Welcome to the 826 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 7,579 smart, curious folks by subscribing here!

Already subscribed and want to climb up the Verified Not Boring leaderboard?

Juul: The SPAC 2020 Deserves

SPACs are hot right now. First, in the markets, and then, of course, among business writers. Matt Levine, Alex Danco, Byrne Hobart, Anuj Abrol, and more have written about SPACs recently, and they’ve done a great job explaining what they are.

I’m throwing my hat into the ring, too. This is Not Boring, and the best way to learn about SPACs is by playing Fantasy SPAC on what would be the least boring SPAC to date: Juul.

Party Like It’s 2018

Let’s travel back to December 2018.

Altria, the sterilized, market-friendly name for the Marlboro-maker formerly known as Phillip Morris, has just invested $12.8 billion in three-year-old e-cigarette giant Juul, valuing the company at $38 billion.

The investment makes Juul the third most valuable private startup, right behind two Softbank-backed companies, $72 billion Uber and $47 billion The We Company, and ahead of Elon Musk’s rocket company, SpaceX, at $31.5 billion, and one half of my favorite fantasy merger, Airbnb, at $31 billion.

Big private funding rounds were so common in 2018 that many wondered aloud whether the IPO was dead. The Atlantic wrote about The Death of the IPO, for example, in November 2018. With easy access to large sums of private capital, the argument went, why would companies subject themselves to all of the regulations, disclosures, and headaches associated with going and being public?

Led by Uber, the buzzy startup IPO made a comeback in 2019, as Uber, Lyft, Zoom, Beyond Meat, Slack (technically a direct listing), Pinterest, Peloton, Medallia, Datadog, Crowdstrike, and more offered shares to the public for the first time. But many of 2018’s largest private unicorns are still private. Some are doing better than others.

The Good: In April, Stripe raised $600 million in a round that valued the payments company at $36 billion. SpaceX captivated the world when it launched astronauts into space in late May, and is currently raising money at a $44 billion valuation. Early in July, Palantir filed to go public (confidentially, of course).

The Down Rounds: Softbank owns the majority stake in a trimmed-down, scaled back $8 billion WeWork that’s once again promising it will be profitable next year. Airbnb raised $1 billion in debt from Silver Lake amidst Coronavirus troubles, and the attached warrants valued Airbnb at $18 billion. And what about Juul?

For a brief moment last year, after Uber’s IPO and during WeWork’s failed attempt, Juul was the most valuable private startup in the United States.

Then, on Halloween 2019, Altria wrote down the value of its investment from $12.8 to $8.3 billion. In January, it took another $4.1 billion charge, bringing the value of its stake to $4.2 billion and Juul’s valuation to $12 billion, a 68% fall.

But there’s good news for Juul: if 2018 was the Year of Private Market Froth and 2019 was the Year of the Unicorn IPO, 2020 is the Year of the SPAC. And a SPAC may be the only way for Juul to go public.

A Juul SPACquisition is the most 2020 deal imaginable. I’m not saying it should happen - there’s a non-zero chance that selling Juul stock to retail investors through a SPAC is the thing that finally convinces the Devil to reveal that he/she won a bet with God and has just been fucking with us for the past few years.

But it makes just enough sense to propose a Fantasy SPAC, and a Fantasy SPAC is a great way to learn some fascinating things:

What the hell a SPAC is

What happened to JUUL

How Juul is like Peloton’s evil twin

Why a SPAC should target Juul

Who the ideal Sponsor for a Juul deal would be

The Year of the SPAC… wait, what’s a SPAC?

If you’re reading this newsletter, you’ve probably heard of a SPAC, and you probably kind of understand it but don’t really understand it.

A Special Purpose Acquisition Company (“SPAC”) is a blank-check company that raises money from the public markets and then has a certain amount of time (typically two years) to acquire an actual business.

Here’s how it works:

Well-respected investor, operator, or group of investors and operators (“Sponsors”) announce the SPAC, how much they’re raising, and (sometimes) for what.

i.e. Not Boring Acquisition Corp is selling 100 million shares at $10/share to acquire a majority stake in an unprofitable, high-growth US technology business.

SPAC sells shares to public market investors and trades on public markets, without actually having a real operating business. It has two years to use its “blank check” to acquire a minority or majority stake in a private company.

SPAC finds a target company to buy and makes an offer. Target company accepts.

