Rivian: The Most Remarkable Adventure

A Deep Dive Into the 12-year-old, Amazon-backed, EV Adventure Company

Welcome to the 552 newly Not Boring people who have joined us since Monday! Join 83,196 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts (shortly)

Hi Friends 👋,

Happy Thursday! This is a unique one over here at Not Boring: it’s a Sponsored Deep Dive (you can read more about my Sponsored Deep Dive selection and thought process here), but it’s not sponsored by the company I’m writing about. I’m writing about Rivian’s IPO, but the piece is sponsored by SoFi.

Before we get to the piece itself, I want to say a few words about why I’m writing it.

SoFi is the only place regular retail investors can buy IPO shares of Rivian at the same time as the institutions. Retail investors getting IPO access is a new phenomenon, so we need new resources.

A typical Initial Public Offering follows the same pattern:

A company decides to go public.

That company chooses a syndicate of investment banks as its underwriters, including a lead-left underwriter, the bank responsible for running the process.

The banks help the company file an S-1, the offering document full of company details and the narrative they’re trying to tell the market, and run a roadshow for the company, in which the company’s management team pitches itself to prospective institutional investors.

Investment banks release research reports that they give only to their institutional and high net worth (HNW) clients.

All of the underwriters get an allocation of shares, which they sell to their institutional and HNW clients at an agreed upon listing price to support the IPO. Typically, the company wants investors who aren’t just going to turn around and sell their shares immediately.

On IPO day, shares start trading, and retail investors, like you and me, are able to buy shares from the institutions and HNW individuals who bought them directly from the investment banks.

Nasdaq laid it out clearly in this graphic:

The problem is, if you’re a retail investor, you’re probably going to pay significantly more than the institutions and HNW individuals. That’s a big part of the IPO pop: the difference between the price at which the institutions buy and where the stock closes its first day of trading. According to Nasdaq’s Jay Ritter, the average IPO pop from 1980 to 2020 was 18.4%. It was even higher for tech companies -- 31.2%!

If you follow Benchmark’s Bill Gurley on Twitter, you know that he thinks the IPO pop, and the whole IPO process, is bad for companies. It means tech companies earn 30% less cash than they could for selling the same number of shares directly to the market. It’s also bad for retail investors, like us. It means that we can pay a 20-30% premium to the prices that well-connected institutions paid just hours earlier!

(This should go without saying, but not all IPOs pop! Some crash. DYOR.)

The trade that the companies were making was that they believed that these large institutional buyers would support the offering and hold the stock, giving them sturdy investor bases who would stick with the company and support its price in the public markets.

The traditional IPO model was built for a different time, when private companies were less well-known to investors, and when retail investors were less active direct market participants. Now, software is eating the markets, and retail is getting involved.

And the IPO process is changing, too.

When Rivian, which makes electric trucks and SUVs, goes public next week, two groups will be able to invest in the companies IPO shares at the listing price in addition to the usual suspects:

People who are on the waitlist to buy its trucks and SUVs, through a directed share program (DSP) -- Rivian is setting aside 7% of shares for pre-orderers!

Retail investors who use SoFi.

That’s why we’re here today. I partnered with SoFi to give my take on Rivian and the company’s IPO. Institutions and HNW individuals have access to sell-side research reports; you’re stuck with me.

Rivian’s IPO will be one of the biggest and most hotly-anticipated of the year. SoFi will have no trouble finding buyers to fill its allocation. But this is the very early innings of a transition in which retail investors will hopefully get more and more access to IPO shares in the best deals. Companies are often nervous about retail investors, though. They’re worried we’re less likely to hold shares and more likely to sell on a pop. In order for retail to get more direct access, we need to not fuck it up. That means understanding what we’re buying, or not, and why. Knowledge makes the diamond hands.

So today, we’ll explain the Rivian thesis and some risks so you’re ready.

Disclaimer: This is not investment advice. I am not a registered investment adviser. We don’t know where Rivian will price. You should do your own research. This is just a starting point.

Let’s get to it.

Rivian: The Most Remarkable Adventure

I’ll tell you this about Rivian’s R1S SUV and R1T pickup truck: they drive.

It shouldn’t need to be said, but thanks to Nikola Motors, it does. Last year, in the face of growing skepticism over whether or not its Nikola One truck actually worked, Nikola released this promotional video, “Nikola One In Motion”:

Looks cool. Great music. Inspiring. The truck was, as promised, in motion. Just one problem.

According to Hindenburg Research, “the video was an elaborate ruse—Nikola had the truck towed to the top of a hill on a remote stretch of road and simply filmed it rolling down the hill.”

Nikola was a black eye on the electric vehicle (EV) space. Rivian is a bright spot.

