Welcome to the 2,121 newly Not Boring people who have joined us since last Monday! If you aren’t subscribed, join 25,452 smart, curious folks by subscribing here!

🎧 To get this essay straight in your ears: listen on Spotify.

This week's Not Boring is brought to you by…

I’m excited to introduce you to OnJuno, which officially launched their new personal checking account with the best startup commercial I’ve seen in a long time (check it out on their site). Join now to get a 2.15% bonus rate on your deposits and 5% cashback on your favorite brands.

After keeping my money with a traditional bank my entire adult life, OnJuno’s gorgeous UX and responsive customer support is refreshing. That’s not how I expected to describe a checking account. If you’re tired of hidden fees and low-interest rates on boring and unintuitive banking products, try OnJuno.

Create an FDIC insured checking account in under 5 minutes

Earn 2.15% Bonus Rate & 5% Cashback on Amazon, Walmart, Netflix, and more

Withdraw your money anytime, with no penalties or hidden fees

Join now, it’s free. (Limited Spots available)

Hi friends 👋 ,

Happy Monday!

It’s an exciting one over here at Not Boring HQ. There are now more than 25,000 of us here! That’s wild.

On New Year’s Day, when there were only 309 people reading a newsletter called Per My Last E-mail, I wrote out some goals for the year.

Obviously, a lot has changed since then. The place-based company I wanted to start is no longer, and I get to write Not Boring full-time. If this is all I did for a living and only 1,000 people subscribed, I’d be in trouble. But it still absolutely blows my mind that 25k of you read what I write, that companies are willing to pay me to tell you about their products, and that this is my job. I’m incredibly thankful to all of you.

To celebrate, I decided to up the difficulty level a little bit this week. Anyone can make Stripe or the Metaverse sound exciting, but what about a company that we all love to hate, run by one of the least charismatic leaders in human history?

Let’s get to it.

Everybody Hates Facebook

The Devil We Know

Look, I don’t want to be writing this. You hate Facebook. I hate Facebook. Regulators hate Facebook. The only person who likes Facebook is that guy you went to high school with who posts Q Anon content and still wishes you happy birthday every year. Just look at the product. It’s a Frankenstein built from years of multivariate testing instead of product vision.

The reasons to hate Facebook are as numerous and fast-growing as their Daily Active Users. I’ve railed in this very newsletter about how wasteful it is that startups spend an estimated 30-40% of the money they raise on Facebook, Google, and Amazon ads. Zuck is not particularly lovable. The New Big Blue is where so much Fake News goes viral. Social media is addictive. Facebook just copies competitors’ best features. Facebook knows everything about us. The list goes on and on.

But here we are, writing about the reasons to be bullish on Facebook, for the same reason that so many businesses turn to Facebook: we don’t have any other choice if we want to grow.

After a euphoric 2020, anything that even smells like a growth stock is up dramatically. I just picked eight names off the top of my head: Peloton, Etsy, Shopify, Virgin Galactic, Tesla, Square, Spotify, Snap. The worst performing, Spotify, is up 128% YTD. Airbnb and DoorDash doubled their IPO price targets before they started trading. Even my beloved, beleaguered Slack got acquired.

A lot of people invested in tech need to think about where to park their gains from the past year. Something safe, but with upside. Something that will benefit from the continued transfer from offline to online, but that likely won’t crash if multiples come back to earth. Something that will at least outpace inflation. Something with international exposure. Something that’s been held back by reasons only semi-related to the company’s performance. Something like… Facebook.

Some of you might be thinking: “Duh yes, Facebook is one of the most valuable companies in the world. I watched The Social Network and The Social Dilemma, too. I know that Facebook is rolling into eCommerce. I’ve seen all of Mark Zuckerberg’s Congressional hearings. I come to Not Boring for new stuff, not boring companies like Facebook.”

Aha! Because of that, I think that we might all be sleeping on Facebook a little bit. I know I have. So many of the things that we view as negative about Facebook are positives if you put on your investor hat and hold your nose.

Monopolistic. While most acquisitions fail, Zuck and Sheryl have been so good at acquiring companies that the government is stepping in post-hoc to try to undo them.

Tax on the Internet. That same “40% of all venture dollars raised” stat that’s rough for eCommerce businesses is great for Facebook. eCommerce needs Facebook to grow.

