Welcome to the 805 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 18,038 smart, curious folks by subscribing here!

💙 Hit the heart at the top to like today’s essay, and if you really love it, share it!

Hi friends 👋 ,

Happy Monday!

I suspect that most of the people reading this newsletter could recite the Facebook, Apple, Amazon, Microsoft, and Google (FAAMG) stories by heart. The American tech giants are widely covered, and rightfully so: they’re the biggest companies in the world, and they’re growing really fast. These companies do everything, vertically integrating and acquiring competitive threats on the path to market dominance.

But there’s a new breed of tech leader emerging in Asia, led by Tencent, Alibaba, and SoftBank, that turn their first acts as product-first companies into second acts as investors. By spreading out their bets, Tencent and Alibaba have made themselves future-proof: they have upside whether customers choose their products or new entrants’, because they own large stakes in the most promising startups. (SoftBank… we’ll see, but I’m bullish.)

Currently, Reliance is taking the western approach, but I think it would do well to follow its Asian neighbors’ lead. The opportunity is just too large for anyone, even Mukesh Ambani, to take on all by themself.

I’ll explain. But first, a word from our sponsor:

This week's Not Boring is brought to you by…

Every Monday after I hit send, Public is the first place I go. Public makes investing social, which means different things for different people. For me, as an eternal optimist, I value having a positive environment in which people smarter than me can challenge my thinking and point out bear cases that my mind just chooses not to see.

After two weeks of writing about Reliance, I couldn't be more bullish on India or on Reliance itself, so it's the perfect time for some friendly pushback and thought-sharpening.

I’ll be discussing today’s essay - including my thoughts on Tencent and SoftBank - and asking people for the bear case on India and Reliance. Join me.

*This is not investment advice. See Public.com/disclosures/.

Reliance’s Next Act

The Cricket Proxy War

Outside of Philly and Duke sports, my favorite sports team in the world is the Mumbai Indians, the Indian Premier League cricket team owned by the Ambani family. If you don’t follow cricket, I highly recommend the Netflix series, Cricket Fever: Mumbai Indians as your gateway.

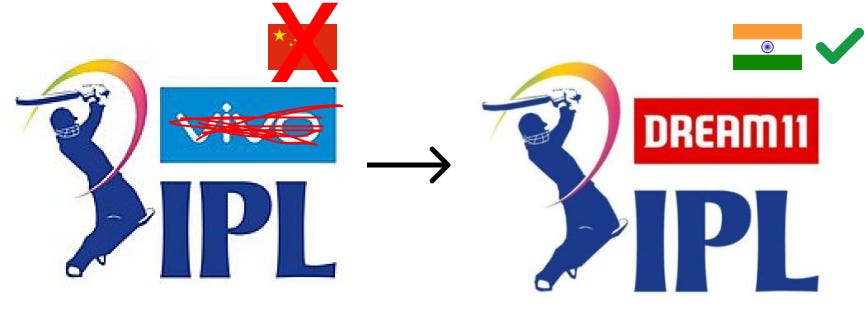

After watching the Indian team in the Cricket World Cup every four years, last year was the first year that Puja and I watched the Indians religiously. We got a Willow subscription and woke up at odd hours to lock in for four hours of high-paced T20 cricket. Every match, in the corner of the screen, we saw this logo:

The Indian Premier League’s logo looks a lot like the league logos westerners are used to seeing -- a silhouette of someone playing the sport with three letters -- with one difference: a title sponsor. In 2019, that title sponsor was Vivo, a Chinese smartphone company.

This year, when the crowdless 2020 IPL season started in Dubai, we noticed a different logo.

Vivo signed a deal to sponsor the IPL through 2022, but amidst the China-India conflicts, India’s cricket board dropped it in favor of a homegrown sponsor. Dream11, the $2.5 billion Indian fantasy cricket startup, took its place.

China was out. India was in. Atmanirbhar Bharat.

Uncharacteristically, Reliance took a backseat on the title sponsorship, but its influence is there, just spread out. Jio is the only company that sponsors all eight IPL teams. Its patch sits prominently on six teams’ jerseys.

It’s just cricket, but when I look at that chain of events, I see Reliance’s future. China’s disappearance from the IPL and Jio’s multiple bets point to Reliance’s opportunity and the approach it should take in the Indian startup ecosystem.

Reliance’s Future

Reliance has a history of vertically integrating, but paradoxically, to capture the most value from the internet, it needs to loosen its grip. Instead of doing everything itself, Reliance should become India’s biggest growth stage investor.

