Is That a Family Office in Your Pocket?

Or are you just a happy Equi client?

Welcome to the 1,067 newly Not Boring people who have joined us since Monday! Join 65,504 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts

This week’s Not Boring, the whole thing, is brought to you by… Equi

Equi puts a Family Office into the pocket of regular accredited investors. Read on to learn more. You can apply to be one of Equi’s 300 beta investors here:

Hi friends 👋 ,

Happy Thursday!

Today’s post is a kind that I’m writing more frequently on Thursdays: the Investment Memo x Sponsored Deep Dive crossover.

I only write Sponsored Deep Dives about companies I’d want to invest in — the whole point is to expose you to some of the most exciting and innovative startups out there before anyone else does — and now that Not Boring Capital exists, I put my money where my mouth is whenever possible. You can read about how I select Sponsored Deep Dive subjects here, and increasingly, I plan to write them about portfolio cos.

After learning more about Equi by writing this, I’ll be investing in the company, too.

Speaking of portfolio companies… I’m launching the Not Boring Jobs Board, right here, right now. The board will feature open roles at Not Boring portfolio companies, and some other roles at fast-growing startups I think would be great places to work.

To kick it off meta: I’m running the board on Pallet, a Not Boring portfolio company that’s getting an absurd amount of early traction, and my first featured role is… a Full-Stack Engineering role at Pallet itself. Calling it now: this will be a unicorn. And speaking of unicorns, Not Boring fav Ramp is hiring a Principal Product Designer.

To apply, or to find yourself another Not Boring Job, go check out my Pallet.

That leaves one challenge: what to do with the beaucoup bucks you make in your new dream job? Equi might be able to help…

Note: This is not investment advice and is for informational and entertainment purposes only.

Let’s get to it.

Is That a Family Office In Your Pocket?

I am but a humble newsletter writer. I don’t have the power to command the stars. But my god have they aligned perfectly for this piece.

When I first talked to Tory Reiss back in December, he was in the early stages of starting a new company. Since then, he and the company’s all-star team of co-founders raised a little money, went into the lab, and built. In June, he reached back out to tell me that it was almost ready, and asked if I could help explain what they’re doing. I said yes. We picked a date: July 29th. (That’s today.)

We had no way of knowing then that today was going to be Robinhood’s first day of trading as a public company.

Nor did we know that Titan was going to announce a $58M a16z-led Series B valuing the company at a $450M valuation last week.

And even with all of the world’s crystal balls at our disposal we could never have guessed that a tweet about capital allocators, of all things, was going to take Twitter by storm.

Those three events are relevant because Equi is a bit of the combination of the three, with a little extra sauce on top.

Like Robinhood, Equi is making it easier to access the financial markets.

Like Titan, Equi is essentially a hedge fund in the back with a tech interface in the front.

Like that poor capital allocator everyone dunked on, a large part of Equi’s strategy is identifying and investing with the world’s best fund managers.

Equi takes pieces from all three, and combines them into something novel: a tech-powered family office in your pocket.

(Note: when I use the term Equi throughout the piece, I’m referring to both Equi’s investment advisor and Equi’s tech platform, which are two separate entities with different functions, but y’all don’t want to read the version that calls them different things throughout, so just know it.)

Here’s the thing. The way that institutional investors and Ultra-High Net Worth individuals (UHNW or the .000001%) invest is very different from the way you or I invest, even if “you” are a High Net Worth (HNW or the 1%) individual. And it’s certainly not because the institutions don’t have the ability to invest the way that retail investors do… they have a broader universe of options available to them than we do, and they mix and match those options into portfolios with better risk-adjusted returns.

The biggest difference between how they invest and how we invest? Alternative investments. Institutions and UHNW individuals, who often invest out of their own family offices, have on average roughly 50% of their portfolios in alternative investments like hedge funds, private credit, volatility, private real estate, crypto-backed lending, and more. Even HNW investors have closer to 6% on average in alternatives.

That creates an enormous disparity in returns over the long-term. The average HNW investor has generated annualized returns of 2.5-5.4% over the past 20 years. The average UHNW investor has averaged 8.8-12.4% returns over the same period. That’s because diversifying with alternatives can increase returns and decrease volatility in a portfolio, which makes a big impact on how a portfolio grows. Throw compounding into the mix and the difference is enormous. After 20 years, $100k invested becomes $217k for the HNW investor, and $750k for the UHNW investor! The gap widens practically on its own.

