Welcome to the 805 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 15,182 smart, curious folks by subscribing here!

Hi friends 👋,

Happy Monday!

It’s hard to avoid SPACs. Everyone has one, Nikola is looking more and more like a fraud, and Chamath just launched three more. It’s easy to dismiss SPACs as a fad and the companies that they take public as immature, risky, and dangerous.

But great companies can go public via SPAC, too, and they increasingly will. When we find one of those, it’s worth doing our homework, which is what today is all about.

But first, a word from our Sponsor.

Today’s Not Boring is brought to you by…

In early June, I wrote:

A startup called Public, backed by top VCs like Accel and Greycroft and celebrities and athletes including Will Smith and JJ Watt, built a product that makes investing social and community-forward, allowing people to build followings based on their investing acumen.

I don’t know about my investing acumen, time will tell, but I know that we’ll make smarter decisions if we’re able to sharpen our ideas on each other. Like today, for example. Whether you’re bullish on $IPOB, bearish on it, or still figuring it out, I want to hear your opinion, so I’ll be posting and discussing on Public and would love to hear your thoughts over there. You can join the conversation whether or not you buy a single share… although everything is more fun with some skin in the game. (This is NOT investment advice, just an observation 😎)

Now let’s get to it…

Knock Knock. Who’s There? Opendoor.

Home is Where the Startups Aren’t

Homes are emotional.

Puja and I are having our first kid, a son, in less than a month. We spent this Saturday cleaning up my parents’ house and getting rid of old junk that we hadn’t used for years to make space for all of the new stuff the little guy will need whenever we come visit. As with any cleaning project, we started by emptying one closet and decided to throw out twenty-plus years’ worth of trash and memories from around the house. As we emptied closets we hadn’t opened in years, my mom came up with reasons we should keep that old empty picture frame or half-used can of WD-40, told us that we should just dry clean the sleeping bag we bought in 1998 in case we might want to use it at some point in the future. None of it is rational, but it’s not unique either. Mari Kondo has made a fortune convincing people to let go of things that once held importance but no longer do.

And that’s just the stuff. You would have to pry us out of the house itself.

Maybe that’s why housing is one of the last major categories that technology has left alone. Sure, companies have tried. Tons of them. The startup graveyard is filled with companies led by entrepreneurs who realized that the way we buy and sell homes sucks, but couldn’t ultimately figure out how to change it. They weren’t thinking big or long-term enough. The companies that have made the biggest impact, like Zillow and Redfin, make it easier to search for houses, but then kick buyers over to agents to go through the offline process, the same way it’s always been done.

There’s this Startup Lindy Effect at play in real estate. If the future life expectancy of something is proportional to its current age, and real estate has survived practically unchanged by technology longer than any other industry, then maybe the way it is is the best we can do.

That’s why most people’s reaction to a company like Opendoor is, “Cool idea. Won’t actually work.”

Opendoor, founded in 2013, lets people transact real estate at the click of a button. It promises to transform a process that has traditionally been “Complex, Uncertain, and Slow” into one that is “Simple, Certain, and Fast” by using technology to make instant offers on homes.

At least one person sees the vision. Last Tuesday, Chamath Palihapitiya announced that his SPAC, Social Capital Hedosophia II (IPOB) is merging with Opendoor to take it public at a $4.8 billion valuation.

(For a refresher on how SPACs work, check out Juul: The SPAC 2020 Deserves.)

So now, without the months of preparation and detailed S-1 that the traditional IPO offers, the question shifts from, “Could Opendoor work?” to “Should I invest in Opendoor?”

My gut reaction to that question was a resounding “NO.” There are three things that companies say that make me want to run away as fast as I can:

The Shark Tank Market Sizing. “X thing is a $y billion market! If we get just z%, we’ll be a multi-billion dollar business!” Stop. If anyone in a given industry can say something, it’s not an advantage.

Capital as a Moat. We talked about this in Masa Madness, but the idea of capital as a moat -- raising more money than competitors and spending it to achieve a dominant position -- has been disproven multiple times in SoftBank’s portfolio alone.

“We’re Like Amazon.” This is my favorite. If there’s a business out there that’s losing money, chances are, they’ve said something like, “Well you know… Amazon lost money for a very long time and look at them now!” Bless your heart. If the only thing that you have in common with Amazon is that you also lose money, you’re fucked.

Opendoor says ALL THREE of those things. Plus, Opendoor faces opposition from the realtors who still control the vast majority of the housing market and competition from Zillow, a company I respect tremendously that has a massive demand generation advantage. PLUS, Opendoor is a well-funded, SoftBank-backed real estate company, like, you know, WeWork. The New York Times wrote about Opendoor in 2017 and titled the article “The Rise of the Fat Start-Up.” If asset light is in, Opendoor should be out.

And yet… the more I dig into Opendoor, the more bullish I get.

I think Opendoor at $4.8 billion will be one of those prices people look back at in a couple years and say, “Shit, I was thinking about buying Opendoor when its market cap was like $5 billion and I missed out,” because the things that most companies say about themselves are true for Opendoor.

