Clear Street: From COBOL to the Cloud

The $2.2 billion startup rebuilding capital markets infrastructure from the ground up

Welcome to the 1,000 newly Not Boring people who have joined us since last week! If you haven’t subscribed, join 220,232 smart, curious folks by subscribing here:

Today’s Not Boring is brought to you by… Clear Street

Read on to learn about how Clear Street is rebuilding the infrastructure of the capital markets.

Hi friends 👋,

Happy Wednesday and Happy Valentine’s Day!

Love is in the air, and besides Puja, Dev, and Maya, there’s nothing I love more than a Hard Startup working to replace crumbling infrastructure with modern technology, and succeeding.

That’s what Clear Street is doing, modernizing capital markets infrastructure through which over $3 trillion flows daily by rebuilding it from the ground up.

Clear Street has been an under-the-radar monster, known well to a select few, like the founder who told me “I would so prefer to be on Clear Street it’s not even funny,” but not as well-known in the wider startup world. I think it’s a company and a story a lot of startups can learn from as they attempt to face-off against entrenched incumbents armed only with technology, talent, and ambition.

Just five years old, Clear Street was recently valued at $2.2 billion. This isn’t a ZIRP valuation: Clear Street did $260 million in revenue in 2023, and it did so profitably. Getting to this point has taken a unique blend of experience, capital, long-term thinking, and technical chops. Relative to its ambitions, Clear Street is just getting started.

This essay is a Sponsored Deep Dive. While the piece is sponsored, these are all my real and genuine views. I’m writing fewer Sponsored Deep Dives, because as I said when I wrote about LayerZero in December, I’m only writing them on companies that I think have a chance to be really important in an area I care about. You can read more about how I choose which companies to do deep dives on, and how I write them here.

Clear Street clears that bar: making the capital markets (and capitalism) run more efficiently and effectively is one of the most important things there is, and the full-stack Hard Startup approach its taking is full of lessons for founders who want to build insanely ambitious things in the face of incredibly deep-pocketed incumbents.

Let’s get to it.

Clear Street: From COBOL to the Cloud

It’s easy to tell when physical infrastructure decays.

You can see the rust on the bridges, feel the bump of the pothole, experience the terror of trice-daily train derailments, fill your cup with brownish water from the sink, and open your social media app of choice to discover how a Boeing 737 Max fell apart this time.

It’s hard to fix physical infrastructure because people use it every day. Shutting down a bridge means a minor inconvenience for thousands of people, so we put it off and risk major catastrophe.

It’s harder to tell when digital infrastructure decays.

Digital infrastructure is invisible, the pipes that power an ever-increasing amount of our lives, how we communicate, work, get around, and transact. It’s easy to forget that digital infrastructure is there because usually, it just works.

Like physical infrastructure, digital infrastructure is hard to fix because people use it everyday. It’s also hard because once companies reap the rewards of building the digital infrastructure on top of which other companies build, no one inside of those companies is incentivized to fix it.

Building infrastructure that others build on is a long journey with a huge payoff: the switching costs of replacing infrastructure are high. If given the choice between risking the cash cow to make the infrastructure better and just letting it slowly degrade while the cash cow produces, most infrastructure providers will choose the latter, to their own short-term benefit but to the long-term detriment of the whole system.

This is the reason banks still run on Common Business-Oriented Language, more commonly known as COBOL, a 65-year-old programming language that pretty much only 65-year-olds (and older) know how to maintain.

Over $3 trillion flows through COBOL every day. For decades, layers upon layers of disparate coding languages and technologies have been built on top of this infrastructure. And for a whole host of reasons, banks don’t rip it out and replace it.

Doing so would introduce the kind of short-term risks that come with tinkering with something built by someone who’s long-since retired and held together by a patchwork of digital duct tape. Not doing so, however, introduces the kind of major risk that threatens the financial markets and the invisible, counterfactual risk that comes from not innovating.

With physical infrastructure, you can’t just delete all of the roads and start fresh. The roads are the roads, and we need to fix what we got a little at a time, like after a bridge collapses on I-95.

With digital infrastructure, you can start fresh. It’s just really hard. It requires a combination of capital, experience, technical sophistication, and a different way of viewing risk.

Clear Street is doing it. In the early stages of a long journey, there are signs that it’s working. The cloud-native prime brokerage company recently closed a $250 million extension to a previous round, bringing that round’s total to $685 million at a $2.2 billion post-money valuation. It has $750 million on its balance sheet – a necessity in the prime brokerage business – and generated $260 million in revenue in 2023, its fifth year of business. Oh, and it’s EBITDA profitable.

The $2.2 billion valuation seems hefty for a five-year-old company, but relative to the opportunity, it’s small. Companies that have chewed off just the easier, surface-level piece of the problem – better interfaces on old infrastructure – like Broadridge and Interactive Brokers - are worth $24 billion and $41 billion in the public markets, respectively. Banks like Goldman, Morgan Stanley, Citi, JP Morgan, and Bank of America are worth, collectively, over $1 trillion.

Clear Street believes that the banks are going to have a very difficult time modernizing their own systems while running them simultaneously and potentially putting the trillions at risk. This isn’t just speculation: Credit Suisse’s demise can be traced to poor risk management stemming from bad infrastructure.

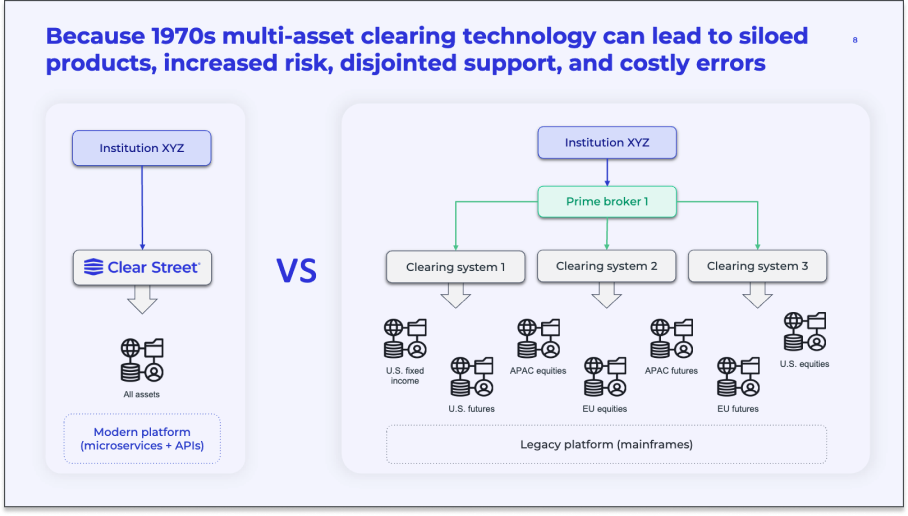

The banks’ reticence is Clear Street’s opportunity: to rebuild the infrastructure from the outside, and replace the old system with the new, slowly at first, one client, geography, and asset at a time, until financial markets around the world eventually run on Clear Street.