But before you get too envious, here’s another thing to know: a lot of the institutions aren’t actually great at allocating…

They have access to alternative investments, but their process is often incredibly manual. They know a guy who knows a guy who runs a fund. References check out. Performance has been pretty good. If, per the tweet, MIT only allocates to the top 5%, they’re ahead of the curve. Definitionally, some institutions are allocating to the bottom 95%. Even most of the institutions allocating to the top 5% aren’t quantitatively structuring a portfolio of non-correlated managers. A small handful of alt-focused Fund of Funds do this, but they're nearly impossible to access and manage the money of a few ultra-rich clients.

Equi’s value proposition is simple: it’s taking the best of the family office model, improving it by making data-driven investment decisions, and offering it to the (HNW, for now) people. Equi combines tech with smart humans to build the modern family office, like if Betterment and a top-tier quant alt-focused fund of funds had a baby.

Although this is a Sponsored Deep Dive, it’s not meant to sell you on Equi specifically. For now, for regulatory and administrative reasons, the company’s investment arm can only let in 300 accredited investors, and their average investor is investing over $1.2m on the platform (although if that sounds like something you might be interested in, you can apply here, fill in Not Boring as the referral source, and I’ll badger the team to let you in). For perspective, to mimic a portfolio like the one they’ve assembled you would actually need well over $90M. Long term they aim to drive minimums lower so these investments become accessible to everyone.

When I asked Equi’s co-founders their dream outcome for the piece, no one said “more customers.” Their answers were consistent:

Tory Reiss (CEO): “I want to de-complexify the layers of what we’re doing and make the concepts more digestible to people beyond our co-founders. Finance does a good job of making things overly complex when they’re not. There’s a lot of great work being done to help people at the bottom of the financial ladder, and our educational content and philanthropic work will target that demographic as well, but what we’re building can help prevent the hollowing out of the middle class.”

Jeremy Smith (CRO): “If we get to the person in each friend group who all the friends go to for finance advice and up-level their knowledge on alternative investing, that’s a win.”

Itay Vinik (CIO): “Accredited investors are 1 in 10 households in America, and they don’t think they have options, because they typically don’t. I want them to understand why family office-style investing makes sense for them.”

So this piece will be about Equi, of course, but it’s also about a topic about which I’ve been banging the drum for nearly as long as I’ve been writing this newsletter: diversification across uncorrelated assets creates better risk-adjusted returns.

Whether or not you invest through the Equi platform, you should be thinking about adding uncorrelated assets to your portfolio. In a bull market, YOLO trading on Robinhood has worked stunningly well. To deliver returns that compound over decades, you may need a slightly more sophisticated approach.

Today, we’ll cover that and more:

Re-Building a Modern Portfolio

Meet Equi

How Equi Invests

Democratizing Access to the Private Markets

A lot of what makes Equi tick under the hood is complex. I couldn’t build the portfolio that Equi offers. But the ideas it’s based on are pretty straightforward. It starts with understanding why the traditional portfolio structure no longer works.

Re-Building a Modern Portfolio

Quick: what’s the best way to structure your investment portfolio?

For the past few decades, the answer has been easy: the 60/40 portfolio. Put 60% in equities, 40% in bonds and call it a day.

That approach is easy to understand. 60% of your money should appreciate and grow, and 40% should generate income. Buy some index funds, buy some treasuries, call it a day. It’s also, unfortunately, the wrong approach today.

Why? There are a few reasons.

Interest rates are super low.

There’s alpha in the private markets if you pick the right managers and strategies.

It’s easier than ever to access alternatives to build a non-correlated portfolio.

Let’s take each in turn.

Interest Rates are Historically Low

If you’ve been reading Not Boring, or watching the markets, or even turned on the news at some point over the past year, this one should not come as a surprise to you. Interest rates are historically low, which has driven up the price of growth assets and forced investors to look for returns in riskier assets.

For most of recent history, investing in Treasuries was essentially free money. On the day I was born in 1987, the 10 Year Treasury yield, referred to as the “risk-free” rate because of the infinitesimally small chance that the US defaults on its debts, was 7.17%. Inflation that year averaged 4.43%. That meant that you could invest, with practically no risk, and have money with 2.74% more buying power the next year.

Take a look at the historical chart of 10 Year Treasury yields versus inflation. Any time the blue line was higher than the red line, you could park your money in bonds and outpace inflation. It wasn’t sexy, and you weren’t going to outperform anyone by doing it, but money’s money.