Amazon didn’t win because it was the first company to sell things on the internet or because it controlled demand. Amazon won because it resiliently put all the expensive and unsexy pieces in place and sacrificed short-term profitability for long-term dominance. Before Marc Andreessen yelled it, Jeff Bezos realized that Amazon had to BUILD.

Opendoor is doing the same thing in real estate. Real estate hasn’t been impervious to startups because it’s structurally immovable. It’s just really hard to change, capital intensive, and slow relative to another B2B SaaS business. No one has taken the vertically integrated approach and long view that Opendoor has. Opendoor built the world’s most accurate home pricing model, operates a distributed network of thousands of inspectors and contractors, regularly accesses both the debt and equity capital markets, takes inventory risk, and coordinates among the many parties involved in the home selling transaction. It consciously decided to take on a ton of risk.

But as Ben Thompson wrote in Opendoor: A Startup Worth Emulating in 2016:

Risk, though, is not only about downside; it’s about upside. More than that, the level of downside risk is correlated to upside risk: Opendoor has many more reasons why it might fail than Zillow or Redfin, but its potential upside is far greater as a result.

Being aware of, comfortable with, and prepared for risk is a major advantage. Opendoor laid out its plan from the beginning, identified the key risks, and has spent the last six years eliminating the downside and building structural advantages that increase its upside potential.

It’s difficult to understand the compounding effect of all of the little things that Opendoor does, and why those little things will give the company such a large advantage over competitors. People grasp its downside much better than they grasp its upside. But grasping the upside is what we’re all about here at Not Boring, so here it is:

Opendoor is executing impressively and intelligently on its original plan.

It is capturing meaningful market share in one of the world’s largest markets -- residential real estate.

It has positive and improving unit economics.

The Zillow threat is overblown. Opendoor has a range of advantages over Zillow in iBuying, which are borne out by the numbers.

Opendoor is the most similar company to Amazon on the market. It is spinning a powerful flywheel and controls its own profitability vs. growth lever.

Investing in Opendoor today is an opportunity to get in before the rest of the world catches up to something that Opendoor’s founders saw way back in 2003.

Opendoor’s Genesis: Everyone Feels the Same Pain

Opendoor had the benefit of perfect timing, but it wasn’t luck. It was an idea waiting for just the right moment.

On This Week in Startups in 2018, Opendoor co-founder, Keith Rabois told host Jason Calacanis:

I had this vision back in 2003 that really was the genesis of the company. The thesis was that you could use data to model the home sight unseen accurately enough to purchase it safely. Back in 2003, Peter Thiel said “Come up with an idea that’s gonna innovate in residential real estate. It’s the largest part of the US economy that’s been unaffected by technology.”

What he might not have remembered is that when I joined PayPal, Peter and I had this negotiation about me joining . At the time, I was living on the east coast and owned a property in Washington, DC. Peter basically said, “I’ll see you on Monday” and I was like what are we talking about, I thought I could start in two to four weeks. And Peter said, “Nope, if you can’t start on Monday, forget the whole thing.” So we compromised, and I started on Tuesday instead of Monday, so that gave me Monday to sell my house.

Around the same time Thiel asked Rabois for a real estate idea, Eric Wu was having a similarly painful homebuying experience in Arizona. When he was 19 and a student at the University of Arizona, Wu used scholarship funds to purchase his first house, a $112k fixer upper. Wu felt the same pain that Rabois did:

It’s not surprising that Rabois and Wu had similarly shitty experiences. Selling a home is universally painful. One in four people would rather attend a funeral than go through the process of selling a home.

But unlike the millions of people who have had similarly rough experiences, Rabois actually tried to start a company to fix the problem and bring liquidity to the housing market. He went searching for $10 million for project “Homerun,” but was only able to secure $5 million. He realized that it had to be all or nothing, so he dropped it, but spent the better part of the next decade biding his time and trying to convince someone to build it with him.

Then in 2010, Wu joined Y Combinator with his real estate startup and sought Rabois out as an adviser. At their first meeting, Keith tried to convince Eric to drop his idea, Movity, which provided location-based data to help home buyers make better decisions, and build Homerun with him. Wu turned him down and stuck with Movity (Rabois invested) and sold to Trulia in December 2010.

After two years at Trulia, Rabois tried to woo Wu again. This time, he succeeded. A decade later, it was time to turn his idea into a reality.

In 2013, Wu built a landing page, opendoorrealty.co, to test whether people would be willing to instantly sell their homes at a discount. Wu told the audience at NFX’s 2019 Proptech Summit that he discovered that there is “a significant liquidity premium for a certain set of sellers.” He talked to ten sellers, and asked whether they would be willing to sell their home for 88 cents on the dollar. Some said yes, and for those who didn’t, he worked his way up until he found an equilibrium. Assessing the opportunity based on price elasticity of the demand curves is in the company’s DNA, and that’s really important. We’ll come back to why a little later.

