Melio: Disrupting the $25T B2B Payments Market

By the Books... A Not Boring Sponsored Deep Dive

Welcome to the 1,222 newly Not Boring people who have joined us since Monday! Join 52,385 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts

Schedule Note: Not Boring is off on Monday for Memorial Day 🇺🇸

Today’s Not Boring, the whole thing, is brought to you by… Melio

Melio is the simplest way for small businesses, like Not Boring, to pay and get paid.

Hi friends 👋 ,

Happy Thursday!

One of the best parts of writing Not Boring is that I get to send out a bat signal about the things I’m interested in and exploring, and then a bunch of smart people share their thoughts and recommendations.

When I wrote Bill-a-Bear in January, and mentioned my displeasure with bill.com, a couple things happened. First, a bunch of people replied saying that I should check out Melio. Second, Melio’s co-founder and CEO, Matan Bar, reached out to tell me about what his team is building, and why. Turns out, I wasn’t alone. Small businesses don’t want complicated software with automations and bells and whistles. They just want to pay and get paid, as easily as they would with Venmo.

I immediately resonated with Melio’s product, and it’s strategy. It’s classic disruption, executed brilliantly thus far. We decided to team up on a piece to tell you about it.

This essay is a Sponsored Deep Dive on Melio. For those who are new around here, that means that Melio is paying me to write about their business, but that it’s a business I would have written about anyway. You can read more about how I pick and work with partners here.

Let’s get to it.

Melio: Disrupting the $25T B2B Payments Market

In January, for the first Not Boring of the year, I strapped on my claws and wrote my first bear take: Bill-A-Bear. In it, I made the case that bill.com was overvalued and susceptible to attack, writing:

Bill.com is the worst software I use to run Not Boring. It takes something that should be joyful -- getting paid! -- and makes it dreadful. That presents an opening for product-first competitors to cut off bill.com’s growth and pick off customers.

After writing that piece, I got two types of responses, from two groups of people:

Founders and Small Business Owners. This group strongly agreed with me. They, too, struggled to figure out bill.com’s product, and they had businesses to run. They shared my dread of logging into bill.com.

Finance and Accounting Professionals. This group vehemently disagreed with me! For them, bill.com’s automations and workflows were great, and actually made their jobs easier. It’s not pretty, but they took the time to learn how to use it and build integrations, and now all of their vendors were on it, so it worked just fine.

Turns out that there’s a segment of the market for which Bill makes sense, but that the vast majority of businesses in the US, most of which are smaller SMBs, are over-served by Bill. That leaves a huge opportunity for both new-market and low-end disruption in B2B payments. SMBs need a smoother, more modern, and more intuitive B2B payments solution, at a lower price, to move off of paper checks or the bank ACH process.

That’s exactly what Melio is building.

Melio, which launched less than two years ago, wants to help small businesses stay in business by making B2B payments fast, simple, and flexible. Melio is fully focused on small businesses, of which there are over 31 million in the US alone. Most of them still use paper checks or bank ACH. Both are slow and full of friction. Of those, 81% are on the small end -- sole proprietors or non-employers. The businesses are small, but the market is huge: SMBs alone do about $14 trillion in payments annually, about $10 trillion of which goes to outside vendors and contractors. That’s trillion, with a T.

Melio wants to make business payments as easy on the front-end as sending a Venmo, with all of the powerful integrations, risk monitoring, and compliance that businesses need built into the back-end.

In January, Melio came out of stealth and announced a $110 million Series C led by Coatue at a $1.3 billion valuation, bringing its total funding to $256 million. It’s ready to fight.

Melio is competing in a seemingly hot and crowded space -- in the past month, bill.com acquired Divvy, Stripe launched more Invoicing features, and B2B payments startups raised big rounds -- but it serves a segment of the market that is still wide open, where it competes with paper checks and banks’ ACH products. It’s a huge market on its own, and the best foothold from which to expand upmarket. How it competes, and why it could win, is the focus of this post.

