Welcome to the 367 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 9,255 smart, curious folks by subscribing here!

The Hard Thing About Easy Things

“Amazon is building an empire, and Shopify is trying to arm the rebels. So maybe some of our customers might compete with Amazon, at some point, but that would be like super cool, and we’re not there yet.”

-- Tobi Lütke, Shopify Founder and CEO

Shopify’s stock keeps doubling and doubling, so everyone wants to know its secret. The most fun explanation is Shopify CEO Tobi Lütke’s claim that the company is “trying to arm the rebels.” But it’s not true, really. By giving everyone access to the same tools, Shopify isn’t arming the rebels as much as it’s profiting off the chaos created by arming everyone.

Here’s the hard thing about easy things: if everyone can do something, there’s no advantage to doing it, but you still have to do it anyway just to keep up.

By making Direct-to-Consumer (“DTC”) easier, software like Shopify increases entropy and lowers the probability that any specific company will generate sustained profits.

Tobi borrowed the phrase “arming the rebels” from a geopolitical strategy in which a big, powerful country, safely separated by miles and oceans, supports rebel forces fighting for change in a smaller, poorer, less powerful country by giving them money, arms, and implied support.

Think the US backing the Contras against the Sandinista Government in Nicaragua or the Soviet and Cuban support for anti-apartheid forces in South Africa. If you want to put on your tin foil hat, think the US funding Osama bin Laden and the Afghan Arab fighters in the Soviet-Afghan War.

Shopify is an amazing company full of great people, but Shopify isn’t really arming the rebels.

When every rebel is armed, none really is. It’s like when you played GoldenEye 007 as a kid. Getting the Golden Gun the hard way was dope. Everyone getting the Golden Gun with a cheat code made the game suck.

When everyone has the same plug-and-play tools, the profit flows away from the rebels, and towards the arms dealers, forcing rebels to devise new guerilla tactics to take back profits.

Arming the rebels involves picking one side and backing it. Armed rebels often win. Apartheid ended. The Sandanistas lost. The Soviets withdrew from Afghanistan, and then the Soviet Union fell.

Shopify’s merchants, on the other hand, are still in the midst of a bloody battle for customers and profits.

So what is Shopify doing?

Shopify -- and Stripe, Big Commerce, Google, Facebook, FedEx, UPS, Flexport, Anvyl, Boxc, Kustomer, Returnly, Alibaba, and hundreds more ecommerce infrastructure companies -- is arming everyone. Using off-the-shelf software and services, anyone with an internet connection and a credit card can set up an online store and sell things to people.

In many ways, that’s a great thing. Particularly in a period of high unemployment, starting an ecommerce business is one potential way to keep paying the bills. Extremely low upfront costs and easy-to-use tools mean low barriers to entry.

This has major drawbacks for DTC companies that want to achieve scale and profitability, though:

First, low barriers to entry mean more competition, and everyone running around with arms means chaos. It means that it’s a great time to be an arms dealer, and a tough time to be a rebel.

Second, now that nearly every piece of the value chain has become modularized, the battle has concentrated in one place: marketing, via paid acquisition and brand, the only moat left for the vast majority of DTC companies.

Looking at the DTC landscape as a battlefield on which thousands of well-armed rebel groups compete lets us explore a few things:

Why everyone gets rich in ecommerce except the DTC companies themselves

Porter’s Five Forces and Value Chains

Who competition is good for

What DTC brands can do to succeed in an increasingly chaotic space

The Innovation → Software → Curation Cycle that impacts most industries

(Note: I know, I know, DTC is just a channel, etc… but I’m using it loosely here to refer to all CPG-esque ecommerce retail businesses)

Let’s kick things off with a paradox.

Why Does Everyone Get Rich in Ecommerce Except the DTC Companies?

Let me let you in on a little secret that the ecommerce industry is very excited about: COVID pulled ten years of ecommerce penetration growth into three months.

When the pandemic began, we bought 16% of our things online. Now, we buy nearly 34% of our things online. That’s the kind of hockey stick growth investors like to see, and the ecommerce infrastructure companies’ valuations are skyrocketing accordingly. In just the past two weeks:

Shopify crushed earnings. 97% YoY revenue growth, led by 148% growth in Merchant Services Revenue (payment processing and transaction fees that go up when overall spend to Shopify merchants goes up). Crossed $31 billion in Gross Merchandise Value.