WhatsApp Unmonetized. WhatsApp is the most popular messaging app in the world, and Facebook has barely started monetizing it. My god…

Zuck Has Too Much Power. If you think he’s an evil sociopath, that’s bad. But if you think he’s also a genius with a hard-to-grasp, long-term vision, that’s really good.

Copycat. While it feels gross, it doesn’t really matter that Facebook copies from a business perspective. It owns distribution.

Privacy Regulation. Paradoxically, the regulations meant to protect users from Facebook and Google just deepen Facebook and Google’s moats.

This as much as anything is why I think regulators are stepping in to try to break up Facebook: all of the things that people dislike about Facebook are the same things that make it such an incredible business. Something just feels off about that.

You know I love me a bearish narrative that I think might crack. While the stock hasn’t dragged quite like Slack pre-Salesforce, Spotify pre-Rogan, or Snap pre-2020 Partner Summit, the fact is that Facebook feels kind of gross, so we just kind of ignore it, maybe buy a little, and focus on younger, fresher, sexier companies. But what they’re building is... actually kind of exciting.

Put your shoes back on and hear me out! It’s going to take some explaining, which I’ll do:

What is Facebook? There’s a lot going on. To understand everything that Facebook is planning, we need a good sense for what Facebook actually does today.

Facebook’s Business Model. Zuck built what is arguably the world’s best business model, and he has the margins to prove it.

Facebook’s Boring Stock Performance. While anything that even smells like eCommerce is exploding, Facebook, which collects a hefty tax on most eCommerce transactions, is underperforming the Nasdaq. That’s why we’re here today.

Digital Real Estate. With the decreased importance of offline real estate, Facebook’s online real estate is some of the most valuable in the world.

The Most Ambitious Backward Integration in History. Instead of just selling ads, Facebook is backward integrating into the transactions themselves.

Facebook’s New Reality. Facebook is pushing heavily into AR, VR, and spatial computing in an attempt to control the next big computing platform.

Putting it All Together. Facebook is an advertising juggernaut on pace to do more than $80 billion in revenue this year at 80+% gross margins, which has only become more critical for advertisers during the pandemic. Because it’s hated, you get all of that at a slight discount without accounting for Facebook’s wild bets on the future.

Just to be extra clear: this is not a value judgement. Facebook may very well be evil. As I was writing this post, I hopped on to Twitter, and this is the first tweet that popped into my feed:

But because we all think Facebook is evil, we don’t spend much time trying to understand the full scope of the business behind the products on which we spend 65 minutes per day.

What is Facebook?

Facebook is so omnipresent that the analysis of the company is all trees, no forest. When I started researching this piece, I realized that despite reading Stratechery daily and spending a lot of time on tech twitter, I don’t fully understand everything the company does and how it all fits together. So let’s all admit that we’ve lost track, hit reset, zoom out, and admire the forest.

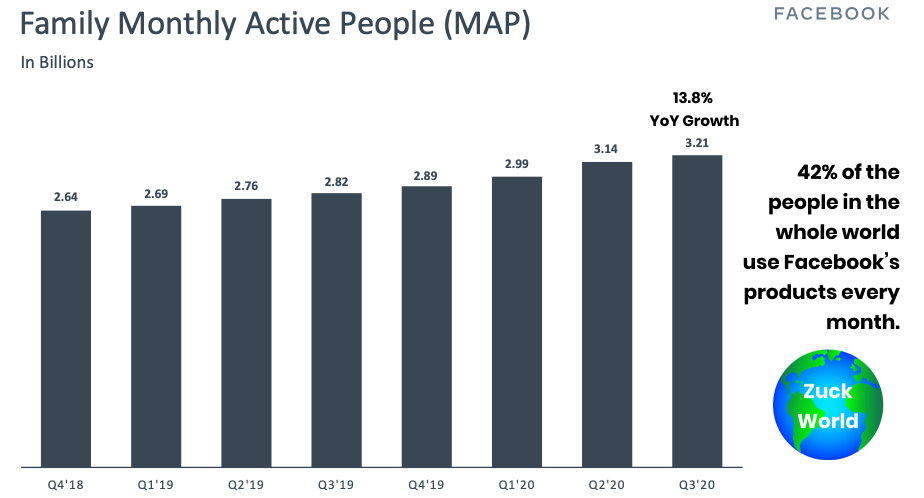

Nearly half of the world’s population uses one or more of Facebook’s four main social media properties - Facebook, Messenger, Instagram, and WhatsApp. Facebook is also building what it hopes is the next computing platform through Facebook Reality Labs, which houses Oculus, Portal, Spark AR, CTRL-labs, and more.