Tackling that opportunity means building a startup in a different way than most startups build. This isn’t a story of minimum viable products and pivots. Because it’s building infrastructure, Clear Street looks more like the Techno-Industrials that operate against a clear roadmap, with higher capital requirements and more specialized talent, from day one, than like a traditional software company.

Clear Street’s cofounder, Uri Cohen, started the business with his own capital in 2018 after experiencing the pain, and worrying about the risk of trading on crumbling infrastructure for over two decades on Wall Street. He recruited a CEO, Chris Pento, and a CTO, Sachin Kumar to co-found the company, both of whom had felt the same pain.

Then, in 2020, they bought their own online brokerage, CenterPoint Securities, to serve as the first customer of Clear Street’s clearing, custody, and prime brokerage products. If they were going to ask financial institutions to move off of their old, but tried and true, infrastructure, they’d need to prove that it worked on themselves, a la Amazon’s first and best customer strategy.

Meanwhile, they got to work completely rebuilding financial infrastructure from the ground up with modern software that needs to communicate with antiquated systems, like DTCC, and a hodgepodge of customers’ bespoke patchworks of code. They also began building all of the things that a prime brokerage needs to do to win clients’ business: research, investment banking, capital introductions, securities lending, margin, and more all at the same time.

Clear Street, while still early in its journey, is executing on its mission to build the cloud native pipes through which the capital markets will one day run, across every major asset class, in every major market, replacing the antiquated system that everyone from small prime brokerages to large banks use to move trillions of dollars every day.

And they’re offering a diverse product set that takes advantage of this modern technology stack, giving the largest hedge funds that currently work with banks, down to the smallest day traders that the bank can’t touch due to their cost structure, clean data from one single source of truth, bringing crystal clarity into their risk, and driving operational and strategic efficiencies in their businesses that could lead to growth that they can only currently dream of.

The ambition seems unlimited, because practically, it is. “The markets” are the world’s largest market.

The risk of capital market participants not modernizing their infrastructure, product offerings, and services, Uri believes, is equally huge: a Boeingesque series of increasingly frequent blowups like the ones that killed Archegos Capital Management, Credit Suisse, and Signature Bank, and worse.

There are a couple of ways they might come to appreciate the risk: the threat and the opportunity.

The threat is the risk of catastrophe that comes from operating on old infrastructure, the risk that Credit Suisse and Signature Bank learned the hard way but that takes at least a decade to remedy, at which point it’s someone else’s problem (or glory).

The opportunity is the set of possibilities that opens up when you can build products on one cloud-based platform with clean, real-time data. Every bank C-suite is thinking through how to take advantage of AI, for example, which could be catastrophic with bad data but nirvanic with good data.

In either case, the banking industry has proven that words aren’t as powerful as incentives. The industry’s current leaders don’t want to wade through the quagmire of replacing infrastructure, so Clear Street needs to build new infrastructure in parallel so that adopting it is a no-brainer for the industry’s future leaders.

Thinking in Risk

Clear Street was born from a lifetime of experience and one specific conversation.

Uri has spent over two decades in the financial markets. He’s a co-founder of Alpine Global Management, a firm with a breadth of sophisticated trading strategies across global markets, the kind of firm that demands a lot from its infrastructure.

A few years ago, Alpine had an issue with one of its large prime brokers, the one-stop-shops investment banks and financial institutions offer to support large investors. Prime brokers offer margin, securities lending, custody, trade clearing and settlement, risk management, reporting and more. But this large prime’s risk management and reporting were broken.

Their system was cobbled together from a string of acquisitions, and it was giving Uri the wrong data and costing him money. They miscalculated how much equity he had, against which they provided margin, and as a result, the fees he was paying were wrong.

He needed it fixed, but there was a problem: the only guy who knew how to fix it was a retired 70-year-old named Neil Stepanich who happened to be vacationing in the Himalayas.

Uri somehow got in touch with Neil, who said that he could fix it, “but it’s going to cost you a lot of money: $2,000.” That was just fine. Two hours later, it was fixed, temporarily, at least.

Over the next few years, Uri kept having more and more issues with the systems his prime brokers provided. He kept thinking, “OK, the banks will have to fix it now,” and the banks kept not fixing it.

Five years later, things had only gotten worse.

That year, in a meeting with two heads of prime brokerages, he asked, “Why aren’t you guys fixing this?”

The answer was simple and human: “It’s going to take seven to ten years, a lot of money, and a lot of headaches. We’re not even sure we will succeed.”

From their perspective, the decision not to fix makes sense: the payoff was too far out and uncertain. From Uri’s, it didn’t work: the system was causing him to lose money.

During that conversation, Uri made the realization that many entrepreneurs make at some point: if he wanted the system fixed, he was going to have to fix it himself.

Why Clear Street is So Hard to Build

What Uri, Chris Pento, and Sachin Kumar set out to build in 2018, on the surface, doesn’t sound too dissimilar from many software startups.

Clear Street was going to take an antiquated system and modernize it with software. Instead of mainframes, Clear Street would be cloud native. Instead of clunky integrations, Clear Street would be API-first. In place of slow, duct-taped systems and manual spreadsheets, Clear Street would give clients a comprehensive view of their portfolios in real-time and the ability to execute trades at internet speed.

And that is what they’re building. Clear Street offers clearing and custody, execution, prime financing, and white-glove services like capital introductions and account management to financial institutions and active traders.

Executing the startup playbook on the world’s financial infrastructure, though, is hard. Clear Street is a Hard Startup. In The Good Thing About Hard Things, I defined Hard Startups as:

The ones with no playbook, the ones that have R&D risk or some other hair on them that keeps competition at bay and gives them a clear path to short-term sales and long-term defensibility if they get a great product to market.

I broke them down to bits and atoms, and included infrastructure in the bits category: “these companies are often 100x harder below the surface than above it; there’s a lot of schlep.”

Clear Street is perhaps the best example of a bits infrastructure Hard Startup I’ve come across. Rebuilding the world’s financial infrastructure has more hair on it than Sasquatch.