Today, we’ll look at Melio’s story, product development, viral growth, and future through the lens of disruption. It’s rare that you get such a clear view of disruption playing out in real time. This one’s going to be in the textbooks. We’ll help the professors get started by covering:

Disruption by the Book

Meet Melio

Started from the Bottom

Viral Growth

Stripes, Squares, and Settles, Oh My!

Melio’s Future

Let’s start with the textbook definition of disruption. You’ll need to understand it to be as in awe of the playbook that Melio’s running as I am.

Disruption by the Book

Disruption is a beautiful sight to behold. Watching it in real-time is like watching one of those scenes from Planet Earth in which one animal is just sitting there, fat and happy, while another waits, off-screen, coiling, ready to spring its trap to the dulcet tones of David Attenborough.

We’ve covered disruption in Not Boring a few times, most recently in Who Disrupts the Disrupters? That piece was more theoretical. It was about how today’s large tech companies may be susceptible to disruption by web3 startups.

Today is more of a case study. It’s disruption in real-time. Melio is executing it flawlessly, and to have a connoisseur-like appreciation for what’s happening, you’ll need the definition.

Harvard Business School professors Clayton Christensen and Joseph Bower coined the phrase “disruptive innovation” in a 1995 HBR article titled Disruptive Technologies: Catching the Wave, and Christensen clarified the meaning in a follow-up piece for HBR in 2015.

Disruptive innovation:

Describes a process whereby a smaller company with fewer resources is able to successfully challenge established incumbent businesses.

Specifically, as incumbents focus on improving their products and services for their most demanding (and usually most profitable) customers, they exceed the needs of some segments and ignore the needs of others.

Entrants that prove disruptive begin by successfully targeting those overlooked segments, gaining a foothold by delivering more-suitable functionality—frequently at a lower price.

Incumbents, chasing higher profitability in more-demanding segments, tend not to respond vigorously.

Entrants then move upmarket, delivering the performance that incumbents’ mainstream customers require, while preserving the advantages that drove their early success.

When mainstream customers start adopting the entrants’ offerings in volume, disruption has occurred.

They proposed two types of disruption:

New-market disruption targets under-served customers who weren’t consuming before because they lacked the money, skill, access, ability, or time to consume existing offerings.

Low-end disruption targets over-served customers by paring down products and offering them to consumers at lower prices.

It’s important to keep in mind that the incumbent typically isn’t stupid or unaware. They see the low-end of the market, and they make an intentional strategic choice to focus on their existing customers and the more profitable ones further upmarket. Their goals and incentives are aligned with driving profitability today, and they’re willing to take the chance that a new entrant is able to both figure out how to serve the low-end profitably, and then come upmarket. Disruption is a long process.

But when it works, it works, and it looks obvious in hindsight. Disruption is one of the most-used concepts in business strategy because it’s the playbook that new companies can use to topple incumbents, kind of like Bill. Melio, it turns out, is an example of both new-market disruption and, increasingly, low-end disruption.

When I wrote Bill-A-Bear, I wrote about the way a competitor might topple Bill:

Bill.com has left a wide opening for new entrants to come in and build better AR/AP software that makes getting paid fun and helps companies better manage their cash conversion cycles.

To knock off bill.com, Square, Stripe, Settle, or a new, product-first competitor will need to:

Build a seamless product to feature parity with bill.com on the things that matter to customers.

Build distribution into the product workflows.

Build up enough customer demand to attract enough vendors and partners onto the platform that Bill’s switching costs and network effects are rendered obsolete.

I wrote that from the perspective of a well-funded incumbent like Stripe or Square. I thought it would be very difficult for a new company to go from 0 to 100 to win the market. I underestimated just how big and unserved the SMB segment was.

As I wrote, unbeknownst to me, a group of people in Tel Aviv and NYC were building a product with the features that mattered most to their target customers, with virality built in, growing like a weed.

It’s just that Melio was still in stealth.

Meet Melio

Melio is the simplest way for SMBs to pay each other. It’s like a reverse mullet: party in the front, business in the back.