BigCommerce, a Shopify competitor, went public and popped 292% in its first day of trading.

Square announced Q2 revenue of $1.92 billion (up 64% YoY) on a 50%+ YoY Gross Payment Value increase.

Ecommerce stocks have popped over the past six months, too:

Etsy is up 169.7%

Shopify is up 118.8%

Square is up 83.1%

Paypal is up 65.1%

Amazon is up 53.4% (to a $1.5 TRILLION market cap)

eBay is up 44.3%.

Even UPS, which delivers so many DTC products, is trading at all-time highs.

Wow - hot space! The whole world is moving online. There must be a ton of hugely successful ecommerce brands, too, right? Ummm…

DTC as we know it was born when Andy Dunn founded Bonobos in 2007. Then came Warby Parker in 2010, Harry’s in 2012, and Casper in 2014. As Len Schlesigner writes in HBR, “The direct-to-consumer startups’ rise was enabled by an environment of abundant venture capital, low competition, and above all, the advertising arbitrage that could be exploited on under-priced social media platforms.”

These early DTC companies were genuinely innovative. They used new technology to invent a new business model. By cutting out the middleman and selling directly to end consumers on their own websites, DTC startups could lower costs, build relationships, and increase lifetime value through repeat purchases. Investors were e-nam-ored! Bonobos raised $127mm in VC, Warby Parker raised nearly $300mm, Harry’s raised $475mm, and Casper raised $355mm. But while funding came easy, strong exits have been harder to come by.

Two of the big VC-backed DTC companies have gone public in the past three years. Casper’s last private valuation in March 2019 was $1.1 billion. It IPO’d at a $470 million market cap in February 2020, and is currently trading near a $350 million market cap. Blue Apron, which raised $200 million in private markets, reached a peak valuation of $2 billion in June 2015. Its market cap is currently $120 million, a 94% decline.

Casper and Blue Apron were too easy to copy. According to CNBC, there were over 175 mattress-in-a-box companies as of last summer. When Amazon filed a patent for “prepared food kits,” Blue Apron’s stock price plummeted 11% in one day.

Increased competition led to more expensive customer acquisition. Well-funded and thirsty for growth, Casper and Blue Apron turned to paid spend and discounts to acquire customers. I know a lot of people who ate free for months by signing up for each meal kit company’s free trial and then canceling and moving on to the next. Scott Galloway pointed out that Casper’s economics would have worked better if they sent you a free mattress stuffed with $300 in cash.

Of course, in typical Prof G fashion, that math is hyperbolic and incorrect -- the $761 COGS plus $300 cash would mean a loss of $1,061 per mattress, while Casper only lost $349 per mattress at the time of its IPO -- but the point stands. Without a differentiated product, forced by their capital structures to grow, and faced with a wave of Shopify-armed competitors, Casper and Blue Apron had no choice but to unprofitably spend their war chests to acquire customers.

The razor industry is the exception that proves the rule.

Razors have really been the only ecommerce category that has had multiple meaningful exits. First came Unilever’s $1 billion acquisition of Dollar Shave Club. Then P&G bought women’s grooming company Billie for an undisclosed amount. Harry’s nearly had the biggest exit of the three when Edgewell bought it for $1.37 billion. I’m biased because Puja worked there, but the fact that the FTC opposed the deal on antitrust grounds is, if anything, proof of Harry’s success.

There’s a reason razors are the exception that proves the rule: you can count with your fingers the number of factories in the world that make high-quality razor blades -- P&G owns one, Edgewell owns one, Harry’s owns Feintechnik, and there are like two or three more in the world. That’s it. Because of limited and hard-to-obtain supply, first-movers in razors had a huge advantage. The unique value chain leads to unique outcomes. In The New Consumer, Dan Frommer made a chart of all the billion-dollar DTC exits.

Somehow, despite massive secular shifts and a lot of noise about rising ecommerce penetration, the DTC products themselves have produced only one billion dollar outcome: Dollar Shave Club (two if you count Harry’s). How can you harmonize those two seemingly contradictory ideas? It comes back to what happens when all the rebels have access to the same weapons, and of course, to Michael Porter.