Not only does Rivian’s R1T drive, it drives really well. Kelly Blue Book gushed, “Not only is it a new kind of pickup truck, it is an excellent pickup truck.” MotorTrend was even more glowing, calling the 2022 Rivian R1T, “The Most Remarkable Pickup We’ve Ever Driven.”

Rivian’s mission is to keep the world adventurous forever, which it’s doing by creating downright sexy electric pickup trucks and SUVs capable of handling rugged terrain and jumping from 0-60 in 3 seconds.

After twelve long and winding years, the company is expected to go public next week. It’s planning to raise roughly $8 billion by selling 135 million shares at a price between $57-62 per share, which would represent a fully diluted market capitalization ((expected shares outstanding + options) * share price) of $55 - 60 billion, down from the $80 billion that’s been rumored since the company released its S-1 in the beginning of October.

That would put it right in line with Lucid Motors, which shot up to a $63 billion market cap after it announced that it would be making the first deliveries of its $169k Air last weekend. Lucid is currently valued at a little over $59 billion.

Rivian also just announced that it made its first deliveries of its R1T pickup trucks in October, the first of its three models to come to market. Its R1S SUV is expected to hit the streets in December, and its EDV delivery van, of which Amazon has ordered 100,000 through 2025, is scheduled to start delivering your packages in 2022. As of Halloween, Rivian has 55,400 pre-orders for the R1T and R1S.

Then there’s Tesla. The 800 lb gorilla in the EV space has delivered 627,350 cars this year through the end of Q3. It’s run by Elon Musk, the first person in the history of the world to be worth more than $300 billion, a record he broke last week after Tesla broke a $1 trillion market cap for the first time. He makes Bill Gates look poor.

A week later, Tesla is worth $1.16 trillion. It’s added more than two Rivians to its market cap in single-digit days.

The EV market is hot. Many would argue it’s overheated. People have been screaming that Tesla is overvalued since I originally bought (and sold) TSLA in 2013. They’ve probably been right the entire time, and they’ve lost money practically the entire time. Elon has burned the shorts.

People have learned not to bet against Elon, and the other EV companies have been beneficiaries. Remember Nikola? The one whose founder was forced to resign and charged with securities fraud? Even Nikola is worth $5 billion.

The EV industry is the double-beneficiary of the government’s largesse: first, because the government offers tax incentives and subsidies to support the manufacturing and purchase of green vehicles, and second, because low rates and a tireless money printer have propelled the prices of growth stocks.

That’s the backdrop against which Rivian is entering the market. It’s perfect timing for a company and a founder who have taken 12 years to reach this point.

Rivian has no revenue; that’s been well-covered in the press around the IPO. It expects to lose $1.2 billion in Q3 this year as it begins delivering pickup trucks. It will need to spend roughly $5 billion to bring on its next production facility. It’s facing chip shortages that could lengthen delivery delays, and well-funded incumbents who are going all-in on electric trucks. It has no revenue. And yet, it will go public at a nearly $60 billion valuation. That seems outlandish on its face.

But the company actually has a path to upside from there. It’s entering an electric pickup truck and SUV market that is temporarily wide-open. More than 70% of cars sold in the US are pickups and SUVs. The reviews for the R1T have been universally slobbery. And in a market in which companies are valued on a multiple of projected 2025 sales, it has a feasible path to growing into its valuation… if it does everything right.

Plus, its backed by Amazon, its largest customer, and Ford, lending credibility and expertise to the company’s manufacturing chops.

This is not a flash in the pan. It’s worth digging in. Like any company, there’s a price at which it makes sense to buy Rivian, and a price at which it doesn’t. That’s not for me to decide for you -- this isn’t investment advice -- but we’ll cover some of the things you’ll need to make up your own mind:

Setting the Stage

The Long and Winding Road to Rivian

Rivian’s Reviews

Evaluating Rivian

Ladies and gentlemen, start your engines.

Setting the Stage

We’ll get to the story of Rivian and all of the juicy details of the EV market in a minute, I promise, but before we do, it’s worth making sure that we’re all on the same page. There are a few facts that will be important to keep in mind and some simple factors that will contribute to Rivian’s value.

First, the facts.

