are a function of the medium on which the song is played or the way its creators are paid. 45s limited a song’s length to below four minutes; Spotify’s pay-per-listen business model encourages shorter songs that can be played more often.

But while each new form factor or delivery method for music stole share from the previous generation, new forms of video and video games increased the size of the overall pie.

The advent of mobile gaming didn’t mean that people spent less time and money on console gaming, it meant that they played more games, because they could do so from anywhere.

Like mobile gaming, new investment platforms will grow the overall investing pie.

The dot-com bubble was driven by both tech stocks, and tech platforms that allowed retail investors to easily trade for themselves for the first time, at the click of a button. E*Trade touted trades for just $14.95 while suggesting that if investors wanted something done right, they had to do it themselves.

That new technology brought more people into the market and encouraged new behavior. Unwatched by the professionals, retail investors could make risky gambles that they would be too embarrassed to tell their broker to put in for them. The time between hearing about a hot new stock and being able to execute a trade fell to practically zero. But the online brokerages’ interfaces were simplistic, and the ways for “investors” to find and communicate with each other limited to clunky, text-based message boards. They weren’t buying new experiences, just trying not to miss out on the gains their neighbors were generating. They moved money from savings, brokerages, or 401ks into accounts they managed, and invested in anything with a “.com” in its name.

In other words, they changed how they invested the same pool of investment funds, personally directing investments towards riskier trades, but didn’t re-allocate money from buying things or experiences. In fact, personal consumption expenditures grew at slightly higher rates in 1999 than in the years leading up to the bubble.

Instead, investors moved money from safer assets, like bonds, into riskier ones, like shares of Pets.com, despite the fact that bonds’ expected returns were higher than stocks’. We all know how that ended.

Today is different. People are looking for new ways to spend money they would have otherwise spent on new clothes, trips, dining, and all of the things that people valued before the pandemic. It even makes sense for most people to move allocations away from bonds -- the most boring asset class -- because of low rates. Concurrently, new platforms are changing both what assets retail investors can buy and their experience owning those assets.

That has major implications on the prices that people will pay and the returns they’ll accept. Because the expected long-term return on many goods and experiences is zero -- you don’t expect to get $120 back after going to a concert for which you paid $100 -- treating investments partially as a consumption good and partially as an experience should mean that consumer investors are willing to pay higher prices, or conversely, to get lower returns.

This won’t just drive up the value of hot stocks. Prices are not nearly as crazy as they were during the dot com bubble, and they won’t be. It will represent a shift from consumption into investments on new platforms and in new asset classes.

New Platforms and Asset Classes

Changes in the availability and user experience of four asset classes are leading the charge:

Stocks, Options, and Bonds

Reg A+ / Alternative Assets

Venture Investments

Crypto

When Cryptokitties burst onto the scene at the peak of the crypto craze in late 2017, supporters heralded a new age of unique, digital assets that people would buy and trade like they trade art or Pokemon cards. Digital items and skins in Fortnite, Roblox, and Animal Crossing proved that digital assets were a multi-hundred-million dollar economy.

But the ultimate digital asset might be investments in traditional assets with new digital interfaces. Assets that were once cells in a spreadsheet or totally inaccessible are coming to life online.

Stocks and Options

The first company that comes to mind when you think of COVID and investing is Robinhood. No private startup has benefited more from COVID than it has. Last July, it raised its Series E at a $7.6 billion valuation. In May, it raised again at $8.5 billion. Then just four months later, in September, it raised at a $12 billion valuation. Today, its shares are trading at a 43% premium to September’s price, or $17.1 billion, on Forge.

It’s no wonder. Robinhood announced that it passed 13 million accounts (up 3 million since the start of COVID) in May, passed every broker in terms of DARTs in June at 4.3 million, and akram’s razor estimates the company now has 16 million active clients. When more investors are consumers, specs matter less than UX. Out are heavy stock-screening tools, in is one-click mobile buying.

