Welcome to the 1,301 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 13,507 smart, curious folks by subscribing here!

Hi friends 👋,

Happy Tuesday! I hope you enjoyed the Labor Day Weekend.

In case last week seems oh so long ago, a little refresher: tech stocks were on an all-time tear until Thursday, when the music stopped and prices tumbled.

The Financial Times did some digging and discovered that an old Not Boring favorite was behind the market’s rise and fall. That’s right… SoftBank is at it again.

Brought to you by… Teachable: Share What You Know Summit

Fun fact: I started this newsletter in May 2019 as an assignment for an online writing course I was taking. That course was built on my favorite Passion Economy platform: Teachable.

Smart people have made over $850 million teaching what they know in courses built on Teachable, and in two weeks, the company is hosting a three-day Summit to share everything that successful creators — including Not Boring favorites Li Jin, Tiago Forte, and Ankur Nagpal — have learned about turning their knowledge into money. I’ll be there taking notes.

Tickets are $29 this week, and going up to $39 on Friday, so get in now. If you want to start or grow an online or content-based business, this will pay for itself thousands of times over.

Now let’s get to it.

Masa Madness

Before I wrote this newsletter, I worked for a company called Breather, where part of my job was running our real estate team. We were responsible for finding and negotiating leases on office spaces that we would design, build, and rent out to clients for shorter time periods.

As we moved upmarket (longer rentals in bigger spaces), we increasingly competed with WeWork for both spaces and clients. It sucked.

Every space we looked at, WeWork looked at. For a space that would typically cost $65/sf, they would offer $70/sf. When brokers brought WeWork potential customers, they would pay up to 100% of one year’s rent as a commission. If a customer asked for an expensive buildout, they would do it. Different WeWork locations would even compete with each other for the same customer by offering lower prices.

We ran our underwriting model to understand if we could do the same things that they could to acquire spaces or customers, and we couldn’t figure out how to make the numbers work. Because they didn’t. And they didn’t have to. Because WeWork was backed by SoftBank.

Dunking on SoftBank became de rigueur when the market realized what all of us in the industry already knew - that WeWork’s unit economics were terrible because they were trying to use capital as their moat. And it wasn’t just WeWork.

Wag. Brandless. Katerra. Uber. Compass. Bloomberg called SoftBank “the Pied Piper of Unicorns” as it lured startups to giant pools of money in which they drowned.

After WeWork’s downfall, the man behind the madness, Softbank CEO Masayoshi Son, or Masa, admitted that maybe he’d made some mistakes. He feigned contrition. Along with the company’s first quarterly earnings loss in 14 years last November, Son told investors, “My investment judgment was poor in many ways and I am reflecting on that.”

And it kinda seemed like he meant it. Masa and SoftBank have stayed relatively quiet by their standards. It announced that it would unload more than $50 billion of legacy assets including stakes in T-Mobile US, Alibaba, and its own Japanese telecom business to shore up its balance sheet and buy back shares. Conservative move. Nice.

The market bought it. SoftBank shares recovered from the 2,687¥ ($25.25) level post-earnings loss in November to as high as 6,932¥ ($65.16) in late August.

Then last Friday, the FT dropped a bomb. Masa and his team of profligate spenders were behind the massive runup and subsequent crash in tech stocks. The Son of a bitch had done it again.

Hard Truth About SoftBank

After I wrote about Stripe last week, one of my favorite anonymous alt accounts on Twitter goaded me:

My brain doesn’t normally work like that. I’m an optimist. But when I saw that SoftBank was behind the public market tech pump and dump, I knew I had my target.

It’s easy to look at SoftBank’s moves and think, “Fuck these guys,” particularly after my experience competing against WeWork. That was my first reaction when the news dropped. SoftBank distorts the markets it plays in. It has had some spectacular private market blowups. And now, it’s messing up the public markets, too.