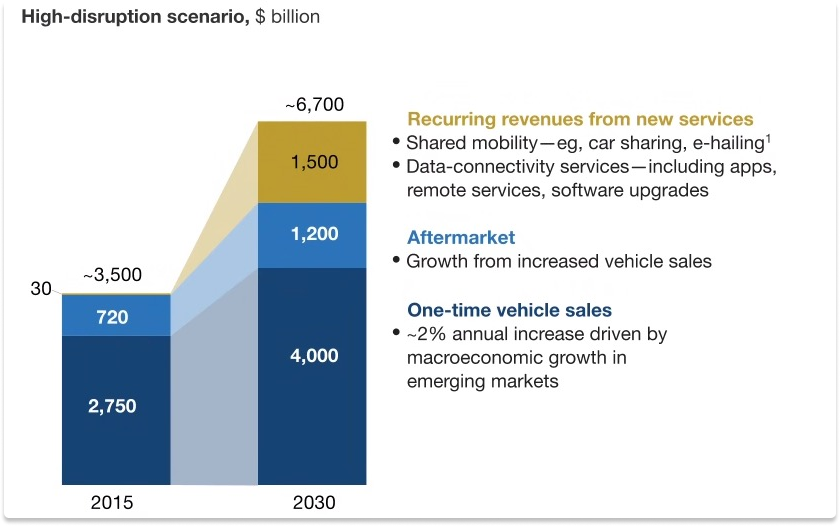

The global automotive market is massive. McKinsey estimates that by 2030, there will be $4 trillion in annual vehicle sales, plus the potential for an additional $2.7 trillion in aftermarket and recurring revenue.

Light trucks are the biggest chunk of the auto market in the US. In 2020, the light truck category -- pickups, vans, and SUVs -- represented 72% of US sales, and IHS Markit expects that share to grow to 78% by 2025.

EV penetration will reach nearly half of all cars sold globally by 2040. Goldman Sachs recently revised its EV penetration and sales estimates upwards significantly, thanks in large part to stricter environmental regulations in the EU and the Biden Administration’s plan to support EVs. They forecast that EVs will make up 11% of global sales by 2025, 25% by 2030, 35% by 2035, and 47% by 2040.

By 2030, Goldman projects that 26.4 million EVs will be sold worldwide each year, up 8 million, or 43%, from its previous projections.

Putting it all together, it seems like a pretty great time to be selling electric light trucks (and services attached to them).

Rivian itself views its market opportunity as all consumer vehicles, not just electric ones or light trucks. In the S-1, it calculates its consumer TAM as all of the cars sold in a year globally, multiplied by its average selling price plus the $67,900 in additional lifetime revenue from selling services, for a total of $8.3 trillion. It’s serviceable addressable market (SAM) is the same thing, just limited by the total number of cars sold in its near-term markets: US, Canada, and Western Europe.

That’s a very aggressive definition of TAM, but no matter how you slice it, the market is large enough to support multiple hundred-billion+ dollar companies.

Then, there’s the market conditions.

Propelled by a combination of those global demand tailwinds and Elon Musk’s awkward charisma, the market for EV stocks has been even hotter than the market for the cars themselves. Tesla is up over 200% in the past year. Lucid Motors, which went public via SPAC, is up 284% from the SPAC’s price before rumors of a merger circulated in January.

Tesla and Lucid are up 51% and 48% in the last month, respectively, thanks to strong Q3 earnings from Tesla and Lucid’s announcement that it was making the first deliveries of its cars. This is a market that is looking for good news from EV companies.

At a $60 billion market cap, Lucid is trading at 27x projected 2022 revenue, 10.8x projected 2023 revenue, and 4.3x projected 2025 revenue.

Tesla is trading at 16x estimated 2022 revenue and 13x estimated 2023 revenue, based on consensus estimates compiled by Atom Finance.

Finally, there’s Rivian itself.

A $60 billion market cap on a company with $0 revenue seems silly, but based on the market, you can actually pencil your way there pretty easily.

The rules of the game, as the market currently stands, are clear. Rivian’s closest EV comps, Lucid and Tesla, trade at somewhere around 10-13x projected 2023 revenue, and Lucid is trading at 4.3x projected 2025 revenue. There are short-term pops to be had just from hitting targets and delivering vehicles on time.

The big question for Rivian is whether it will be able to stick to its production and delivery targets over the next 3-5 years. It sounds simple, but that’s the current equation: make and sell cars on time.

Where you’re willing to buy $RIVN depends on how many cars you think it will be able to deliver in the next 3-5 years, and on whether you think revenue multiples will compress or expand. I have no idea on the latter, I sadly lost my crystal ball. But we can work our way into the former by looking at its production capacity, demand, and average selling price, which we’ll do a little further on. Quick preview, so you have it in mind:

For a $60 billion valuation to make sense, given current multiples and Rivian’s average selling price of $78k (including recurring revenue), you need to believe that Rivian will deliver roughly 67k vehicles in 2023 and 192k vehicles in 2025.

Amazon, which owns 20% of Rivian, has an order in for 100k EDVs through 2025, and Rivian has 55k pre-orders. That’s a great start. Now it needs to deliver.

With all of that context under our belt, let’s jump into Rivian’s story shall we?

The Long and Winding Road to Rivian

If Rivian Founder and CEO RJ Scaringe had a conductor’s baton to which the whole world responded, he couldn’t have conducted a more perfect environment in which to begin delivering electric pickups and enter the public markets. But this was not planned from the beginning. RJ just wanted to make cars.