The front-end feels like a consumer payments product. It’s smooth and fast. I use it, and it is a breath of fresh air after using bill.com. Onboarding took a couple of minutes, and it takes me no more than 15 seconds to send an invoice. Look, I’ll show you.

That party in the front is made possible by powerful technology in the back -- things like risk models that pull directly from bank and payments data, powerful fraud detection, robust compliance, and B2B-grade workflows.

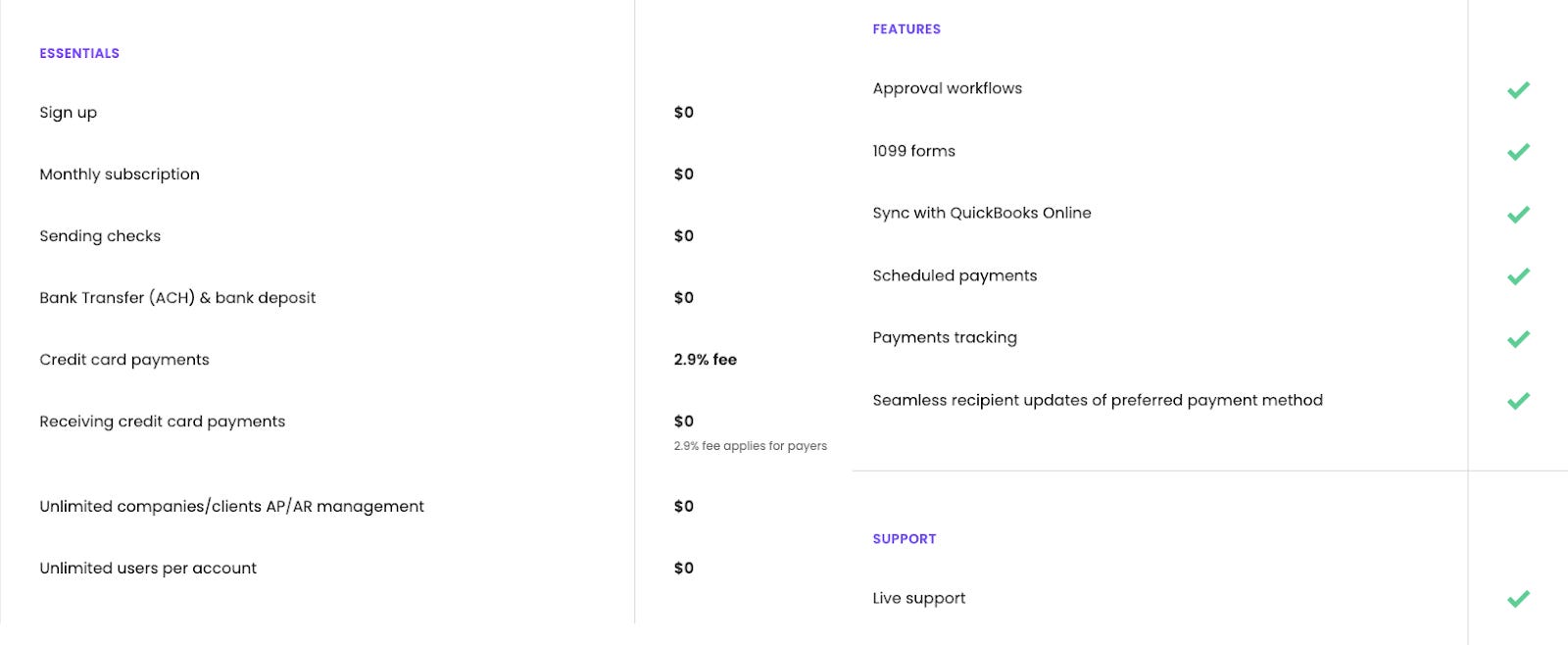

To date, Melio has mainly focused on Accounts Payable (AP) and Accounts Receivable (AR), helping small businesses pay or get paid in whatever way works best -- ACH, debit card, they’ll even mail physical checks. And they do it all for free. They only charge when they help businesses improve their cashflow by sending or receiving money more quickly, or by using a credit card.