Because SoftBank is so nakedly ambitious and takes such big swings, it’s extremely polarizing. Most recently, SoftBank’s Vision Fund went from “This is going to change the world” to “They’re ruining venture capital” to “See! This guy is an idiot” in the blink of an eye. As a result, there’s not a lot of nuance in the conversation around the company.

That’s what I’ll try to bring today, by covering the three ways to look at SoftBank:

Bullish: Masa has a vision that no one fully appreciates and trades at a discount

Neutral: Masa is Lennie from Of Mice and Men for Tech Companies (I’ll explain)

Bearish: Masa is just a WallStreetBets Trader with a lot of other people’s money

SoftBank is a reflection of its founder. Masa is optimistic and hyperbolic. He is a mix of finance and technology, but is much better suited towards the latter and gets himself in trouble (with a couple of very notable exceptions) when he goes too far towards the former.

In a 2014 interview with Charlie Rose, at a time when both men’s reputations were cleaner than they are today, Masayoshi Son compared himself to Steve Jobs.

“If Steve is art and technology,” he said, “I am finance and technology.”

Masa’s history, and SoftBank’s, is a decades-long progression from one end of that spectrum to the other. The further it veers from technology into finance, the riskier it becomes.

Masa often sees only the upside while ignoring downside risk - a valuable characteristic in a technology entrepreneur and a liability in a financier. It’s easy to root against Masa without knowing his story, but hard to root against him once you do.

Meet Masa

Born in a fishing village in Japan in 1957 to a family of Korean immigrants, at a time when being an immigrant in Japan was not a good place to start, Masayoshi Son came into the world with a chip on his shoulder. The Japanese government forced Son’s family to change its surname to a Japanese one, Yasumoto. Masayoshi hated it. Luckily, he was gifted enough to make his own name for himself.

When he was sixteen, Masa cold called the founder and president of McDonald’s Japan, and receiving no response, flew to Tokyo and sat in the man’s reception area until he gave in and agreed to meet with the precocious teenager. During those fifteen minutes, he gave Masa two pieces of advice:

Learn English.

Study computer science.

Ever impatient, Masa moved to the US that same year. He dispensed with high school quickly.

I went to school at Serramonte High School. I had spent three months in Japan as a freshman in high school, so I entered Serramonte High School as a sophomore. After one week, I was promoted to a junior. After three or four days as a junior, I was promoted to a senior. I was a senior for another three or four days, then I took an exam and graduated. The result was that I finished high school in the United States in two weeks. Then I went to Holy Names College for my freshman and sophomore years before transferring to Berkeley.

Wanna guess what he studied at Berkeley?

Economics and Computer Science. There it is: Finance and Technology.

He started his career on the tech side of the spectrum.

While at school, he patented an electronic translator with a professor, Forrest Mozer, and sold the patent to Sharp for around $1 million within a year.

He also imported hit arcade games, like Pac Man and Space Invaders, from Japan, tweaked the software to make the games US-friendly, and made at least a million dollars doing that, too. He made game software, too, and sold his stake in that company, Unison World, to his associate in that venture for close to $2 million.

None of these companies would be his life’s work, though. After selling those businesses, he moved back to Japan as a young millionaire, changed his surname back to the Korean “Son,” and spent about a year and a half thinking. In a 1992 interview, a decade into the SoftBank’s life, he told HBR:

I spent all my time just thinking and thinking, studying what to do. I went to the library and bookstores. I bought books, I read all kinds of materials to prepare for what I would do for the next 50 years. Then I had about 25 success measures that I used to decide which idea to pursue. One success measure was that I should fall in love with a particular business for the next 50 years at least.

He launched SoftBank, the company he still runs today, in 1981 -- 39 years ago. SoftBank started its life as a distributor of PC software at a time when computers were viewed as toys in Japan and when software was sold on disks in stores. Within one year, he grew SoftBank’s sales from $10,000 to $2.3 million.

Six months into the new business and already restless, Masa launched two magazines simultaneously - Oh!PC and Oh!MZ. He wanted to own both software and content in the growing computer space.