Since the Financial Crisis in 2009, that’s mostly flipped. Today, the risk-free rate is at 1.29% while inflation is at 4.31% (based on the Consumer Price Index, whether that’s accurately capturing real inflation is for another conversation). That means that if you invest in 10 Year Treasuries, your money buys 3% less every year.

Oaktree’s Howard Marks wrote an excellent memo on this topic back in October titled Coming Into Focus. If you want to go deep, you should read the whole thing. The takeaway is that lower interest rates have a dramatic impact on every part of the market. When the risk-free rate is lower, returns on all other asset classes come down, too.

To generate the same returns you were used to at a higher risk-free rate, you need to take on more risk. This is one of the reasons so much money has flowed into growth equities and venture capital since the Fed lowered rates in response to COVID.

Long story short, bonds should not be 40% of your portfolio unless you have a strong thesis for why they should be.

There’s alpha in the private markets if you pick the right managers and strategies.

The difference between the 25th and 75th percentile managers in funds focused on traditional, publicly available assets like US Fixed Income or US Large Cap Equities is tiny. You’re probably better off avoiding paying the fees and just buying an index.

BUT, and this is one of the tropes that Tory wants to kill, that doesn’t mean that all hedge funds underperform the market after they take their fees. That’s become a popular narrative, and when you look at it in the aggregate, it looks true, but there is a huge variance in performance between top and bottom managers in private, alternative asset classes like Venture Capital, Real Estate, Growth Equity, Private Equity, Private Credit, and more.

That means that you should be able to generate above-average risk-adjusted returns if you can pick, and allocate to, the best managers across a diversified portfolio of non-correlated strategies.

It’s Easier Than Ever to Access Alternatives and Build a Non-Correlated Portfolio

All of this makes sense on paper. The challenge is, until very recently, it was exceedingly difficult for a regular person to even access alternative investments. Top performing funds require minimum investments of $1 million or more, and often much higher, and that’s just for one fund. If you wanted to diversify across strategies, that would run you into the tens of millions of dollars.

That’s changed. As I wrote about in Software is Eating the Markets, new platforms give (mostly accredited) investors access to alternative investments. Platforms like Fundrise and Cadre let regular people invest in real estate projects, Masterworks lets us invest in world-class art, Rally and Alt give people access to fractions of rare collectibles like The Declaration of Independence. Titan is a mutual fund for a new generation, like a long-only hedge fund behind a tech-first interface and portfolio-related educational content.

Regular people can also invest in startups much more easily than we could in the past, both directly and via funds, driven by companies like AngelList, Republic (portfolio company), Syndicate (portfolio company), and Party Round (portfolio company). (Do you see a theme?)

AltoIRA will even let you invest in most of these platforms with your self-directed IRA.

All to say, not only does 60% equities / 40% bonds no longer make sense, we no longer need to settle for the mix. There are better … alternatives.

That doesn’t mean that a balanced portfolio no longer makes sense. Quite the contrary.

60/40 or 50/50 or some permutation based on your own goals certainly makes sense. This is not a call for you to ape into the riskiest stuff you can find. The trick is figuring out what goes into the 60% appreciation bucket and what goes into the 40% income bucket.

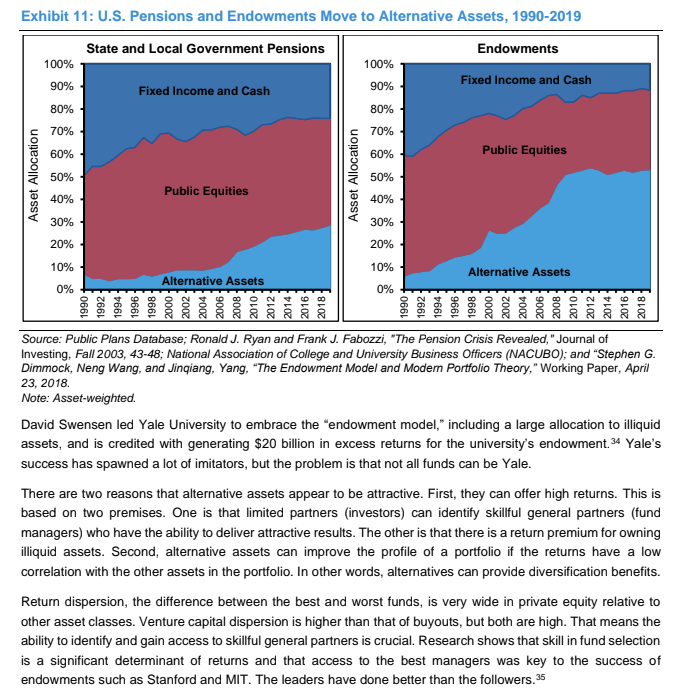

A good guidepost is how people allocate when it’s their job to do so, and they have access to the entire universe of potential options. In an August 2020 report for Morgan Stanley titled Public to Private Equity in the United States, Michael Mauboussin highlighted the shift in the way that government pensions and university endowments allocate their money over the past three decades.