Rabois, then a partner at Khosla Ventures, committed to lead a $10 million Series A for the renamed Opendoor, with Wu at the helm as CEO. At the time, $10 million was a big first check, but both men understood that they couldn’t MVP their way into transforming residential real estate. They needed to do it right from the beginning. Part of doing it right meant recruiting a founding team with necessary experience:

Ian Wong, CTO: Stanford Ph.D. dropout and Square Data Scientist

JD Ross, VP Product: VP, Product at Addepar

Ryan Johnson, VP Operations (founding team): Bain Capital and McKinsey

In its founding team, Opendoor had the real estate, pricing, product, and capital markets expertise necessary to make housing liquid.

Sticking to the Plan

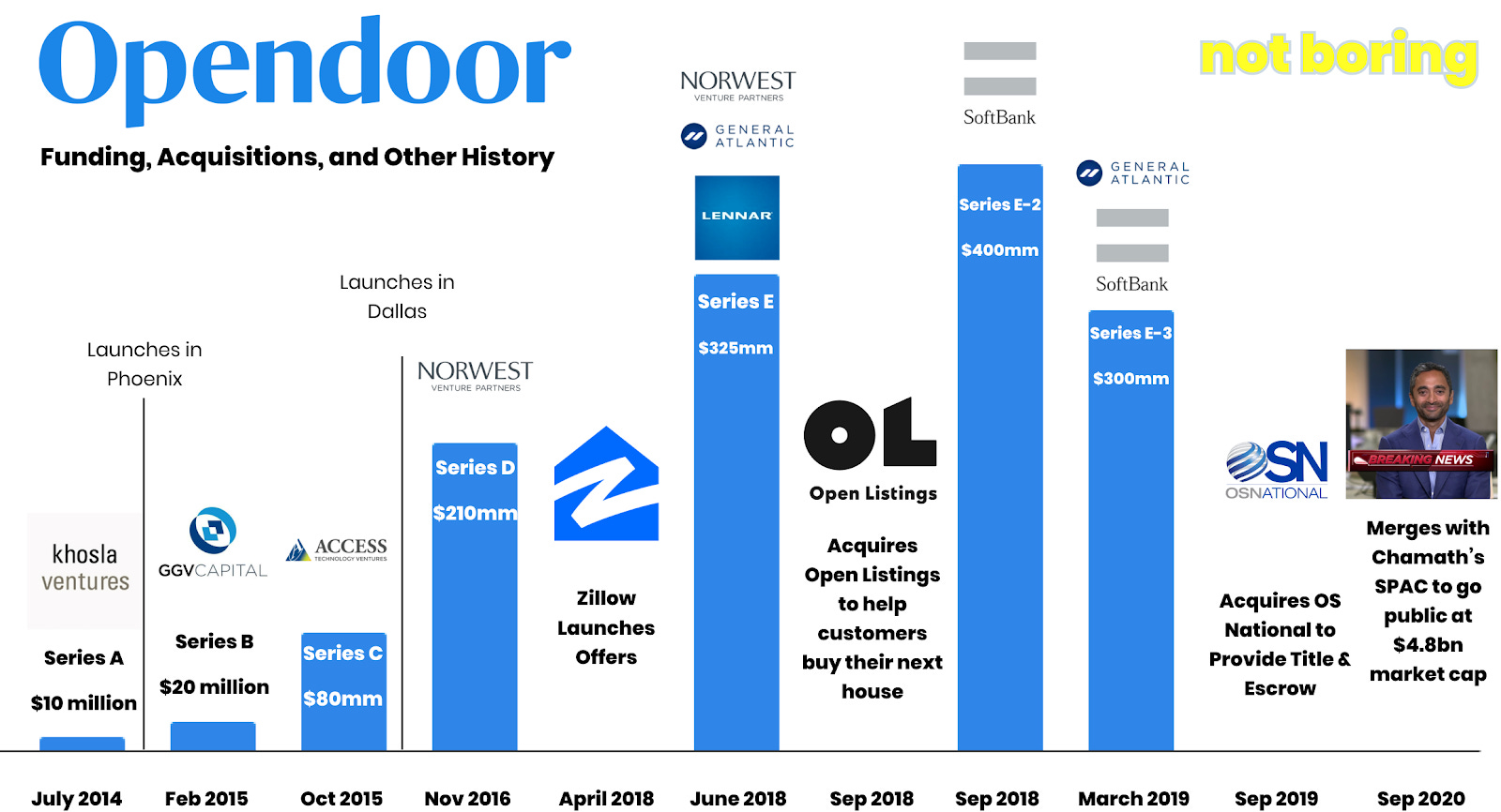

With the team in place, Opendoor closed its Series A, led by Khosla, in July 2014. Incredibly, its Series A deck laid out most of the plan that Opendoor is still executing on today.

Here’s how it works:

Opendoor uses an Automated Valuation Model (AVM) to algorithmically price homes.

Sellers enter their address, answer some questions, and receive an offer instantly.