In a February 2019 Forbes Wheels profile, RJ said that his love affair with “things that move” began when he was a kid. “As soon as he was old enough to handle tools,” Forbes wrote, he helped a neighbor rebuild Porsche 356s in his garage in Melbourne, Florida.” His father, Robert, is also an engineer, according to Bloomberg Green, “with a scrappy shop called Mainstream Engineering. There, the elder Scaringe invents stuff largely for the Department of Defense: diesel engines, water-processing units and a system to make medical-grade oxygen from ambient air, to name a few.”

By high school, he knew that he wanted to build his own car company. A lot of teenage boys love cars, but RJ was serious. He went to Rensselaer Polytech (where he was #1 in his class), then to MIT for a masters in mechanical engineering, then did his PhD in Mechanical Engineering at MIT’s Sloan Automotive Lab. Then Rivian. That’s it.

I dare you to find me a cleaner or more singularly focused LinkedIn profile.

No face. Just Rivian, MIT, and MIT. The man’s only interest is Rivian. He tweets about one thing and one thing only. You guessed it. Rivian.

Here’s how he told The New York Times he spends his time: “‘Rivian is 100 percent minus family,’ Mr. Scaringe said, estimating that his wife and children get 5 percent of his time.”

That kind of focus is required to build a car company. The road to what Rivian is today has been rocky. It wasn’t even called Rivian when RJ started his car company in 2009, fresh out of MIT.

Running out of his dad’s engineering shop, he called it Mainstream Motors. And Mainstream Motors didn’t make electric trucks. RJ and his team of 15 designers and engineers planned to build a high-performance, fuel-efficient sports car that would sell for less than $25,000. After a year of building, they had a prototype that Bloomberg Green described as looking “like a Honda hatchback in a gawky teenage phase.” RJ tried to use the prototype to raise money to no avail, and ended up scraping together $3.5 million when he and his father mortgaged their homes and the State of Florida chipped in some funding.

The next couple of years were a cycle of pivots to new ideas and investor meetings, all unsuccessful, including this sports car design:

Around that time, Mainstream laid off employees and rebranded to Averra, then Rivian. And RJ continued to try to raise money, which took him to the Saudi Arabian desert, where he met fellow MIT alumnus Mohammer Abdul Latif Jameel, CEO of Abdul Latif Jameel (AJL), which owned and operated car dealerships across the world. Bloomberg Green described the meeting:

He was sitting on a rug in the Saudi Arabian desert, surrounded by smoky hookahs and dusty Toyotas. Over tea and sweets, Jameel’s son, Hassan, gave Scaringe homework: Design an efficient, rugged pickup — the lovechild of a Ford F-150, a Toyota Prius and a dune buggy.

In the intervening months, AJL, which had decided to invest, agreed to let RJ build a luxury truck instead of a desert one. One day, RJ walked into a board meeting and said, “I’ve made the decision this will be an all-electric vehicle. We don’t need to discuss this further.”

The green focus was new for Rivian, but not for RJ. According to Wired, while at MIT in 2006, RJ wanted to see what it would take to eliminate his carbon footprint:

How much would you have to change—and how fast, for how long—if you desired to wipe away the carbon traces of your everyday life? Scaringe decided to conduct an experiment, using himself as the subject. For months, he walked, biked, or used public transportation wherever he went. He took cold showers, washed his laundry by hand, and traded his dryer for a clothesline. When he ate out, he brought his own spoon, to cut down on plastic waste.

Thus, combining its founder’s distaste for carbon emissions and his love of cars, the real Rivian was born.

It was a high-leverage bet: light trucks are the best-selling vehicles in the US, and SUVs have done more to increase CO2 emissions in the past decade than planes, cargo ships, or heavy industry. Fix light trucks, help fix the planet.

New marching orders in hand, the team got to work on the all-electric trucks. In 2017, Rivian purchased an old Mitsubishi factory in Normal, Illinois. Long bottlenecked by cash, Rivian raised $200 million in Debt in May 2018. That November, RJ and, of all people, Rihanna (she was dating AJL’s Hassan at the time), unveiled the Rivian R1T to the world.

RJ’s initial fundraising hunch had been right: show investors the right prototype and they’ll come flocking. Now, he had the right prototype.

In February 2019, after Jeff Bezos himself spent a day at Rivian’s Plymouth, Michigan office, Amazon led a $700 million round in the company. The TechCrunch article announcing the deal mentioned that the company had grown to 750 employees.

Amazon’s involvement set off a blizzard of investment.