Since 1990, both government pensions and university endowments have moved away from something like the traditional 60/40 portfolio to include a much higher allocation to alternative investments. University endowments, which can be more nimble, have moved to 50% alternative assets and stayed there for the past decade. That makes sense. The late David Swensen created the “endowment model,” which shifted endowment portfolios more heavily into illiquid private investments, while running the Yale endowment.

Mauboussin cited two main reasons that alternatives are attractive:

High Returns. As KKR highlighted, the best managers can offer above-market returns, plus there’s a premium for holding illiquid assets.

Diversification. Alternatives can provide diversification benefits if they offer low correlation to other assets in the portfolio, i.e. if a credit fund’s performance has little to nothing to do with how the S&P 500 is performing.

That last point is incredibly important, and one that I’ve highlighted a few times in Not Boring. In fact, I’ll just re-write what I wrote in my piece on Fundrise.

Today, retail investors have access to a larger universe of options than we did before, and investing in uncorrelated assets creates better risk-adjusted returns than investing only in stocks.

In his seminal paper on the topic, “Engineering Targeted Risks and Returns,” Bridgewater CEO Ray Dalio wrote about his hedge fund’s Post-Modern Portfolio Theory approach, an evolution of the Yale Endowment’s Modern Portfolio Theory. He describes different approaches to get to a target 10% annual return. In the traditional approach, an investor needs to put most of his or her portfolio in equities, which typically generate higher returns than cash, bonds, or real estate, but at a higher level of risk. Being so heavily concentrated in one, high-risk asset class is a riskier way to generate returns than he’s comfortable with, so he recommends another approach, that boils down to a few ideas:

You can generate a similar risk/return profile to equities by using leverage in other asset classes.

Diversification into uncorrelated assets -- both of asset classes (beta) and the managers who invest in those asset classes (alpha) -- produces better risk-adjusted returns than high concentration.

By leveraging non-equity asset classes to the same risk/return level and diversifying across more uncorrelated asset classes and managers, you can hit your 10% target with lower risk.

For our purposes, the specifics are less important than understanding this key concept: allocating money across a diversified portfolio has historically generated better risk-adjusted returns than concentrating in just stocks, bonds, or even the traditional 60/40 split.

I’m the last person who would ever say that you should 100% optimize your portfolio for long-term returns. In Software is Eating the Markets, I wrote that retail investors are buying a lot more than just returns when they invest.

By all means, buy Tesla because you love Elon’s mission and think he’ll continue to prove the shorts wrong. What’s the point of any of this if it’s not fun?

But professional investors are increasingly shifting their allocation mix to alternatives, and you should have the opportunity to do the same with a portion of your portfolio. Until recently, though, building a portfolio like a top-end family office would have been out of reach for even accredited investors. That’s why Equi was born.

Meet Equi

Many of the best companies are created because their founders had a problem, couldn’t find a solution, and had to build it themselves. Equi was born out of its founders’ champagne problem…

All four of Equi’s co-founders have done really well for themselves.

Tory launched the first USD-backed stablecoin, TrueUSD, an AI-enabled debt refinancing platform, and was on the founding team at Lob.

Jeremy co-founded SpotHero, led BD at Zeus, and sold another venture to Coinbase.

Itay advised UHNW clients at UBS and at his own advisory shop, and ran a quant hedge fund from which he cashed out after making the trade of a lifetime during Volmageddon in 2018.

Romil Verma was a well-compensated FAAMG engineer at Facebook and Google, and also co-founded two companies of his own.

This isn’t the story of some scrappy founders eating Ramen in their parents’ basement. It’s about four guys who, in their 30s, were already rich, and wanted to not only safely grow their own portfolios but help others do the same. They were also knowledgeable; they knew how they should be investing. Itay worked with UHNW clients every day and ran his own hedge fund. Tory has been running financial literacy classes for eight years. Jeremy had been investing in private real estate as a cross between a hobby and a profession for years.