Opendoor sends an inspector to confirm the condition and price repairs (and collect data to feed back into the model), before settling on a final price.

Opendoor charges 6% in the form of a discount to cover fees plus a liquidity discount of between 0-6% depending on riskiness. Its average today is 7.3% total (6% + 1.3%).

Opendoor closes with the seller quickly, makes repairs, and sells the home. Originally, it did this through agent partners, and increasingly, it’s bringing that process in-house.

Rabois and Wu started the company on the belief that certain customers would be willing to pay a premium for certainty, and that many more customers would take certainty for free. Simply put, the strategy that Opendoor has pursued since day one is:

Start with the least price sensitive customers → use them to improve accuracy and lower costs → attract slightly more price sensitive customers → use them to improve accuracy and lower costs → launch new markets with least price sensitive customers → rinse, wash, repeat

This is the first point at which Opendoor starts to remind you of Amazon. In Two Ways to Predict the Future, I wrote that Jeff Bezos had a strong claim for the G.W.O.A.T. (Greatest Worldbuilder of All Time) crown because he saw that everything would be sold online in the future and set out to patiently execute on his long-term vision. While Bezos started with books, which the internet with its infinite shelf space was uniquely positioned to handle, Rabois and Wu started with homes, which the internet has been notoriously bad at handling.

As Byrne Hobart pointed out, “Homes may be the single most heterogeneous asset class and product in existence. There are 95m single-family homes in the US, all of which are in some way unique.” So Rabois and Wu picked the most homogenous product within the universe of US residential real estate: newly constructed homes in Phoenix.

It’s important to keep in mind how systematic Opendoor has been throughout its life. The Series A deck highlighted three risks -- model accuracy, buying overvalued homes, and capital -- and used its Series A and Phoenix to address each. It used subsequent rounds to de-risk, scale, expand, acquire, and drive down costs. Remove friction, improve margins.

For a full history, including links to fundraising articles, check out this Google doc.

By the time it raised its last venture round in March 2019, less than five years since it raised its Series A, Opendoor accomplished a lot:

Raised $1.48 billion in equity capital and over $2 billion in debt capacity

Launched in twenty-one markets

Acquired Open Listings and OS National to expand its service offering

Improved pricing, brought down costs, accessed cheaper capital

Purchased and sold billions of dollars worth of homes ($1.7 billion in 2018)

Hit a $3.8 billion valuation

In 2019 alone, Opendoor did $4.7 billion in revenue with positive contribution margins. All of that capital, including SoftBank money, which has often been a kiss of death for its recipients, made Opendoor stronger. Opendoor’s strategy had always involved launching markets, proving and improving the model, de-risking, and launching new markets. Whereas SoftBank money forced companies like Wag to expand before they were ready, Opendoor knew exactly when it was ready to expand and what it wanted to accomplish by doing so. Its focus on unit economics meant that it wouldn’t light the money on fire, and a strong balance sheet meant that it was ready for turbulence.

When the Coronavirus hit, Opendoor was prepared. It dramatically de-risked, laying off over 600 employees (35% of staff), paused buying while continuing to sell, and brought its home inventory down from $1 billion to $172 million. CFO Carrie Wheeler pointed out that it sold down without sacrificing margins, which dipped just slightly from 7.1% in Q1 to 6.8% in Q2.

Then in the midst of the pandemic, some good news. Last week, after a week of rumors, Chamath announced that his second SPAC, IPOB, was merging with Opendoor to go public at a $4.8 billion valuation.

Chamath’s SPACtacular Vision

Chamath is the voice of the SPAC movement, and CNBC is his pulpit. Last Tuesday, he went on CNBC to lay out his thesis for Opendoor:

Residential real estate is a massive market ($1.6 trillion annually) with low customer satisfaction and an inconsistent experience (28% of realtors do the job part time). Opendoor’s model has five tailwinds at its back:

Underbuilding since the financial crisis has led to a supply/demand imbalance

Rising state taxes and elimination of SALT deductions are motivating people to move

75 million millennials entering the housing market who expect to transact online

WFH is here to stay, so people are moving to higher quality-of-life cities

The Fed signaled that it will keep interest rates near zero at least through 2023

The former Facebook exec and Social Capital CEO has high hopes for the company:

The times I’ve come on, I’ve tried to find asymmetric upside opportunities and present them to you. This to me feels like Bitcoin in 2012, Amazon in 2015, Tesla in 2016, Virgin last year. This is an enormous bet for me, and I think that Opendoor is going to build a huge, huge business.

After a run-up to $18, IPOB closed the week at $14.60. A healthy run-up, but nothing like high-margin tech IPOs like Snowflake, which more than doubled on its first day of trading.

That makes sense, though. With both SPACs and IPOs on the table as viable options, IPOs are for easily-understood companies, and SPACs are for companies whose potential is underappreciated. Opendoor is underappreciated.

Understanding Opendoor

Chamath clearly appreciates Opendoor’s vision, but there are many who remain skeptical. Here’s the bear case:

It’s a super low margin business that isn’t profitable and may never be.