Ford and Cox Automotive each led rounds in 2019, and in September of that year, Amazon, which owns 20% of Rivian, announced that it would buy 100k vans from Rivian, the largest EV order in history. Then T. Rowe Price backed up the … truck. The asset manager led three rounds totaling $6.5 billion over thirteen months. This past July, D1 Capital joined existing investors in a $2.5 billion round.

Rivian’s S-1 revealed the company’s full investor list, and it includes the largest asset managers in the world: PIMCO, Fidelity, Blackstone, Third Point, BlackRock, TD, Mutual of Omaha, MassMutual, Coatue, Prudential, the pensions of Xerox, Delta, American Airlines, Costco, L’Oreal, Toyota, Kaiser Permanente, Johnson & Johnson, and Ohio’s engineers. The list goes on, but it’s as blue chip as blue chip gets. IPO investors will be joining some of the world’s deepest pockets and most sure-handed capital.

$10.7 billion is a lot of money for any company to raise, let alone a private one which at the time had never delivered a product to a customer. The reason? It’s really honking expensive to build a car company, especially one that’s taking a fully vertically integrated approach like Rivian is.

It’s building everything from factories to batteries to its skateboard platform to a national charging station and dealerships. Let’s take a quick look.

Rivian’s Vertically Integrated Products

When Forbes Wheels asked why it took over a decade to produce its first vehicle, RJ replied simply, “We’ve been getting all the pieces lined up.”

There are a lot of pieces. In its S-1, Rivian highlighted the breadth of its capabilities: it does the vast majority of its own R&D in-house, including its own batteries, chassis, Advanced Driver Assistance Systems (ADAS), fleet management software, and more, plus all of its own manufacturing, financing, insurance, vehicle services, and charging network. All backed, of course, by data and analytics.

Rivian offers both consumer and commercial vehicles, and believes that doing both in a vertically integrated, direct to consumer model creates a flywheel.

Rivian will make three vehicles to start: the R1T pickup truck, R1S SUV, and EDV delivery van.

The R1T starts at $67,500, the R1S starts at $70,000. The EDV’s price is undisclosed, but the target customer is clear: Amazon will be the only customer anyway through at least 2025 (Amazon has a two-year option to extend after that).

Both the R1T and the R1S are built on Rivian’s proprietary skateboard chassis, which houses its batteries, motor, and electric components. Each wheel is powered by its own motor.

Part of the chassis is its proprietary battery, the expensive ($10k add-on) version of which will last up to 400 miles on a single charge (Tesla’s longest-lasting goes 405 miles). The standard version will run 300 miles. The company has said that it may also sell or license its skateboard chassis and battery to other car manufacturers. Ford, which owns 12% of the company, is a potential licensee of the technology.

Every one of Rivian’s trucks, SUVs, and vans will be manufactured in the 3.3 million square foot Normal, Illinois plant that it bought from Mitsubishi in 2017.

When it gets to full capacity, the plant will be able to produce up to 150k vehicles per year (with the ability to expand to 200k with some adjustments). The company plans to expand the facility as it introduces new models on the R1 platform by 2023. According to InsideEVs, Rivian expects to fill its pre-order backlog of 55,400 by that same year, in addition to roughly 30-40k of the vans that it owes Amazon, and any orders that come in between now and the end of 2022.

But even with expanded capacity in Normal, Rivian will need to expand. Since this past summer, it’s been on the hunt for a second factory. Rumors suggest the company will follow Tesla to Texas, where it has its eyes on Fort Worth digs. The new plant would cost $5 billion to get up and running by 2024, and would provide capacity for an additional 200k vehicles per year. Bloomberg, which has been strong on the Rivian beat, also reported that the company is searching for its first European plant, which it hopes to bring online by 2023.

From the factory, Rivian’s R1T and R1S will get to customers in two ways, both direct-to-consumer: online and through Rivian’s own network of showrooms, a la Tesla. Going direct-to-consumer, as in all industries, will allow Rivian to save costs and give customers a more brand-controlled experience. It’s planning to open Hub showrooms in Chicago, Brooklyn, Bellevue, Denver, and LA, among other locations.

It’s worth noting that in March, Rivian was sued by car dealers in Illinois who claim that manufacturers are not allowed to sell directly to consumers. I’m no lawyer or judge, but that sounds like the dying gasps of an old model.

True to its mission to “Keep the world adventurous forever,” and its target demographic of affluent outdoors lovers, Rivian will also set up Outposts in adventure destinations where people can rent Rivians and push them to their limits, and Preserves, protected land that Rivian will conserve and on which it will provide vehicles for community use.

Rivian also offers a range of post-sales solutions, which McKinsey would bucket under “recurring revenues from new services,” including:

Rivian Cloud: Rivian can deliver remote diagnostics, vehicle controls, and software updates, powered by AWS (of course, Amazon wouldn’t invest without tying AWS to the deal).