Last Monday, in Reliance: Gateway of India, we covered Reliance’s history and present. Reliance is a sprawling giant that spins cash flow from its legacy businesses into a tech-forward future:

India’s Biggest Company. $202 billion market cap on revenues of $105 billion

New Focus. Reliance Retail and Jio, make up 30% of revenue ($31 billion) but took up the lion’s share of the screen time at the company’s most recent AGM (84%).

Reliance Playbook. Undertake projects with high upfront costs, building complex businesses around them, wrangling Indian supply and demand, spreading out the costs over hundreds of millions of users, leveraging its favorable position with the government, and selling stakes to foreign companies and investors.

Gateway of India. Foreign companies and investors poured $20.4 billion into Jio for a 33% stake and are in the middle of investing in Reliance Retail, which has raised $5.1 billion for 8.5%.

Reliance, which had raised billions of dollars in debt to fund its new projects, now has zero net debt, strong relationships with the world’s largest investors, communications and retail infrastructure that powers India, and the support of the Modi government, with whom it is working to realize PM Modi’s mission of Atmanirbhar Bharat, a Self-Reliant India that takes its place as a power on the global stage.

In Part II of the essay, we’ll cover Reliance’s future and that of the Indian startup ecosystem, which will become increasingly intertwined:

Made by Reliance. Reliance has always vertically integrated. Jio and Retail seem to be following the same path, with homegrown and acquired solutions. That works better for infrastructure than it does for consumer apps.

The Indian Tech and Startup Ecosystem. The bull case for India tech is that it is China, just seven or eight years behind, with better western relations. Realizing the bull case would mean multiple hundred-billion dollar tech companies and trillions of dollars of value creation. As it stands, Chinese investors will capture more Indian upside than Reliance.

Reliance’s Tencent and SoftBank Opportunity. Reliance is well-positioned to become the next Asian mega-conglomerate turned investor. It can follow either Tencent’s or SoftBank’s approach, with a unique Indian spin.

To date, Reliance has only built or acquired, while a thriving startup ecosystem has grown up around, and on top of, Jio. This is Reliance’s opportunity: to become the largest investor in India’s booming tech ecosystem. Investing in Indian startups represents a massive opportunity, but Reliance will need to evolve how it operates to take advantage of it.

Made by Reliance

Owning as much of the value chain as possible is in Reliance’s DNA, but it will need to find some corporate CRISPR to thrive in a time of Jio-powered Indian tech abundance.

As discussed in Part I, Reliance’s history is one of vertical integration. From import licenses on yarn to textiles manufacturing to petrochemicals to petroleum refineries, Dhirubhai Ambani pushed Reliance to own an increasing amount of the value chain.

Mukesh is no different. Instead of selling equity early or entering into JVs to finance his two biggest projects, Reliance Retail and Jio, Reliance raised debt and did the hard work itself, only selling stakes to foreign investors when his new business lines were well-established.

Reliance built out the infrastructure and reduced its net debt to zero, and now, it’s building the devices, OS, and products and services on top of it with in-house or fully acquired technology, or via exclusive partnerships with global tech giants.

In an excellent overview, What is Reliance Jio’s Plan?, Arjun Malhotra of Indian VC Good Capital, described Reliance’s plan to move up the stack with Jio, vertically integrating from infrastructure up to products and services.

Reliance and the global tech companies that recently invested in Jio are working together to build out the full mobile stack:

Infrastructure. Through Jio, Reliance built a wireless data and broadband network across all of India over the past decade. It is now the largest telco in India.

Device. With Google and Qualcomm, Jio is building an affordable smartphone for the Indian market.

OS. Old Jio Phones ran on Linux-based KaiOS, but the new JioPhone will run on Android.

Product/Service. Jio will work with Facebook and its WhatsApp subsidiary to build the Super App through which Indian consumers do everything they need to do online.

When Jio launched its wireless data service in 2016, it launched Jio Chat as its answer to Facebook’s WhatsApp and Tencent’s WeChat. The product looks like a WhatsApp clone. Since then, Reliance has all but abandoned JioChat as its entrant to the Super App battle royale. Its website hilariously features testimonials from 2016 befitting a pre-seed, pre-customer startup and a slapped on integration with its music service, JioSaavn. It reminds me of the Spotify integration I was so proud of building into the website for my party bus company in 2013, just to show that I could (note: I am not an engineer).