Melio is a product born of deep customer empathy and time spent on the light side of the payments industry: consumer.

Matan Bar has been in the payments space for a long time. In 2009, he co-founded The Gifts Project, a group payments platform. eBay acquired the company in 2012, and Matan became the GM of the company’s Israel Innovation Center. In 2015, when eBay spun off PayPal, Matan went with the payments giant, where he led Global P2P Payments, working on PayPal’s own app and its Venmo subsidiary.

Consumer was a great place to start. Peer-to-Peer (P2P) payments are further along than B2B payments. Think about the last time you paid a friend, and the last time your business paid a vendor. They’re entirely different. Venmo takes a second. Paying vendors can take weeks, or longer. Venmo is fun, bill.com is… not fun. And the people who use bill.com are the lucky ones. Most companies still write checks or send payments via ACH and wait days.

B2B payments are also much, much bigger than consumer. Globally, all P2P payments are expected to reach about $4 trillion by 2027. B2B payments are a $25 trillion market, today, in the US alone. Within that, small and medium businesses (SMBs) represent about $10 trillion.

But while small business owners use Venmo to pay their friends, when they’re at work, they write checks. Somewhere around 40% of SMB payments, somehow, still, happen via check.

So in early 2018, Matan teamed up with co-founders Ilan Atias and Ziv Paz to figure out why.

They started out the way you’d expect a new company to start out: they met a lot of small business owners, and they asked them a lot of questions. After a bunch of conversations, though, they realized something important. They didn’t even know which questions to ask.

This is the first lesson to take from the Melio story: you need to feel your customers’ pain as much as they do. Sometimes, founders are the target customer. They leave whatever they were doing before to solve their own pain points. If not, it’s worth taking the time to do things that don’t scale in order to really feel the problem. That’s what Matan, Ilan, and Ziv did.

To understand the pain small business owners feel, they opened a bookkeeping firm in NYC with an Israeli accountant living in the city, signed up 10 clients, and did everything for them, via WhatsApp. They managed Quickbooks. They sent checks. They sent invoices. And they learned.

“Being part of the flow is better than asking questions about the flow,” Matan told me. “We picked up 40 nuances we couldn’t have discovered by asking questions, because we didn’t even know which questions to ask!”

Hard-won insights in hand, they got to building. In mid-2019, they launched in NYC, starting with wine shops.

Started From the Bottom

As incumbents focus on improving their products and services for their most demanding (and usually most profitable) customers, they exceed the needs of some segments and ignore the needs of others. Entrants that prove disruptive begin by successfully targeting those overlooked segments, gaining a foothold by delivering more-suitable functionality—frequently at a lower price.

The first rule of disruption is, intuitively, to start at the low-end, the part of the market that incumbents overserve and overlook as they chase bigger, more profitable customers. Melio isn’t stealing customers from bill.com yet. It doesn’t need to.

Bill.com is focused on mid-sized businesses, and it’s moving upmarket. It has guided investors to expect that it will sign up fewer but larger customers. Classic incumbent move. This is one of the most fascinating things about disruption -- the moves that the incumbent makes often make sense. If Bill can acquire larger customers, it will generate more revenue, more profitably over the next few years. What CEO wouldn’t want that?

But it does leave the low-end of the market wide open for Melio.

Melio started with wine shops, creators, makers, and crafters, small businesses doing tens or hundreds of thousands or low millions of dollars in revenue. Many of these businesses were still paying paper invoices with paper checks, even though bill.com has been around since 2006, and Tipalti since 2010. This is new-market disruption, serving previous non-consumers.

If you want to understand why they didn’t consume existing tech solutions, look no further than the category name: Accounts Payable Automation Solutions.