Five Forces, Value Chains, and DTC

Back in the 1980s, an HBS professor named Michael Porter wrote two foundational strategy texts. In 1980’s Competitive Strategy: Techniques for Analyzing Industries and Competitors, he introduced his Five Forces. In the 1985 follow-up, Competitive Advantage: Creating and Sustaining Superior Performance, he introduced the concept of the value chain. Both are as relevant today as they were then.

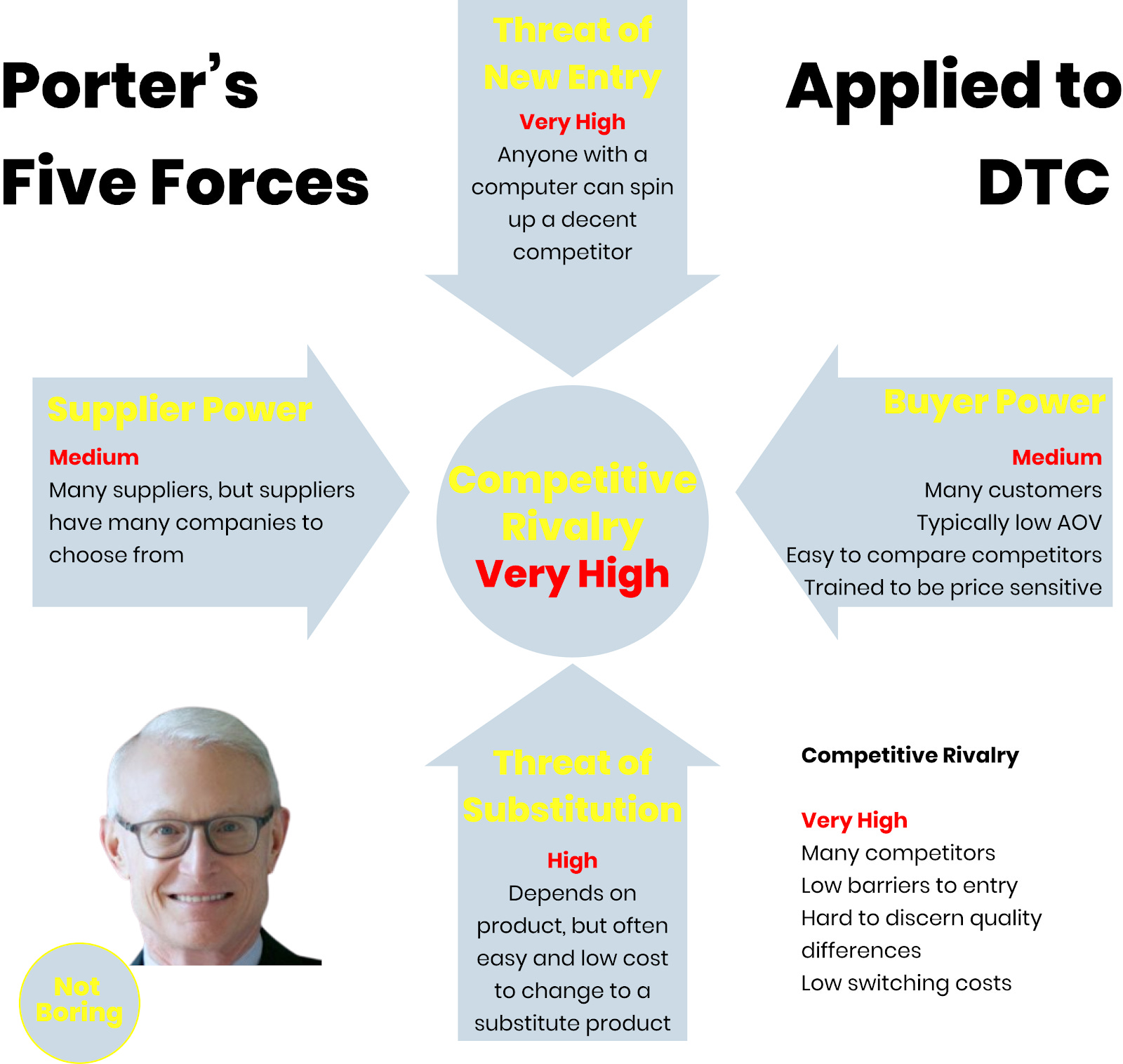

Porter’s Five Forces describes an industry’s competitive dynamics by looking at … five forces: Competitive Rivalry, Supplier Power, Buyer Power, Threat of Substitution, and Threat of New Entry. Oversimplified: the weaker each of the five forces is, the better your competitive position.