The software challenge is incredibly hairy in its own right, and software is only one part of the story. Clear Street needs capital, risk management, and the client services muscle of an investment bank in order to get big clients to even use the software in the first place.

Let’s start with the software. It’s the core of the business and the thing that makes Clear Street different from other prime brokerages.

Jon Daplyn, the former Head of Prime Brokerage Technology at Morgan Stanley and now Clear Street’s Chief Information Officer, explained the challenge.

“The hardest thing,” he told me, “is that the systems you’re interacting with were built decades and decades ago. No one is building them; they were built in the past. You’ve effectively got to go and learn them from scratch.”

He described a steep learning curve and a ton of tech that needed to be built in order to put in even the first trade.

To start, you need to build your own core books and records that keep track of client information, account balances and positions, cost basis, margin details, and more, a big database of client information that updates in real-time. A database sounds relatively straightforward, but with so much information, from a variety of sources, including up-to-date market data, it’s a beast.

When I asked Jon for an example of something that was particularly hard to build, he cited this “account master,” the core system that maintains all client information and positions.

“You’d think implementing an account master would be straightforward,” he said, “but we’re already rolling out the second version because we didn’t get it quite right the first time.”

He noted, though, that this is the advantage of being a fintech instead of a bank: instead of saying “Why did you make that mistake?” they looked at it and said, “That didn’t work, let’s rip it up and do it again.”

“Our core value is technology, so we need it to be excellent.”

Step one is building excellent technology internally – that single source of truth that provides clean data to Clear Street and its clients. From there, Clear Street needs to connect its own systems with a patchwork of external ones that have no willingness to change the way they work to speak with a new entrant.

To enable even the first trade, Clear Street’s systems need to communicate with an alphabet soup of organizations, each of which have their own antiquated and mission-critical systems, like DTCC (Depository Trust & Clearing Corporation) and ICE (Intercontinental Exchange). The DTCC is responsible for clearing US securities, but individual exchanges, like NASDAQ, have their own clearing processes and systems that occur alongside the DTCC’s centralized clearing.

Just taking NASDAQ, trading activity on that exchange generates data that needs to flow through to post-trade systems for proper clearing and settlement. That includes obvious things like trade details – how many shares, what price, etc… – and less obvious things, like accounting for the exchange’s fees. Then there are the periodic things that happen – like stock splits, dividends, and repurchases – that happen at the exchange level and must get reflected properly in Clear Street’s own systems.

That’s just one exchange! Clear Street needs to send data to NASDAQ, other exchanges, clearinghouses, and regulators in formats in which they can digest it, and take data back in whichever format they choose to send it, clean it all up, and show it accurately in its own internal systems in order to give clients a real-time understanding of their positions, and in order to give Clear Street itself the data it needs to do things like extend margin to clients without blowing itself up.

And then, it needs to share that data with clients in a format that works for them. Many hedge funds and brokerages have built their own patchwork of systems and ways of handling data on top of old infrastructure, and since they’re not going to rip everything out and replace it with Clear Street whole cloth on day one, Clear Street needs to translate the data in its own system into language that each of those systems understands. It’s like a real-time Rosetta Stone operating inside of the chaos of the Tower of Babel.

And that’s just US equities!

Then, with the core systems built, Clear Street has to scale all of that – to more clients, more assets, and more geographies, each with its own idiosyncrasies and old systems with which to integrate.

Let’s say they wanted to support bonds, or “fixed income,” in the US. They’d have to integrate with the DTCC’s FICC system (Fixed Income Clearing Corporation), Fedwire, TradeWeb, and the fixed income exchanges, among other systems. Internally, they’d need to update their systems to account for securities that don’t trade like equities and come with their own valuation math. I still get nightmares from reading Frank Fabozzi’s The Handbook of Fixed Income Securities early in my career. Clear Street essentially has to incorporate the bond math from that 1840 page tome into its internal systems in order to properly account for risk.

And then there are options (hello OCC!) and futures and all sorts of exotic derivatives, some of which trade on exchanges and many of which trade over-the-counter (OTC) in bespoke deals. Those need to be reflected in the system, too, if Clear Street is to maintain a clear picture of its clients’ risk.

And if you want to add new geographies? Well, then you need to rebuild all of these integrations with the equivalent agencies and exchanges in each country you plan to service, each of which have their own regulations and idiosyncrasies. Some of these countries’ systems run on COBOL; others are more modern and run on Java and SQL. Whatever language they speak, you must too.

No one gives you bonus points for managing all of this extra complexity; they just expect it to work, to show up as a set of clear numbers that clients can use to trade and manage their own risk.

It’s no wonder that banks have no desire to rebuild all of this; if it works well enough, the distant-seeming threat of catastrophe pales in comparison to the clear and present schlep of having to redo all of that.

Simply put: Clear Street itself builds modern software, but that software has to speak to legacy technology in whichever way partners and clients require.

“The DTCC (Depository Trust & Clearing Corporation) isn’t going to change their protocols for us,” Jon explained. “We need to adapt to the way they like to speak. Then clients [like hedge funds] also have their own ways of speaking that you need to adapt to. Our clients say ‘This is how we talk,’ and if we want to do business with them, we need to learn to talk that way.”

I have some personal experience here. At Breather, some of the buildings we were in used building access systems like Kastle that ran on old software. To give our customers access to their spaces in those buildings, we had to get them past security, which meant getting their names in the security system. Which meant we had to integrate with the building access systems.

Something so seemingly simple turned out to be brutal. Integration with each new system took months of our developers’ time, and whichever backend developers were unlucky enough to be put on those projects absolutely hated it. And that was just to get some names in a database.

Multiplying that by hundreds of systems and adding the zero-room-for-error nature of handling money is a mind-numbingly complex and painful challenge to contemplate.

But if Clear Street wants to replace the world’s financial infrastructure with modern software, that’s where they have to start. Because the world’s financial infrastructure runs on COBOL, the people who know how to build on COBOL are getting old, and the banks aren’t incentivized to fix the problem themselves.

COBOL Cowgirl, Cowboys, and Cow-Paced Banks

There are two themes that we should unpack a little further before continuing the Clear Street tale.

First, we need to understand COBOL, the brilliant and long-lived software that still underpins so many of our systems, why it is that pretty much only 70-year-olds like Neil Stepanich know how to fix it, and what kind of risk that represents.

Then, we need to dive deeper into the incentives that keep the banks on their cobbled-together COBOL despite the risks.

COBOL Cowgirl and Cowboys

Even the people betting their career on replacing COBOL are in awe of it.

When I asked what he thought about the language, Jon Daplyn warned me that he was about to recite me a love letter to COBOL.

