Welcome to the 1,309 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 8,888 smart, curious folks by subscribing here!

We have a referral program! Share your unique link to win stickers, t-shirts, and fame!

Hi friends 👋,

Happy Monday! We’re bringing back an old favorite format today: Fantasy M&A!

Let’s get to it.

Acquisition in the Key of G Sharp

Back in 2013, when he was just starting Slack, WIRED asked Stewart Butterfield, “What’s your ambition?”

Stewart: (Straight Faced): “Be the next Microsoft.”

This essay is about how he can achieve that ambition.

Welcome to M&A Country

On Friday afternoon, the internet lit up with rumors that Microsoft might buy the most exciting company on the market: TikTok. It doesn’t seem like a natural fit. Microsoft is the 45-year-old purveyor of such office productivity mainstays as Word, PowerPoint, and Excel while TikTok is a short-form video app for Gen Z and Young Millennials.

The deal spent all weekend on-again-off-again after, on Friday night, President Trump suggested that the United States would ban TikTok altogether instead of allowing a sale to go through. His reasoning? “We are not an M&A country.”

With all due respect to the Art of the Deal author, mergers & acquisitions drive growth at many the nation’s largest companies and provide founders and employees the most capitalistic realization of the American Dream. The United States is very much an M&A country.

While Microsoft is distracted with the biggest acquisition in company history, Google should strike at its heart by making its own largest acquisition ever. I feel like I’m walking my daughter down the aisle right now, giving my baby away, but it’s for the best:

Google should buy Slack.

(Full Disclosure: I own shares and call options on Slack. It’s my biggest position.)

A Google/Slack combination — I call it G Sharp — bolsters both companies’ offerings in the productivity and collaboration battle against Microsoft today, and more importantly, sets the combined company up to own the future. Ultimately, the acquisition comes down to three main things:

Slack needs distribution and patient capital. Google can help.

Google needs growth outside of Search and a boost in the Cloud. Slack can help.

Slack fills the biggest hole in G Suite’s offering. Together, Google and Slack would own the work productivity and collaboration market for young companies, setting them up for Office-level dominance as those companies and their employees grow.

Plus, because Microsoft Office is so dominant, this deal likely wouldn’t trigger the regulatory scrutiny that comes with doing M&A as Google, Apple, Facebook, or Microsoft in 2020.

In this M&A country of ours, Microsoft and Google, with combined market caps of $2.5 trillion, are the biggest buyers. Each company aggressively spends income from its respective cash cow to bolster its offerings, diversify its revenue streams, and hunt for the next big growth engine, but each takes very different approaches to M&A.

Microsoft uses M&A to build a portfolio of standalone businesses that are profitable and growing today that might help bring in future Office 365 customers.

Among Microsoft’s biggest recent acquisitions are professional network LinkedIn for $26.2 billion, engineering network GitHub for $7.5 billion, and Mojang, the maker of the popular worldbuilding game Minecraft, for $2.5 billion.

As unnatural as it seems, a $40-50 billion TikTok acquisition fits within that strategy. Unlike a Facebook acquisition, TikTok won’t become TikTok by MICROSOFT. It will remain independent, drive meaningful growth for a company that brought in $143 billion in 2019, and potentially bring the cool kids over to Office at some point. The #excel hashtag is surprisingly popular on TikTok.

Google, on the other hand, uses M&A for two main things:

To bet on moonshots that have a small chance of becoming massively impactful and carrying the company after Search revenues fade away.

To pour fuel on the fire of its fastest-growing businesses.

Google’s moonshots, which it calls “Other Bets,” are so out there that the company restructured itself in 2015 to separate them from the core business, creating Alphabet as a holding company that owns Google and Other Bets. They’re fascinating for what they might become -- bets include life extension, self-driving cars, internet balloons, cities, and drone delivery -- but they’re even more fascinating for what they tell us about the way that Google thinks. They’re happy to lose $1 billion per quarter on Other Bets today for the chance to build tomorrow’s next big thing.

We’re not talking about Other Bets today, though. The Google/Slack deal is the other kind of M&A - it would pour fuel on the fire of Google’s fastest-growing business: Google Cloud.

The marriage of Google and Slack would create the most powerful kind of combination in tech: the best product and the best distribution into the most important customers.