Matan told Harry Stebbings (and you should listen to the full episode):

Even the name of the category -- Accounts Payables Automation Solutions -- that’s such a terrible name for a category. Accounts Payable is an accounting term, and Automation is this value proposition that probably resonates really well with the CFO of Nike. However, to a wine shop owner that manages 100 payments a month, automation is not that big of a deal… what these businesses care about is cashflow, not automation.

Targeting the low-end of the market means so much more than just which value proposition to highlight, it means building everything completely differently, from the ground up.

The economics are different. A wine shop with no finance team is very different from a Widget Corporation with finance, accounting, and purchasing teams that buy millions of widget parts. Each Melio customer sends fewer payments and spends less money, which changes how Melio need to approach the top and bottom line. Onboarding happens directly in the product. There’s no “Schedule a Demo,” no manual credit checks or risk assessments. The economics don’t support that.

What seems like a constraint can be an advantage, though. Melio needed to build great software to do all of the things that a company targeting larger customers can pay to do manually.

As one example, Matan told me that early on, when Melio started advertising on Facebook, scammers started signing up and making a lot of transactions. They looked like great customers, because they signed up and transacted a lot, right away, so Facebook served them more scammers. They had to choose between cutting off that channel and building fraud detection right into the signup flow to catch them before they could do any damage. They chose the latter. That’s something that Melio can do as a modern tech company that Bill couldn’t with a more manual onboarding.

Those constraints also force focus.

Instead of aiming for full feature parity with the incumbents, including automation, Melio focused on the things that are important to small businesses: self-serve onboarding, a consumer-like experience, and most importantly, cashflow management.

Because Melio spends less to acquire and onboard customers, and because software handles the vast majority of the work to serve them, Melio has low marginal costs and can offer a lower price -- free, in many cases. Customers can use Melio to send and receive payments for free. I’ve collected tens of thousands of dollars through Melio, and I haven’t paid a cent.

Instead, Melio makes money by offering its customers products that improve cashflow. Melio customers can pay a couple of dollars to send payments to vendors more quickly than ACH, for example. Sending payments in one day instead of five means that you can keep cash in your bank account for four extra days. Vendors can also pay to receive money more quickly.

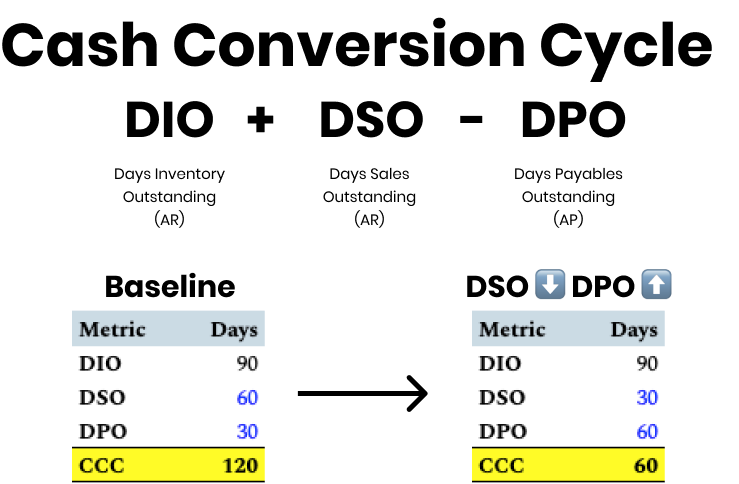

In any business, particularly SMBs, cash is king. A company can improve its cash position without doing a dollar more in sales or cutting any costs by stretching out payables and pulling in receivables. There’s even a formula for it: the Cash Conversion Cycle formula.

Shortening the time it takes to collect money (DSO) or increasing the time it takes to pay money (DPO) both improve the cash conversion cycle. Melio takes risk to make it possible -- one of the biggest loss-drivers for this kind of business is fronting a customer money and getting hit with an “Insufficient Funds” when they try to collect -- and gets a fee in exchange.

To make that possible, Melio uses sophisticated risk and credit models to automatically underwrite any business’ likelihood of payment. The name of the game is extending more credit while taking less risk.