Over the next decade, Masa grew SoftBank’s sales to $354 million.

Flush with cash, Masa transformed SoftBank in the 1990s, taking the first steps towards turning it into a finance company:

1994: Went public on the Tokyo Stock Exchange at a $3 billion market cap.

1995: Bought US-based tech media company, Ziff-Davis, and Comdex, which threw events that were the SXSW of the day.

1996: Launched a venture fund; Invested $100 million for 35% of Yahoo! and created Yahoo! Japan in a JV.

1999: Turned SoftBank into a holding company.

In the late ‘90s and 2000, SoftBank’s venture fund made over 100 investments in startups, the most successful of which is one of the best venture investments of all time. Masa personally led SoftBank’s $20 million investment in Alibaba, and gradually built up the position to 34% ownership. Of the meeting that led to the investment, Alibaba CEO Jack Ma told the WSJ in 2000:

We didn't talk about revenues; we didn't even talk about a business model. We just talked about a shared vision. Both of us make quick decisions.

When Alibaba IPO’d in 2014, the investment was worth $60 billion, a 3,000x return. This is one of the few times that Masa’s finance side paid off, and like a gambler hitting his number on the roulette wheel, gave him the irrational confidence, and bankroll, that would get him in trouble down the line.

Back in 2000, fueled by the dot-com bubble, Masa briefly became the world’s richest man. He told Charlie Rose, “For three days, I was richer than Bill Gates. For three days, we were a $200 billion market cap.”

Then, the bubble burst, and Masa lost more money than anyone in the history of the world. SoftBank’s market cap tumbled 99% to $2 billion, and Masa’s net worth followed suit, plummeting from $70 billion to $600 million.

Masa had leveraged profits from his technology operating business into financial investments. At first, it worked tremendously well, because the late 90s were a great time to be a techno-optimist. Then it failed spectacularly, because the early 2000s were a terrible time to be a techno-optimist.

Despite his nauseating losses, though, Masa remained optimistic and aggressive. He foresaw that just as the ‘90s were about the rise of the internet, the mobile internet would be the next wave. But he didn’t have a mobile play and he’d (temporarily) learned his lesson about arms-length investing, so he set his sights on acquiring and operating Vodafone Japan.

In 2005, before buying Vodafone, Masa flew to Cupertino to meet with Steve Jobs, bringing with him a sketch that he’d drawn himself of an iPod phone. He wanted Jobs to make it. Jobs told him, “We’re actually working on this already, so I don’t need your sketch, but since you’re the first person to come and see me about this, I’ll give you the exclusive rights in Japan.”

With the iPhone rights up his sleeve, Masa convinced a banker at Deutsche Bank, Rajeev Misra (remember that name), to loan SoftBank the $20 billion it would need for the acquisition.

The bet paid off. SoftBank rebranded Vodafone Japan as SoftBank Mobile and launched the iPhone in Japan in 2008. It acquired Sprint for another $20 billion in 2013 to go deeper on mobile. From a low of 418¥ ($3.92) in late 2008, SoftBank’s share price more than 10x’ed over the next six years, peaking at 4,370¥ ($41.08) on September 14th, 2014, the day that Alibaba IPO’d, driven by three things: Yahoo! Japan, the Alibaba investment, and SoftBank Mobile.

Riding high on his operating wins, Masa geared up for his most ambitious bet yet.

The Vision Fund

If you’re familiar with SoftBank, it’s probably because of the Vision Fund. It’s the most ambitious and controversial venture capital fund ever raised, and it massively distorted the private startup market. After nearly two decades operating, Masa was ready to get back to investing.

When Masa met with Saudi Crown Prince Mohammed bin Salman (“MBS”) in September 2016, he offered him a $1 trillion gift. “Give me $100 billion,” he said, “and I will give you back $1 trillion.” Masa laid out his vision for an AI-powered future, and his plan to both bring it into being and profit from its existence through the Vision Fund. MBS was sold. After 45 minutes, he agreed to invest $45 billion.