The Battlefield: Product v. Distribution

There’s this debate in tech about which wins: product or distribution. Is it more important to have a) a great product or b) a great way to get your product in front of potential customers?

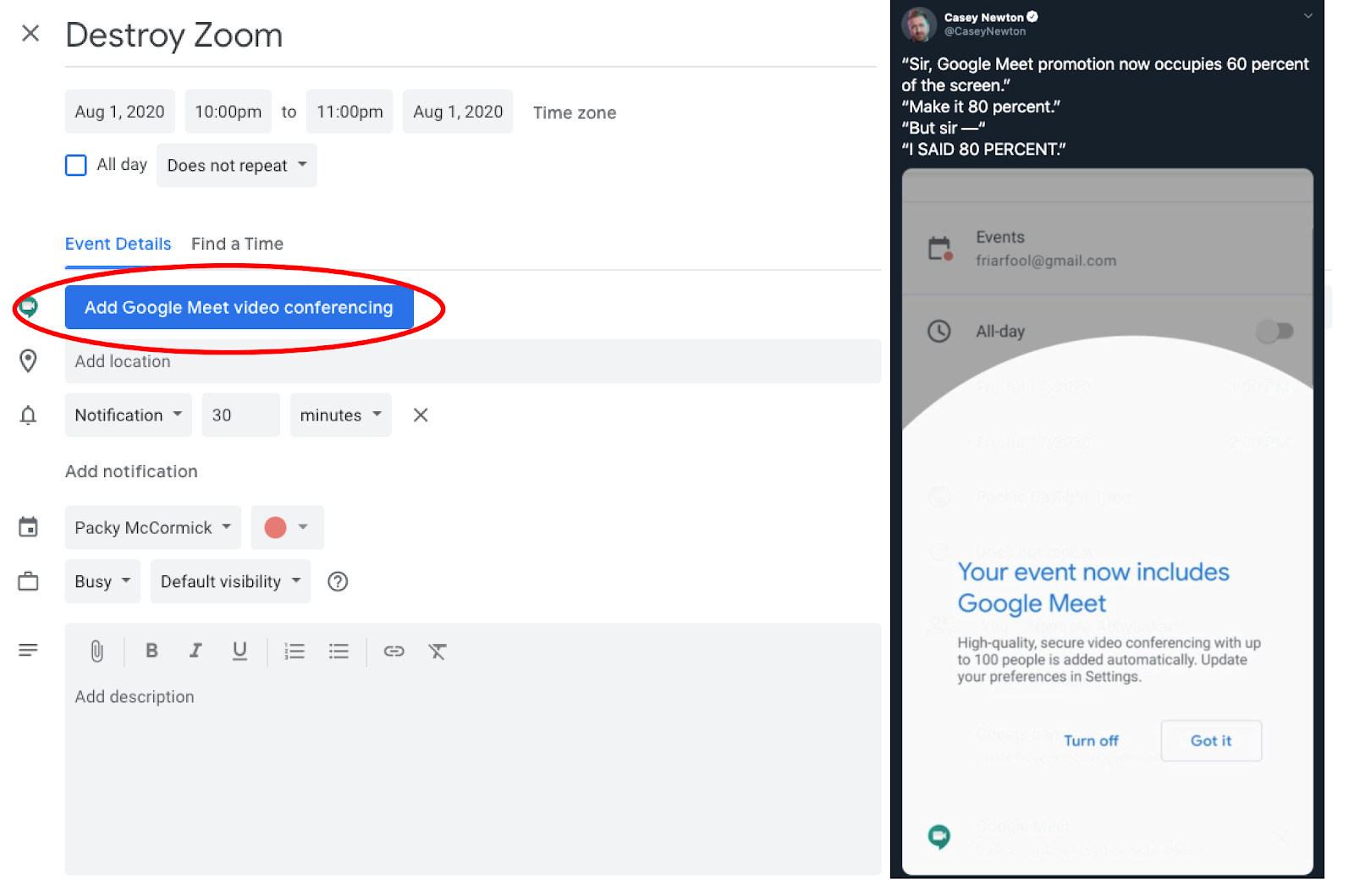

If you use Google Calendar, you’ve likely noticed this battle playing out on your screen.

Zoom, the video conferencing software, has exploded during the pandemic. Google, which has its own video conferencing, Meet, got jealous and fought back.