Instead, through Facebook’s $5.7 billion dollar investment in Jio, the two companies are forming a partnership that could solidify WhatsApp as India’s Super App. Already, India is WhatsApp’s biggest market, with over 400 million MAUs, and is also the second largest market for Facebook’s Instagram, with 80 million users. But Facebook has faced regulatory hurdles in attempting to expand its Indian offering beyond chat. It has been unable to launch WhatsApp Pay, for example, despite years of attempts.

Luckily for Facebook, jumping over (or through) regulatory hurdles in India is what Reliance does best. Combined, the two companies can offer users an all-in-one platform where they can chat, shop (Facebook Marketplace, Reliance Digital, Smart, Jewels, Trends, etc…), get healthcare (Jio HealthHub, Facebook’s Preventative Health Tool), find things to do (Facebook Local, Network18), and more.

Facebook and Reliance are starting small, in part to assuage concerns that Reliance serves as the conduit through which a foreign tech giant can steal business from local companies. The two are partnering on JioMart (which is itself a partnership between Reliance Retail and Jio), allowing users to order from local kiranas via WhatsApp. Messaging the local kirana for delivery is an existing Indian consumer behavior, accelerated by COVID, that the two companies hope to make more frictionless through their partnership.

From there, it’s easy to imagine a world in which WhatsApp, powered by Jio, becomes the way that Indian consumers access the internet, with the Super App essentially serving as the OS, as WeChat does in China. As I wrote in Tencent: The Ultimate Outsider:

Chinese users do everything on WeChat. They communicate with friends, co-workers, and clients through WeChat. Businesses communicate with customers through Official Accounts. They can also sell things through those accounts. Thousands of businesses, including ridesharing (Didi) and food delivery (Meituan Dianping), launched on WeChat.

Tencent’s approach should be instructive for Reliance. Even though WeChat sits in the most valuable position in China’s mobile value chain, Tencent decided to prioritize investing over building for most categories. In his piece, Tencent Has No Dreams, blogger Pan Luan criticized the company for losing its product focus, abandoning in-house projects in favor of investments. He missed the point. By leveraging its place in the value chain, Tencent could watch battles play out in each category and back the winners instead of building its own category laggards.

Instead of building its own social commerce app, it invested in Pinduoduo.

Instead of building its own local shopping app, it invested in Meituan-Dianping.

Instead of building its own ecommerce store to rival Alibaba, it invested in JD.com.

Recall Ben Thompson’s Bill Gates Line definition of a platform, based on this Bill Gates quote about Facebook as a Platform:

This isn’t a platform. A platform is when the economic value of everybody that uses it, exceeds the value of the company that creates it. Then it’s a platform.

A short-term play to capture as much value as possible from the services on top of a platform has negative long-term consequences to the value of the platform overall. With the right incentives in place, the ecosystem can build better products than the platform owner.

Reliance is right to partner with Facebook to make WhatsApp the platform on top of which the Indian mobile economy runs, but it will undershoot its potential if it continues its attempt to vertically integrate the services on top of that platform.

Today, to name just a few examples, Reliance has built or acquired solutions for:

E-commerce: JioMart

Education

Reliance acquired Embibe to serve as the foundation of its EdTech product

Video Conferencing: Jio Meet

Tencent actually built its own Zoom competitor, VooV, as well

Payments: JioMoney

Launched in August to compete with popular existing solutions like Paytm, PhonePe, Google Pay, BHIM, and Mobikwik

Healthcare: Jio Health

Like Teladoc or Livongo for India

Entertainment: Jio Cinema and Jio TV+

Jio Cinema is Jio’s own OTT streaming service, while JioTV+ aggregates all of the best streaming services (Netflix, Prime, etc…) on a set top box

Music: JioSaavn

Acquired Indian-market Spotify competitor Saavn in 2018

Chat: JioChat

Acquired conversational AI company Haptik to facilitate business conversation on the app

Despite its buying spree and massive budget, Malhotra points out that, as a result, Reliance doesn’t have the leading consumer aggregator in any category it plays in.

Because Reliance has been insistent on building itself, it has missed out on the upside from category-leaders being created in India’s thriving ecosystem. Fortunately for Reliance, and for Indian consumers, it has been handed another gift from the government: a chance to get in the fastest-growing game in town.

The Indian Tech and Startup Landscape

To understand Reliance’s opportunity, you need to understand the Indian tech and startup landscape.

The bull case for Indian tech is that it is China, just seven or eight years behind, with better western relations. According to Dhaval Kotecha, the Indian economy has some major tailwinds and will continue to be one of the world’s most dynamic consumption environments for five reasons:

Income Growth. The Indian economy is expected to grow at 7.5% per year through 2030. The lower-middle and upper-middle classes have grown fastest since 2005, from 23% and 7% respectively to 33% and 21% today. The upper-middle class and upper class are expected to double from 21% and 3% today to 44% and 7% in 2030.