It’s too capital intensive.

Most people won’t want to sell their houses online.

Of course it’s done well in a rising market; wait until we see a downturn.

Zillow is a higher-margin business with better distribution. It will eat Opendoor’s lunch.

See, it laid off 35% of its workforce. Just another overfunded SoftBank house of cards.

I understand where the bears are coming from. At first glance, Opendoor smells too much like WeWork. And a first glance is all some people will give it, because understanding a business like Opendoor’s can seem opaque and unapproachable, particularly with phrases like SPAC and iBuying in the mix. But it ultimately comes down to one question, which is the same question you need to answer for any business:

Will the company be able to generate positive and growing cash flows for a long time?

That one question breaks down into three sub-questions:

Is the market big enough that the company has room to grow and cover central costs?

Does the company make money on each transaction and can it become profitable?

Is the company’s advantage defensible against competitors?

That’s pretty much it. So how does Opendoor do on each?

1. Is the market big enough?

This is an easy one. Real estate is massive. According to Zillow’s research, the total value of US homes is $33.6 trillion. Much of that value is locked up because people don’t sell their homes every year, but according to Opendoor, 5 million homes are sold annually, representing $1.6 trillion per year in volume. That’s twice as big as the used auto market (Carvana has a $28 billion market cap) and 60% more than Americans spend on food (Domino’s alone has a $15 billion market cap).

Ok got it, housing is big. No one disagrees that housing is big. But how about iBuying? No one’s actually going to sell their home through an app, right? Wrong.

In Phoenix, Opendoor’s most mature market, it already has over 4% market share of all home sales. And the company is growing market share faster in its new cohorts. After 12 months, Phoenix only had 0.8% market share. Its last 15 markets got to 1.3% market share within the first year.

As Opendoor gains awareness in new markets, it grows, and as it improves its playbook and gains national recognition, it’s able to scale up more quickly. The company and its new partner, Chamath, believe that if it just executes on this playbook across the country, it can achieve $50 billion in run-rate revenue with 4% market share in 100 markets.

Ok ok fine, iBuying is a big opportunity. But anyone with a lot of money can just buy a lot of houses. Can they actually make money?

2. Does the company make money on each transaction? Can it become profitable?

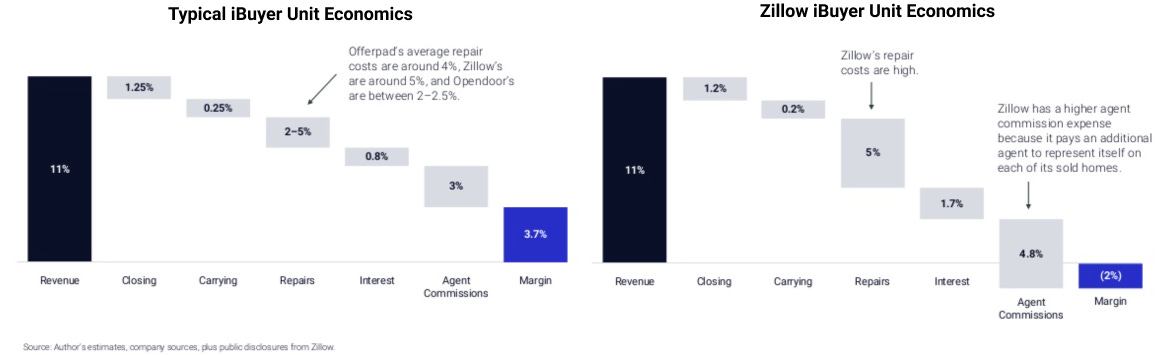

iBuying is a low margin business, but Opendoor has positive unit economics. In Phoenix, it generates a 4% contribution margin (CM) on each home, and 3% after paying interest (CMAI) on the money it uses to buy the home. Because the total transaction value is high, that low margin percentage is actually a lot of dollars. It makes $8k per home after interest in Phoenix.

Across all markets, it generates a CM of 3.1% and a 1.9% CMAI. It expects those numbers to improve to 5.5% and 4.7% in 2023, respectively. That seems like a small improvement, but at the scale Opendoor anticipates by 2023, every 1% in CMAI improvement is another $100 million that drops to the bottom line, and at a 20x P/E multiple (CarMax is at 21.4x), each 1% represents $2 billion in market cap.

Long-term, Opendoor is targeting a 6-8% CMAI as it improves pricing, lowers costs, and adds on high-margin services like title and escrow (82% of customers use Opendoor title & escrow), mortgages, warranties, insurance, and moving. Forbes called title insurance America’s Richest Insurance Racket, because of “antiquated state laws that thwart new competition, allow prices to soar despite declining costs and force almost every home buyer to pay for insurance that most of them will never need.” Opendoor’s purchase of OS National means that it gets to participate in that racket with a captive audience of sellers.

When considering additional services, Opendoor’s targets actually seem conservative. The more additional services it attaches, the higher its margins or the lower its price, which would lead to more demand and ultimately higher margins.