Deal closes, and the SPAC turns into shares in the acquired company, which then trades on the public market without having to IPO.

Sponsors often get founders shares and warrants to buy the stock cheaply, and make a lot of money.

SPACs have been around since the 1990’s, but recently, SPACs are on fire. According to SeekingAlpha:

So far this year, 48 SPACs have raised $17.1 billion, representing 40% of all dollars raised in the 2020 IPO market. More SPACs have gone public than any other sector, leading healthcare (45 IPOs; $11.1B), technology (14; $4.0B), financials (7; $2.2B), and industrials (6; $4.3B).

As Danco points out, SPACs have three advantages over traditional IPOs that make them well-suited for the kind of uncertain market we’re in today:

Price Certainty. A SPAC looks more like an acquisition than an IPO. Two parties negotiate the price up front, and that’s the price. No long underwriting process.

Speed. The IPO process can take well over a year, which leaves a lot of time for things to go wrong - either at the company, in the markets, or both. WeWork certainly would have benefited from a faster process (although the longer one saved investors).

Brand Halo. Well-respected sponsors can lend their trustworthiness to a company.

SPACs aren’t just good for uncertain markets; they’re good for uncertain businesses, too. SPACs allow companies with an otherwise difficult path to IPO to access public market liquidity as easily as getting acquired.

To whit, the three highest-profile SPACs of 2020 acquired Draftkings, Nikola, and Virgin Galactic. What do those companies do?

Draftkings is a daily fantasy sports, sports betting, and online casino app that faces regulatory uncertainty in terms of which states will legalize online gambling and betting, and at what tax rates. Draftkings is the least risky of the big three because it has customers and makes money.

Nikola is an electric truck company with zero revenue and no product that went public via SPAC and hit a market cap near $30 billion by drafting on retail investors’ love of Tesla.

Virgin Galactic is Richard Branson’s human space tourism company that earned $238,000 in Q1 2020 revenue from “providing engineering services” and hit an $8 billion market cap in February, good for a casual pre-product 8,000x revenue multiple.

Part of the reason that SPACs have been so successful is that the retail investing maniacs on the WallStreetBets subreddit love SPACs. I first invested in Draftkings when it was Diamond Eagle Acquisition Corp, and a friend who frequents the penny stock subreddits told me that it was going to explode when the deal closed and the ticker switched from DEAC to DKNG… and he was right.

These SPACs work in part because of the reasons Danco laid out, and in part because they feed frenzied retail investors exactly what they’re looking for: stocks that are too risky to go public via traditional channels.

SPACs were in the news again last week because famed activist hedge fund manager Bill Ackman just launched the biggest SPAC of all time: the $4 billion Pershing Square Tontine Holdings (PSTH.U). Rumors are swirling that Tontine is eyeing a minority stake in one of 2018’s big private unicorns, like SpaceX or Airbnb.

That got me thinking: what about a company that was valued higher than either of those two in 2018?

What Happened to Juul?

You know Juul. As recently as a few months ago, it was hard to walk down a single block in New York without seeing at least one person puffing a slender black or silver stick and exhaling mango vapors into the air. The product was ubiquitous, attracting hardcore smokers looking for a satisfying way to quit and curious teens looking to look cool. That was a problem. If there’s one thing regulators hate (rightly), it’s companies marketing nicotine or alcohol to kids. Just ask Four Loko.