“If you think about it,” he said, “Someone wrote a piece of software decades ago that’s still working today. That’s remarkable.”

COBOL is truly remarkable.

In the 1940s and 1950s, computer scientists had to speak the language of machines, which they did at first by setting switches and plugging and unplugging cables…

Or by feeding punch cards with data and code into machines and getting punch cards with results back out…

Grace Hopper, a lieutenant junior grade in the US Navy, first worked on such a machine in 1944, when she was assigned to work with Howard Aiken’s Bureau of Ordinance Computation Project at Harvard University to work on the Mark II, the successor of the computer in the image above. Five years later, in 1949, she joined the Eckert-Mauchly Computer Corporation as a senior mathematician to work on the UNIVAC I, which would become America’s first commercially available electronic computer.

While working with UNIVAC, Hopper realized that the way humans programmed machines – not just speaking their language, but speaking a different language for each machine – could be improved. She thought that humans should be able to speak English to machines, or more specifically, to use English-like syntax to program computers.

Hopper “was told very quickly that I couldn’t do this because computers didn’t understand English. Nobody believed computers could understand anything but arithmetic.” She disagreed, or rather, she recognized that for computers to understand English, they’d need a translator.

In 1952, Hopper and her team created the first compiler, a program that translates high-level programming language code into machine language code that a computer's processor can execute. Then she developed one of the first English-syntax programming languages, FLOW-MATIC, specifically to program the UNIVAC, in 1955.

While Hopper was developing better ways to speak to computers, others were designing better computers themselves. In addition to the UNIVAC, IBM built its 700/7000 Series, Digital Equipment Corporation (DEC) released the PDP-1, and National Cash Register (NCR) offered the NCR 315.

Recognizing the need for software that worked across all of the various hardware systems, a committee formed by the Department of Defense and the private sector proposed the idea for a common business language. In 1959, it established the Conference on Data Systems Languages (CODASYL) to develop that language.

Hopper was on the committee. Drawing on her work, CODASYL proposed a readable, English-like language that could be adopted by businesses for data processing tasks. In 1960, it completed the first version of the Common Business-Oriented Language, or COBOL.

COBOL was a hit. It worked on mainframes from IBM, UNIVAC, Honeywell, Burroughs, and Control Data Corporation (CDC), each of which provided its own compiler to translate the machine-independent COBOL into machine code specific to their machines.

IBM’s System/360, which I wrote about in Internet Computers and which IBM developed for $48 billion in today’s dollars, took the business world by storm. As Computerworld’s Frank Hayes explained, “Hardware compatibility meant platform stability. That led to application longevity, which made complexity possible. A whole new world opened up for IT, a world of huge, business-changing megaprojects.”

Many of those business-changing megaprojects took place inside of large banks, programmed in COBOL.

In Internet Computers, that’s where I left the mainframe era and moved on to the Next Big Thing: personal computers. The banks, however, and many other large institutions, from insurance companies to government agencies, never left.

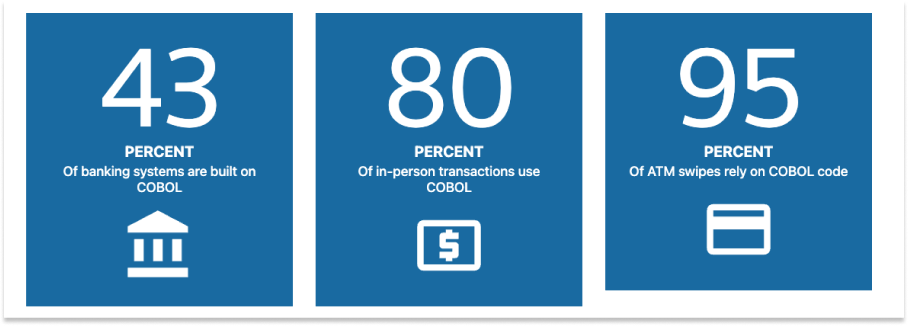

More than 60 years later, 44 of the top 50 banks and all 10 of the largest insurers, are still using mainframes programmed in COBOL.

That, as Jon said, is remarkable, and deserving of a love letter.

COBOL is reliable and efficient. Its fixed-format syntax optimizes code generation. “Rigorous syntax and error-checking capabilities have helped COBOL programs withstand multiple updates and adaptations without endangering system integrity and run relentlessly for decades.” Did a mainframe engineering services firm write that? Yes. But it seems to be true. COBOL programs are as Lindy as computer programs get.

But there are a couple of challenges with continuing to rely on COBOL.

The first is a straightforward one: we’ve developed much better ways to write and run software. No one starting from scratch builds on COBOL.

The second is the bigger risk: the people who know how to work with COBOL are leaving the workforce.

When I wrote about Hadrian, I wrote about a huge problem facing the precision manufacturing industry: the average machinist is in their mid-50s, the average precision parts shop owner is in their 60s, and the younger generation isn’t joining the business.

The same thing is happening here. The average COBOL programmer is in their 40s or 50s, and the younger generation isn’t backfilling them.

It’s no wonder. One Hacker News commenter compared learning COBOL to “swallowing a barbed cube shaped pill,” but cheerfully pointed out that that’s not the hard part.

Even worse, the ones who really know how things work, like Neil Stepanich, are even older and no longer in the workforce. Reuters begins a great 2017 piece on the “COBOL Cowboys” by writing, “Bill Hinshaw is not a typical 75-year-old. He divides his time between his family – he has 32 grandchildren and great-grandchildren – and helping U.S. companies avert crippling computer meltdowns.”

Hinshaw and his wife founded a company called COBOL Cowboys, named after the movie Space Cowboys in which retired Air Force pilots are brought in to troubleshoot a problem in space that only they know how to solve.

The challenge, according to Hinshaw, is even though some young people still learn COBOL, there are some things you just can’t teach: “COBOL-based systems vary widely and original programmers rarely wrote handbooks, making trouble-shooting difficult for others.”

Only people who were there when the systems were built know how it all fits together, and worse, that dwindling group of people won’t be around forever.

Accenture’s Andrew Starrs put it bluntly. The risk is “not so much that an individual may have retired," he says, but that "he may have expired, so there is no option to get him or her to come back."

What happens when the COBOL Cowboys ride into that eternal sunset?

There will be no one left who knows how the infrastructure on which trillions of dollars daily all fits together, no one to fix it when its inevitable crumble accelerates. COBOL is incredibly impressive infrastructure, but even the best infrastructure is no match for time.