Steady and Dispersed Urbanization. In 2005, 28% of the population lived in cities. Today, 34% do, and by 2030, 40% of Indians will live in cities.

Favorable Demographics. Today, 82% of India’s population is under 50-years-old, and by 2030, 77% of the population will comprise of Millennials and Gen Z.

Tech & Innovation. There will be 1 billion Indian internet users by 2030, driven in large part by Jio, which has reduced data prices by 95% since 2014.

Evolving Consumer Attitudes. As the population skews younger, richer, and tech-friendlier, more commerce will take place online. The online retail market is expected to quadruple, from $30 billion today to $100-120 billion in 2025.

Kotecha highlights that India trails China by 7 years in internet users and 8 years in online shoppers, and that both are on a much steeper growth trajectory than the US.

If India becomes the next China, its tech companies will create massive value over the next decade.

A decade ago, China had four of the ten largest companies in the world by market cap: PetroChina (oil & gas), ICBC (bank), China Mobile (telco), and China Construction Bank (banking), worth a combined $890 billion. Reliance looks similar to that composition - it is both India’s largest energy player and its largest telco.

Today, China has two companies in the global top ten, Alibaba ($831 billion) and Tencent ($688 billion). Both companies drove and benefited from the sharp rise in internet usage and ecommerce in China, and from investing in China’s startup ecosystem early.

Tencent, for example, owns 20% of Meituan-Dianping, which despite being a decade old, is worth as much ($201 billion) as all of Reliance Industries today. Other investments, like JD.com ($127 billion) and Pinduoduo ($100 billion), are worth about as much individually as all of the Indian unicorns are worth today, combined.

Over the past half-decade, India’s unicorn production has accelerated faster than any other country in the world, but it still has a lot of room to run. China, with its ~eight year head start, has 227 private unicorns worth $869 billion, according to Hurun.

Including public companies, Chinese tech companies have created trillions of dollars worth of value. India’s are less than 10% of the way there.

According to CB Insights and Hurun, there are thirty-three Indian unicorns, startups worth at least $1 billion on paper (including Zerodha, which hasn’t raised outside capital and bootstrapped its way to an estimated $3bn valuation). That number includes Flipkart, of which Walmart bought 81% for $16 billion in 2018. Combined, the Indian unicorns are worth $111 billion.

The gap between India and China will close. Today, despite really starting to create unicorns consistently over the past four years, India has more unicorns than any country except the US and China (and potentially the UK, depending on which list you look at).

The Indian startup ecosystem is just starting to hit its stride. Of the 33 Indian Unicorns, 27 crossed the billion-dollar mark since Jio’s launch in 2016. While there are a host of factors, Reliance and Jio have undoubtedly made things better for the tech ecosystem. Indian tech companies refer to their “Jio Moment,” when their user and engagement charts shot upwards because more people were able to access their products.

Startups that are largely building on top of Jio’s infrastructure are beating it across the categories in which they compete:

Flipkart, owned by Walmart, has a head start on JioMart in ecommerce, as do companies like Jumbotail on the grocery wholesale side and Facebook-backed meesho in social commerce.

Alibaba-and-SoftBank-backed Paytm has 150 million users and is valued at $16 billion.

Byju’s is the most valuable edtech startup in the world at $10.8 billion, and has a massive lead on Jio’s Embibe.

It’s still early, and Reliance has the resources, relationships, and partnerships to put up a good fight. But the question is: why should it fight? As Indian startups go global, the opportunity is so large that Reliance should back Indian startups to take on the world.

To date, most of the Indian startup ecosystem has been inward-looking: companies Made in India, Made for India. Flipkart is Amazon for India, Paytm is Ant Financial for India.

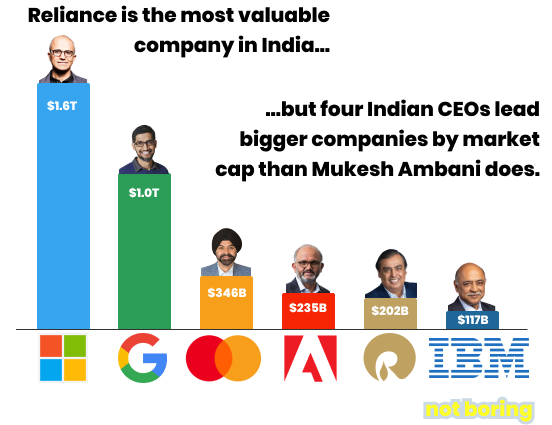

India has mainly exported the raw material of tech -- engineering and management talent -- instead of finished products -- entire companies. Already, Indian-born CEOs run some of the largest companies in the US. Indians lead Google, Microsoft, IBM, Adobe, and more tech giants, controlling trillions of dollars of market cap. Mukesh Ambani runs India’s largest company, but his company is only the fifth most valuable global company run by an Indian CEO.