Porter’s Value Chain insight is that:

“Competitive advantage cannot be understood by looking at a firm as a whole. It stems from the many discrete activities a firm performs in designing, producing, marketing, delivering, and supporting its product."

Breaking a company’s value chain into its discrete components allows you to think about how the whole business fits together -- what should the company build, what should it buy, where should it differentiate, where is it OK to use modularized or commoditized inputs, and how is each component linked to the others? Getting the combination right means sustained profits.

Value chain analysis and the Five Forces explain the DTC landscape today and provide strategic frameworks support to the Hard Thing About Easy Things.

First, let’s look at the DTC value chain, the set of discrete but linked activities companies perform to deliver products direct to consumers.

Back in 2013, Harry’s integrated R&D, Manufacturing, Retail, and Marketing by designing its own products, buying its own razor factory, selling directly to consumers from its own website, and building a referral engine from day 1 to drive tens of thousands of signups. It is able to create and capture profits because it has a differentiated value chain.

Think about the value chain for a DTC company today, though. Over the past decade, companies have sprung up to build software that allows anyone to do each of the unique things that Harry’s did in-house. There are so many high-quality, modularized inputs, that one person with a computer can spin up a company and start shipping product in under a week.

One more time, just to be clear: you don’t need to know anything other than how to use a few pieces of software to start a DTC brand.

If I were a rebel starting a sunglasses company, let’s call it Rebel Sunglasses, and didn’t want to go through Amazon (the empire), here’s what I would do. I could find and order product wholesale on Alibaba, set up a store on Shopify, drive customers to the site by buying ads on Facebook, Google, and Instagram, either myself or by hiring a growth marketing contractor on Marketerhire, take payments via Stripe, drop ship directly from China with Boxc or import with Flexport and ship with USPS, answer customer questions on Zendesk or Kustomer, and return items via Returnly.

Not all companies do it this way, of course. Many do their own R&D, set up their own supply chain, lease their own warehouses, and acquire customers in novel ways. Some roll their own tech stack to make sure that their tech meets their companies’ unique needs.

But the fact that competitors can easily launch a DTC product means that any one brand’s strategic position, and ability to generate profits over the long-term, is weakened.

To understand why, let’s take the second tool out of Porter’s toolkit: the Five Forces.

By giving all of the rebels and incumbents access to the same weapons, Shopify and the rest of the DTC-enabling software and services make the environment more competitive, and weaken the ability of any individual company to become profitable, particularly at meaningful scale and over a long enough time frame to exit.

Rebel Battle Royale

Let’s go back to my hypothetical company, Rebel Sunglasses. Big things have been happening while you read the past few paragraphs: I launched successfully, used that success to raise money, and used that money to build a big team and acquire a lot of customers. I sold a lot of sunglasses, and proved that customers do in fact like less expensive, well-branded sunglasses delivered directly to their door. But as Biggie and Puff predicted: mo’ money, mo’ problems.

Attracted by my success, More Rebellious Sunglasses launched using the same tools and supply chain that I did, and then MOST REBEL SHADES followed them with the same playbook. Each company stole my look, copied my website pixel-for-pixel, and even priced their products exactly the same as mine. To add insult to injury, Rebel Visors launched a line of visors that, although not an exact ripoff, do the same thing for customers: keep the sun out of their eyes.

All of a sudden, my current and potential customers have four choices: three sunglass companies and a visor company. We’ve all built the same value chain, and we can all move just as quickly. I add new colors, they add new colors. I drop my prices, they drop their prices. I plug in Affirm so customers can buy my sunglasses on credit at a 0% interest rate, theyfollow suit.

This is Entropy Theory to a “T”. Shopify and the ecommerce infrastructure tools create chaos, and that chaos will reign until a company comes in to wrangle it. This is what Shopify’s Shop app may try to do, and certainly what Amazon does on a larger scale.