The problem was, they didn’t have access to those investments because, individually, they weren’t appealing enough for an interesting manager to care, let alone plop down the $1-5 million required per fund, across enough non-correlated funds to build the portfolio they wanted.

So last year, they started talking about how to build the ideal alternative portfolio. Itay figured out what to do on the fund-of-funds side, Jeremy figured out a value-add real estate strategy that could create both appreciation and income, and Tory figured out how to structure a tech platform that could scale. They started running the models, and they realized that it would be possible to generate above-market returns at below-market risk. The easy path would have been to just start a fund of funds, or a hedge fund, and take institutional money to run the strategy for themselves.

But they also realized that they wanted to build something big, that would help a lot more people invest like the best. So they’re working on the legal and regulatory work, setting up as a Registered Investment Advisor (RIA), and working with lawyers to figure out a novel FoF structure that would allow them to scale to thousands of accredited investors (with hopes to scale far beyond that eventually). Serving this many customers would be impossible for a traditional fund, but for a technology company, it’s a cake-walk.

Although it was born out of a champagne problem, the Equi co-founders built the product to solve a very real problem: the hollowing out of the American middle class.

“We all come from humble middle class upbringings from across the world,” Jeremy told me. “It’s hard to see that we’ve been able to get to the next level but that those opportunities aren’t the same for the next generation.”

While the initial version of the product seems like it serves a champagne need, it’s actually directed at another group of people who are worth millions but don’t have great options: retiring Americans who have spent their entire careers saving, but find themselves holding portfolios that are predominantly in bonds in order to generate retirement income. That means they’re losing buying power right when they stop earning an income.

For sure, Equi has billionaires on the platform -- three, to be exact -- but it also serves Itay’s aunt and Tory’s mom, who worked in the public school system for 30 years and had half her portfolio in muni bonds earning 1.6%. The fact that Equi can serve both billionaires and Tory’s mom with the same product is a pretty unique thing.

It all comes back to Equi’s mission: to create generational wealth for as many people as possible. They realized that doing so would require a combination of tech and humans. Romil joined to build out the tech side, both the back-end tools to make and manage investments and investors, and the front-end application that will give people a “family office in their pocket.”

Equi isn’t claiming to have developed something totally novel. There are leading FoFs who employ similar strategies. What makes Equi special is that they’re opening up access to this type of investing to non-UHNW investors and educating even non-clients on better ways to invest their money.

Which begs the question: how does Equi invest?

How Equi Invests

“You need to talk to Itay, he’s a genius.” I heard that same phrase from both Tory and Jeremy when I spoke to them.

I talked to Itay. He’s as good as advertised.

He started off our conversation with two hindsight-obvious but important observations:

Every investment in the world relies on either appreciation or income (real estate is a hybrid, it has both).

In the 21st century, allocators still don’t use data to source the best alternative managers.

To Itay and the Equi team, there’s nothing wrong with a 60/40 split; the magic is in what makes up the 60 and what makes up the 40. It’s about investing in a diversified, non-correlated portfolio of assets and fund managers to push out the efficient frontier. That, in turn, is about which strategies make up the appreciation portfolio and which make up the income portfolio, and as importantly, who’s running those strategies.

Which brings me to the second thing Itay pointed out, which I hinted at before: the way that institutions and family offices source the managers in whom they invest is still pretty manual. When he started researching how to build the portfolio for Equi, Itay sought out every CIO he could talk to, and he came away unimpressed.

“The way that 95% of the CIOs I spoke to diligence managers is primarily a relationship game,” he told me. “Either they get introduced by their prime broker, or someone they know at another endowment said they were good, then they have lunch, get along, double-check the track record, and invest.”

That’s fucking crazy, because as KKR, Mauboussin, and Marks all pointed out, manager selection is the alpha in the private markets.You generate outsized returns by picking the right people to back.