The main Facebook product had 1.8 billion Daily Active Users (DAUs) and 2.7 billion Monthly Active Users in Q3 2020, while the “family” of products saw 2.5 billion Daily Active People (DAPs) and 3.2 billion Monthly Active People (MAPs). They don’t report weekly figures, or what I’d assume they’d call “WAPs.”

Mark Zuckerberg founded Facebook in 2004 from his Harvard dorm room and IPO’d the company in May 2012 at a $104 billion market cap. The story is well-covered, but I’d be remiss if I didn’t mention one of my favorite quotes in recent cinematic history, from 2010’s The Social Network: “If you guys were the inventors of Facebook, you’d have invented Facebook.”

To build out its current Family of social products, Zuckerberg made three big moves:

Acquired Instagram for a then-astonishing $1 billion in 2012, a month before IPO. (Read Sarah Frier’s excellent book, No Filter, for the full story.)

Acquired WhatsApp in 2014 for an even-more-eye-popping $19 billion in 2014.

Spun out Messenger from the core product in 2014.

(Facebook also tried to acquire Snapchat in both 2013 and 2016, but CEO Evan Spiegel turned them down both times.)

Facebook has used social acquisitions both offensively and defensively:

Instagram. Investors’ biggest concern going into its IPO was its weakness on mobile. Facebook acquired the mobile-first Instagram to fill that gap (in addition to what Wharton Magazine called “the most epic tech pivot of the decade” to make Facebook itself a mobile product.)

WhatsApp. Just as Facebook was making messaging a core service, WhatsApp was eating Messenger’s lunch in terms of engagement, and growing much faster.

Snap. While the acquisition failed, the logic behind the attempt was clear. Facebook struggled to attract young users who were turned off by their moms’ presence. Snapchat is excellent at acquiring and retaining young users.

Last week, the FTC and 46 states announced that they are suing Facebook to unwind the Instagram and WhatsApp acquisitions post-hoc, even after the FTC investigated and allowed the Instagram acquisition back in 2012. The FTC highlights emails in which Zuckerberg discusses “neutralizing potential competitors,” which sounds pretty anticompetitive, but they likely wouldn’t have brought the lawsuit if the acquisitions hadn’t been so darn successful.

Instagram. The Acquired podcast called the Instagram acquisition the greatest acquisition of all time, reasoning that, at the $20 billion in 2019 revenue Bloomberg reported it did, the $1 billion acquisition is worth $153 billion of Facebook’s market cap.

WhatsApp. WhatsApp is the most popular messaging app in the world, and it’s not even close. WhatsApp has a reported 2 billion monthly active users, followed by Messenger with 1.3 billion, and Weixin/WeChat with 1.2 billion.

All told, advertisers across the globe can reach nearly half of the world’s population via Facebook’s properties. Despite a massive base of 2.82 billion people, it grew MAPs 13.8% YoY.

And that’s despite being banned in China, the world’s most populous country. If you remove China, Facebook reaches over half the world’s people.

India is crucial to Facebook’s story: it has the most Facebook users (310 million) and most WhatsApp users (340 million) in the world, and Facebook recently invested $5.8 billion for 9.99% of Jio Platforms, Reliance’s telco which provides the 4G and 5G infrastructure powering India’s digital revolution.

Back on the homefront, the company’s legal battle looms. I’m not an antitrust lawyer, so I have no idea whether the FTC’s attempt to break up Facebook will succeed. Prevailing wisdom seems to be that Facebook won’t be broken up, but that it will be limited in its ability to make future social acquisitions.

That’s just fine. Facebook is in a pretty good spot with what it’s got.

Facebook’s Business Model

There are a lot of good business models on the internet, but Facebook’s might be the best of all. To understand why, it’s helpful to compare Facebook’s business with Google’s.

Facebook makes money by aggregating consumer attention and data through its four main properties, and selling both to advertisers so that they can reach the right people with personalized ads. Like Google, Facebook generates the vast majority of its revenue (98.52% of its $70.7 billion in 2019 revenue) from selling ads.