India will continue to export some of the best tech talent in the world, particularly as COVID has made remote work an accepted reality. The country is expected to have the most software developers in the world by 2023, and companies like Pesto are training Indian developers to be remote employees for US startups and tech companies, upgrading them from outsourced resources to full-fledged members of the team.

But India is also poised to become an exporter of finished tech products in a COVID-shaped world that is increasingly remote and tech-focused. Byju’s, the Tencent-backed education platform, is the most valuable edtech startup in the world. It recently acquired coding school White Hat Jr which runs these incredible* commercials against cricket matches:

Note: Incredible as in entertaining. Critics charge that WHJ is running misleading advertising and that its instruction quality has suffered in its pursuit of growth at all costs. Mo’ money, mo’ problems is a universal startup phenomenon.

Byju’s is gearing up to launch both products in the UK, Australia, New Zealand, Singapore, and Germany. Another Indian edtech startup, Quizizz, is used by 30% of elementary through high schools in the US and boasts an astonishingly high 82 NPS.

At the earlier stage, Sequoia Surge lets Sequoia India invest earlier without signaling risk if the main fund doesn’t do follow-on rounds. Its structure allows it to experiment, and it’s currently working on building companies in India for a global audience.

Typically, a startup would launch in the US, operate in the US, maybe hire a few remote engineers in India, and hire a local GM to try to enter the Indian market. Surge’s program flips that on its head. It builds companies in India to serve both the domestic and global markets, with executive, product, and engineering teams in India and GMs or local marketing positions in the markets they serve. For example, OnJuno, which offers a high-interest checking product (and is an upcoming Not Boring sponsor), is built and run from India with one person on the ground in the US to provide local market knowledge, expertise, and relationships.

Indian startups now both Make for India and Make for the World, increasing the potential for China-sized outcomes. Particularly given the western world’s growing hesitation to work with Chinese tech companies, if India can Make for India and Make for the World, it has the potential to close the startup valuation gap with China and even surpass it over the next decade. One Indian entrepreneur and angel investor put the opportunity this way:

What has changed? India can build for the world. We have the best talent and the best minds, and no shortage of passion and hunger. Chinese entrepreneurs are the only ones that have equal or better energy and passion to create a global impact, but they’ve had policies that have not allowed for that. There’s something to be said for policy and language. We will see India leapfrog China in terms of global impact.

As it stands, though, Chinese investors will capture more of the upside from that impact than Indian ones.

Backed by the World

Atmanirbhar Bharat does not jibe with the current state of the investment world, in which, when an Indian startup succeeds, foreign investors, most disagreeably and prominently the Chinese, get wealthy.

In fact, of the 11 funds that have invested in at least three Indian unicorns, none is entirely Indian. SoftBank leads the way with 11 Indian unicorn investments, and of the twelve largest Indian startups, only one -- Freshworks -- hasn’t taken money from any of SoftBank, Tencent, or Alibaba.

* The funds’ countries imprecise, because as my friend Anmol Maini (whose investment memos on Indian startups are well-worth reading if you’re interested in learning more) pointed out to me that venture capital in India is complicated. Nexus is actually an India-US venture fund, SAIF Partners was originally founded in Hong Kong, and Sequoia, Accel, Matrix, and Lightspeed, while related to funds originally formed in America, operate as their funds with separate teams on the ground in India.

But SoftBank is clearly Japanese, and Tencent and Alibaba are clearly Chinese, and India’s Asian neighbors are clearly benefiting from the rising valuations of Indian startups more than Reliance.

SoftBank is the leading Indian unicorn investor by number of deals (11) and second by total valuation ($49.1 billion). The Chinese giants aren’t far behind. When I was researching Tencent, I noted that:

It has shown a particular affinity for non-gaming investments in India, the only other country with as large a population as China’s. It has invested in ecommerce standout Flipkart, transportation unicorn Ola, education startup Byju’s, food delivery app Swiggy, and fintech darling Khatabook, among others.

The numbers back that up. Tencent is invested in eight Indian unicorns, and is the largest investor by valuation, with $49.5 billion worth of Indian unicorns in its portfolio. Alibaba isn’t far behind, with 5 Indian unicorn investments valued at a combined $24.6 billion.