Helping payers and vendors improve their cash conversion cycle isn’t just good for revenue, though. It’s phenomenal for growth. And Melio is growing fast.

Viral Growth

Build distribution into the product workflows.

Two years ago, Melio served a handful of wine shops in NYC. Coming into 2020, it had 30 employees. Then a pandemic hit, threatening to kill the small businesses that were its customers. And yet, Melio grew. And grew. And grew. In 2020, Melio grew monthly active users (MAUs) by 2,200%.

How did it do that?

Melio’s product is naturally viral. It focuses on AP and AR for small businesses, each of whom have dozens or even hundreds of vendors. When a Melio customer wants to pay a vendor, they add bill details, connect their bank account or enter their credit card, and send a payment request to the vendor.

The vendor doesn’t need a Melio account to receive a payment -- Melio will send a paper check or ask them to enter their bank details -- but if they do sign up, they get paid faster. That’s a pretty strong incentive, and it seems to be working. The graphic below shows how Melio has spread among wine merchants and distributors.

The purple boxes represent customers who use Melio to send payments, and you can see how it flows: a customer pays a vendor, some of those vendors set up an account to receive payments more quickly, and some of those vendors start paying their vendors using Melio. This viral growth allows Melio to serve small businesses profitably in ways that larger incumbents can’t.

Viral and rapid growth explains why Melio, less than three years in, was valued at $1.3 billion. And it explains why I think Melio will overtake Bill in the next couple of years. In Ramp’s Double Unicorn Rounds, I wrote that “trajectory really matters, and it matters more than you can easily comprehend” to explain how Ramp, less than two years old, could be worth $1.6 billion. The same argument applies to Melio, and we can compare it with Bill, a public company, to see why.

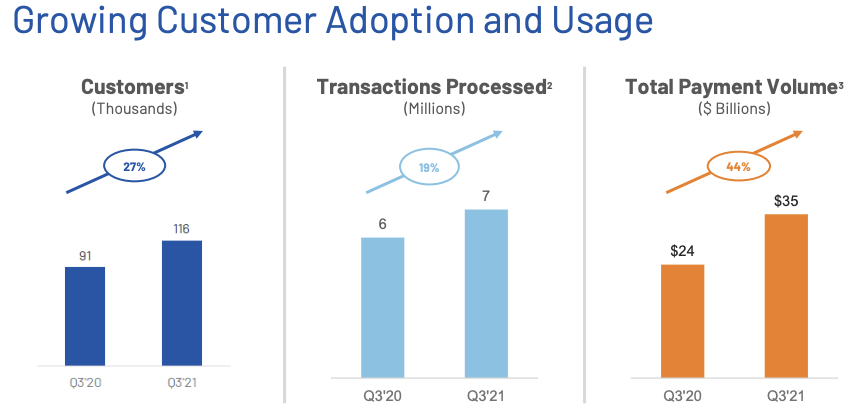

In 2020, Melio grew off of a relatively small base, but now, it has “tens of thousands” of customers and handles “double-digit billions” of payments volume annually. Off of this much larger base, it’s still growing by a percentage in the “high-teens” every month. Matan wouldn’t tell me the actual numbers, so let’s make some conservative estimates and see what Melio’s growth looks like.

Let’s use 30,000 customers, $11 billion in payments volume, and 16% MoM growth in year one, dropping to 8% MoM growth in year two.

For comparison, as of Q3 2021, bill.com’s numbers looked like this, and we’ll assume that those growth numbers remain consistent for the next two years.