FleetOS: For EDV customers, FleetOS is a full suite of tools to help owners manage their fleets, from tracking vehicles to remote diagnostics to safety training to collision reports.

Driver+: Driver+ is Rivian’s Advanced Driver Assistance System (ADAS), which is currently capable of level 2 autonomy. Rivian is not as advanced as Tesla, which hopes to get to fully autonomous level 4/5 vehicles, but will support level 3 via a software update when available.

Rivian Financial Services: Rivian customers can finance their vehicles through Rivian, a common feature among large car companies, in partnership with Chase.

Rivian Telematics-Based Insurance: Rivian will offer auto insurance to its customers, and will be able to offer lower insurance rates for safe driving, tracked through its telematics.

All of these features mean sweet, sweet recurring revenue, and Rivian expects to make an additional $67,900 per customer over ten years.

Rivian is even rolling out its own charging network, the Rivian Adventure Network, across the US and Canada.

It plans to roll out 3,500 DC fast chargers (140-mile charge in under 20 minutes) in 600 locations through 2023. It will also have Waypoints, slower chargers at partner destinations like hotels, restaurants, and parks, throughout the US and Canada. Rivian is only the 3rd EV company, besides Tesla and China’s NIO, to roll its own charger network. It’s an expensive and slow proposition, and may be frustrating for drivers as it builds out the network, but the company hopes to make charging accessible in places where no EV has dared travel before.

All-in, it’s a capital intensive proposition for which the company will likely have raised just shy of $20 billion when the IPO is completed next week. What does all that money get you?

Rivian’s Reviews

“I hate to use the word gamechanger, but this is going to change the way pickup trucks are seen.” When Motor Trend reviewed the Rivian R1T in August, they were floored. The headline says it all:

Given that the category responsible for the three top-selling car models in the United States, that’s saying something. For you gearheads, here are some of the highlights (all direct quotes):

Rivian's killer apps are its powertrain and suspension setup

Like many EVs, it is very quick: The two motors at each axle deliver 415 horsepower and 413 lb-ft of torque to the front wheels and 420 horses and 495 lb-ft to the rears, and Rivian claims a 0-60 time of 3.0 seconds. We've yet to turn an R1T over to our test team, but we think that number is eminently possible.

A motor powering each corner also means remarkable agility on- or off-road.

We felt the R1T's torque-vectoring superpowers at work: The outside-rear motor powered up and brought the R1T's nose around, and we blasted out of the turn like the Millennium Falcon.

It's a sensation we've experienced in only a handful of cars, and never in a heavily laden pickup truck.

Off-roading in the R1T is a mind-bender.

I could go on, but words don’t do it justice. Watch the review video for yourself:

Tech reviewer Marques Brownlee (MKBHD) called Rivian “the most impressive electric truck I have ever seen” and “the most interesting of all of” the EV companies.

He also pointed out that under the center armrest, there’s a whole bluetooth speaker that charges the whole time you’re driving (Rivian knows its audience), among many other delightful features targeted at the outdoor, adventurous set:

Kelly Blue Book (which is owned by Rivian investor Cox Automotive) was equally blown away. The reviewer praised the interior, saying “There is a finesse here that feels drawn from beyond the automotive realm.” Watch the review here:

KBB called out the gear tunnel, an 11’ storage space for long items like skis, as particularly unique.

Also notable is the fact that the YouTube commenters, a typically snarky bunch, seem genuinely excited for Rivian’s products.

We like the trucks! Do we like the stock?

Evaluating Rivian

Headlines like “Rivian Expected to Go Public at $60 Billion… With No Revenue” grab eyeballs, but they miss a lot of the story. Rivian is in year 12 of a multi-decade journey to build excellent vehicles that “keep the world adventurous forever.”

There are two parts to that: adventurous and forever. Rivian’s vehicles are the first EVs built for off-road adventure, and the more people who buy a Rivian instead of an internal combustion engine (ICE) pickup truck or SUV, the better it is for the environment. In addition to the product’s environmental impact, Rivian the company is making a financial pledge:

We are putting 1% of Rivian’s equity into Forever, providing it with a substantial and growing financial platform to focus on high impact climate initiatives with an emphasis on preserving and restoring wildlands, waterways and oceans.

If you associate EVs with SPACs and get-rich-quick schemes, get that idea out of your head when evaluating Rivian. It’s going public via a traditional IPO, backed by the world’s bluest-chip institutional investors, and giving away 1% of its stock.

So if its target price range isn’t just the result of EV market froth and greed, how should you think about where $RIVN is worth buying?

In this market, it’s going to come down to the company’s ability to generate demand in the face of coming-soon competition from incumbents, and its ability to meet that demand and deliver vehicles. Remember, given current multiples, a $60 billion valuation at the top-end of its range means that Rivian will need to deliver roughly 67k vehicles in 2023 and 192k vehicles in 2025.