In a country that so tightly controls who can invest in its companies -- recall that Indian companies cannot list directly on foreign exchanges (yet) -- allowing foreign investors to become the largest owners of India’s fastest-growing startups had to be an intentional decision. It was designed to increase foreign investment in the country to stimulate growth.

However, given the fresh enmity between China and India, the Indian government passed legislation mandating its approval for any investments from countries with which it shares a border, most notably China. As a result of the new law, $3.6 billion food delivery startup Zomato reportedly can’t access $100-150 million of its investment from China’s Ant Financial.

All of which leaves us here:

A thriving Indian startup ecosystem, with the third or fourth most unicorns in the world.

Increased consumer and business demand driven in large part by Reliance’s Jio Platform and Retail products.

Macro conditions shifting in India’s favor, including China’s practical expulsion from the country, at least temporarily.

A focus on Atmanirbhar Bharat, meaning both a vast TAM expansion for the best Indian startups and a gaping hole to be filled by an investor that will keep the financial upside in India.

Reliance and Jio have the opportunity to take advantage of antipathy towards China to provide growth-stage capital to Indian startups that were until now largely funded by their Asian neighbors.

Reliance’s Tencent and SoftBank Opportunity

The genius of Reliance’s Asian tech conglomerate peers Tencent, Alibaba, and SoftBank has been to turn cash flows from its core businesses into investments in fast-growing startups at home and abroad.

The Indian startup scene is roaring at the same time that China/India relations are frayed and Atmanirbhar Bharat is in the air. That presents a golden opportunity for Reliance, and one that the company has hinted at wanting to capture: Reliance needs to become the next in the line of Asian conglomerates turned growth funds, one Made in India, Made for India, and Made for the World.

To date, to Ambani, Made in India has meant Made by Reliance. Increasingly, Made in India should mean Backed by Reliance.

At the end of Reliance’s long section on Jio in its most recent AGM (at 56:30 in this video), Mukesh Ambani made an appeal to India’s startups:

Jio is still very much a startup. As such, we have a very special place in our heart for startups, who we consider our brother-in-arms. I believe there is no better partner for Indian startups than Jio. We are well-positioned to help Indian startups in a number of ways: technology development, product development, distribution market access, or even scale-up capital…

We believe that this will be the true measure of success for Jio, to create a mighty knowledge coalition that solves India’s problems and opens the door for many more companies from India to step successfully onto the global stage.

Ambani paints a compelling picture of a Reliance-supported startup boom, but thus far, it has made only limited forays into “scale-up capital.” Instead, it has competed with or fully acquired startups to roll into its own offerings.

Instead of just acquiring, it should build up a portfolio of investments. I don’t think it’s a coincidence that many of the investors in Jio Platforms and Reliance retail, like the Saudi Public Investment Fund, Mubadala, and ADIA are also some of the world’s largest venture fund backers. Leaving SoftBank off the cap table and dealing directly with the Vision Fund’s LPs signals, to me at least, that Reliance is looking to cut out the middleman and start aggressively investing themselves. The move would make sense for both offensive and defensive reasons.

The points on the offensive side are easy to understand:

Capture Upside Beyond Reliance. Investing in India’s top startups helps Reliance capture the financial upside it helped create, a $750 billion opportunity if it just catches up to where China is today. Investing vs. building or owning means that Reliance can capture upside even when other major players succeed.

Support Portfolio Companies. It has the opportunity to put its thumb on the scales for the companies it backs in India.

Cement Mukesh’s Legacy. Investing further cements Mukesh’s push from energy and petrochemicals into technology. He can become a less crazy Masa on the world stage.

Transform the World. Mukesh has publicly stated that the world will change more in the next eight decades than it has in the previous 2,000 years. Investing in a portfolio of early and growth stage companies is the most surefire way to capture the upside that creates.

The points on the defensive side are less obvious but even more important:

De-risks Succession. Mukesh knows all too well that succession battles can tear a family apart. If you’ve watched Cricket Fever: Mumbai Indians, which follows the Indians’ 2018 IPL season and heavily features his son and potential heir, Akash, you know that Mukesh needs to diversify against his succession risk. While Isha seems to have more potential, investing in a broad portfolio of the best Indian, and eventually global, startups would protect the company from relying solely on the third generation of Ambanis.