Google owns some of the most valuable real estate in tech -- people’s Calendars -- and it’s tired of Zoom using that real estate to direct people to its competitive product. In late April, Google also dropped the pricing hammer, making Google Meet free for everyone. Where Zoom limits people to 40 minute meetings on the free plan, Google gives them an hour, and it’s not even enforcing that limit until October.

Zoom has the better product, but it’s just so easy to schedule a Meet, and plus, it’s free. Anecdotally, distribution seems to be winning. I’ve gone from 90% Zooms / 10% Meets early in the Quarantine to 10% Zooms / 90% Meets over the past couple of months.

Zoom vs. Google is important, because it shows us that Google is willing to use its distribution might to win the office, and because it mirrors another battle happening for the enterprise -- Slack vs. Microsoft Teams.

Slack vs. Teams

Microsoft Teams is flexing its reach into Office users’ computers in an attempt to extinguish Slack’s growth. The market is reacting as if Microsoft’s plan is working, but look a little deeper and Teams looks more defensive than offensive.

Slack, launched in 2013, makes the best workplace communication product on the market -- fast, well-designed, playful, and open to thousands of integrations. While it has recently built out an enterprise sales team, much of its growth has come from bottoms-up adoption. A technical person in a company uses it in another context, brings it to the company to test on a small team for free, and then expand to the rest of the company and a paid account. That go-to-market strategy is predicated on building a product that people love enough to advocate for.

(For a deeper dive on Slack’s business model, see While Zoom Zooms, Slack Digs Moats.)

Microsoft, on the other hand, launched its competitor, Teams, in 2016, as the result of a reactive internal hackday, and it shows. The product seems like it was built with a simple mandate: give the over 1 billion people who use Microsoft Office or Windows something good enough, for free, that they never try Slack. It’s distribution over product.

More concretely, Microsoft installs and auto-starts Teams on existing Office users’ computers. Two weeks ago, Slack brought an antitrust complaint against Microsoft in the EU, claiming that “Microsoft has illegally tied its Teams product into its market-dominant Office productivity suite, force installing it for millions, blocking its removal, and hiding the true cost to enterprise customers.”

My wife, Puja, still uses a Windows laptop. Every time she turns on her computer, Teams starts up, even though she never installed it and doesn’t use it. It’s the PC equivalent of Google’s growing Meet button.

As a result of its aggressive intrusion, Teams has grown from zero to 75 million Daily Active Users (DAUs) in under four years. The last time Slack reported DAUs in September 2019, it had only 12 million.

But as Slack wrote in a blog post, Not all daily active users are created equal. Microsoft is myopically winning the battle and losing the war. It’s putting up big numbers right now by giving a free product to older buyers who don’t know any better.

That’s a major difference between Zoom vs. Google Meet and Slack vs. Microsoft Teams. With Meet, Google is actively competing against Zoom for the same customer, whereas Microsoft is just trying to keep its existing customers from switching to Slack. It won’t be able to steal existing Slack customers. As I wrote in the piece on Zoom vs. Slack:

Once a team has onboarded to Slack, it’s really hard to leave. As a company’s Slack usage approaches 100%, it becomes possible to replace e-mail, those awkward texts from your boss, and even meetings with Slack.

Since I wrote that piece, Slack introduced Slack Connect, which allows different organizations to collaborate and work together. The move potentially deepens its moat by building cross-organization network effects, eating away at email’s dominance, and becoming the central artery for professional collaboration and communication. As Ben Thompson wrote in The Slack Social Network:

Not only can you have multiple companies in one channel, you can also manage the flow of data between different organizations; to put it another way, while Microsoft is busy building an operating system in the cloud, Slack has decided to build the enterprise social network. Or, to put it in visual terms, Microsoft is a vertical company, and Slack has gone fully horizontal:

Microsoft’s positioning against Slack is defensive. It knows that there are better products out there, and that the closed Office ecosystem won’t win head-to-head product battles, so it’s trying to make sure its customers never even look elsewhere. Slack’s press release on the antitrust complaint gives the company’s (obviously biased) perspective on why Microsoft feels threatened enough by Slack to try to stop it with Teams:

“Slack threatens Microsoft’s hold on business email, the cornerstone of Office, which means Slack threatens Microsoft’s lock on enterprise software.”

“Slack ... is a gateway to innovative, best-in-class technology that competes with the rest of Microsoft’s stack and gives customers the freedom to build solutions that meet their needs. We want to be the 2% of your software budget that makes the other 98% more valuable; they want 100% of your budget every time.”