So why aren’t the banks getting ahead of the problem and doing whatever they can to avoid catastrophic risk?

Cow-Paced Banks

The short answer is that replacing the COBOL-based systems while the bank runs on them is slow, expensive, and introduces short-term risks.

Chris Pento, Clear Street’s CEO and co-founder, has spent his career in operations at financial institutions, from large established investment banks like Merrill Lynch to startup broker dealers like Exos Financial. If anyone feels the brunt of bad systems, it’s the operations people who are responsible for cleaning up their mess every day.

I asked Chris why a big bank couldn’t just throw a bunch of money at the problem. He told me they probably could build new systems, before listing off a litany of reasons they wouldn’t:

Building the system while running a company with diverse needs – including keeping clients happy on a daily basis – adds complexity

Technical debt has built up in these systems over 30 to 40 years as people patch problems

There’s all these connection points – internally and with external systems – that have to be unconnected and reconnected, “and it takes five years just to figure out what the connections are.”

Then, midway through the process, someone on the risk team says, “Hey, you forgot about this” and shuts the project down.

“You drive on the BQE (Brooklyn-Queens Expressway),” he said. “You know how bad decade-long projects can get.”

The complexity and time to build it is hard and long, fraught with risk. Recall the patchwork of integrations we talked about earlier, integrations with the DTCC, OCC, exchanges, and regulators, in countries around the world and on a variety of computer systems. Like a game of Operation, touching any one of them the wrong way might mean game over, so you have to go very slowly and very carefully, all while protecting the core.

Jon Daplyn, who was responsible for these systems at Morgan Stanley, echoed Chris’ assessment and added a technical lens. To Jon, the issue is that, while the banks have tried to improve their systems, they’ve only gotten so far because they’re afraid to touch the core and break the whole thing.

What you’d have to do is take a small piece of functionality from the core, pull it out and rebuild it, and then bridge it back in until the core gets smaller and smaller. Thousands of people have been building and patching and patching, never really changing the core because they’re too scared. Pulling it apart will take decades of consistent effort.

Decades may as well be millennia from the perspective of the people running the banks today: they would need to foot the bill under their watch for a payoff that might come long after they’ve sailed into retirement. So they take the hidden but pernicious risk that comes with inaction.

What Happens When the Infrastructure Breaks?

The big risk in the old system is that the different people who need to see the same data, don’t.

Do you have a single source of truth? Is there one place where your firm calculates the value of an option or many? Do your finance team, risk team, and the client all see the same values or do they see different values? Do they see the same thing eventually, or in real-time?

Sometimes, bad infrastructure shows up as potholes. Slower transactions, extra work for the back office, miscalculated fees like Uri dealt with. Annoying and inefficient, but not the end of the world.

Other times, it rears its head in the financial equivalent of a bridge collapsing with drivers on it.

Like when Archegos Capital Management blew up and took Credit Suisse down with it.

Remember this one?

In March 2021, ViacomCBS sold some stock and its stock tanked. That was bad news for Archegos, Bill Hwang’s $10 billion family office, which was turbo long swaps on ViacomCBS and a number of other tech stocks on margin extended by the fund’s prime brokers. As the prices fell, the prime brokers demanded more collateral.

When Archegos failed to meet its margin call, its prime brokers – including Credit Suisse, Nomura, Goldman Sachs, and Morgan Stanley, among others – raced to sell off Archegos’ collateral and recoup their money, crushing the prices of the assets they all held.

Archegos collapsed, of course, and it brought some, but not all, of its prime brokers with it. As The Trade News reported, speed made all the difference. And speed depended on risk management systems.

When Archegos blew up, Goldman had the intel within seconds, Morgan Stanley hesitated but sold on the same day, and Credit Suisse, which was still on antiquated risk management systems, waited days to catastrophic effect.

Goldman was the first to sell. Over the course of the day on March 26th, “Goldman Sachs sold $10 billion of shares in stocks linked to Archegos.”

“We have robust risk management that governs the amount of financing we provide for these types of portfolios,” said David Solomon, CEO of Goldman Sachs, on the bank’s first quarter 2021 earnings call. “We identified the risk early and took prompt action consistent with the terms of our contract with the client.”

Morgan Stanley was almost as quick, dumping $8 billion that same day. The firm lost $911 million between money owed by Archegos and trading losses. A mere scratch.

Nomura wasn’t as lucky. It lost $2.87 billion in the winddown.

But the biggest loser was Credit Suisse. The Swiss bank was the slowest to appreciate and unwind its exposure to Archegos, and lost a nauseating $5.5 billion. It had to raise $1.9 billion to stay afloat, and fired both its investment bank CEO Brian Chin and, tellingly, its Chief Risk and Compliance Officer, Lara Werner.

It wasn’t enough. Two years later, in March 2023, the Swiss Government and Swiss Financial Market Supervisory Authority organized the $3.2 billion fire sale of Credit Suisse to its Swiss Rival, UBS.

“Credit Suisse would be here today,” Uri told me, “if they’d had the right tech in place.”

Or take Signature Bank.

The same month that UBS acquired Credit Suisse, March 2023, Signature Bank faced a bank run as depositors raced to withdraw their funds on the heels of the collapse of Silicon Valley Bank.

As the FDIC went to work to assess the damage, they asked all of the at-risk banks for tallies of the wires they had going out.

Signature Bank said, essentially, “We’re actually not sure because of our systems.”

The FDIC said, essentially, “Are you kidding me?” and told the New York State Department of Financial Services to take possession of the bank that Sunday.

The bank’s exposure to crypto was blamed in the press, but as the FDIC wrote in its report, “SBNY management was sometimes slow to respond to FDIC’s supervisory concerns and did not prioritize appropriate risk management practices and internal controls. Management was described by FDIC supervisors as reactive, rather than proactive, in addressing bank risks and supervisory concerns.”

The real challenge that affected these firms is a lack of clean data.

At the surface level, that sounds like a silly and trivial-to-fix problem given the stakes. But as we’ve learned, for international firms that handle every asset class, getting clean data means integrating hundreds of systems, all which speak different languages, into one central database that can translate all of that disparate data into clear metrics as fast as digitally possible. When that database is built in a 70-year-old programming language that few people alive truly understand, and when it needs to translate from exchanges, clearing houses, and clients that each speak their own language, the problem becomes prohibitively complex.

Little inconsistencies compound on each other, and as they do, the risks compound, too, until… KABOOM.

These are the kind of risks that Uri thinks are going to come due more and more frequently if the infrastructure isn’t fixed from the core out.