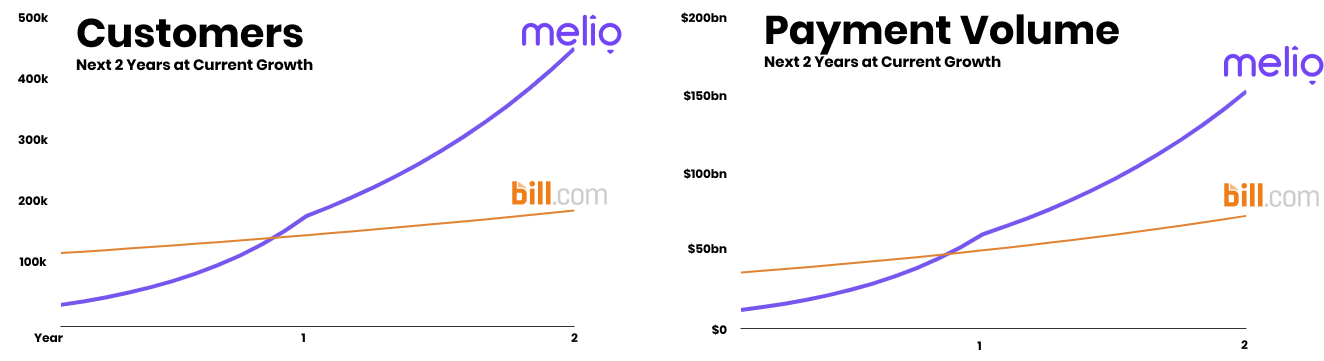

Ok, so running those numbers through my trusty spreadsheet, beep boop bop:

That’s the beautiful thing about growth, and why the best startups are worth so much so early. Trajectory matters a lot. Slope over intercept. There are a lot of assumptions in that chart, but it seems as if, even if Melio’s growth slows by half, it will surpass Bill by customers -- which makes sense, it’s going after smaller customers, of which there are more -- and even payment volume over the next twelve months.

A lot could change between now and then, and it’s harder to grow the bigger you get, but it illustrates the power of disruption. A new entrant can pick up steam in the low-end of the market, and use momentum to propel past the incumbent.

That doesn’t necessarily spell doom for Bill, though. As they continue to move upmarket, they’ll get larger and more profitable customers. Combined, Melio and Bill serve fewer than 1% of the estimated 31 million US SMBs that Melio sees as potential customers. Both of them are fighting a battle against paper invoices, paper checks, and ACH, and both want to help businesses manage cashflow to survive and thrive.

They’re also not alone.

Stripes, Squares, and Settles, Oh My!

The B2B payments space is heating up. In just the past few months:

Stripe rolled out new features to its Invoicing product

Bill.com acquired Ramp-competitor Divvy for $2.5 billion

Routable raised a $30 million Series B led by the Altman brothers

Settle raised a $15 million Series A

It’s surprising it’s taken this long. There are not many $25 trillion markets in the world. How will Melio win?

There’s a short answer and a long answer.

The short answer is: this is not a winner-take-all market, and Melio has carved out a massive niche in the SMB segment. There are trillions of dollars worth of transactions happening via paper invoices and paper checks in the US alone, and more when you include ACH; the more companies working to fix that really well for different customer segments, the better.

The long answer depends on which competitor and customer segment we’re talking about.

For Consumer-to-Business (C2B) payments companies like Square and Stripe, everything that they’ve built is oriented towards customers buying from businesses. It seems like a minor-ish distinction, but it means that they’ve built differently. As one example, these businesses’ risk and compliance models are set up differently than an AP solution. They have a relationship with the payee, the one receiving the money, whereas Melio’s risk and compliance models are built to understand the payor, the one sending the money. Beyond that, there are so many little things that add up to a cohesive experience -- like how to handle payment terms, internal workflows, and checks -- that Melio is fully focused on. Stripe Invoicing and Square Invoices will undoubtedly see a lot of demand with their existing customer bases, but that’s a different group than Melio targets.

Settleis very focused on getting direct-to-consumer companies more working capital. In addition to bill pay, they also extend their customers payment terms of 30-120 days. That’s not a space in which Melio competes yet, but the two may become competitive as Melio rolls out more lending products. Again, though, they’re focused on different customers.

Routable looks to be attempting to go head-to-head with Bill with a tech-savvier solution. They highlight tech companies as their customers, and also tout automation as a value prop. They do it by building the type of software tech companies are used to, including a B2B payments API.