The way we collaborate and communicate at work is changing, becoming more entropic. Office is yesterday, Slack is tomorrow. Slack is built for the early adopters, tech employees, and young people who will become old, big budget-controlling people one day.

The Compounding Power of Young Users

On a long enough time horizon, Slack has already beaten Teams. It’s true for the same reason that I’m so bullish on Snap, and it’s a really important concept to understand broadly.

If you can acquire the youngest users, retain them as they get older, and continue to attract the new cohorts of young users, you will win over time. It’s the Compounding Power of Young Users.

Microsoft knows this. It’s how they got to where they are in the first place. When Excel came out in 1985, it wasn’t the 50-year-old Managing Directors using the product, it was the 22-year-old Analysts. As those Analysts became Excel whizzes, got promoted, switched companies, became Managing Directors themselves, and forced their own Analysts to use Excel, the product gained ubiquity. The same is true for Word, PowerPoint, Outlook, and even Windows. Start with the youngest users and grow with them as they age.

That’s why Microsoft acquired Minecraft and Github, and why they’re pursuing TikTok.

The market doesn’t fully grasp this concept, or isn’t patient enough to put its money behind it. It views the opportunity set as stagnant, when really, it’s dynamic.

Slack’s current customers are startups and small businesses full of young and tech savvy people. These people aren’t going to suddenly switch to Teams when they turn 50. Slack will become the new paradigm. Slack just needs to retain these people, keep them engaged, and continue to acquire every new startup and small business that pops up.

The market rightly yells at Slack to acquire enterprise customers, but it also misses the fact that it’s already acquired tomorrow’s enterprise customers.

This is why I’m bullish on Slack whether it gets acquired or not. As I wrote about, they’re built for steady growth and high retention.

The market wants what the market wants though, and Microsoft’s moves are putting a damper on Slack’s stock performance. While Zoom has popped 273% YTD, Slack has only grown 31%. The most oft-cited reason for Slack’s sluggishness is that investors are worried about Teams.

Slack needs two things in its fight against Microsoft:

More patient capital that understands The Compounding Power of Young Users.

Distribution power to win as many young users today as possible.

Google has both of those things.

G Sharp vs. Teams

Google and Slack (“G Sharp”) fit perfectly together.

They have the same target customer in the enterprise -- growing tech companies and small businesses -- Google just has more of them.

G Suite has 6 million paying customers, Slack has 122k.

Google has Chat, but it does not have a real workplace communications solution beyond Gmail.

Slack fills in G Suite’s major hole. Google owns the backbone of startup email, Gmail, and Slack owns the backbone of startup internal communications today and external communications tomorrow.

Google gives Slack immediate distribution and confidence that they’re not afraid to use it.