Facebook and Google are the only companies that Ben Thompson refers to as “Super-Aggregators”:

This, then, is a super-aggregator: zero transaction costs not just in terms of user acquisition, but also supply acquisition, and most importantly, revenue acquisition, and Google and Facebook are the ultimate examples.

In other words, Facebook has almost zero marginal costs -- they don’t pay to get me to use their products, I go there to see my friends’ content (which Facebook also doesn’t pay for), and advertisers self-serve through Facebook Business Suite without talking to an expensive sales person.

While Google is intent-based -- I search for shoes and Google serves me ads for companies that make shoes -- Facebook is interest-based -- I am a 24-35-year-old male with feet who likes running, so companies that sell running shoes can reach me and others like me across Facebook’s properties (and on other sites via its Audience Network). Google can show me different variations of something I want, Facebook can show me products I didn’t even know I wanted. According to eMarketer, Facebook is slowly stealing market share from Google:

Not only is Facebook growing faster than Google, it’s doing so at a much higher margin. Facebook’s numbers are astonishing.

Revenue. $70.7 billion in 2019, grew 21.2% YoY in Q3.

Gross Profit. $57.9 billion in 2019, good for an 81.9% gross margin. (Google’s is 55.6%)

EBITDA. $34.6 billion in 2019, for a 48.9% EBITDA margin.

Cash. $55.6 billion as of September 30, 2020, even after its $5.8 billion Jio investment.

Users. 3.2 billion Monthly Active People across its apps worldwide.

Despite its mind-blowing business model and the fact that Facebook is essentially a tax on eCommerce, its stock has remained relatively sleepy even as eCommerce penetration has doubled.

Facebook’s Boring Stock Performance

In Software is Eating the Markets, I wrote about the idea that because of new software products and increased access, retail investors are actually buying more than just a financial asset when they buy a stock; they’re buying social status, entertainment, education, and a digital asset that they can proudly display.

Tesla is Exhibit A here. Owning Tesla gives you social status - its fans are a community, and its products ostensibly save the planet. Elon Musk is entertaining as hell (watch Elon debate Jack Ma). Following Tesla (and by extension, SpaceX) is an education on the bleeding edge of technology. All of that means that Tesla bulls are proud to show off their Tesla shares as if they’re a digital asset with their own independent value. As a result…

This can work both ways, though.

Take Facebook. Owning the company has negative social status and is not a digital asset that most people would proudly display. We’re already bombarded with news about Facebook and all of the evil things it does, and spend over an hour on its properties every day, so investing in it is not that educational. And the company is a $700 billion-plus behemoth under attack from regulators; the stock doesn’t move wildly, it’s as blue chip as tech gets, which isn’t very entertaining. And have you ever watched Mark Zuckerberg speak? 😴

The Retail Investor Chart for Facebook looks something like this:

Is anyone pumped to tell their friends they bought Facebook? I feel kinda embarrassed writing this whole thing, tbh. Add some antitrust hairiness into the mix, and you get this...

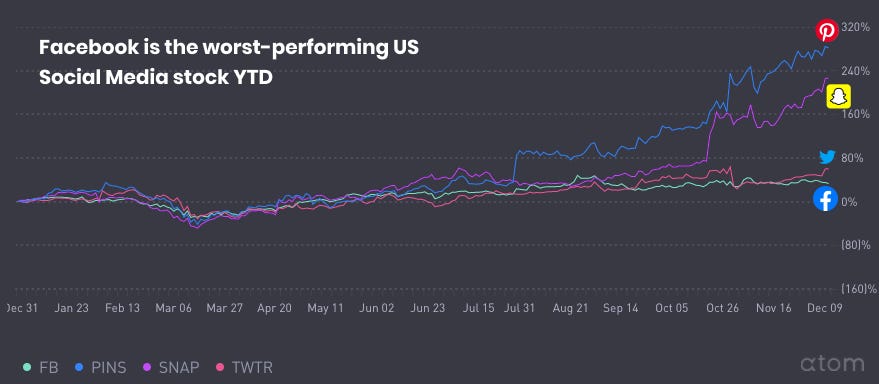

The underperformance is more stark when you compare Facebook to its competitors across Social, FAAMG, and eCommerce. Here it is versus the social media companies Snap, Pinterest, and Twitter.