Fixing the infrastructure from the inside – rebuilding the roads while people are driving on them – doesn’t seem to be an option. If it were, Clear Street wouldn’t exist.

Rebuilding the infrastructure from the ground up is hard, but it might actually be the easiest way to make sure it happens. That’s Clear Street’s bet.

What Clear Street is Building

A long time horizon is a competitive advantage, one that requires capital, vision, and the right blend of patience and momentum.

When I wrote about Anduril, I said that it was in a goldilocks position when it came to acquiring advanced technology companies: “it’s well-funded enough that it can make meaningful acquisitions, but privately held enough that it doesn’t need to justify its investments in the same way public companies do.”

Clear Street sits in its own goldilocks zone: it’s well-funded and experienced enough that it can build new infrastructure with the patience it requires, but fresh enough that it’s not constrained by the same demands and risks as the banks.

Clear Street’s mission is to build a modern, single source-of-truth platform capable of handling every asset class, in every investor, and in any currency.

But that’s not something you can build from day one. Uri started the company to solve his own pain point, but even he doesn’t do most of his trading on Clear Street yet.

“Alpine is 95% at other clearing firms,” he readily admitted.

The goal is, over time, to win more and more of Alpine’s business, and by extension, to be able to serve an increasing share of other firms’ trading business, from the very small to the very big.

That means building bulletproof core infrastructure, and then racing to build new products to handle more assets in more geographies on top of the infrastructure.

So what’s in the core?

“Clearing, settlement, and the bookkeeping ledger,” Jon told me, “Those are the things that we’ll protect completely.”

Trading a security like a stock or bond seems simple. You just hit a button in Robinhood, and voila! But there’s a lot that goes on behind the scenes to make the trade happen, which can be broken into three steps for simplicity:

Execution. Someone wants to sell at a certain price, someone else wants to buy at that price. They’re matched through an order book (or automated market maker in crypto). The price is locked in. This is the front-end, what you see when you trade.

Clearing. After the trade is executed, the details are verified and the obligations of both parties – one makes a payment, the other delivers securities – are established.

Settlement. Finally, the securities and money trade hands. How and when that happens depends on the type of securities traded and the markets they trade in. Stock markets are typically “T+2,” meaning that they settle two days after execution.

If you’ve ever bought or sold a stock before, you know that you don’t need to meet the person on the other side of the trade somewhere, hand them cash, and receive a stock certificate. The role of clearing and settlement software is to orchestrate everything that needs to happen behind the scenes, including interacting with all of the intermediaries that touch a transaction, like the DTCC.

For a much deeper read on how it all works, check out this classic thread Compound248 wrote in the middle of GameStop mania:

For our purposes, what you need to know is that the core of Clear Street’s software, the stuff they’ll protect completely, is the infrastructure that handles all of that behind the scenes work and keeps track of who owns and owes what. It also handles custody, holding securities and money for clients.

Sachin Kumar, Clear Street’s CTO, explained that it’s really all about data management and workflows.

At this point, most assets exist and move as bits of data. Execution, he said, is relatively simple: sending an order to buy 100 shares of Apple at a certain price changes fewer than 10 fields in a database. But the post-trade side – clearing, settlement, and custody, which he calls the “critical path” – is more complex: 30-50 fields, each of which has a different meaning, each of which drives business rules, and each of which has compliance, risk, and regulatory implications.

He sees Clear Street’s role as bringing modernity to the critical path.

Instead of COBOL databases on mainframes, Clear Street has a proper, modern Snowflake data lake with different layers with increasing fidelity.

Instead of direct access to a messy database, Clear Street offers APIs its clients can use, and recently introduced Clear Street Studio to provide a client-facing user interface.

What makes Clear Street’s software so hard to build is that it needs to deliver modern APIs and interfaces to bulletproof data to clients that abstracts away all of the complexity of integrating with antiquated software like the DTCC’s in the background as table stakes. Then it needs to do a million other things that clients demand across a growing number of asset classes and geographies with the same zero-fault-tolerance.

It’s a perfect example of what I described in APIs All the Way Down:

That leads to one of the most important things to realize about API-first companies: they’re a lot more than just software… The magic of companies like Stripe and Twilio is that in addition to elegant software, they do the schlep work in the real world that other people don’t want to do. Stripe does software plus compliance, regulatory, risk, and bank partnerships. Twilio does software plus carrier and telco deals across the world, deliverability optimization, and unification of all customer communication touchpoints.

Clear Street does software plus compliance, regulatory, risk, custody, and all of the things prime brokerage clients expect, and delivers it via clean APIs.

“While we’re building infrastructure,” Uri said, “We have to remember that it’s the products we offer that will actually drive demand.” Things like:

Better access to capital and financing

Better stock loan to borrow

More margin, cross margining and enhanced leverage

“Products – more and more integrated products”

As one example of the products modern infrastructure can support, Clear Street can build products on its single source of truth, real-time data that take advantage of pre-trade analytics, predictive risk modeling, and intelligence instead of reactive products that wait for the data to catch up.

Studio has a “Shocks View” that lets clients see what would happen to their portfolio and margin requirements if asset prices swung violently up or down. It also has built-in risk simulations that let clients ask “What would happen if I put this trade on?” both to the existing portfolio and in the case of shocks. Currently, to do this, traders pick up the phone and ask their risk team what the impact might be. In a field in which milliseconds can make a difference, the speed advantage from replacing phone calls with software can be enormous.

As another, moving everything onto one real-time cloud software platform means that Clear Street can provide more bespoke margin, lending, and financing packages that respond in real-time to clients’ portfolios.

Because Clear Street is building API-first, third parties can build products that inherit these advantages on top of its infrastructure and/or Clear Street can offer those products itself.

For now, many of those products are assets. Clear Street started by offering just US equities. Then it added options, fixed income, and swaps. Now, it’s scaling out the swaps business and building a futures business.

In July, it acquired React, the maker of cloud-native futures clearing platform BASIS, and it recently applied for Futures Commission Merchant (FCM) membership. It’s the kind of acquisition a company can make when it’s well-capitalized enough to be acquisitive but small and technologically clean enough to integrate new products smoothly.

Then, it needs to bring those products to major markets around the globe, each of which has its own regulations and its own antiquated systems with which to integrate. My head hurts.

Oh, and it launched an investment banking business.

Andy Volz, Clear Street’s COO and Head of Prime Sales, is responsible for bringing in hedge fund clients. And he said that a big part of that – of getting hedge funds and other institutional clients to try and trust the technology Clear Street has built in the first place – is offering them the services that investment banks offer.