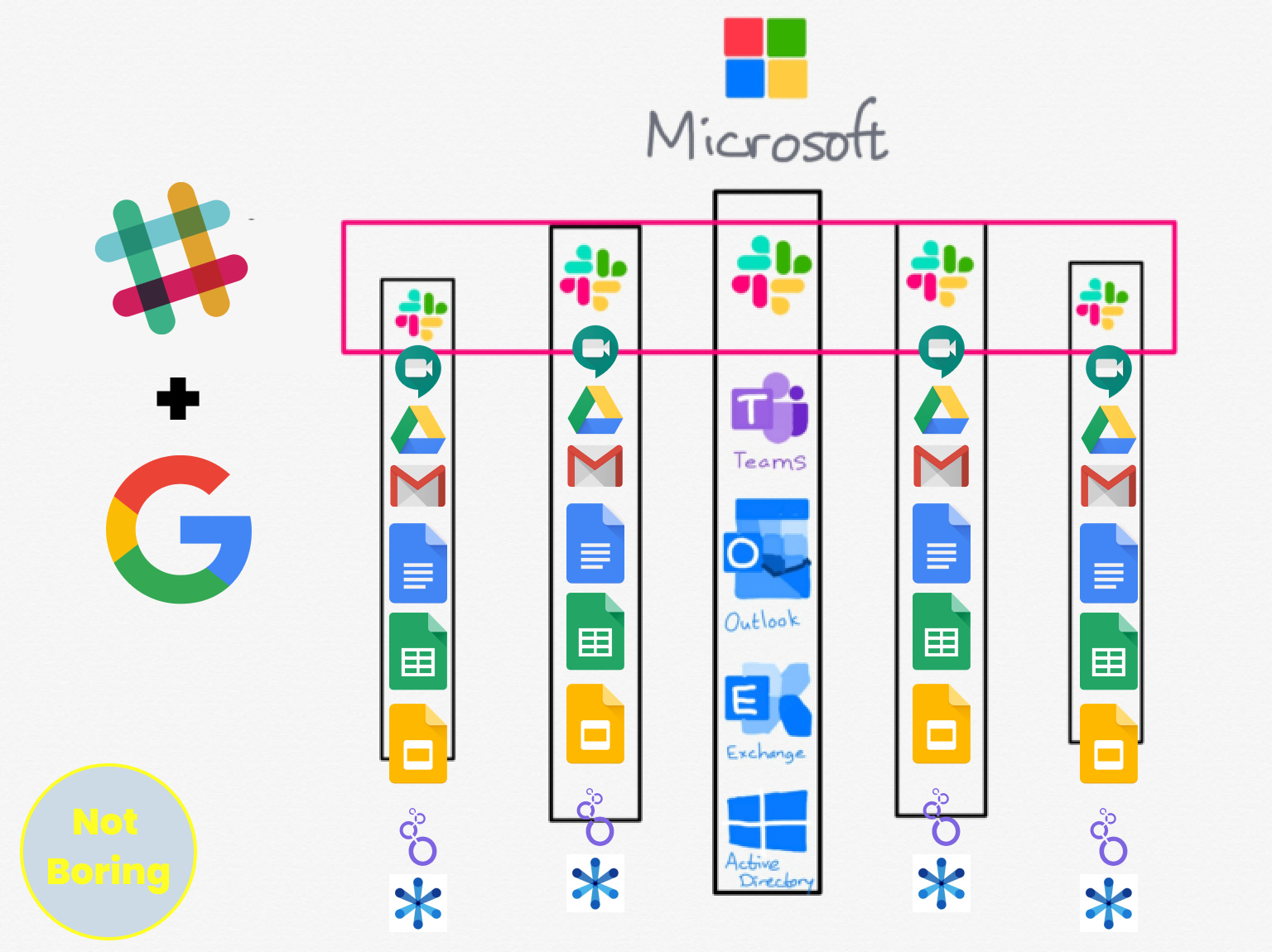

Bundling software and forcing it down users’ throats is what Microsoft does best, much to the chagrin of antitrust regulators. Together, Google and Slack can beat Microsoft at a modern, user-friendly version of its own game.

I’m no designer, but I mocked up one of many ideas for distributing Slack through Google:

In addition to reminding people to move conversations to Slack at every opportunity, Google can bundle Slack with G Suite. Overnight, Slack could nearly 50x the number of companies using the product, cutting off Teams and securing users that the company will grow with.

From Slack’s perspective, a Google acquisition would solve its major growth impediment and help it do what it does best - acquire and grow with young companies. But at a price tag of between $30-50 billion, would Google do it?

Google is the UAE

One way to think about Google is like a tech version of the United Arab Emirates. The UAE is ridiculously wealthy right now because of oil, but it knows the oil money won’t last forever, so it’s investing heavily in new growth opportunities like tech and tourism. Search revenue is Google’s oil - it’s making them rich right now, but one day, that well will dry up. The company is constantly on the lookout for the thing that will keep the growth alive after the Search revenue slows to a trickle. There are signs that we might be approaching Peak Search already.

Google never made less money in a quarter than it did in the same quarter the previous year… until Q2 2020. Google generated $38.3 billion in Q2 2020 revenue, down from $38.9 billion in Q2 2019. The biggest culprit? Search revenue, which dropped by nearly 10%.

Google Search is one of the greatest cash cows in history, and outside of the pandemic, it’s still growing. Over the past 10 years, Google ad revenue has grown at a 16.9% Compound Annual Growth Rate (CAGR). Growth did slow from 22% in 2018 to 16% in 2019, but for context, it grew ad revenue by more than Slack’s entire market cap in 2019.

It will be many years before the search ad well runs dry for Google. In the meantime, the company is investing its Search revenues in businesses that show the potential to grow faster than 17% per year and carry the company into the future. Using acquisitions to expand its capabilities within its best business segments is in Google’s DNA.