How about a downturn, though?

Even during the Coronavirus-induced selldown, Opendoor was able to maintain positive margins. In A Skeptical Look at Opendoor, though, Twin Oaks Group points out that it’s “inappropriate to portray Covid as a stress on the single family market when indeed it’s a tailwind.” The author noted that home prices actually increased by 1% in the quarter, and by removing that, Opendoor only saw contribution margins of 2.1% and 0.9% after interest.

Fair, Opendoor has yet to face a real downturn, but it’s actually better positioned than competitors or individual home sellers if it does, for a few reasons:

Centralized pricing gives it the best pulse on the market of anyone in it.

Customers are uncertain in a downturn. When customers are uncertain, they should be more willing to pay a premium for certainty.

Home prices move much more slowly than other asset classes. Rental prices have dropped much more dramatically than sales in Brooklyn, which I’m checking daily.

Opendoor only holds houses for an average of 88 days, so their exposure is limited.

The government’s response to recent crises has been to lower rates, which is ultimately beneficial to Opendoor’s unit economics.

Ultimately, though, no two downturns are the same. This is a risk to keep an eye on, but I think it’s overblown. Nothing makes me more excited than an overblown bear case.

3. Is the company’s advantage defensible in the face of competition?

So if a bear market doesn’t take Opendoor down, what about competitors? Opendoor faces increasing competition from both startups and bigger incumbents in the iBuying market.

On the startup side, it faces competition from companies like OfferPad, Orchard, and Knock, as well as a host of regional players. This is where Capital as a Moat comes in. More specifically, Opendoor takes advantage of Cost-of-Capital as a Moat. Because of its track record, short durations, balance sheet, and team, it is able to secure the lowest rates of any iBuyer. That means that all else equal, it can make more money on each transaction than any of its competitors, or put another way, it can charge customers less and still make the same margin. But all else is not equal. Opendoor’s data, algorithm, and scale mean that it can price more accurately than its competitors and remodel at lower costs for a higher ROI. No startup will unseat Opendoor or put much of a dent in its plans.

Where it gets really interesting is in the head-to-head battle with Zillow Offers.

Zillow vs. Opendoor

In April 2018, after Opendoor had been buying houses for four years, Zillow announced the launch of its own iBuying program. Instead of choosing markets in which Opendoor doesn’t have a presence, Zillow chose to compete head-to head. Each company buys homes in twelve states, but each only has one state that the other isn’t in (Zillow in Ohio and Opendoor in Utah).

I’ve been long Zillow since their stock tanked on the Offers announcement in part because I thought that their core product and Zestimate gave them a distinct demand advantage over Opendoor or any other iBuyer. I’m up 142% on Zillow and holding, but I actually think the advantage in iBuying belongs to Opendoor. Here’s why.

Running an operationally-intensive business is just so much different than running a pure tech company. I can’t think of any company that has turned an advantage in SEO into a leading vertically-integrated business. Yelp didn’t win food delivery, Kayak didn’t launch Airbnb, and Google Shopping hasn’t put a dent in Amazon’s dominance.

Opendoor was built from the ground up to do what it does. It has a culture that’s fixated on driving down costs and passing them on to customers. It’s hard to imagine that a company used to software margins can transform its culture without a tremendous amount of pain.

In addition to its culture, Opendoor has a bunch of structural advantages built into its DNA that Zillow will struggle to compete with:

Data. Zillow’s Zestimate, which I love and wrote about in Zillbnb, actually doesn’t have the right level of accuracy on the right things to optimize for iBuying. It’s a good starting point and great for demand gen, but Opendoor has proprietary and unique data that it’s built up from sellers and its custom inspection app over six years. It knows far better, for example, how to price out repairs than Zillow does.

Agents. Zillow uses agents and Opendoor sells homes itself. Because of that, Zillow has structurally higher costs, and it can’t collect the kind of data that Opendoor can, like how many visits it takes to sell a house in a particular microneighborhood. Plus, it can’t offer the seamless experience of self-hosted tours via smart lock that Opendoor can.

Aligned Incentives. Working with agents also creates a principal/agent problem for Zillow. Agents are incentivized to hit a price that clears the deal, whereas Opendoor can hold out to achieve its optimal price target.

Zillow undeniably has an advantage in top of funnel demand generation over Opendoor. It’s why I’ve been so bullish. But the more I think about it, the more I realize that that doesn’t matter in iBuying.

CAC is less important than I thought. Because the transaction is so large, the cost of acquiring the customer represents a very small percent of the total transaction value. It’s far more important to get pricing right than CAC.

Opendoor can generate demand through partnerships. Zillow is the largest demand generator in real estate, but there are others. Opendoor partners with Redfin and Realtor.com, for example, and pays each to send it leads. The Redfin deal is particularly interesting. Redfin tried to get into the iBuying game but realized that it was too hard, so it decided to partner with Opendoor instead.