People like Robinhood because it gives them control of their portfolio, at their fingertips. On the other side of the coin, another 2010s investing darling, Wealthfront, has been eerily quiet during COVID, not releasing a new Assets Under Management (AUM) number since they reported having $20 billion AUM last September.

People are less interested in playing it safe and passive with Wealthfront, opting instead to control their own portfolios. Data from audience intelligence platform Pulsar on social media mentions of the two companies backs that hunch up.

In 2017, people talked about Robinhood and Wealthfront about the same amount. Today, people talk about Robinhood 20-50 times more than Wealthfront.

That said, as I’ve written before, I think Robinhood is like Napster. It reshaped how consumer investors trade and forced legacy players to adapt, but it will face issues with regulators and new companies that learn from Robinhood, take its advancements for granted, and build new and better user experiences will ultimately win.

As I wrote about in the Not Boring Investment Memo on Composer, companies that give users the control of a Robinhood with the ability to build hedge fund-like strategies, like Composer, stand to do tremendously well. For relatively sophisticated retail investors, Composer will make Sharpe Ratios the new returns, and enable individuals to profit from building strategies that others use.

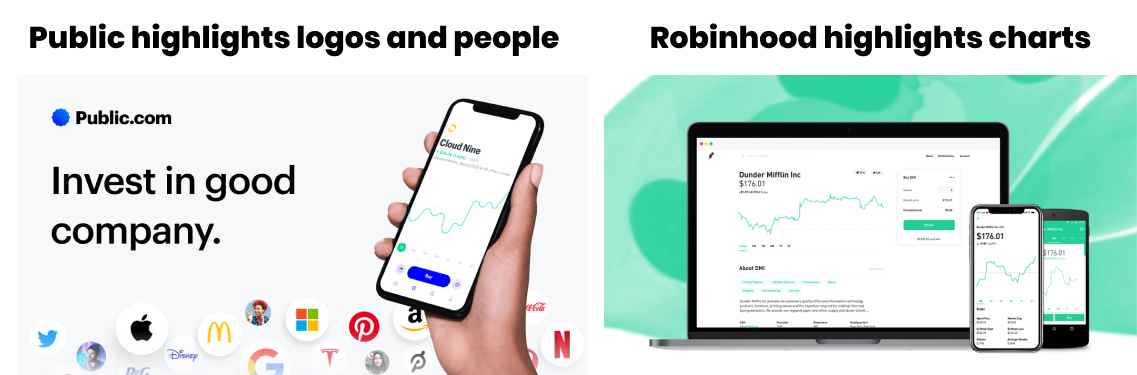

As financial assets become more like digital assets or consumer goods, companies like Public that let customers show their allegiance to their favorite companies will thrive as well. Seemingly small design differences between Public and Robinhood will matter more over time. For example:

Robinhood is single-player, and those who want to talk about their holdings need to take screenshots and discuss on Twitter or Reddit. Public is multi-player, facilitating conversations among users around particular companies and themes in the app.

Robinhood shows tickers on the home screen, while Public shows logos.

Public sends users t-shirts with their top holdings on them, tying peoples’ identities more closely to the companies they own, and built a Twitter plug-in that brings up a company’s chart when users scroll over its $hashtag to be where the conversation is.

A stock bought on Robinhood feels like a gamble or an investment. The same stock on Public feels like ownership of a company, with the digital and physical assets to prove it.

Another startup, CommonStock, adds a community element and competition layer on top of any brokerage account by creating a global leaderboard based on actual portfolio performance. CommonStock landed a massive $9.7 million seed round in August. CommonStock allows the best consumer investors to build followings, and less experienced investors to learn from them.

Consumer investors can now get access to professional-quality data through tools like Atom Finance and TIKR, which offer lightweight Bloomberg Terminal functionality at a fraction of the cost.

We will see more products that make owning stocks feel like owning a piece of the company itself over time, whether from existing startups or new entrants. One idea would be to create a digital equivalent of AmEx’s “Member Since ‘00” card for stock ownership. I would love to show off the fact that I’ve owned Shopify since $89 and SNAP since $20 without screenshotting my position sizes.