The history of Google is the history of an ingenious page ranking algorithm paired with a brilliant business model, some strong internal product development, and a whole lot of smart acquisitions.

Since 2001, the company has made 236 acquisitions, making it the second most acquisitive of the five largest tech companies, only six behind Microsoft, which had a 14 year head start. Alphabet CEO Sundar Pichai and Microsoft CEO Satya Nadella are such aggressive buyers, you could call them the… Indian Matchmakers. (I’m writing this with a Rakhi on my wrist, happy Raksha Bandhan!)

Google acquisitions have become some of the company’s most successful products, and among the most widely-used in the world.

Android (2005): Google bought Android for $50 million fifteen years ago. Today, Android runs 74% of the world’s smartphones.

YouTube (2006): Google bought YouTube for $1.65 billion, a number that people thought was crazy at the time. YouTube brought in $3.8 billion in revenue in Q2 alone.

DoubleClick (2008). Google acquired DoubleClick for $3.1 billion to build out its display advertising network. Network Member Properties, which DoubleClick helps power, did $4.7 billion in Q2 revenue.

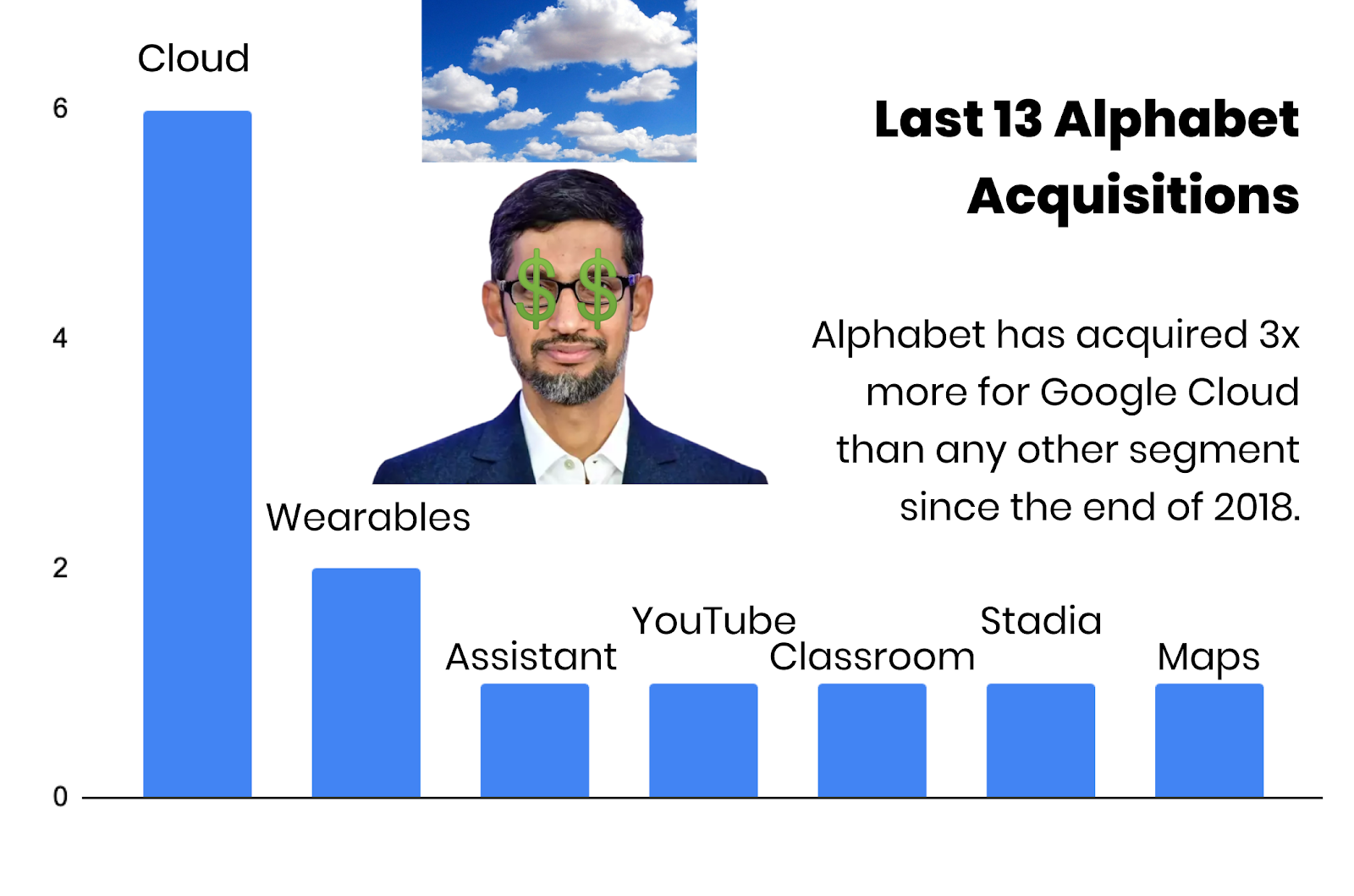

Software acquisitions are what Google does best, and these days, it’s turning its $121 billion acquisition cannon on software acquisitions in its fastest-growing segment: Google Cloud.

Growth in the Cloud

Google Cloud is the fastest-growing segment of Google’s business. While Google’s Search revenue fell, its Cloud business grew by 43% YoY, from $2.1 billion to $3 billion in the second quarter. Slack would immediately add nearly $1 billion in annual top line revenue to Cloud by rolling into the G Suite business segment.

Google Cloud is made up of two parts:

Google Cloud Platform (“GCP”) is Google’s cloud computing services product, like Amazon’s AWS or Microsoft’s Azure. GCP is for developers.

G Suite is the much catchier name for what the company used to call “Google Apps for Your Domain.” It’s a suite of collaboration and productivity apps, including Gmail, Meet, Chat, Calendar, Drive, Docs, Sheets, Slides, Forms, and Sites. G Suite is for businesses.

Google used acquisitions to build G Suite, a veritable Frankenstein of acquired technology:

XL2Web (2006) and DocVerse (2010) --> Sheets

XL2Web, DocVerse, and QuickOffice (2012) --> Docs

Tonic Systems (2007), DocVerse, and QuickOffice --> Slides

Under the leadership of former Oracle exec Thomas Kurian, Google Cloud is looking to get spendy to catch up to AWS and Azure. At an event in February 2019, Kurian said, “You will see us accelerate growth even faster than we have to date. You will see us competing much more aggressively as we go forward.”