For companies that don’t want to rely on Amazon, there’s only one place left to compete: paid acquisition. Rebel Sunglasses, More Rebellious Sunglasses, and MOST REBEL SHADES turn to Google to find new buyers, competing for keywords like “Stylish Sunglasses.” We even compete with Rebel Visors for “Keep Sun Out of My Eyes.” AdWords get more expensive for all of us. Then, we all go to Facebook to bid on 18-35 year old American males who live near the beach and like White Claws. Same thing happens - more competition means more expensive customer acquisition, but it’s the only thing we can do to grow. What’s worse, because my competitors’ marketing teams are run by mom and pop founders, inexperience and optimism drive up the prices I need to pay. It’s like playing Black Jack at a table full of drunk amateurs.

This is why 40% of venture dollars go to Google and Facebook - when every piece of the value chain is modularized and easily copied, companies are forced to compete by outspending each other to acquire customers.

It’s also why it’s so much better to be the companies arming the rebels than to be the rebels themselves. Who wins and loses here?

Shopifywins - there are now four paying customers instead of one, and we’re all spending money to grow the market. Shopify takes a subscription fee and a cut of revenue.

Google and Facebook win - we’re all spending a ton of money on ads.

UPS, FedEx, and USPS win - we’re fighting to bring customers online, and more customers shopping online instead of in store means more shipping.

All of the tools and services in the DTC value chain win - more competition means that each of the rebels needs more powerful weapons.

Customers win slightly - they have more choice on the surface, but we’re all offering the same thing, and because we’re paying so much to acquire them, we don’t have room for major discounts now that venture capital isn’t bankrolling us as heavily.

Sunglass and visor companies lose - by fighting against each other, we erode profit margins and enrich suppliers.

There’s a reason powerful countries arm rebels, and a reason platforms do the same: it’s a whole lot easier than getting in the trenches and fighting each fight yourself. Shopify and the other ecommerce tools have an added advantage. Unlike governments, who need to use their own taxpayers’ dollars to support foreign rebels, Shopify gets paid by every side. Shopify has good intentions, but it’s more akin to a war profiteer than a rebel-armer.

The Sunglass Wars are a fictional example of a real battle that plays out every day. Unlike tech companies, which spend a lot of money upfront and then make a lot of money by selling a differentiated product with low marginal costs, DTC brands’ upfront spend proves out what works and then sends out pheromones to new entrants.

This isn’t just a hypothetical. Away, the luggage company, has raised $181 million, most recently at a $1.4 billion valuation. It was noteworthy not just because of its fantastic growth, but because it got profitable very early. That success, of course, attracted copycats, like Monos.

According to LinkedIn, Away has 481 employees. Monos has 24. Away needed to do the hard work to understand what customers want, develop product, educate consumers, figure out merchandising, and even work with the FAA to get suitcase batteries approved. Monos just needed to look at everything Away did, copy it, and buy some ads. Notably, Away is built on Spree Commerce and has a big team building and maintaining its website; Monos is built on Shopify and I can’t find any engineers on their LinkedIn. The websites look and feel the same. And it’s not just Monos. July, Arlo Skye, Roam Luggage, and Paravel all do the same thing, as do countless cheaper knockoffs.

After tens of millions of dollars and the hard work of 481 employees, the only unique weapons that Away has against Monos are brand and bank account. It’s forced to compete with a copycat on the level playing field of keyword bidding and trade margin for growth.

So What’s a DTC Brand To Do?

The Arming of Everyone means that massive scale is likely out of reach for any one DTC company. There won’t be another Nike or Coca-Cola built direct-to-consumer. But there will be thousands or millions of small, profitable DTC businesses built online in the coming years that will make their owners very comfortable, and in some cases, rich.

When all of the rebels are armed, and empires like Amazon and Walmart have scale that new entrants can’t compete with, there are only a few places where startups can win.

The first question to ask is whether you want to go venture-backed or bootstrapped. Neither choice is right or wrong, but everything you do needs to align with the choice that you make and your desired outcome.

Bootstrapped

Nine times out of ten, the answer should be bootstrapped - don’t raise VC, grow slowly, get profitable before all of your credit cards are maxed out. If you’re targeting small niches that you know how to reach without giving all of your margin to Google or Facebook, you can build a really nice business.

If you’re starting from scratch without an audience, focus on high-margin, high Average Order Value (AOV) products that give you a lot of room for costs and let you achieve profitability without reaching a scaled customer base.