What could get in the way of that happening?

It might not be able to generate that much demand for its vehicles.

If it can generate the demand, it might not be able to produce and deliver enough to meet it.

Let’s start with demand.

While there are other EV companies, and other light truck manufacturers, Rivian is actually targeting a unique audience among EV competitors:

Tesla’s Model X starts at a higher price point and is better suited for the city and suburbs instead of the mountains.

Ford’s F-150 Lightning is aimed at the workers who currently drive F-150s, and is expected to price around $40k.

Tesla’s Cybertruck is targeted at robots, I think.

The closest competition for now might come from the GMC Hummer EV when it delivers later this year or early next.

Adventurous affluent might seem like a small group to go after first, but it makes a lot of sense as an initial wedge. The people who love the outdoors the most are likely the ones who would be willing to pay a little more for a car that helps protect the environment, and the most likely to jibe with Rivian’s brand and ethos. They’re also dramatically underserved in the EV space: there is no other EV on the market currently that can handle rugged terrain. There will be others, but Rivian will have the market to itself for a while.

Plus, we know that there’s demand. There are 55,400 pre-orders as of October 31st, up 14.5% from the end of September, likely driven in part by increased visibility from the IPO. Expect the pre-orders to roll in over the next week as it gets more free press and attention.

Plus plus, Rivian has 100k vehicles on order from Amazon, likely rolling out with 10k in 2022 and then 30k for each of the next three years. Assuming that Rivian fulfills half of its consumer pre-orders in 2022 and half in 2023, it already has 55k of the 67k vehicles it needs to deliver in 2023 accounted for from the demand side.

Given Rivian’s reviews and pre-orders, the fact that Rivian hasn’t even really rolled out its showrooms yet, and the fact that it’s planning to expand to Europe in 2023, I don’t think it will struggle to hit the required 192k orders it will need to reach by 2025, or even 50% above that to give it cushion assuming that multiples contract. The value of a high-quality product is that it should lower customer acquisition costs by increasing word of mouth.

As a sense check, if Rivian hits that target and generates $15 billion in revenue in 2025, that would represent about 3% of global EV revenue (McKinsey’s $6.7 trillion x Goldman’s 11% EV penetration), or 0.7% of total EV units sold globally (Goldman’s 26.4 million units). That seems reasonable given that Rivian is the de facto leader in the largest vehicle category.

The real challenge, then, will be on the production side.

Assuming that Rivian is able to bring its new plants online when it plans to, and that it ramps up to full production by year two, it should have plenty of plant capacity to meet 2023 and 2025 targets:

Even if EV 2025 revenue multiples got cut in half, and it had to deliver 120k vehicles in 2023 and 400k vehicles in 2025 to justify a $60 billion market cap, it should have the capacity to do so. (Note: these are just rough ballparks to help you think through the math).

But things are always cleaner on paper than they are in reality.

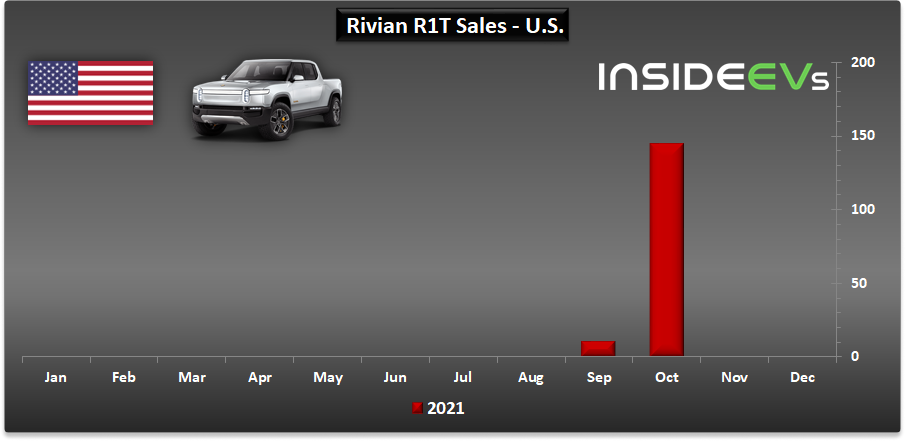

The July 2019 New York Times article timestamped Rivian’s production goals, writing, “While Tesla has failed to reach its own lofty production targets in recent years, Mr. Scaringe is promising only about 20,000 to 40,000 vehicles in 2021, the first full year of production.” The year isn’t over, and it’s impressive that Rivian has even started delivering vehicles in the same year it projected it would, but it looks as if they’ll fall a little short of the 2019 goal.