To be sure, Pinterest and Snap grew much faster (off much smaller bases) than Facebook. While Facebook grew 21.2% YoY in Q3, Pinterest grew 58.2% (2.7x faster) and Snap grew 52.1% (2.5x faster). But their prices grew much faster than the relative revenue growth rates would suggest: Pinterest’s price is up 8.5x more than Facebook’s, and Snap’s is up 6.8x more. And then there’s Twitter, which actually grew revenue more slowly (at 13.7%) but has outperformed Facebook stock by 1.8x.

So maybe it’s just that the market loves anything with a lower market cap because those stocks have more perceived upside (it doesn’t make sense, I know). If that’s the case, Facebook should fare better against the other FAAMG stocks (Apple, Amazon, Microsoft, and Google).

Nope. Facebook is tied for the worst YTD performance among the FAAMG stocks with Google, at 33.3%, just slightly behind Microsoft (35.2%). Amazon and Apple have outperformed Facebook by more than 2x at 68.7% and 66.7% respectively. Facebook, though, sports the second-fastest YoY revenue and EPS growth behind Amazon, growing nearly twice as fast as Apple, Microsoft, and Google, and the highest gross margins and EBITDA margins of the bunch.

We can do the same thing for eCommerce, where AMZN is the laggard at 68% YTD growth.

Summarizing all of that in one, clean metric: Facebook trades at the lowest LTM and forward P/E multiples of any of the FAAMG, Social Media, or even eCommerce stock in its comp set.

Like I said, people hate Facebook. But ‘tis the season, and anything even resembling value that has tech upside is a gift from Market Santa.

Plus, holiday shopping might break the floodgates. Facebook owns the most valuable digital real estate in the world during the time when digital real estate is more important than it’s ever been.

The Importance of Digital Real Estate

In the Social Capital 2018 Annual Letter, Chamath Palihapitiya wrote: “Startups spend almost 40 cents of every VC dollar on Google, Facebook, and Amazon.” I’ve written about this many times, but only from the perspective of the startups doing the spending. From Facebook’s perspective, taking its share of 40% of the money startups raise is a fantastic thing. And Chamath wrote that back when many startups had the option to spend on retail distribution…

In order to counteract Facebook, Google, and Amazon’s power and decrease customer acquisition costs (CACs), many DTC companies came offline, into physical retail. Physical presence gives brands the opportunity to acquire customers who happen to be walking by. What they lose in margin from paying rent and employing store associates, the idea goes, they make up in lower CACs.

Warby Parker kicked off the trend a few years ago by launching their own brick and mortar stores, and other DTC darlings like Bonobos, Casper, and Everlane followed suit. A 2018 JLL report projected that digitally native brands would open 850 retail locations in the next five years. Countless more added retail to their channel mix by selling through Walmart, Target, and other big box stores.

COVID stopped that trend in its tracks. Not only did it push digitally native brands back to online-only, it forced offline businesses to move online in earnest for the first time.

eCommerce platforms’ share prices have skyrocketed during COVID as a result. Amazon is the only one in this basket of eCommerce leaders that hasn’t more than doubled, and it’s up 68% off a market cap that was just under $1 trillion coming into the year.

And it’s about to get really crazy. The fourth quarter is traditionally the strongest time of the year for retailers and eCommerce companies because of holiday shopping. This is what Black Friday used to look like:

This year, most of that chaos moved online. Shopify saw a 76% increase in Black Friday/Cyber Monday sales from $2.9 billion in 2019 to $5.1 billion in 2020, while independent sellers on Amazon increased sales 60% to $4.8 billion. It makes sense that eCommerce platforms’ shares would rally. That’s where shopping gets done today.

But Facebook should be a major beneficiary too, because brick and mortar wasn’t just where the sale happened, it’s where discovery happened as well. Now, both digitally native and traditional retailers are being forced to acquire customers online, creating marginal demand for Facebook’s product and driving up CPMs across the board.

I spoke to two people who confirmed my hunch:

An eCommerce company told me they were seeing higher CACs than ever before because of increased competition from offline retailers, but that they were spending anyway, because they needed to hit holiday targets and were still seeing a positive return on their Facebook ad spend.

A venture capitalist told me their portfolio companies, large private companies in the US and abroad, were setting records for Facebook spend recently.