“These are discerning customers, and it’s hard to get them to trust you,” Andy said. “Clients traditionally come in in one of a few ways: research, corporate access, capital introductions, balance sheet. We didn’t have that stuff, and now we do.”

And even with all of that stuff, winning prime brokerage clients still requires a sales team with the right relationships. Some know a few big clients really well, others cover 200 smaller clients. Clear Street started with that group, targeting the hedge funds that the big banks don’t focus on.

With Studio, a self-serve product, they can open up the top-of-funnel even further to capture the long-tail of the roughly 6,000-8,000 hedge funds in their addressable market.

Software, services, and sales. Winning a foothold in prime brokerage requires all three. And from that foothold, Clear Street can expand its share of wallet as it adds new products in new geographies that those same clients, and new ones, want to use.

Eventually, the goal is to serve all types of clients – from the day-trader to the largest multi-strategy hedge funds like Alpine – across all of their needs. It’s better for Clear Street, obviously, but they believe that it’s also better for those clients from a risk, financing, and speed perspective.

As Uri described the flywheel, “More products, more exponential value in terms of capital efficiency and cross-margining, all on one database is very powerful.”

That flywheel is just beginning to spin in the grand scheme of things – Uri still has 95% of his activity with other prime brokers – but the traction to date has been impressive.

Business Model, Traction, and Moats

Aside from the quest to de-risk the financial system by improving its infrastructure, there’s an important business model reason to build modern financial software from the ground up.

More efficient software makes it cheaper to serve each client, which means that Clear Street can serve clients that the largest prime brokerages can’t profitably serve.

Owning the full-stack means that it can capture more value, and offer better financing and cheaper software, than electronic brokerages without their own infrastructure like InteractiveBrokers profitably can.

Building the best clearing, settlement, and custody infrastructure for the most products in the most geographies, and delivering it all via APIs, means that it can power more fintech apps more affordably and more safely than companies like Apex Clearing or Alpaca can.

Clear Street makes money by facilitating and financing trades. It can make transaction fees on trades and earn a spread on products like margin and securities lending.

Everything it builds is in service of increasing the volume of transactions taking place on top of its infrastructure and minimizing the risk, to itself and to its clients, of those transactions.

It’s incentivized to lower the barriers to using Clear Street – whether by giving smaller clients software for free or providing larger clients with investment banking services – so that it can earn fees on a growing volume of transactions. And because of the higher fixed CapEx it spent to rebuild the infrastructure, it can capture higher margins than a competitor using legacy systems, more humans, or more third-party services.

It seems to be working, although it’s early.

Clear Street is currently clearing 3% of the US equity market daily - $13 billion in volume.

Across roughly 1,500 clients ranging from active individual traders to hedge funds to market makers, they support over $30 billion in revenue producing balances.

In 2023, Clear Street generated $260 million in revenue, and most impressively, they did it profitably, earning positive EBITDA margins.

Now, the name of the game is to expand into more products and more geographies in order to serve more customers and grow the share of current customers’ transactions.

The opportunity if they do is massive.

Clear Street is currently valued at $2.2 billion. Broadridge, an ADP spinout that offers clearing technology built on top of the old infrastructure, has a $23.7 billion market cap. Interactive Brokers has an astonishingly large $41 billion market cap. Goldman, which does many things besides prime brokerage so isn’t a clean comp, is valued at $126.5 billion.

If Clear Street succeeds, it has the opportunity to win clients, and market cap, from each of them, and do so in a truly defensible way.

Infrastructure is incredibly hard to build, but the reason that certain entrepreneurs are drawn to building it nonetheless is that if they pull it off, it’s incredibly defensible. Specifically, using Hamilton Helmer’s 7 Powers as a framework, infrastructure has high switching costs. Once a customer has built their products and systems on top of your infrastructure, it’s expensive and even risky for them to switch to another system.

It cuts both ways. High switching costs are why banks still use the same 70-year-old infrastructure despite the risks and bottlenecks to growth it prevents! Incumbents’ switching cost moats work against new entrants until the new entrant is able to cross the moat and put the same switching costs to work for itself.

Overcoming incumbents’ switching costs is why Clear Street isn’t just building infrastructure, but also products that run on top of it.

Buying a brokerage to prove the advantages of operating on Clear Street’s infrastructure is one way to show clients that the switch is worth the cost. Products like Studio, which offers a powerful and intuitive UX made possible by better infrastructure, is another. Opening up access to the infrastructure with modern APIs that have good developer ergonomics is a third. And providing the full suite of prime brokerage services, for a certain client group, is a fourth.

The bet that Clear Street seems to be making is that if it provides as many easy on-ramps to its infrastructure, for clients as small as a single developer building a new trading platform to a large hedge fund that requires white glove service, it will be able to retain and grow their business over time.

Clear Street has strong traction, a business model that allows it to capture its fair share of the value it creates, and features that should make the business defensible as it grows. That said, there are risks. Uri is the first to call them out.

Risks to Clear Street

Uri thinks in risk, so I asked him what the biggest risks to Clear Street are. He rattled them off.

“There’s risk at so many levels. There’s a risk if we don’t hire the best people, there’s execution risk, there’s risk in how we manage our clients’ risk because we lend them money, there’s compliance risk.”

Those are the obvious risks, the ones that anyone would think of when analyzing Clear Street.

And then there’s the risk of not leaning into the momentum.

I hadn’t thought of this category of risk before. I’ve written about the advantages of taking the longest view in the room over and over without thinking about this particular challenge that comes with it. In my piece on Stripe, I included a great quote from its CEO Patrick Collison:

The way in which Jeff Bezos has been persistently and continually able to use time horizons as a competitive advantage is something I have deep respect for. There’s something quite deep about the notion of using time horizons as a competitive advantage, in that you’re simply willing to wait longer than other people and you have an organization that is thusly oriented.

What I failed to appreciate is that maintaining momentum over long time horizons is really hard. I think that’s why Jeff Bezos also insisted that the company behave like “It’s always Day One.”

In Clear Street’s case, Uri said, “We have great momentum, great clients, great employees, a lot of buzz. But if you slow down too much, it gets boring, because it’s already taken 3-4 years to build, and it will take another 3-4, then another 3-4, and that becomes boring and stale over 10-15 years.”

More succinctly, he said: “Forward momentum and excitement is a big element of success. It’s hard to understand the risk of losing it because it’s not quantitative.”

More generally, Uri views his job as making sure that the company avoids the risks that don’t seem risky, but are.

Like relying on AWS alone, which he views as massive risks because of the impact on the off chance that it does.