Eight months later, in May 2017, Masa launched the Vision Fund with $28 billion of SoftBank’s own capital, $45 billion from the Saudis, $15 billion from the UAE’s fund, Mubadala, and $1-3 billion each from Apple, Qualcomm, Sharp, Foxconn, and Larry Ellison’s family office.

The fund is unique not only for its size, but for its term as well. Whereas most venture funds have a 5-10 year time horizon, the Vision Fund has a 12 year time horizon with a two year extension. Masa controls a lot of money for a long time. To run the Vision Fund, Masa brought in Rajeev Misra, the Deutsche banker who gave him the loan to acquire Vodafone Japan.

SoftBank set out to make investments in companies that would bring about an AI-powered future in which humans live harmoniously with machines. It was meant to be the financial manifestation of SoftBank’s 30-Year Vision, as laid out in this insane 2010 presentation.

Far from focusing on AI investments, however, SoftBank built a portfolio of capital intensive, atoms-based companies. When you have $100 billion to deploy, it’s tempting to invest in the kinds of businesses that can consume a lot of cash, even if those are the worst businesses to invest in.

Over its first three years, SoftBank invested in 86 companies, including:

$18.5 billion WeWork

$9.3 billion in Uber

$8.2 billion in ARM Holdings (about 25% of SoftBank Group’s full ownership of the company)

$5 billion in NVIDIA

$2.5 billion in Flipkart

$2.3 billion in GM’s Cruise

$1.9 billion in PayTM

Investments in Compass, Katerra, Oyo, Opendoor, and other real estate companies

The knocks on the Vision Fund are manifold:

Aggressive Overbids. The Vision Fund is notorious for offering companies multiples more money at higher valuations than they were planning on raising and threatening to invest in competitors instead if they said no. If a company set out to raise $250 million, Masa asked them what they’d do if they had a billion. This elbowed out other investors and inflated private market valuations for startups.

Self-Markups. In order to show gains on its investments, SoftBank invested in follow-on rounds at higher valuations. Since no one else was willing to pay what they were, they were artificially setting prices higher than the private, and eventually public, markets were willing to bear.

Capital as a Moat. The Vision Fund stuffed money down its portfolio companies’ throats under the assumption that the best-funded startup could outspend competitors and win winner-takes-all markets. Having capital as a moat, though, meant businesses ignored real, sustainable moats.

SoftBank brashly poured billions of dollars into “tech-enabled businesses” with large CapEx requirements, like WeWork and a dog walking company, Wag, and pushed them to grow fast. That’s how we found ourselves in the situation we did at Breather, faced with a competitor that pursued growth to the exclusion of unit economics.

In many cases, though, not only was more capital not a moat, it actually actively harmed the recipient. Companies like WeWork, Wag, Brandless, Compass, and Uber abandoned the strategies and tactics that got them to where they were, pivoting to unsustainable spending in order to grow. Each of those companies has faced massive difficulties, with many having to lay off hundreds of employees and sheepishly emphasize that they’re now focused on strengthening unit economics and achieving profitability.

Many of the Vision Fund’s investments were simply bad investments, and many were good companies fatally wounded by SoftBank’s money and attention. Masa was a better entrepreneur than many of the entrepreneurs he invested in, and a worse investor than many of the investors he crowded out.

Last July, SoftBank announced that it planned to do it again, and bigger, with the $108 billion Vision Fund 2, focused (for realsies this time) on AI investments. In the middle of fundraising, though, the wheels started to come off of Vision Fund I.

In September, just weeks away from going public, WeWork’s embarrassing S-1 and subsequent revelations of mismanagement tanked its IPO. In May of this year, due to a WeWork writedown and Uber’s post-IPO underperformance, SoftBank announced a $17.7 billion loss in the Vision Fund for the Fiscal Year ended March 31, 2020, wiping out any other SoftBank Group profits and causing a $13 billion loss for the parent company.