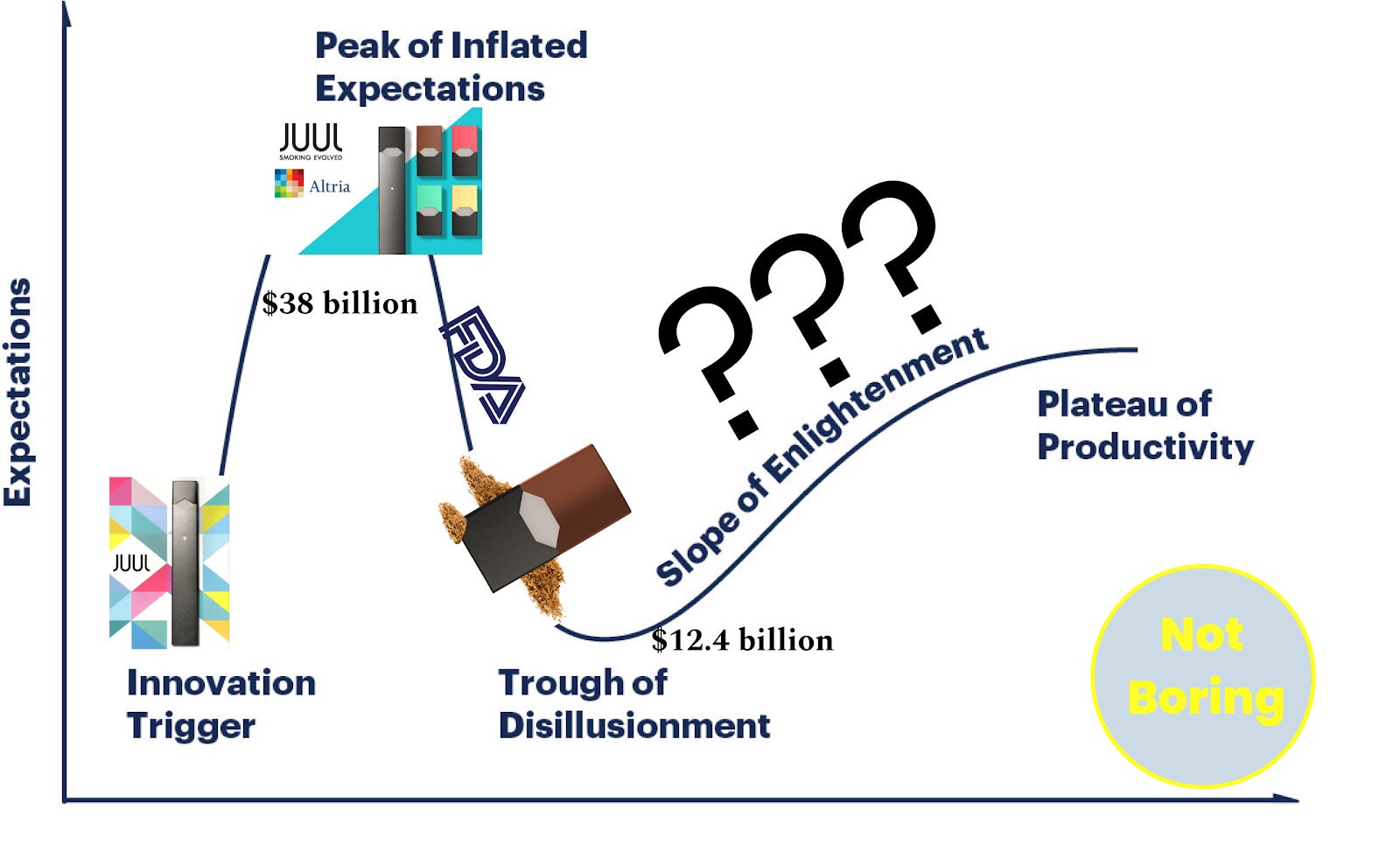

Juul’s arc should be familiar to anyone who’s been reading Not Boring for a little while. It’s the Gartner Hype Cycle.

Launched in 2015 by Pax Labs, Juul sales skyrocketed 700% to over $322 million by 2016. By 2017, the company had already sold 1 million units, and that December, Juul raised $112 million.

Things got choppy in 2018. Early in the year, the FDA began cracking down on the sale of Juul to minors, and in June, San Francisco became the first major US city to ban Juul. Undeterred, the company raised $1.2 billion at a $16 billion valuation in July. In the fall, as Juul passed 70% of the US e-cigarette market, the FDA seized documents from Juul’s headquarters. Juul responded by volunteering to stop selling its sweet and fruity flavors in stores.

Then, amidst all of the regulatory turmoil, Altria stepped in. The cigarette maker, threatened by e-cigarettes’ rising popularity, invested a whopping $12.8 billion in Juul at a $38 billion valuation.

“We have long said that providing adult smokers with superior, satisfying products with the potential to reduce harm is the best way to achieve tobacco harm reduction.”

-- Howard Willard, Altria CEO

Surprisingly, instead of a Nobel Peace Prize for Medicine, Altria won a lifetime supply of headaches. In 2019, the FDA, Senate, House of Representatives, and US Attorney’s Office were all investigating Juul. Then China halted Juul sales and India banned vaping, cutting off the two biggest smoking markets in the world. Juul halted the sale of sweet and fruity pods online, and laid off 500 people.