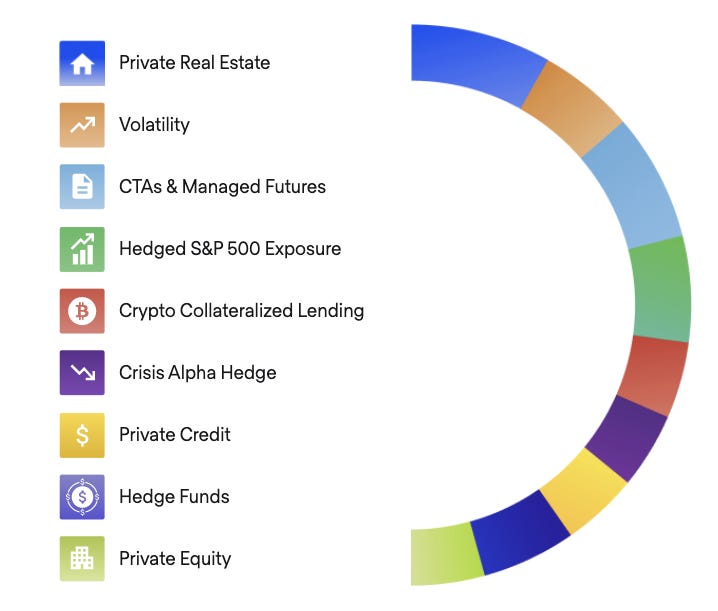

The way Equi does that is to divide managers up into asset classes, find the best-in-class in each category, and then build a portfolio of managers that are uncorrelated to each other and the broader market.

To replace the 40% fixed income piece of the traditional portfolio, they look at managers in categories like private credit (and actually build out their own value-add real estate and crypto-backed lending funds in-house).

Itay is responsible for replacing the 60% equities piece in the traditional portfolio. To do that, he looks for managers doing managed futures, volatility, and a dozen other hedge fund strategies. To cover their ass in case everything explodes, they look for crisis alpha managers, people like Michael Burry from The Big Short who buy deeply out of the money puts, or cheap insurance policies, that pay off extremely well when things occasionally fall apart.

To identify those managers, Itay has a “database of databases.” Since none of the existing providers were comprehensive enough, the Equi team pulls data from over eight different databases, including their own proprietary data. This gives Itay a list of over 10,000 funds across the world and as much performance data as he can scrape together on them. He filters that list for a few things, including:

A track record over 100 months long to prove staying power.

Assets Under Management (AUM) between $200M and $500M because he’s found that larger funds than that don’t perform as well, and smaller ones have a higher likelihood of going out of business.

Other measures of return per unit of risk, so they can minimize the risk included in any area of the portfolio.

By taking the data-driven approach, Itay can find incredible managers most allocators have never even heard of. As he put it, “There are a lot of nerds out there who just aren’t good at raising money clipping 20% per year.” One of the best funds in the world by returns asked Itay how he even found him. No one else had come knocking.

To test the power of the database, I asked Itay to show me the fund with the best Sharpe Ratio (used to measure risk-adjusted return) in the world. He showed me the numbers in his dashboard, and then told me the backstory from memory. (FYI: It’s a tiny fund in a tiny European country with an unheard of Sharpe Ratio of 5.83 (!!!) that generates 18% annual returns with 3% volatility. Equi couldn’t get in because the strategy only works up to $100M.)

So Itay identified top managers across different asset classes and strategies using their database of databases. He found twelve that balanced each other perfectly. Just like you or I might try to build a portfolio of uncorrelated assets -- stocks or bonds or startups or pieces of art -- he can build a portfolio of uncorrelated managers, each of whom have their own portfolios:

Some funds might have higher expected returns and higher expected volatility.

Some might have lower expected returns and lower volatility.

One, the crisis alpha fund, had both lower expected returns and higher volatility than the S&P 500. It stood out like a sore thumb on the chart, and Itay explained that it was there to hedge the entire portfolio against catastrophic downside risks.

Then, he went into sell mode. Most of the best-performing funds don’t need to actively market themselves or even take new money. For one fund, a Danish mortgage arb fund with a stellar track record, it took Itay five months of cold-calling and emailing to get a meeting. The fund manager told him they were closed to outside investment. Itay somehow convinced him to let Equi invest $100 million.

Plus, somehow, Equi has been able to negotiate lower fees with these funds, who like the idea of giving the benefits of their strategies to more people while only having to deal with one investor on the cap table.

The end result is that they have come up with a strategy that should push out the efficient frontier. If you were an econ or finance major, this concept should be familiar. The efficient frontier is the set of portfolios that provide the best returns for a defined level of risk, or the lowest risk for an expected return. The goal is to get the highest expected return for the lowest risk. He did a pretty damn good job.

Itay has constructed a set of portfolios that gives him a targeted return of 17% with less than 4% volatility and a low correlation of 0.16 with the S&P 500. That’s world-class. Equally importantly, low volatility means a lower likelihood of blowing up, no matter what the market conditions. It also means a much smoother compounding of an investment portfolio. Itay showed me a stress test he ran over the worst market environments since 2008, and the max drawdown was tiny.