Masa placed some of the blame on the “Valley of Coronavirus” that many of the Vision Fund’s unicorns fell into.

He also halted plans to raise outside capital for Vision Fund 2, moving forward with only the $38 billion that SoftBank Group invested into the fund off of its balance sheet. In March, pushed by the activist hedge fund Elliott Management, it announced plans to sell $41 billion worth of assets (it recently announced it would actually do $50 billion) including part of its stakes in Alibaba, Sprint/T-Mobile, and SoftBank Mobile to shore up its balance sheet by paying down debt and buying back shares.

That plan is underway. On July 30th, it approved a $9.6 billion tranche of buybacks, half of the nearly $20 billion it will repurchase. On August 3rd, its stock hit 6,932¥ ($65.16), higher than it’s been since the dot com bubble burst twenty years ago.

It seemed that Masa had learned his lesson -- that it’s impossible to brute force your way to victory -- and was retreating before his next big push.

And then last Friday, the FT reported that SoftBank was up to its old tricks again.

The 555 Fund

Not content to just blow up private market valuations, SoftBank spent the last couple of months pouring fuel on public market caps. In the process, Masa has moved squarely from technology to finance, and from visionary to mercenary.

After plummeting early in COVID, tech stocks have been on a tear. Some of the move has been warranted -- we have been spending more of our lives and money online, and tech companies are benefiting. But the moves have been too big, too fast. Tesla is up 800% YTD. Zoom is up over 300%. Apple is up 125% with a market cap over $2 trillion.

Whispers rippled across Wall Street trading desks that a “NASDAQ Whale” was behind it all.

Until Friday, no one thought to connect a recent announcement out of Tokyo to the move. On August 10th, along with reporting quarterly profits of $12 billion and highlighting the Vision Fund’s $2.8 billion quarterly gain, Masa announced the creation of a $555 million fund to invest in tech giants like Apple, Amazon, and Facebook.

Scratch that. Turns out 555 was just a placeholder name and not the fund size. That number is closer to $10 billion, and growing. “555” is slang for “Go Go Go” in Japanese gaming culture, and go go go it did. Over the spring and early summer, the fund bought $4 billion worth of shares in companies including Amazon, Microsoft, Netflix, and Tesla.

Then on Friday, the FT reported that SoftBank was the “NASDAQ Whale” behind billions of dollars of call option trades on the tech giants. Those trades fueled a massive rally in tech stocks, and last week’s steep decline.

Even with $10 billion, though, you can’t typically move markets. So how’d the 555 Fund do it?

Bought $4 billion worth of shares in major tech companies.

Bought $4 billion worth of call options on $30 billion worth of those same companies’ shares.

$4 billion is a lot of stock to buy in just a few companies, but it’s not unusual. $4 billion in call options, however, is an extraordinary amount, because call options can give their owners exposure to more shares for less money. With $4 billion, SoftBank was able to gain exposure to $30 billion worth of shares. Here’s how:

Call options give the buyer the right to buy a stock at a given price (the strike price) on a certain date (expiration). As an example, Apple is trading at $120 today. With $1,000, I could either buy:

Eight shares of Apple stock (😴), or

1,000 calls on Apple stock at a $170 strike price expiring on October 16th for $1 each

The latter gives me more leverage to make money and to move Apple’s price.

Whether I buy shares or call options, the most I can lose is the $1,000 I invested. But if the price goes above $170, I can make a lot more money, and the person selling me the option can lose a lot more money, by trading calls.

If the price goes to $200, I make $29,000 ($200 - $171 * 1,000). If the price somehow goes to $250, I can make $79,000. My gains and her losses can go infinitely high since stocks have unlimited upside.

If the price goes to $250, I’d generate a 108% return by buying the stock, but a 79x return with calls! This is why WallStreetBets traders with small accounts love options trading, and why the lottery is called the “poor tax.” They give you a small chance to turn a little money into a lot.