Small design improvements like that would build both loyalty to the platform and encourage holding on to investments longer instead of recklessly day trading.

While Robinhood seems like the winner, we are just getting started. In October, Alpaca raised a $10 million Series A to continue to grow its API-powered trading service, which makes it easier for startups to build new products focused on the user experience instead of the back-end tech.

Reg A+ and Alternative Assets

As I wrote about in Fundrise & The Magic of Diversification, diversification produces better risk-adjusted returns than a highly correlated portfolio. With interest rates at all-time lows, investors are looking away from bonds and to new asset classes.

A new crop of companies is taking advantage of regulatory and technological changes to give regular investors access to alternative asset classes, from collectibles to real estate to SaaS receivables. This will pull money from consumer goods, experiences, and bonds into assets that are as much fun to own as they are good investments. While returns are certainly important to these companies’ customers, a UX that makes the assets feel more tangible is equally important. Design blurs the line between investment and digital asset.

Many of these companies take advantage of Reg A+, which was passed as part of the 2012 JOBS Act and lets companies raise up to $50 million per year from non-accredited investors. Reg AT companies often let people invest in fractional shares of an asset, like a classic car or an Andy Warhol painting, that would otherwise have been too expensive for all but the ultra-wealthy. To give you a taste, here are five of the alternative asset investing platforms that are most interesting to me:

Rally (née Rally Rd.) is “a platform for buying and selling equity shares in collectible assets,” including exotic cars, memorabilia, watches, rare books, and wine.

Rally raised $17 million in September, and cited 200,000 users with transaction growth of 195% over the past 12 months. With people stuck at home and not able to buy things, they moved money into investments in things that may appreciate over time.

Otiscalls itself “the investment platform for culture.” Investors on the platform can buy shares in a wide-range of assets from a LeBron James rookie card to original X-Men comic books. The company recently partnered with MSCHF to turn ridiculously high medical bills into art, and sold $20 shares in the art to pay off 73k of peoples’ medical bills.

Fundrisegives retail investors access to institutional quality real estate investments through a product that they call an eREIT. Fundrise has a clean interface through which investors can see and track the performance of the individual properties that the fund invests in. That makes the investment more tangible, which provides value beyond the financial returns.

Masterworkstakes art collecting digital and makes it accessible to regular investors. With as little as $1,000, investors can buy shares in works by Andy Warhol, Jean-Michel Basquiat, Keith Haring, Picasso, Banksy, and Monet. Even a digital portfolio of blue-chip art is more tangible than a bond, is something buyers can brag about to friends, and provides an excuse to learn art history, and returns from blue-chip art have doubled the S&P 500’s over the past twenty years.

Pipe, founded in 2019 and launched in June, turns SaaS contracts into a new asset class.Instead of raising dilutive venture capital, SaaS businesses can sell their contracts to investors looking for yield and exposure to a different asset class. It’s a fixed-income like product with more tangibility than buying a bond, giving investors some of the social status and fulfillment they might get from a venture investment but with predictable returns.

This is a growing category, and as more money moves from consumer goods to investments, I expect new companies to make more and more assets investible. For this space to grow into its full potential, I would love to see a company build APIs to knock down silos and bring these alternative assets into the context of an investor’s full portfolio. Alt, which is building a tool for people to value and manage all of their existing alternative assets -- like the physical baseball card collection or wine cellar -- hinted that it might tie into the other alternative investment platforms, and from there, it could provide the one connection to investors’ brokerages.

Venture Investments

One of the reasons that angel investing in the Bay Area was such a status symbol is that it was fairly exclusive. Venture investments don’t trade publicly, so to invest in the best companies, you needed to know someone or know someone who knows someone.