In the worst periods of the past thirteen years, when the S&P 500 lost as much as 16.9%, the most Equi’s strategies would have lost was 0.31% according to these hypothetical projections. It only lost money once in the ten periods tested. Again, backtests are not perfect predictors of the future, they don’t account for future market risk or fully capture fees and transaction costs, but it demonstrates the power of a diversified, non-correlated strategy in protecting the downside and powering compounding.

Here’s another thing that sounds obvious, but isn’t. Avoiding losses is key to compounding. If you lose 50% of your money at some point, that stops compounding in its tracks. A 50% loss means that you need to double your money to get back to where you were and start compounding again. After the Great Crash of 1929, it took the market until 1954 to get back to its pre-crash levels.

Compounding is the name of the game for Equi. Based on their projections (understanding that past performance is not a guarantee of future results), the portfolio Itay and team have constructed (green and light green lines) would have dramatically outperformed the S&P 500 and a BarclayHedge Fixed Income Index. The difference between the two green Equi lines is that one is equally-weighted (one-twelfth allocation to each fund) while the other balances them based on Itay’s efficient frontier weightings. That weighting caused ~100 bps of outperformance and speaks to the importance of not just picking the right managers, but constructing an optimally-weighted portfolio of managers.

This is complex stuff and it is just a hypothetical illustration. Most institutional investors can’t or don’t do it. But it’s worth it, and gets more worth it over time. The Equi investment team’s strategy has crushed the indices, and that recent uptick isn’t due to much better recent performance; it’s just what a chart looks like when things keep compounding. It’s exponential.

Meanwhile, the Equi team realized that some things are better done in-house. For example, as part of the strategy that replaces the ~40% income piece, Jeremy leads an in-house real estate team. They go out in the field, backed by data, to identify and purchase multi-family properties (that’s what the real estate world calls apartment buildings). They run a value-add strategy, which means that they’ll buy assets that need work, hire contractors to renovate, and then rent out the units at a higher price than they could have before the work.

Multi-family real estate is an important piece of a portfolio for a few reasons:

Tax-Efficient. The tax code allows for depreciation and cost segregation which means the cash flows investors receive are heavily tax-advantaged.

Able to Get Leverage. A robust lending industry means that Equi can lever up its equity to purchase investments, like you would when buying a home while keeping a safe enough monthly cash flow to amply cover their loan.

Can Run Value-Add Strategies. By doing heavy renovation and repositioning, value-add investors can often generate outsized returns on both the income and appreciation sides.

Inflation Hedge. I had never thought of it this way, but Jeremy made a really good point when we spoke: because leases roll over every 12 months, multifamily rental income is a great inflation hedge. If inflation rises dramatically and wages rise, landlords can increase rents annually to reflect the new reality.

On the income side, Equi also plans to manage private credit investments and a market neutral digital assets fund.

Private Credit. Thanks to Dodd-Frank, banks have restrictions on who they can and can’t lend to. They might not be able to give inventory loans or motorcycle loans, or to factor accounts receivable. The banking system was made for a world in which everyone is a 9-5 W2 worker, which is becoming less true by the day, providing endless opportunities for alternative lenders who are willing to give loans to, say, a self-employed newsletter writer like me.

Market neutral digital asset fund. Equi recently brought on Uddhav Marwaha, a former BP energy trader who has spent a lot of time in DeFi, to build its market neutral digital asset fund. To see Uddhav in action, watch him talk DeFi (minute ~17) at Equi’s May Financial Market Analysis session. The Equi team wrote that Uddhav, “Agrees that the market neutral arbs available in Defi today are some of the most attractive in the world.” This strategy is similar to the ones that I wrote about in the piece on BlockFi.

Jeremy and his team have their sights set on any asset that produces good cash flows. Private equity, which buys boring, cash flowing businesses, seems like a natural extension.

The last piece of the Equi puzzle is the app, which is launching in the coming weeks. In the beta, investors will be able to set their allocations across Equi’s three strategies: Balanced, Growth, and Income oriented. Balanced and Income are designed to generate more income for holders, Growth is focused on appreciation. Real Estate is a separate fund because (for now), it has a longer lockup period due to the illiquidity of the investments. Even among the diversified, non-correlated strategies, investors will be able to diversify by investing in a combination based on their needs and goals.