The downside is equally dizzying for the call seller, and not nearly as fun. So instead of taking that risk, she “hedges,” either by buying shares of Apple today so that she can just give those shares to me in case the price is above $170, or by buying calls herself to neutralize her exposure. By buying either shares or calls, she pushes up their price. In either case, I win.

Now with $1,000, I can’t actually move the market. But with $4 billion of calls, SoftBank is effectively forcing sellers to buy tens of billions of dollars worth of stock, which can push the market faster in the direction it’s been trending anyway.

This is an incredibly Masa way to trade. He’s not passive; he likes to alter the markets he plays in.

In the private markets, with a $100 billion fund, he can bully companies and send valuations soaring above reasonable levels. The public markets are much bigger, though. Buying $4 billion of Apple shares would barely make a dent on the company’s $2 trillion market cap. Buying $4 billion worth of calls, though, particularly during the slow summer months when a lot of traders are vacationing, gives Masa leverage to move the markets and make beaucoup bucks in the process.

It’s a quick way to make up losses if it works. So far, it’s working. Over the weekend, the FT reported that as of last week, SoftBank was actually up $4 billion on the trades, even after Thursday and Friday’s decline, although they haven’t sold the positions yet and are at-risk if tech stocks tumble further this week. In just a couple of months, between the rise in the underlying stock prices and the options premiums, the 555 Fund has made up a good chunk of the Vision Fund’s losses.

Options are a very dangerous game, though. Masa, and Rajeev Misra, brought in a host of ex-Deutsche Bank traders and bankers to help run SoftBank Investment Advisers, which manages both the Vision Fund and the 555 Fund. In October, efinancial careers reported that many of those people are the same ones who tanked Deutsche Bank with bad derivatives trading.

Notably, the ex-DB team is largely made up of credit and derivatives traders, not tech equity investors. With this latest move, Masa has gone from technology to finance all the way to financial engineering.

So what does it all mean? Is SoftBank good or evil? Should investors be bearish or bullish?

The Bull Case

Masa has a vision that no one fully appreciates, and you can buy SoftBank at a massive discount to book.

For those of us who were introduced to Masa through the Vision Fund, it’s easy to look at his tactics and hate him, his company, and everything he stands for.

But watching Masa’s interviews and learning more about his story, I’ve come to appreciate him. He’s kind of adorable, and I genuinely think he wants to make the world a better place. Plus, he’s been right before:

His $20 million check into Alibaba was one of the best tech investments of all time.

Yahoo! Japan was a major success.

He nailed the timing of the mobile revolution.

Convincing Steve Jobs to give him the exclusive rights to sell the iPhone in Japan before he even owned a wireless carrier is one of my new favorite business stories.

With rose colored glasses on, you can even squint and see the Vision Fund as genius. 10x Genomics has doubled its market cap as a public company, the world has woken up to ByteDance’s value two years after Masa invested, and y’all know how I feel about Slack. Sure WeWork has been a dog and Uber is struggling, but maybe Masa just got a little carried away, and they’re just fun stories for the media to pile onto.

If just a few of the 86 investments become breakout successes, he might yet be able to return the fund, and even if he doesn’t, the management fees on $72 billion ($100 billion minus SoftBank’s own investment) are nice steady cashflow. He set the twelve year time horizon for a reason; technology bets can take time to pay off.

And the 555 Fund, despite messing with the market, is up! He’s wrestled gains from the jaws of defeat yet again. If it blows up, assuming they’re not trading on margin, they’ve only lost $4 billion in options premium, a relative drop in the bucket. But the upside is massive. It’s actually kind of smart.

If you subscribe to the idea that Masa’s still got it and is among the world’s most visionary operators and investors, there’s a case to be made that SoftBank is just hitting an early rough patch on the road to a massive opportunity. People underestimate how big an impact technology is yet to make; Masa does not. If he needs to be the villain for a couple of years while everyone else catches up to his vision, so be it.