With the Divvy acquisition, Bill.com is trying to infuse some new-school vibes into its old-school offering. It recognizes the potential synergies between a corporate card and B2B payments -- for one, the buyer is likely the same for each. The move represents a push further into the finance suite, and further away from SMBs led by owner-operators.

Interestingly, the further you dig in, the more it seems that the competition is happening in the middle and high-ends of the market, leaving Melio to capture the low-end… and grow from there.

Melio’s Future

Entrants then move upmarket, delivering the performance that incumbents’ mainstream customers require, while preserving the advantages that drove their early success. When mainstream customers start adopting the entrants’ offerings in volume, disruption has occurred.

Aka build up enough customer demand to attract enough vendors and partners onto the platform that Bill’s switching costs and network effects are rendered obsolete.

Currently, Melio is pursuing new-market disruption. Most SMBs have been ignored and unserved by fintech companies. That makes sense, by the way. Since the whole market was ripe for the picking, the logical move was to go after the juiciest segment. That left a huge opportunity for Melio, though: there are enough SMBs still using paper, who have not entered the world of digital B2B payments at all, that they’ll have years’ worth of opportunity in that segment of the market alone.

Plus, the segment keeps growing. According to Yelp’s Q1 Economic Average Report, over 56k new small businesses launched in the US in March 2021 alone.

These are brand new businesses with no established workflows that will need to pay other businesses. Each monthly cohort represents an opportunity larger than Melio’s current customer base. This will be a $10B+ company just by winning its fair share of new US SMBs as they pop up. It’s all about helping those new small businesses stay in business.

At the same time, though, Melio is being pulled towards low-end disruption -- targeting over-served customers with pared down products at a lower price. Because SMBs don’t just pay SMBs, they also pay larger companies.

When they do, they’re spreading Melio to companies that might otherwise use bill.com or another competitor. Since Melio has had to build a tech-first product from the ground up to serve the lower end of the market, they offer a better, cleaner, more modern experience. Once businesses experience it for themselves, they may switch.

This is the final stage of disruption, building out features that incumbents’ mainstream customers require while keeping the magic that made the company appealing to new or over-served customers in the first place.

Matan admitted that their AP product received a lot more attention in the first few years than their AR product did. AP is the biggest pain point for SMBs, and the biggest growth driver. But well-funded and growing, with 270 new employees since last year, there are full teams dedicated to bringing the rest of Melio’s product offering to par with its AP solution. In just the last couple of weeks, they rolled out a Pro version of the AR product, for example.

It’s clean, fast, easy, and appealing to previously over-served customers. Look at me. I was using bill.com (and still do when certain sponsors make me, network effects and switching costs are hard to overcome!), but I’ve moved as much of my invoicing over to Melio as possible. It feels so much more like the software I’m used to using everywhere else and it’s free. It’s a no-brainer.

The opportunity ahead of Melio is massive. The challenge is equally big. To serve more mainstream customers, it will need to add a lot of complexity on the back-end, while keeping it all abstracted away from the user on the front-end. To expand wallet share with existing customers, and help small businesses stay in business, it will need to add new products. Melio should be able to roll out lending, for example, using the same data and models they currently use to give customers more cushion.

The biggest challenge, though, will be remaining focused on the customers that got them here in the first place, America’s SMBs. Going upmarket while preserving the advantages that are driving its early success. That’s how Melio will avoid getting disrupted itself.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading, see you Monday after next!

Packy

Really? Payers agree to pay 2.9% for each ACH transaction instead of $0.3-$0.6 per transaction which is the market price for ACH? For how long...?

Really sharp breakdown - especially how Melio’s focus on SMB cash flow and simplicity contrasts with feature-heavy incumbents. TCLM often explores the financial side of these shifts: how B2B payment tools impact trade credit, working capital, and liquidity management. Might be useful alongside your strategy view.

(It’s free)- https://tradecredit.substack.com/