“AWS can’t go down!” “But what if it does go down?” “Then it’s a real issue!” “So make sure we have a great backup for Amazon if it goes down.”

And then there’s the thing that I think might be the sneakiest risk to the business: the team.

Assembling a Team

In every conversation I’ve had with Uri, Chris and the Clear Street’s leaders, one thing that comes up over and over again is the importance of building the right team.

This is something that practically every founder will tell you: the team is the most important thing. But given what Clear Street is attempting to pull off, I think it’s particularly true, and particularly difficult, in this case.

In a nutshell, Clear Street needs to build a team of people with the drive and technical competence to both build modern software and integrate with legacy systems, and with the credibility and experience to sell to both individual traders and the world’s largest financial institutions, all while maintaining the right level of risk that they can maximize profits without blowing themselves up.

On the software side, Daplyn said that they hire “a combination of pure high-tech developers from Google, Meta, Amazon, etc… and others who are very good technically but also have deep subject matter expertise.” You need to find people who know how to build flexible, modern software, but who are also willing to do the tedious work of integrating with legacy systems, people who have experience working inside large financial institutions, who understand exactly what the customer needs, but people who are willing to work in a high-paced and hungry startup environment.

Sometimes, all of that exists within the same person; often, it comes from a mix of different people who you need to get to work together towards the same goal. When I asked Daplyn the secret for getting that kind of group to work together, his answer was simple: “Get people in a room. Part of this job is making sure that everyone is at the table sharing the right information.”

The even more daunting challenge is leadership hires.

Uri has not been shy about the fact that he wants to hire the very best and most experienced people, even if they’re the type of people who would typically never consider working at a startup, like the leaders of large financial institutions.

Culturally, I view this as one of the biggest risks to Clear Street. As a non-technical person who assumes that smart engineers can figure out the technical challenges, I view this as perhaps the biggest risk.

In a business like prime brokerage, one that works with large institutional clients and handles billions of dollars, hiring experienced people is necessary. But as anyone who’s worked in a startup that’s hired big names from big companies can tell you, that can often go horribly wrong. Nothing kills momentum like a bad executive hire.

So how do you counter that risk?

Specifically on the hiring side, you spend a lot of time upfront making sure that the big name hires are there for the right reasons and willing to get their hands dirty.

And even when you get it right for the given moment in the company’s life, Uri told me, you can always keep aiming for the best. That creates a unique culture, one where people have to be bought into the overall success of the mission as much as or even more than their own personal ambitions.

It seems to be working so far. The executives that I met at Clear Street all seemed to balance experience and tenacity, motivated to be there by decades of frustration of having to deal with shitty systems and an inability to change them within large bureaucracies.

They view Clear Street as their best opportunity to fix the thing that they’ve always wanted to fix, and understand that the company is going to bring in the best possible people to fix that thing.

Assembling a world class team pulling from startups and financial institutions is a major challenge, and getting them to work together productively is an even bigger one. It’s a risk that Uri acknowledges and is willing to take.

But it’s worth it, because there’s one risk to the system that we both see equally clearly: the risk of not innovating.

The Other Side of Risk

Crumbling infrastructure is bad because disaster can strike when it crumbles, but it’s also bad because it makes it difficult for people to experiment with building new things.

In Framing the Future of the Internet, I tried to capture the relationship between infrastructure and experimentation:

Good infrastructure enables experimentation; experimentation solidifies infrastructure.

In Clear Street’s case, most obviously, that means making it easier for anyone, anywhere to access the market, and even to run their own fund.

Jon Daplyn told me that one of the things that excited him about joining was the shared vision around creating a “hedge fund in a box– the full thing, not just servicing, but tools that allow them to run their own business, from pre-trade analytics and data all the way through to regulatory compliance reports front to back.”

It also means better and more innovative financial products.

One fintech founder I spoke to, who only let me quote him anonymously because his product is built on a competitor's clearing, said: “I would so prefer to be on Clear Street it’s not even funny.”

When I asked why, he said: “Better technology, way more reliable, way more control. Apex is just too antiquated, it’s like going back in time 20 years, and that across everything.”

(He hasn’t made the switch yet because Clear Street doesn’t yet offer an off-the-shelf way to create thousands of customer accounts – still Day One.)

There’s an apparent irony in me writing about a company building traditional financial infrastructure when I’m so interested in crypto, but the two worlds are beginning to come together, and that connection requires connective tissue.

In a recent interview, BlackRock CEO Larry Fink said, “We believe the next step forward will be the tokenization of financial assets.”

The company that’s furthest along in making that happen, our portfolio company Ondo Finance, works with Clear Street as its bridge into the traditional financial system. Clear Street clears, settles, and custodies the US Government securities that back Ondo’s USDY and OUSG (and soon OMMF) products.

Better infrastructure leads to more experimentation, and Clear Street is building better financial infrastructure.

The bet on Clear Street is that not only is better financial infrastructure a way to avoid the known risks, but a way to defend against the infinitely large risk of not innovating when the opportunity arises.

If AI is going to infuse itself into financial markets, it will need clean, real-time data to work with. Attempts to bolt AI onto COBOL-based systems will only accelerate the risk of collapse. And as global markets become more interconnected, as individual traders and large financial institutions trade products from around the globe, the value of a single source of truth for all of it becomes even more pronounced.

One of the criticisms of fintech products is that they put lipstick on a pig: they’re shiny interfaces on top of the same slow, antiquated systems the industry has relied on for decades. That’s not because fintech companies don’t want to build better products, but because the infrastructure is so entrenched – technically and regulatorily – that deep innovation has been hard to do.

Clear Street is tackling that difficulty head on. It’s rebuilding the infrastructure that underpins the traditional financial system as a parallel system that speaks the language of the traditional one until it becomes the system of record.

If it succeeds, it will have pulled off something that few companies ever have: replacing old, crumbling infrastructure with newer, stronger pipes on top of which everyone from the old guard to the new relies, lowering risk and raising the ceiling in the process.

Thanks to Uri, Ru, and the Clear Street team for working with me, and to Dan for editing!

That’s all for today! We’ll be back in your inbox on Friday with a Weekly Dose.

Thanks for reading,

Packy

Now when I'm using our enterprise software I feel like I'm going over a 60's era bridge. Thanks, I think?

Some "sponsored pieces" are not worth reading but this is not one of them!

I have a reasonable understanding of Cobol but didn't know anything about Clear Street.

I now have huge admiration for what they are achieving, the timeline is going to be long but this is going to be so worth it. Thank you for putting in the time to create this profile. Really appreciated.