If you have a built-in audience that trusts you, you can sell that audience anything that fits your brand and what fans expect from you. Kylie Cosmetics is the canonical example. Kylie Jenner leveraged her massive following to enter the crowded cosmetics space and become a billionaire (kinda, almost). JoJo Siwa sellseverything from bows to dolls to juice boxes to her tween fans. Linear Commerce is a response to overcrowded markets and expensive paid acquisition, and it’s not just for celebrities. Most bootstrapped DTC entrepreneurs should build an audience before they build their first product.

Venture-Backed

If you want to raise venture capital, you need a really good reason besides “to spend money acquiring as many customers as possible via Google and Facebook.” You need to spend that money developing differentiated tech or IP, or a brand that captures a very particular audience that you can sell to an incumbent.

Differentiated Tech or IP

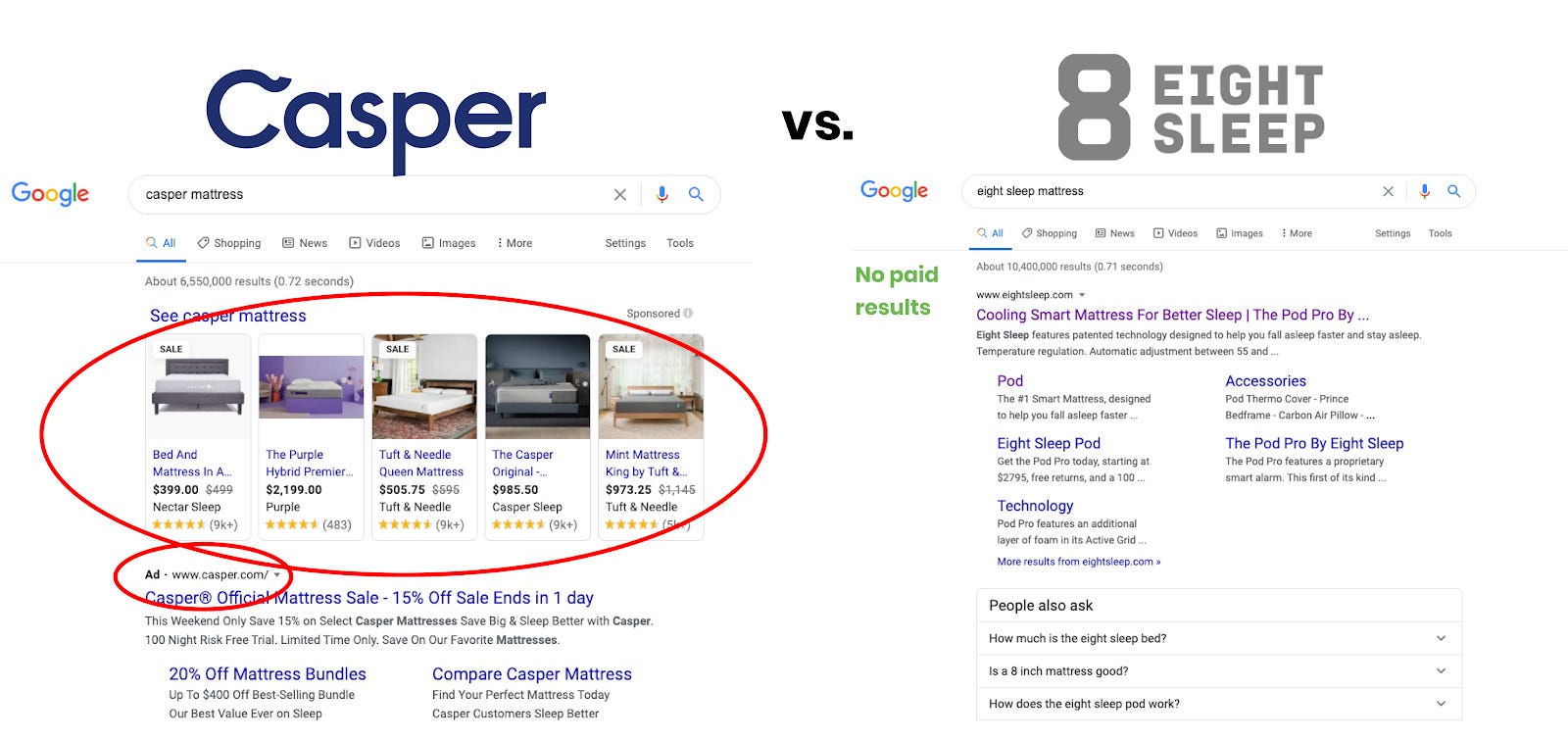

Eight Sleep is a sleep fitness company that has raised $70 million, which should set off alarm bells after reading the Casper section. But Eight Sleep sells more than a mattress, it sells a tech-enabled a sleep system, including a mattress, automated heating & cooling, sleep tracking, and HRV monitoring. Eight Sleep spent its venture money building tech and has five patents that it has used to build a differentiated product to compete on features, not price.

Casper and Eight Sleep’s branded search results tell the story.

When someone searches for “Casper mattress,” the first thing they see is a set of ads for competitors’ products. Casper even has to pay for its own link to show up when someone searches for it. That’s because when someone Googles Casper, what they really mean is “a mattress-in-a-box,” and competitors are willing to spend money to entice the customer to buy their mattress-in-a-box.

When you search for “Eight Sleep mattress,” though, the page is clean. The organic link appears first on the page, and there’s not an ad to be seen. That’s because Eight Sleep’s product is differentiated enough that if I’m searching for it, it’s because I want the Pod sleep system, and a Nectar or Purple mattress won’t do the trick.

Brand That Captures a Particular Audience

The other venture-backable approach is building up a specific audience in hopes of selling it to an incumbent that struggles to reach that audience.

This is the approach that minted Dollar Shave Club its $1 billion exit to Unilever, and on a smaller scale, the reason that P&G bought Bevel, which was aiming to be the “P&G for people of color” for $40 million. At this stage of the DTC game, Bevel’s $40 million exit is more typical than Dollar Shave Club’s now that each of the big CPG companies has made its splashy early play to acquire the DTC skillset and are buying brands mainly for their audiences.