The end result is that, for hundreds of thousands of dollars, investors will be able to access a portfolio that has previously been available to only those with $100M or more in the bank. In future versions of the app, investors should be able to gain even more fine-grained control over the investment strategies they include in their portfolios and how they want to balance between growth and income to match their risk preferences.

Democratizing Access to the Private Markets

I’ve avoided using the word democratization up until this point. Democratization in this case is relative. Not everyone will be able to invest in Equi for a long time, not until the SEC loosens accredited investor restrictions at the very least.

But over the next couple of years, Equi is embarking on a journey to gradually democratize the investing strategies previously available to only UHNW investors. That plan has five stages.

In their MVP, the investment minimum was $1m and limited to only a few dozen early customers.

For the beta of the tech platform, Equi is limiting investment to a group of 300 people with a minimum check size that’s in the hundreds of thousands. This is the beta test, and all of the company’s co-founders are participating themselves, by putting at least 80% of their liquid net worth into Equi’s strategies. In the next wave, they’ll let in 1,000 more investors.

In Phase III, thanks to the novel FoF structure I mentioned earlier, Equi plansto scale to thousands of accredited investors (hopefully lowering the minimum even further). They also plan to expand the technology platform to offer lines of credit against investor’s alternative investments and a spending product.

In Phase IV, Equi plans to launch an advisor platform that helps financial advisors offer alternatives to their clients.

In the master stroke, Equi hopes to register public funds that can scale to tens of thousands of investors, retail and accredited, at much lower $10-15k minimums.

If the Equi team could offer this to everyone today, they would. They’re going through the complexity of dealing with smaller checks in the first place because they want to bring a superior style of investment out of the institutions to the people. But it’s going to take some time.

There are regulatory hurdles to overcome. Figuring out how to let people withdraw money when Equi’s funds are invested in other funds with their own lockup periods and restrictions is a non-trivial technical and administrative challenge. They’ll need to figure out how to scale their investments across more managers and in-house strategies while maintaining or improving the current efficient frontier. All of this takes time and work, but truly democratizing access to alternative investments is Equi’s North Star.

For now, Equi’s early traction has been phenomenal. The company has spent $0 on marketing, and they’ve already received $136M of inbound AUM interest. People are hungry for products like this, including some incredibly sophisticated investors who’ve already committed to invest through the platform.

Instead of spending on paid acquisition, the company has focused on education. Its YouTube channel is chock full of entertaining, educational content, and Itay is sharing unbelievably valuable content on Equi’s open market calls. They give a glimpse into a side of the market that most people never get to see. As someone who’s obviously a fan of the content + investing approach, I’m really impressed by how Equi’s built a following among sophisticated investors.

The next step is launching the tech platform, which Equi plans to do in August. In the beginning, the app will help clients onboard, understand how Equi might fit into their portfolio, learn about the asset classes supported on the platform, and personalize their investments to match their goals.

Soon, the product might provide more granular portfolio customizability.

Over time, the Equi platform might power borrowing, spending, automated client servicing and investing, and liquidity for illiquid investments… in other words, many of the things that investors would get if they had $100M+ and a family office, and more, without needing to talk to a human, right in their pocket.

Again, this post is not a call to go invest all of your money through the Equi platform. Even institutions and family offices allocate only about 50% to alternatives, and Equi is best thought of as a way to add more alternative investments to your portfolio.

Personally (this is definitely not investment advice), if I had enough cash lying around to invest in Equi, I would probably do something like 40% equities (a mix of discretionary and systematic, via Composer, of course), 15% crypto, 15% venture, and 30% to alternatives via Equi. For me, investing is about fun, competition, and learning as much as it is about generating the best possible returns, so I’d have about half safely in Composer (equities) and Equi (alternatives), and take more hands-on risk with the rest.

The beauty of Equi is that, for the first time, accredited investors have access to invest the way that the institutions do and the ability to choose from the full universe of options. There’s no dogma; the best new investing products will give normal people more arrows in their quiver, and the agency to shoot those arrows however they decide.

If you would like to apply to invest as one of Equi’s first 300 customers, you can right here:

While they can’t guarantee anything, they will give Not Boring readers a special look.

If you want to keep learning and go deeper down this rabbit hole, that’s what it’s all about! Sign up here to receive Equi’s emails and invites to Monthly Market Update Calls, and check out the Equi YouTube channel. It’s really excellent at explaining complex topics simply.

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Monday!

Packy

um