Turns Reliance from Bully to Benefactor. One of the biggest knocks on Jio Platforms is that even if its products, like its payment and chat apps, are inferior to startups’, it will suck the air (and money) out of the startup ecosystem by outspending and undercutting new entrants. Instead of starving young competitors, Reliance should back them. Anything the company does that is seen as supporting instead of limiting the Indian tech ecosystem will let it continue to operate in its quasi-monopoly status without strong public backlash.

Keeps Prices Low. Reliance caught heat for anti-competitive practices by extending Jio’s free period past the common 90-day window and then jacking prices once customers were locked in. While price gouging may be better for profits in the short-term, building an engine that benefits from the overall health of the economy would allow Jio to keep prices low while still capturing upside. Tencent doesn’t charge for WeChat; it does well when the people and companies that use it do well.

Depending on the success of Jio Platforms, there are two approaches that Reliance might take as it goes down the Mega-Corporate Venture route: the SoftBank approach and the Tencent approach.

The Tencent Approach

As I wrote in Tencent: The Ultimate Outsider, Tencent leveraged its Super App, WeChat, and its position with the government to invest in companies at home and abroad. In China, it runs the Tencent Capital + Traffic Flywheel: see which companies perform well on WeChat, invest in them, send them more traffic, profit. It has invested in Chinese giants like Meituan-Dianping, JD.com, and Pinduoduo using this approach.

Tencent also leverages its place as a gateway to China to invest in foreign companies including Spotify, Snap, and Tesla. As mentioned earlier, it’s also the largest investor in Indian startups by market cap. With an increased focus on Indian self-reliance and increased scrutiny on Chinese investment in the country, those are investments that Reliance should be making instead of Tencent. It’s beginning to look a lot like Tencent already:

It is working on a Super App for India, likely WhatsApp in partnership with Facebook.

Like Tencent, it’s focusing on “smart retail” with Reliance Retail and Jio Mart.

Its dominant position and close ties with the government mean that foreign companies that want to play in India are all but forced to partner with Reliance (see: Facebook, Google, Amazon).

If it succeeds in building a Super App, Reliance will be in a similar position in India to Tencent’s in China. It will be able to see which Indian startups are performing well in its ecosystem, invest in them, and give them the capital and traffic to all but guarantee success. Like Tencent, it can invest off its own balance sheet, now that it is debt free, hugely profitable, and focused on tech growth, and it can invest even more in the winners to acquire controlling stakes and turn them into subsidiaries, as it did with Embibe.

It can also invest in foreign companies, both public and private, who want preferential access to the Indian market. Through Retail and Jio, Reliance has already done so much of the hard work to wrangle supply and demand that it could present a ready-made package to foreign companies who want to launch or grow in India.

By investing broadly and supporting its portfolio (and “supporting” can be a pretty strong word when it comes to Reliance in India), it can capture upside no matter which sectors or companies succeed in India.

Unlike Tencent, Reliance doesn’t even have an Alibaba to compete against. It’s the undisputed leader in the market, which means that its upside is potentially unlimited should India continue to catch up to China and become the preferred Asian opportunity for foreign investors.

The SoftBank Approach

In Masa Madness, I wrote about Masa’s journey to transform SoftBank from a PC software distributor to a telco to the world’s largest and most profligate venture fund. With the success of Jio, Reliance underwent a similar transition, from an energy and petrochemicals company into India’s largest telco.

It may continue to follow SoftBank’s path: use a combination of cash from its operating businesses and investments from LPs to spin up an off-balance sheet fund to invest in growth-stage startups. Its relationships with the Jio and Retail investors place it uniquely to build its own, more domestically-focused, less insane version of SoftBank’s Vision Fund.

Today, SoftBank is the largest investor in Indian unicorns by number of investments, but two things signal Reliance’s desire to compete, instead of partner, with the Japanese giant:

SoftBank was looking to invest $2-3 billion in Jio but never closed the investment, either because SoftBank was forced to sell assets to raise cash or because Reliance wouldn’t have it. SoftBank is currently sitting on the waitlist for a Reliance Retail investment.

Reliance is raising money directly from the Vision Fund’s LPs. Instead of using Masa as an intermediary, Ambani built direct relationships with the Saudis and Mubadala.

Look at SoftBank’s LPs vs. Jio and Retail’s investors. Reliance doesn’t need SoftBank, and given the mission of Atmanirbhar Bharat, I don’t think that India’s startups will either if Reliance enters the growth equity fray.

The Vision Fund’s two largest investors also invested in Jio or Retail, as did Qualcomm, and Jio has spoken to Foxconn about manufacturing its higher-end LYF smartphones. Instead of SoftBank’s Apple and Sharp, Reliance has Facebook, Google, Intel, and potentially Amazon. Instead of Larry Ellison, Reliance has KKR, TPG, Silver Lake, L Catterton, General Atlantic, GIC, and Vista Equity Partners.