With physical real estate’s decreased importance, digital real estate is more important than ever. And no other digital platform can reliably deliver the same returns for advertisers that Facebook can across its Facebook and Instagram properties (although some companies outperform in specific channels).

That position is starting to show up in the numbers. In July, Facebook guided to 10% YoY revenue growth in Q3. Thanks to an unexpectedly strong August and September, it grew 21% YoY, blowing out its own expectations. While it didn’t give specific guidance for Q4, CFO Dave Wehnher said on the earnings call that the company expects Q4 growth to be higher than the Q3 growth rate. I think it’s going to report eye-popping Q4 numbers.

Today, ten million businesses advertise on Facebook across the globe. If they consolidate all of their spend online over the holiday season, it will provide a short-term spark to Facebook’s stock. But it’s Facebook’s backward integration directly into commerce that gets me most excited.

The Most Ambitious Backward Integration in History

What Facebook is trying to pull off is unprecedented: it’s a $780 billion company that generates 98.5% of its revenue from a high-margin ads business backward integrating into eCommerce. Ads won’t just be top-of-funnel, they will be the funnel.

Facebook does more for businesses than just allow its ten million advertisers to target customers with personalized advertising. It also gives 200 million businesses a suite of free tools to reach, communicate with, and now, sell to customers.

To hear Zuck and Sandberg talk about it, it almost sounds like Stripe without the Irish brogue -- they, too, want to increase the GDP of the internet by empowering small businesses. While Stripe benefits from a growing internet in the form of transaction fees, Facebook benefits from more demand for ads.

Increasingly, Facebook is backward integrating from simply being an advertising platform into building the tools to facilitate customer communication and commerce in-app. Just like Tencent built tools for businesses in WeChat after seeing businesses communicating with customers in the app, Facebook saw businesses in Thailand use profiles on WhatsApp, Facebook, and Messenger as their homepages and leaned in by adding features. They built catalogs, then a Marketplace Tab, then power tools. Now, Facebook powers roughly 1% of Thailand’s GDP (~$5 billion in GMV), and Facebook is rolling out the tools that it built there in the US and around the globe.

Over the past year, Facebook has undertaken two related projects to unify the Family of products and help businesses sell through them: Messaging Interoperability and Shops.

Messaging Interoperability. Facebook is in the middle of a large infrastructure project that will allow people to send messages to each other from their Facebook messaging product of choice -- Messenger, Instagram Direct, or WhatsApp. If I spend all of my time on Instagram, but my mom uses WhatsApp, I’ll be able to send a message from my Instagram Direct to her WhatsApp, and vice versa. In September, Facebook released the first leg of the project: cross-platform messaging between Messenger and Instagram.

Interoperability has two main benefits for Facebook. First, it strengthens its network effect by increasing the utility for any user if their friends use any of the three Facebook messaging products. Second, it allows businesses to communicate with customers wherever they prefer. Facebook’s new Business Suite, which it also rolled out in September, features one inbox for customer messages from Instagram Direct and Messenger and comments on Facebook and Instagram posts.

Communication is the easiest path online. It’s easier than building a website and accepting payments, even with Shopify and Stripe. If Facebook’s Business Suite and improved messaging capabilities allow more businesses to sell online, it will create more potential ads customers and maybe more businesses willing to pay for Facebook to run the lightweight backend of their business.

Shops. In May, Facebook announced the launch of Shops on Facebook and Instagram. Shops let businesses set up free storefronts on their Facebook or Instagram profiles, powered by one backend. From the Facebook or Instagram stores, customers can either click through to buy on the businesses’ websites, or buy directly in-Shop via Checkout.

Instead of building all of the eCommerce infrastructure itself, Facebook is partnering with any eCommerce platform not named “Amazon.” When Zuckerberg announced the product in May, he invited Shopify CEO Tobi Lutke to the stream. That highlights Shopify’s relative importance, but it is not, as originally reported, Facebook’s exclusive partner. Understanding the relationship between the two companies in light of Facebook Shops is a whole ‘nother post, but it’s interesting that Shopify is acting like an API-first company for Facebook here.

Shops does a couple of things for Facebook. First, it should help increase conversion by removing friction, which will ultimately make businesses want to buy more ads. Second, Facebook will make money from a small transaction fee via Checkout.