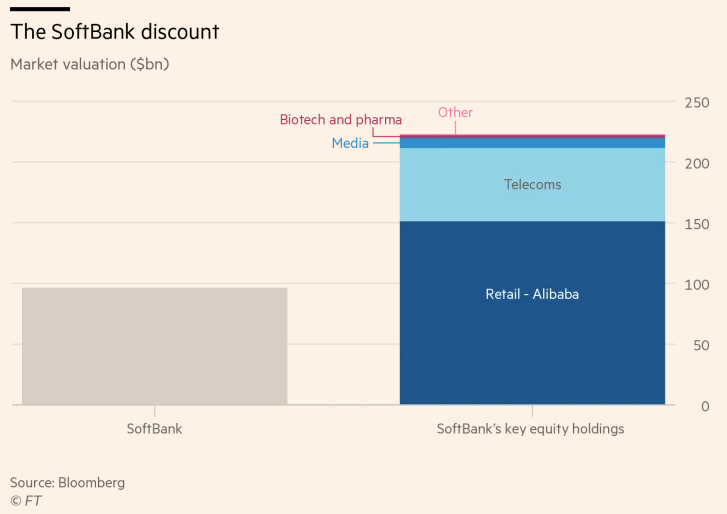

Plus, because people think that Masa might be insane, SoftBank trades at a steep discount to the book value of its assets. Before it started selling off part of its stake in Alibaba, for example, its ownership of Alibaba was worth more than SoftBank’s entire market cap.

When Elliott Management took a $2.5 billion position in SoftBank in February, they did so because they believed that the company could close that gap. And SoftBank is playing ball with Elliott, agreeing to the $20 billion worth of share buybacks the hedge fund demanded.

In the bull case, when you buy SoftBank at its current 11 trillion yen ($104 billion) market cap, you’re getting a deeply discounted portfolio of assets plus the potential upside if Masa is right in his vision of the future. He’s been right before.

The Neutral Case

Masa is like Lennie from Of Mice and Men, loving his investments so much that he crushes them.

The night before my wedding, my great friend and groomsman Nick got up to make his speech. In it, he compared my high school dating life to Lennie, a character in John Steinbeck’s novel, Of Mice and Men. Lennie was a simpleton. He loved his rabbits so much that when he pets them, he invariably crushes them to death. I didn’t harm any rabbits, but Nick argued that when I had a crush on someone, I would get so excited that I couldn’t play it cool.

In the Neutral Case, Masa is Lennie, and tech / tech-adjacent companies are the rabbits.

He couldn’t help himself but to turn SoftBank’s profits into investments in exciting new startups that matched his vision for an internet-powered future in the runup to the dot com crash.

He overfunded companies through the Vision Fund not to mark up his own valuations and crowd out other investors, but because he was so excited to see what these potentially revolutionary companies could do if money was no issue.

He wasn’t trying to manipulate the market via the 555 Fund, he just so strongly believes in the potential of technology companies that he wants long and leveraged exposure any way he can get it.

Masa and SoftBank aren’t evil or manipulative, this argument goes, they’re just really, really excited and they don’t know their own strength. Time will tell if their enthusiasm and approach are warranted.

The Bear Case

SoftBank is just a WallStreetBets Trader with tens of billions of other people’s money.

Remember that strategy that I told you about earlier? The one in which you buy call options in big volumes to force the fund writing the calls to buy the underlying stock, driving up prices? If it sounds at all familiar, that may be because it’s the same one employed by the Robinhood traders on the now-infamous WallStreetBets subreddit.

During COVID, one of the persistent themes in the market has been that retail traders, like the ones on WSB and people who trade on Robinhood more broadly, have been moving the markets with their dumb trades. According to this theory, that’s why Tesla’s stock has run up, why Apple popped after it announced stock splits, and why SPACs like Virgin Galactic (SPCE) and Nikola (NKLA) have seen their shares rise in ways that don’t make sense given the underlying numbers.