Customers are going to price shop. I don’t have numbers to back this up, but we can think our way into this one. Someone’s home is typically their largest asset. People compare prices when they’re buying a t-shirt; they’re certainly going to shop around for the best price when selling their home. To that end, Zillow’s SEO strength is actually good top of funnel for Opendoor as well. Zillow shows customers that iBuying is a viable option; if Opendoor has the best price, which it should given its data and cost advantages, it will end up winning the deal.

These advantages become clear when comparing the two companies’ unit economics. According to iBuying expert Mike DelPrete, Zillow operates its iBuying program at a -2% net margin, while Opendoor operates at a 3.1% margin. Two slides in his 2020 iBuyer Report Preview highlight Opendoor’s structural advantages.

Because it has built up from the hard parts -- including building networks of inspectors and contractors in each market, six years’ worth of data on which improvements drive ROI, and buying more supplies than anyone else -- Opendoor spends around 2% of revenue on home repairs versus Zillow’s 5%.

Because Zillow’s main customers are agents, it can’t cut them out of the transaction, and ends up paying over 50% more than Opendoor on agent commissions. To lower this cost, it would have to risk pissing off the people who pay it the marketing fees that drive the majority of Zillow’s revenue and margin.

Worryingly for Zillow, its loss per home increased throughout 2019. It does not seem to be improving efficiency with scale, and it will be interesting to see how long investors let it compete with Opendoor instead of partnering with it.

So Opendoor passes all three tests: it’s the leader in a massive market with a clear path to growing profits and has moats that protects its margins from competitors.

The advantages that Opendoor has over its competitors are also why I think that the company has a legitimate claim at comparing itself to Amazon.

The Bull Case: Opendoor is Amazon for Real Estate

At this point, we’ve established that Opendoor has the potential to be a great business in an enormous market practically untouched by innovation. The thing that gets me most excited about the company, though, is how similar it is to Amazon.

Many of the skeptics’ concerns that I highlighted above are the same concerns that Jeff Bezos once heard. It’s a low margin business. It just keeps losing money. It’s so capital intensive. eBay has a better business model and lower costs; it will eat Amazon’s lunch. Most people won’t want to shop online, anyway.

The criticisms aren’t the only similarities between the two companies. Amazon and Opendoor are similar in four ways:

Customer Obsession

Culture of Frugality

Control Over Profitability

Flywheels

Customer Obsession

Customer Obsession is the leadership principle that Bezos credits most for Amazon’s success. Because Amazon is customer obsessed, it’s now fashionable for companies to say that they’re customer obsessed, too. But few live up to it like Opendoor does.

Everything that Opendoor does is designed to remove friction, lower prices, and create a better experience for customers. As one example, when asked why he would partner with a competitor like Redfin, Wu said,

Customers want choice. The best possible experience is that a customer walks into any funnel and says, ‘Great! What are my options to sell?’ and be fully informed to make a decision both on the economics and the experience. Why not give your customer the option and let them choose? If you start with the customer and walk through the logic, we can all be partners in that.

Choice and experience is one part of the customer obsession, but for such a large transaction, nothing is more important to customers than price. In the same interview, Wu said, “If you make the process cheaper and more efficient, the customer benefits.” The company’s employees are willing to make sacrifices to make that happen.

Culture of Frugality

In Amazon’s early days, instead of buying desks for each new employee, everyone, including Bezos, made their own desks out of doors and 2x4’s. Bezos instilled a culture in which people realized that every penny they didn’t spend on themselves, they could pass on as savings to customers.

Opendoor is Amazon’s spiritual frugality successor, and it has the best core value I’ve ever come across to back it up: bps for breakfast. The value means that employees need to always be on the lookout for ways to cut basis points (bps) from its costs, because the lower the company’s costs, the lower prices it can charge customers.

Wu brought in Amazon executives to help instill that culture. Its President of Homes & Services, Julie Todaro, was the VP of Operations at Amazon. In 2019, the company added Jason Kilar, who held a variety of leadership roles at Amazon, to its board.

He’s also made the hard choices to instill frugality into the company’s culture.

Eliminated free lunch

Installed a $120k salary cap in the early years, and have a higher salary cap in place now

Moved from operating in a decentralized manner to centralizing the core business

Early in COVID, Opendoor laid off 35% of its staff. Critics saw the move as another example of an overfunded, SoftBank-backed company getting over its skis. But given Opendoor’s bps for breakfast culture, I think Wu saw it as an opportunity to get Opendoor’s org structure right.

From 2018 to 2020, Opendoor increased the percentage of fully-automated offers made from 41% to 63%, meaning that algorithms could now do the jobs that humans did before. It’s hard to tell someone they’ve been replaced by an algorithm; COVID made it easier.

Control Over Profitability

A tight grip on costs and deep understanding of the customer gives Opendoor more control over its profitability.