InsideEVs put out this incredible chart on deliveries thus far, most of which have gone to employees.

Rivian’s official plan, according to its recent S-1 amendment, would have the company deliver 1,025 vehicles this year, including 1,000 R1T, 15 R1S (scheduled to deliver in December), and 10 EDV. It’s impressive that they’re able to deliver in the year in which they said they would, but 1,025 isn’t 20,000 or 40,000.

Rivian’s S-1 has a 50 page section on risks that you should check out before investing that highlights a lot of what you’d expect and what we’ve discussed, like the fact that it needs to generate demand in a competitive automotive market, and that it may not be able to produce trucks at scale, and that material costs could go up or that supply chains could be disrupted. A lot of them have to do with being a new company that hasn’t done any of this before.

A few of the most interesting beyond the basics are:

Key Man Risk: We are highly dependent on the services and reputation of Robert J. Scaringe, our Founder and Chief Executive Officer.

Quality Over Short-Term Profits: Our passion and focus on delivering a high-quality and engaging Rivian experience may not maximize short-term financial results, which may yield results that conflict with the market’s expectations and could result in our stock price being negatively affected.

Pre-Orders Aren’t Money in the Bank: Preorders for our vehicles are cancellable and fully refundable.

The market could turn, too. If EV manufacturers start getting valued on earnings multiples instead of year 4 revenue multiples, it will take a while for Rivian to grow into its IPO price.

But in the market we’re in right now, the $57-62 per share range for Rivian feels fair. It’s spent 12 years completing the really, really hard, question-mark-ridden part of the journey. Now, it has cars on the road. If it hits, or exceeds, near-term production targets, the market will likely respond positively. As the pre-orders grow, the market will likely respond positively.

Deliveries will be the key metric to watch for Rivian. If it stays on schedule, it should perform well. If it misses, it could sink. If it delivers ahead of schedule, watch out.

Plus, Rivian has upside optionality that we’ve barely discussed. Because Rivian’s done all of its own R&D in-house, and owns its own tech, it may be able to sell or license its technology to other auto manufacturers like Ford. It may be able to add on other lines of high-margin recurring revenue, or cross-sell other products to its targeted community of adventurers.

You’ll read a lot of articles about how crazy Rivian’s price is, comparing the company to others like Nikola, but they’re not the same. I hope you come out of this piece armed with the ability to do your own research. You know what to look for: pre-orders and deliveries. Do the work, figure out the price at which you’d be willing to buy, and if it prices the IPO at that price, sign up for SoFi to get access before you have to buy from the institutions.

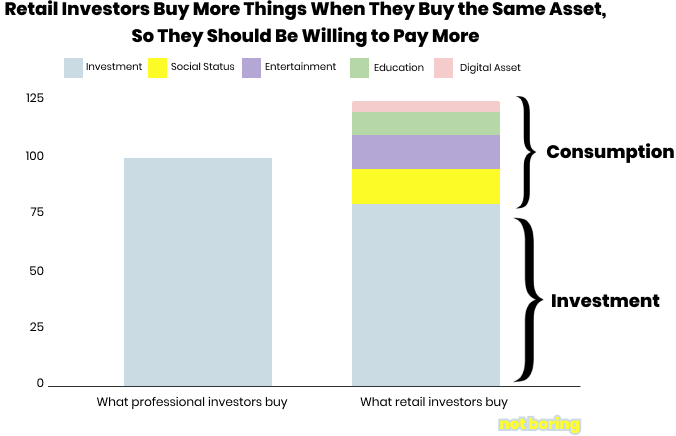

In Software is Eating the Markets, I wrote that retail investors are buying more than just cashflows when they buy an asset.

We’re buying social status, entertainment, education, and a digital asset to show off. NFTs and tokens more broadly have proven that to be true. Rivian, like Tesla, might be a way to express and support a belief that we can unfuck the planet and get better products.

Rivian is a company you want to root for. It’s a founder living out his dream, making cars for adventurers, in America, that are good for the planet. It’s “the most remarkable pickup” Motor Trend has ever driven without guzzling an ounce of gas. Its success means more money for environmental causes. RJ has been working day and night on this for twelve years; we get to hop onboard now that the hardest work is done and participate in its IPO. God Bless America.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Thursday,

Packy

This hasn't appeared yet on Apple Podcasts or Spotify. Any ideas when that might happen? Would love to listen!

Great Article. I think it all comes down to production capabilities. Seems a bit crazy to be looking at two new factories when their existing factory is at the very beginning of the ramp. Another thing I've heard mentioned is the complexity of bringing multiple models to market off the bat (different components, suppliers, production engineering). Will be an interesting story to watch - the EV market is growing rapidly and there's a lot of market share available for the taking. Will come down to Rivian's ability to execute on the production ramps.