Turns out, though, that people had the right crime but the wrong culprit. This is exactly what SoftBank’s 555 Fund has been doing, on the largest names in the world. When it works, it works really well; if you get the timing wrong, you lose it all.

In the Bear Case, this is just the latest example of Masa’s overeagerness to risk it all. Viewed in this light, SoftBank’s selling its most valuable assets to fund risky bets seems negligent at best.

When I was younger and dumber, in 2013, I bought Tesla at $29, Facebook at $19, and Apple at a price I don’t want to think about. The market was booming, and I didn’t want to miss out on maximizing my gains, so I sold those stocks and rolled them into call options. Instead of a portfolio of stocks that would make me look like a genius today, I ended up with $0 on those trades. In selling stakes in Alibaba, T-Mobile, and SoftBank Mobile to bankroll a tech options hedge fund (run, I might add, by a bunch of former credit traders who ran their bank into the ground), SoftBank is doing the same thing on a much bigger budget.

The Bear Case is not that SoftBank loses this 555 Fund money. Assuming they have $8 billion invested and half of it is their money, even if they lose 50%, they’ve lost $2 billion. Not the end of the world.

The Bear Case is that this move signifies a few worrisome things:

Masa has an increasingly big risk appetite. Not content with Vision Fund gains or even price increases in the big public tech stocks, he’s making risky bets for the chance to achieve outsized gains. He may continue to sell off core assets to take on more risk.

Masa wants easier, faster wins. You can’t double $4 billion in a few weeks investing in startups. Options trading is one of the only ways to do it. He’s impatient and getting sloppy.

Masa’s shifting from technology to finance, and Masa kind of sucks at finance. Other than the Alibaba investment, nearly every good thing that SoftBank has done has been when Masa focused on the operating / technology side of the business instead of the finance side.

The question that investors need to ask themselves is: do I want to invest in SoftBank if it’s just a very big alternative asset manager that invests in the same big tech companies I can on my own?

Anyone with a Robinhood account can buy calls on Tesla. Why take on all of the other risk associated with investing in SoftBank to get to the same spot?

If I want to invest in a tech holding company, why not invest in Tencent, which has accumulated a more impressive portfolio, has proven its ability to add value to its investments, and has both a vision and a plan for bringing about and profiting from a tech-powered future?

And if I want to invest in an alternative asset manager, why not invest in Blackstone, which is also publicly traded, has a better track record, and launched its own, more disciplined, tech growth equity fund?

Plus, SoftBank lacks the subtlety to manipulate the markets in secret. Whether in private markets or public, when there’s a big, head-scratching inflation in prices, SoftBank is always standing right there, holding the bag.

So Am I A SoftBank Bull or Bear?

I came into this piece with an axe to grind. I expected to tear SoftBank apart, had the Bear Case written in my head, and was going to leave it at that.

Ultimately, I think that Masa is just an unrelenting optimist. Optimism is an incredibly important characteristic in an entrepreneur. Only an extreme optimist would lose $69 billion, then fly to California with a sketch and a dream, convince Steve Jobs to do a deal on spec, convince a bank to loan him $20 billion, and create a legitimate challenger to Japan’s biggest telecom company.

But naked optimism is a detriment in finance, and even venture investing. It lets you get swept up by people like Adam Neumann, who have more charisma than sense. And it allows you to YOLO trade call options on some of the world’s most heavily traded stocks without covering your downside.

I probably wouldn’t bet on Masa the Investor. There are very few people I’d want to back more than Masa the Entrepreneur.

Whether SoftBank is a good investment or not, to me, comes down to whether it continues to move towards Masa’s finance side, selling operating assets in the pursuit of higher, faster returns, or whether it rolls up its sleeves and starts making its vision come true with more than its checkbook.

I’m staying on the sidelines for now, but I’ll be watching with fascination instead of contempt. And, I never thought I’d say this, but I’ll be rooting for Masa. I hope he can pull this off:

Thanks for listening,

Packy