Just like Amazon in the early days, I think that most people are missing Opendoor’s massive potential by focusing on its current low margins and lack of profitability. While every money-losing company claims to be like Amazon, this chart from Opendoor’s investor presentation convinced me that it actually is:

The chart shows the price elasticity of demand for sellers on the Opendoor platform. When Opendoor charges a 6% fee, sellers convert at 44%. When it charges 10%, sellers convert at 23%. Understanding this curve and how it changes by market, price point, and over time is key to understanding that Opendoor can choose whether it wants to grow faster or be more profitable.

This has always been the huge difference between Amazon and the money-burning companies that compare themselves to Amazon: Amazon chooses how profitable it is today to maximize its potential tomorrow, whereas other companies just lose money today and will likely lose money tomorrow.

Opendoor chooses to make less money today in order to make more tomorrow. Take Phoenix as an example, where Opendoor has an Adjusted Gross Margin of 7.3%. Based on the chart above, that means it’s converting somewhere near 36%. If it decided to slow growth by a third, from 35% to 23%, Opendoor could generate an additional 2.7% in contribution margin, increasing CM from 4.0% to 6.7%.

There’s another vector to consider, too. By growing faster, Opendoor is able to do more volume on both its labor (inspectors and contractors) and materials (it laid over 1 million square feet of carpet last year), driving down those costs. It makes sense for Opendoor to give up some short-term contribution margin today in order to drive down costs, which will allow it to lower prices and generate more demand tomorrow, which will... Wait a second…

Amazon and Opendoor’s Flywheels

Amazon and Opendoor obsess over customers and sacrifice comforts to pass on savings to customers not because they’re altruistic, but because doing so creates flywheels that lead to large and growing advantages.

Amazon’s flywheel is famous. It focused on the customer experience because having the best customer experience drives traffic to Amazon, which allows it to attract more sellers, which means more choice, and a better customer experience, which leads to more growth. More growth and a culture of frugality mean a lower cost structure, which means lower prices, which also leads to a better customer experience. Once the wheel starts turning, it just keeps building on itself, and Amazon runs further and further ahead of its competition.

Opendoor has a similar flywheel to Amazon, which Chamath highlighted both on CNBC and in the investor presentation.

As he explains it:

The entire value of Opendoor starts with the ability to make offers, because the more offers they make, the more homes they buy and the more homes they sell.

As they do that, they can win a market, they can refine a playbook, and they can expand with confidence into more and more markets.

As they do that, two things happen:

The first is that they’re able to cross-sell and upsell a whole suite of value added services, and these things have a very good attach rate. They also drive long-term profitability and contribution margin.

All of this scale also allows them to work with their lending partners to secure more and cheaper forms of capital.

Together, all of these things just continue to give consumers more value. It continues to lower costs. And then consumers reward Opendoor with more demand, which then allows Opendoor to make more offers, and then the cycle continues.

The more Opendoor continues to execute on its playbook -- the more offers it makes, the lower costs it drives, the better it prices homes -- the further ahead it gets. This flywheel will allow Opendoor to both win against existing competitors and expand iBuying market share as the costs to customers drive down to levels below what they’re paying in the traditional process today.

Opendoor’s Future

Just like you couldn’t have predicted AWS by looking at Amazon in 2000, it’s hard to predict what Opendoor might look at in twenty years. But that doesn’t mean we can’t try.

Short-term, its plan is obvious because it’s the same one it’s been running for six years: Opendoor will continue to execute on the flywheel by expanding into more markets, lowering costs, and attaching more additional services.

To understand whether Opendoor is succeeding against its plan in the short-term, watch its contribution margins. After it’s officially public, it will have to report earnings every quarter, and contribution margins will be the first thing I look for.

Medium-term, Opendoor will add services beyond the home sale transaction. It has announced plans for moving, but I wouldn’t be surprised if it started offering ongoing home repairs and maintenance, painting, lawn care, cleaning, and anything else related to the home that does one or more of three things:

Lets Opendoor collect proprietary data to feed into the pricing model

Keeps Opendoor top of mind

Improves the experience of living in a home

Long-term, it can achieve its vision of providing real liquidity to the housing market. Imagine a world in which it’s easier to buy a home than it is to rent. Opendoor could provide low transaction costs, fast turnaround times, easy moves, recommended houses, and more. Opendoor can increase its addressable market by increasing the velocity of home transactions and enable the currently-unattainable combination of home ownership and flexibility.

It might also flex its capital markets muscle and unique position in the real estate value chain to create a financial asset that gives investors exposure to city indices, either by syndicating out the equity it holds on its balance sheet or by giving buyers a new form of equity-based financing. I love New York, but I’d love some exposure to markets like Philadelphia, Austin, and Denver right now. Opendoor is best positioned to make my dream come true.

Technology has fundamentally transformed every industry except real estate. Opendoor is changing that. When it does, it could be as big as Amazon… if Amazon doesn’t buy it first.

Big thanks to Dan and Puja for editing what started as my longest draft ever. They saved you.

Disclaimer: This is not investment advice! I have no idea if the stock will go up or down in the short, medium, or long-term. This is just my analysis of Opendoor’s strategy and opportunity.

Thanks for listening,

Packy