Over time, Messaging Interoperability and Shops will continue to converge. On the Q3 earnings call, Zuckerberg said that the goal is to build a commerce platform around messaging, starting with bringing Shops to WhatsApp and Messenger, and by building tools that let businesses follow up with customers, complete transactions, and accept payments.

In a first step towards monetizing that vision in the US, Facebook began testing a new ad product, click-to-messaging, through which businesses can generate conversations with customers.

That ad product, and the increased focus on commerce through messaging, helps explain Facebook’s late-November $1 billion acquisition of Kustomer (talk about a high Kustomer acquisition cost!). Kustomer is a control center for conversations that take place across channels -- from text, to email, to social media -- which fits nicely with Facebook’s goal of unifying messaging, and also uses AI to handle simple requests, which should allow businesses to deal with increased conversation volume generated by click-to-messaging ads.

Just last week, Facebook rolled out more features to improve messaging-based and in-app commerce. Last Wednesday, it added carts to WhatsApp, and on Friday, it added shopping to Reels, its TikTok clone.

These solutions are still clunky. In the US, for example, WhatsApp carts don’t support payments, so businesses and customers need to arrange payments separately. But Facebook recently rolled out WhatsApp payments in India, where it is the country’s SuperApp, after years of government pushback. Facebook’s $5.8 billion investment in Reliance’s Jio Platforms likely helped grease the wheels. As with Marketplace in Thailand, as Facebook works out the kinks in India, it will roll out messaging-based payments to its 3.2 billion MAPs around the globe as it slowly convinces governments it can be trusted with our money.

As it continues to connect its various platforms and integrate more commerce and payments functionality, Facebook will complete the most ambitious backward integration in history, from ads into eCommerce. It will own the funnel.

To be sure, all of this is early and unproven, and Facebook isn’t exactly known for its product innovation. For a unification project, it all feels a bit piecemeal. Plus, the company has also faced headwinds in markets around the globe, where governments are slow to trust Facebook to handle payments. But it points to how Facebook is thinking about unifying its products to help businesses not only reach, but communicate with and sell directly to, new and existing customers, wherever they happen to be.

To that end, it’s not hard to imagine that Facebook might even roll out Shops and messaging functionality through its mobile app ad network, Facebook Audience Network. The implications of that would be enormous. It would mean businesses will be able to set up … shop … anywhere they’re able to place ads today. Imagine checking out directly in ads across the internet; see, click, buy, or talk to a person (or AI) to answer any questions. If Facebook pulls off that vision, it will have its own Everywhere Store to battle Amazon’s Everything Store.

Oh yeah, and one more thing…

Facebook’s Next Reality

Everything that Facebook has achieved on mobile is made more impressive by the fact that Facebook almost missed the platform altogether. It was a desktop-first product when it went public, and the market didn’t believe it could make the transition to mobile. The app was janky and built on HTML5 (RIP), and analysts feared that a mobile NewsFeed couldn’t support an ad load. Its shares fell from $42 to $19 in Facebook’s first three months as a public company.

Zuck fixed the mobile problem by acquiring Instagram and pushing the company into a hard pivot, but it was harrowing, and he vowed to not miss the next one. To that end, Facebook made two acquisitions that are particularly intriguing:

Oculus. Acquired the maker of VR headsets for $2.3 billion in 2014.

CTRL-labs. In a less splashy move, acquired the brain-computing startup for between $500 million and $1 billion in 2019.

As of August, Facebook rolled Oculus, CTRL-labs, Portal, and Snap Lens Studio lookalike Spark AR into Facebook Reality Labs. The division, reporting to Andrew ‘Boz’ Bosworth, is responsible for Facebook’s efforts in VR, AR, and the spatial computing operating system. With its hands tied on social and messaging acquisitions, eight of its last ten acquisitions have been under Facebook Reality Labs. It’s easy to dismiss the effort -- who wants Facebook controlling the Metaverse? -- but it’s showing potential.

Portal. After a chilly reception that went something like “no fucking way am I letting Zuck into my house,” Portal sales have taken off during the pandemic. My sister lives in Ghana, and she and my mom talk over Portal every day. When we’re all physically distanced, the Portal can make people feel closer together.