Technology, new fund structures, and regulatory changes are combining to work their magic here, too. Platforms like AngelList and Forge give regular (albeit, currently, high net worth) people the opportunity to access high risk, high reward venture investments, from early to late stage, and even in the public markets. These investments are often as much about status, education, and helping something new come into existence as they are about expected returns.

Syndicates and Rolling Funds

The rise of syndicates (like the Not Boring Syndicate) and Rolling Funds, which allow leads to raise money via quarterly subscriptions instead of through closed funds, mean that any accredited investor can now access and invest in early stage deals, sourced by people that they trust, in rounds priced by more experienced investors.

AngelList is the leader in both syndicates and rolling funds. The company makes it simple to set up a fund, take investments from LPs, and deploy capital into startups. In exchange, AngelList takes a fee and keeps a piece of the upside, or “carry.” As of 2019, AngelList had $1.8 billion in AUM, and 1,657 startups were funded on the platform last year. The company hasn’t released 2020 numbers, but I expect that there will be a significant uptick. Already, there are 47 unicorns in the portfolio -- AngelList, via its carry and investments it makes in deals, sneakily has one of the most impressive startup portfolios in the world.

Assure sits behind the scenes and provides SPV and fund administration, so that leads can focus on deal flow and investor relations. AngelList is actually an Assure client, as is Republic, which lets non-accredited investors put as little as $100 into startup deals. For those with big enough syndicates and their own network of LPs, it may make sense to skip AngelList and work directly with Assure to save on carry and keep more of the upside.

Pre-IPO Equity Marketplaces

Assure also powers marketplaces on which startup employees can sell their shares to accredited investors before a liquidity event. Employees get liquidity to make important purchases, and diversify their holdings, and investors get access to investments before public market investors. Investors also get the chance to say, “I invested in [Stripe, Robinhood, Airbnb, DoorDash] before it was public” without as much risk as earlier stage ventures. There’s no greater status symbol right now among a certain group than Stripe equity.

The three biggest players in this space are Forge, EquityZen, and SharesPost.

Like Public, these marketplaces are logo-first. The investments are as much about being involved in the companies as they are about the potential financial returns.

This space will get much more interesting in the next couple of years as two unicorns compete to make startup equity more legible and liquid. Carta is using its position as the system-of-record for startup equity to launch CartaX, the “first vertically integrated market ecosystem for private equity.” CartaX will compete with Forge, EquityZen, and SharesPost from a strong position - nearly every startup already tracks their equity in Carta, so selling should be as easy as flipping a switch.

Just last week, Stripe announced that it’s entering the fray by leading a $10 million dollar round for Carta competitor, Pulley. While neither Pulley nor Stripe has mentioned plans to build a secondary shares marketplace, I think it’s only a matter of time.

SPACs

One way to view Special Purpose Acquisition Companies (SPACs) is as a way for companies to go public before they’re ready, dumping risk on less sophisticated investors to give investors, employees, and sponsors equity. I don’t subscribe to that view. I think that SPACs are a necessary intermediate step that bridges the artificial line between private and public markets.

Today, it’s clunky. There are some great companies going public via SPAC, like Opendoor and DraftKings, some risky ones, like Virgin Galactic, and some outright frauds, like Nikola. SPAC-hungry investors are bidding some companies’ prices up to levels that don’t make sense. But more people have access to investments earlier in companies’ lifecycles than before because of SPACs.

Structures that push the boundaries, like SPACs, make the way things are seem ridiculous. Why, for example, can a non-accredited investor buy shares in Nikola, but not a strong private company like Stripe? That will force regulators to re-think who can invest in which types of companies, and how. Taking it a step further, why can anyone with enough cash in the bank spend it all on something like a jetski, but not shares in a startup? As investments take more wallet share from goods and experiences, we’ll need to rethink how they’re regulated and communicated, and SPACs are one step in that direction.

Crypto

Crypto is back. After relative obscurity in its first few years, Bitcoin’s price chart looks almost exactly like the Gartner Hype Cycle.