After all of that, Altria’s Halloween 2019 writedown of its Juul investment, from $12.8 billion to $8.3 billion, came as no surprise. Nor did its January announcement, one quarter later, that it was writing down the investment by another $4.1 billion, to $4.2 billion. Juul and Altria also modified their original agreement - instead of providing marketing and distribution to Juul, Altria will be providing legal and regulatory support.

In the four weeks ended January 25th, the company’s in-store sales fell 25% compared with the same period a year earlier, according to Nielsen.

And all of that before Coronavirus - a respiratory disease from which smokers are more likely to die than non-smokers and against which the best defense is to not exhale our germs onto each other. Try Juuling through a mask.

Things look bleak, but remember this arc from Oh Snap!? Juul has gone through the first half of the Gartner Hype Cycle.

Sometimes companies recover and emerge from the Trough of Disillusionment. Snap has. Other times, though, they drop all the way to oblivion. Sometimes, the product was a fad, a Meme Startup without a second act.

Juul doesn’t suffer from poor product-market fit, though. If anything, customers love it so much that the government feels it needs to step in to protect them from themselves.

Peloton’s Evil Twin

One of the past year’s most successful IPOs, Peloton is almost as addictive as Juul, but regulators aren’t trying to stop it. Peloton makes its customers healthier, using high-energy classes, star instructors, and good old fashioned competition to keep customers working out.

Peloton’s magic is that it sells customers expensive hardware upfront, and then sells them a monthly subscription to fitness content. The bike costs $2,245 and the All-Access Membership, obligatory for the first year, costs $39/month. It’s high AOV hardware plus software subscription. Once someone has invested in the bike, they’re not going to cheap out on the $39 subscription.

Juul is Peloton’s evil business model twin.

I remember talking to a friend at a hedge fund about Juul a couple of years ago. His fund purchased aggregated credit card data to inform trading decisions, and he told me he’d never seen anything like Juul. People bought Juul pods so consistently and often that the company behaved like a subscription business with low-to-negative churn.

Here’s how Juul’s business model works:

Pay $50 for a Juul device.

Pay $20 for Juul pods, the little plastic things that hold the nicotine juice.

Pay $20 for Juul pods

Pay $20 for Juul pods

Pay $20 for Juul pods

Pay $20 for Juul pods

…. forever

Pay $20 for Juul pods.

Juul, too, sells more expensive hardware upfront and then essentially generates sticky subscription revenue for years and years. Despite the fact that a Juul costs just 2% of what a Peloton bike does, Juul customers can actually end up spending more than Peloton customers over five years.

How sticky are Juul customers? The company found out when it tried to appease regulators by pulling its sweet and fruity flavors, including its most popular, mango, from US shelves. Retailers got creative and started importing mango pods from Canada. Customers who were used to paying $20 for a four-pack of Juul pods happily paid $30 - $50 for the North of the Border Mangoes. Juul pods had almost no price elasticity of demand - because they’re addictive, customers are willing to pay almost anything to get them.

That’s the type of sticky cashflow that investors love to buy, and why smart investors like Tiger Global poured so much money into the company despite regulatory and moral risks. A company like that will survive until the government shuts it down, and the product, in one form or another, will survive even that.

Juul’s business model is solid, its problem is regulation. It did an evil thing by marketing its product to teens, and it needs to make amends. The company needs to work with regulators, continue expansion into friendlier markets, and wait for the US, Chinese, and Indian governments to come around to its arguments that e-cigarettes are safer than cigarettes, and that Juul’s products are safer than competitors’ knock-offs. To do that, it needs cash.

In February, the Wall Street Journal reported that Juul had raised $700 million in debt, to keep it afloat and allow it to make long-term decisions. (Wait, what about the $12.8 billion it raised from Altria? It paid $2 billion in employee bonuses and returned all but $1 billion of the rest of the money to investors. Whoops!)

Debt is certainly one way to fund a company with a ravenously loyal customer base that would inevitably face too much scrutiny, including around its recent slowing performance, to go public via a traditional IPO.

But it’s 2020, and debt is nowhere near wacky enough.

A SPAC Should Acquire Juul

Juul is a high-risk target. There’s a real chance that the company isn’t around in two years. But that risk is why a SPAC’s Sponsor and Investors might get the deal of the century, and why a SPAC is the only way to take Juul public. A deal stands to benefit all of the parties involved: the Sponsor, Juul, Altria, and the Investors.