Oculus. Facebook lowered the price point for the Oculus Quest 2, it’s newest VR headset, to $299, and pre-orders surpassed the original Oculus’ by 5x. Oculus Quest 2 is the best standalone headset on the market, and is likely to be the best-selling of all-time.

Spark AR. While this is a painfully blatant rip off of Snap, the same logic I used for Snap holds here: by putting lightweight AR in hundreds of millions of peoples’ hands, Facebook is getting an early headstart on building Mirrorworld.

AR Glasses. Facebook has plans to release AR glasses next year, in partnership with Luxottica. Early attempts to build AR glasses -- from Google Glass to Snap Lenses -- have ranged from butt-of-joke to toy-like, but if Facebook can marry what’s worked in Oculus with the lighter touch needed for AR, it has a shot.

Just like Facebook’s social apps, the Facebook Reality Labs products will work together, in this case to try to usher in the era of spatial computing on Zuck’s terms. To become the platform, Zuck predicts the company needs to sell 10 million Oculus headsets in order to attract enough developers to build an ecosystem. That’s why the company dropped its price to $299.

The prize couldn’t be bigger: if Facebook becomes the default platform for VR, AR, or both, it will hold the position that Apple and Google hold in mobile today. Plus, it will be able to plug in its social, messaging, and commerce features to the new platform from day one, creating new opportunities for businesses, and of course, for Facebook itself.

Is Facebook owning a foundational Metaverse platform a good thing? Probably not. Over the past two weeks, I finally read Ernest Cline’s 2012 Metaverse instant classic, Ready Player One, and his new sequel, Ready Player Two, so I’m on high-alert. If the real thing turns out to be anything like the books’ fictional OASIS, the decisions that the platform owner makes will have an unprecedented impact on billions of lives.

Ready Player One takes place in a VR world powered by an advanced Oculus Quest-like headset. Ready Player Two raises the stakes when it moves players from VR headsets to ONI, a non-invasive neural interface through which players can control their avatars and experience others’ lives just by thinking. Facebook has its own answer to ONI in CTRL-labs, which brings great promise and great danger, and will need to be regulated appropriately if it comes to market.

Dystopian visions aside, in both fiction and, I suspect, reality, the company that owns the Metaverse will be the most valuable in the world. We’re many years away, and I prefer Tencent and Epic’s more decentralized approach, but Facebook is a contender, and you get that upside potential for free.

Putting it All Together

Facebook is hard to love. Concerns around privacy and anticompetitive behavior abound, it rips off other companies’ product work, and I’m not convinced Mark Zuckerberg isn’t a robot.

But as Ben Graham told a young Warren Buffett, “In the short run, the stock market is a voting machine; in the long run, it’s a weighing machine.”

Facebook will do more than $80 billion in revenue with gross margins over 80% and EBITDA margins over 40%. Half of the people in the world outside of China use its products. It’s built arguably the best business model in the world. It stands to benefit as much as anyone this side of Seattle from the dramatic and sudden shift to eCommerce.

But despite that, it’s trading at the lowest P/E multiple among FAAMG, eCommerce, and social media companies.

There are obvious headwinds. We’ve discussed many in the piece, including an active antitrust lawsuit, and we haven’t even mentioned two of the strongest:

Apple’s IDFA update in iOS 14 which will hurt Facebook’s ability to collect data and target customers in apps.

TikTok may steal attention, the lifeblood of an Aggregator, from Facebook, or at the very least, hamper its ability to acquire young users.

But Facebook is undervalued relative to any set of peers, and that’s before taking its bets on the future into consideration. In the near-term, it is unifying messaging, social, and commerce in the most ambitious backward integration in history. Long-term, it may become the platform on which the Virtual Reality economy is built. And we got through this without mentioning Facebook’s crypto project (currently: Diem) 😏 or its Giphy acquisition.

I love finding an overblown bearish narrative. Normally, I disagree with its sentiment. In this case, I agree -- Facebook feels icky -- but in this market, I’m not letting a little ick get in the way of a good value.

Thanks to Dan and Puja for editing! You’re both the Sheryl to my Zuck.

Full Disclosure: I own shares in Facebook which make up less than 2% of my portfolio. This is NOT INVESTMENT ADVICE and I am not a registered financial adviser or CFA. I’m a guy who writes a free newsletter. Caveat emptor.

Thanks for reading, and I’ll see you on Thursday,

Packy