In this approach, companies need to build a product, experience, community, messaging, and ethos that resonates strongly enough with certain customers that they aren’t tempted to buy the knockoff version. If they need to decide between profitability and acquiring a target customer, these companies should choose acquisition, as long as they are able to retain and grow with those customers. Expect to see multiple $10s-to-low-hundred-millions acquisitions that help aging brands acquire Gen Z customers in the next few years.

Ultimately, when everyone is armed with the same tools, differentiation, brand, and audience/community matter for DTC brands more than ever.

We’re All Armed Rebels Now

This cycle holds across industries and verticals:

Innovator does something innovative.

A brave few try to copy the innovator.

Someone builds software to let everyone do that innovative thing.

The innovative thing is no longer innovative.

Everyone does what the innovator did, making it hard to stand out and shifting the battleground to audience-building and brand.

Curation becomes important.

Next innovator comes along and does something innovative, and the cycle starts again.

It’s happening in newsletters, where Substack gives writers an easy way to try to become the next Ben Thompson. It’s happening in video games, where Epic Games is building the tools and literally giving them away for free to expand the Total Addressable Market. It’s happening in AI, where OpenAI is giving everyone GPT-3 to build on top of.

Substack, Epic, OpenAI, and Shopify don’t need to pick the winners. They benefit from their customers spending their own time and money to bring audience to their platform. They sit back and happily take a cut.

It also happened in video, when YouTube made it easy for anyone to become a creator. Then TikTok came along, and became the curator, and is capturing the massive value that comes with wrangling all of that entropy.

The best way to make money in a war is to sell weapons to everyone. It creates its own demand. If the enemy has the best weapons, you’d better have them too. Once everyone is armed, the next opportunity to make money is to bring order to the chaos.

I’m long Shopify -- arming everyone while convincing each of them that they’re the rebel is great business -- and I’m on the lookout for the curation innovation that lets the best DTC companies go around Facebook and Google and rise to the top.

Thanks to Puja and Dan for editing and helping me sound like less of an idiot on ecommerce.

If you enjoyed this piece, help spread the word by sharing it on Twitter, LinkedIn, or wherever you talk ecommerce with your rebel friends.

Quick note: this week, we’re not going to have a Thursday edition. See you next Monday!

Thanks for listening,

Packy