The Sponsor

In Juul, the Sponsor has an opportunity to acquire a large stake in what was recently the most valuable private company in the United States at a deep discount, and take it public with almost no downside. SPAC Sponsors (Ackman is a notable exception) typically receive founder’s shares worth 20% of the acquisition amount for a nominal fee (like $0.05 to buy a $10 share). The Sponsor, and public market investors, also receive warrants, which allow the holder to purchase more shares by a future date at a specified price. For setting everything up and attracting capital, the Sponsor receives a piece of the company (the 20% founders’ shares) that makes them money even if the deal goes poorly, and warrants that pay off if things go well.

The Sponsor will be negotiating with Juul from a position of strength. Juul’s valuation has plummeted by more than two-thirds in under a year, it is battling regulators and angry parents, its reputation is deeply tarnished, and it has no other means of accessing public markets.

That means that a Sponsor could end up with founders’ shares and warrants in one of the stickiest, fastest-growing businesses in history for less than a third of what it would have cost them a year ago. It’s too tempting not to try.

Juul

It would be really hard to take Juul public via traditional IPO, but the company will continue to need cash as it fights regulatory battles and works towards getting its products on more shelves. Going public would give Juul access to bigger pools of capital. A SPAC might be the only way to do it, and investors have never been hungrier for a deal like a Juul SPAC.

Juul is at a regulatory low point that makes the company hairy and uncertain. The company is being made an example of while more harmful cigarettes and less popular e-cigarette products roam free on bodega shelves. There is strong demand for the product, though, and it is likely healthier than cigarettes, so there is a compromise to be made with regulators in the coming years.

Through a SPAC, Juul would just need to find one Sponsor who sees the business’ potential versus needing to convince a series of institutional investors in a traditional IPO roadshow. Once Juul and the Sponsor strike a deal, the company will have a powerful ally in its battle with regulators and its campaign to convince the public that it does more good than harm.

Altria

After two consecutive writedowns, Altria seems like it would be more than happy to get out of its shares. Currently, Altria is not allowed to sell. As part of Altria’s investment in Juul, the two sides agreed to a “standstill agreement” which says that Altria can neither buy more of Juul or sell its shares for six years. Juul should be able to let Altria out of the agreement, though, if it does a SPAC deal, and I can only imagine that Altria would be OK getting out of a portion of its shares for the right price.

Investors

Now is the perfect time to take Juul public. The WallStreetBets crowd and Robinhood traders are bidding up shares of SPACs and anything with a good meme attached to it. Juuling is a meme among the same type of people who frequent WSB, and I think a stock trading under the JUUL ticker would go crazy.

More than the frenzy, though, investors would get the opportunity to buy an incredibly sticky business at a deeply discounted price. Juul makes a product that people love, and repurchase over and over again. If it can get past regulatory hurdles (a big if), it has a model similar to Peloton’s, which public market investors, who don’t need to tie their name to a company as publicly as private market investors do, will love.

Of course, this deal is risky! Regulators are coming after Juul hard, the company is hated by parents, educators, and many others who believe that it is ethically bankrupt, and the time and money it spends fighting legal battles is time that competitors have to catch up or pass them. Normally, I’d view this risk as a bad thing, but in this market, investors seem to love risk for its own sake. With a SPAC, they’re doubly rewarded for taking the risk in the form of the warrants that SPAC investors receive. For example, the warrant might allow them to buy more shares for $10 in the future, even if the price rises to $30.

Taken together, this means a SPAC might be able to acquire Juul cheaply, sell shares to a market that has never been more friendly to meme stocks, and retain upside in the form of warrants and cheap founder shares if Juul is able to regain the momentum that made it the most valuable private startup in the world for a brief moment last year.

So which Sponsor is crazy enough to acquire Juul?

I have some thoughts, which I dropped in the comments, and I’d love to hear yours. Join the conversation:

Unfortunately, I don’t think the Devil is going to let 2020 end until someone steps up and makes this deal happen. Luckily for whoever is crazy enough to try, Juul represents an opportunity that is tailor made for 2020 SPAC-ing. It’s definitely not normal, and it might not even be moral, but if Juul can get past regulatory concerns, there’s actually a great business hiding under all of the red tape. A SPAC offers enough upside to the Sponsor that someone should step up and try. If there was ever a time for this, it’s now.

The WallStreetBets crowd is going to go mangoes for this one.

Thanks for listening,

Packy