Bitcoin itself exhibits the characteristics of a Bay Area angel investment -- looking forward from 2013, investing time, money, and effort in Bitcoin might or might have been a good financial decision, but being a person who invested in Bitcoin said something about you. It provided social status within the community, an education on a new technology, entertainment, and other rewards not captured by Bitcoin’s price.

Today, Bitcoin’s price is rising steadily as institutional investors realize that an allocation to crypto makes sense at least as a hedge against inflation and potentially as a way to get in early on a new payments infrastructure. Last week, PayPal announced that it would allow its customers to buy and sell Bitcoin on the platform, and even spend it via PayPal and its Venmo subsidiary.

While Bitcoin is going mainstream, other crypto-based decentralized finance (“DeFi”) applications are turning more companies, products, and people into potential investments and broadening the definition of what is investible. According to Pulsar, social buzz around both Bitcoin and DeFi are up significantly on the year, but it looks as if Bitcoin’s recent rally has taken some of the shine from DeFi.

Everything going on in crypto deserves its own Not Boring essay soon, but I’ll give you two examples to give you a flavor for what I mean.

Roll is “blockchain infrastructure for social money. Built on top of Ethereum, Roll allows creators to spin up their own cryptocurrency that their audience, customers, or community can earn by doing things that the creator wants to encourage. For example, my friend Holyn launched her own token, $HOLLA, that readers can earn for subscribing to her newsletter, sharing it on social media, or referring friends, and redeem for conversations with Holyn, tweets, or beta app invites (like Clubhouse).

Richard Kim recently launched a User-Governed Collective called R.N.G., which is a Discord server for founders and investors in the gaming community in which status is determined by the amount of $RNG users hold. Users earn $RNG by signing up early, by doing cool things for the community, by creating, and winning competitions. Unlike $HOLLA, Kim wants to create liquidity for $RNG holders, making positive participation in the community akin to an investment.

Source:From Nothing to Something with R.N.G.

By making it trivial to launch a token, Roll gives creators the power to create new use-cases underpinned by cryptocurrencies.

Fairmint, which created the Continuous Agreement for Future Equity that allows businesses to make equity programmable,barely even mentions crypto on its website. Instead, it focuses on what the technology makes possible: seamlessly granting equity in a business to all stakeholders, not just employees or investors.

Airbnb might give equity to hosts automatically when they become Superhosts, or a new SaaS company might give equity to people who refer new customers, theoretically aligning the incentives of everyone involved, and turning all stakeholders into investors.

We are in the earliest innings in this space, but I’m now more bullish on crypto than ever before because it is both an inflationary hedge and a way to empower new forms of ownership in a world that is trending towards everything becoming an investable asset.

Taken together, new technologies and financial products are blurring the lines between investing, consuming, experiencing, and participating. COVID was a catalyst; will the shift persist?

This Time It’s Different?

In the 1930s, investor John Templeton said, “The four most dangerous words in investing are: this time it’s different.” Michael Batnick amended that claim in 2017 when he said, “The twelve most dangerous words in investing are ‘the four most dangerous words in investing are: it’s this time it’s different.’” It’s dangerous to think that the fundamental mechanics of the market have fundamentally shifted, but it’s also dangerous to think that they haven’t. So which is it this time?

I have no crystal ball. I don’t know if stocks and other asset prices will be higher or lower this time next week, next month, or next year.

But I do think that the composition of the market, what consumer investors invest in, how they do it, and what they care about are fundamentally changed. On a long enough time horizon, as more assets become investible, information is more freely available, and companies create new user experiences that continue to blur the lines between consumption and investment, software will have the same impact on the financial markets that its had on media, retail, travel, transportation, and even space travel.

Software will eat financial markets, cut out middle men, and turn investing into an experience from which consumers get more than a financial return. Still, only a relatively wealthy subset of consumers participate in financial markets; for software’s impact here to be truly revolutionary, it will need to increase access and participation in the markets. There are early signs that make me hopeful.

This time, it really will be different.