In the SoftBank approach, Reliance raises a fund from these investors to use its advantageous position in India to invest in growth-stage and public companies, both domestic and foreign, who want to operate in India. Increasingly, that will be every company.

The SoftBank approach is lower-risk, lower-upside than the Tencent approach of investing off of its own balance sheet. I think that the company is more likely to take the Tencent approach -- it’s closer to the company’s historical approach of vertically integrating and capturing more upside -- but either approach is a better long-term play than its current one.

In either scenario, Reliance has the scale, expertise, and relationships to pull this off:

Jio and Retail have taken in more investment in the past 6 months ($25 billion) than the entire Indian startup ecosystem raised in 2019 ($14.5 billion).

Reliance has the stated desire to work with startups.

Prime Minister Modi has been friendly to Reliance, often to the detriment of foreigners, and his Atmanirbhar Bharat mission seems to call for local funding instead of the traditional reliance on outside capital.

It is better positioned than anyone to capture upside if India grows and exports its expertise to the rest of the world.

Reliance can ride the Indian tech wave with its operating businesses if the demand stays in India, but it has the desire to do more - Made in India, Made for India, Made for the World. It’s the playbook that Reliance is beginning to run itself, and it should open that playbook up to Indian startups and keep the upside from those companies’ global success in India.

Made in India, Backed by Reliance

When I ran the idea that Reliance should become a growth equity investor past a few people involved in the Indian tech ecosystem, I got some variation of the following:

“That’s probably what they should do, but it’s not in their DNA. Their culture is all about building and owning everything.”

It’s hard to argue with the Ambanis’ results. Reliance’s stock, which has compounded at a 32% CAGR for an astonishing 43 years, is already up 44% YTD, making it the first company in Indian history to trade at a $200 billion market cap.

But the internet behaves differently than infrastructure. It’s an environment of abundance and power law returns. On the internet, it’s often better to own a smaller piece of the category-leader than it is to own all of the second-or-third-place company. Today, Reliance is the only company in India worth over $200 billion. In a decade, there are likely to be many, and Reliance should facilitate that explosion and participate in the upside.

If it can pull off the transition from operator and investee to operator and investor, it will remain the best way to invest in India for decades to come.

So how to play it? It’s difficult to invest in Reliance because of Indian laws around foreign listing. You’d need to set up an Indian bank account and demat account, or just buy something like the INDA ETF, of which Reliance makes up about 16% of the weight. But as we speak, driven in part by Reliance’s desire to offer shares in Jio on the NASDAQ, India is hammering out changes to its laws that would allow its companies to list directly on foreign exchanges. If that happens, and if Reliance lists in the US, I think its price could explode.

Spend the next few months before foreign listing getting smart on India, starting with Reliance. It’s a company to watch and learn from. Not many companies can make the transition from one generation of leadership to the next, from old-line industries like oil and petrochemicals to new technology infrastructure, platforms, and smart retail. Its next act, investing in Indian unicorns before they hit the scale of China’s startup darlings, could be its most impressive and impactful yet.

India is the next tech superpower. Its companies are going to Make in India, Make for India, and then export to the rest of the world. Indian tech today is like China a decade ago, with more upside given the two countries’ relative status in the west.

I am bullish on Reliance whether it continues to vertically integrate or begins to invest in India’s startup ecosystem. Owning the infrastructure in a fast-growing market is super valuable. But over time, I believe the latter approach will lead to an outcome that is multiples better than the former. Investing in Indian startups is both a smart offensive and defensive move, and will ensure that the company can thrive even with eventual internal and governmental succession.

Chak De India!

Massive thanks to Anmol Maini, Arjun Malhotra, Rohan Malhotra, Sid Jha, my father-in-law, and uncle Sudhirbhai for educating me on India’s history, economy, and startup landscape, and to Dan and Puja for editing.

Verified Not Boring

If you’re enjoying Not Boring and want to spread the word, you should get involved with the Verified Not Boring referral program. It means the world to me.

10 Referrals: Thank you shoutout in the next Not Boring

20 Referrals: Not Boring Stickers

30 Referrals: Limited Edition Not Boring T-Shirt

Get your referral link and track the leaderboard by clicking this button, and start sharing with your smartest, most curious friends on Twitter, LinkedIn, text, or email.

We will be back on Thursday with a new Not Boring Investment Memo 👀

Thanks for listening,

Packy