Just four months later, Kurian made his first big move, acquiring analytics startup Looker for $2.6 billion to become part of the GCP offering. Looker is the crown jewel in a recent Google Cloud acquisition spree. Of Alphabet’s last thirteen acquisitions, six are for Google Cloud.

Google’s new focus is unsurprising. Like Greek gods, the tech giants are battling in the clouds, and for good reason. The market is huge -- Allied Market Research estimates that the cloud services market will reach $927 billion by 2027, nearly quadrupling from its current size of $265 billion -- and it requires such huge upfront investments to compete that only a handful can pay the entry fee.

Cloud is also the ultimate grow-with-your-clients space. As a result, the big three are doing everything they can to attract young clients -- free coworking, partnerships with incubators, prizes, and hundreds of thousands in free credits. These companies aren’t being altruistic. Once a company builds on one cloud or another, they’re likely sticking with that cloud for the rest of their lives.

Unlike Microsoft, which breaks out Intelligent Cloud and Productivity and Business Processes (where Office sits) into separate business units, Google houses G Suite and Google Cloud Platform together. Google realizes that both products are selling the same idea to the same people at the same companies.

The better G Suite is, the more compelling the offer is to the CTO, and the more likely it is that Google wins the business. Currently, G Suite offers a lot. The biggest hole in the entire offering is chat. That’s where Slack comes in.

G Sharp: The Modern Office Suite

Together, Google and Slack could finally build the Microsoft Office killer. It won’t be a quick death -- Microsoft is too ingrained in too many companies that are too slow-changing -- but within ten years, by growing with today’s most innovative companies, G Sharp will be the default workplace collaboration and productivity suite.

Today, many startups run their companies mainly on G Suite (although, notably, most still build their product on AWS):

Buy the domain from Google Domains

Set up the first firstname@company.com email address on Gmail

Schedule the first meetings on GCal

Start collaborating on their business plan in Docs.

Anxiously watch real-time users in Google Analytics.

Build out the first dashboards in Looker (technically GCP, not G Suite).

With so much in Google already, users make do with the products in G Suite that aren’t quite as good as competitors’.

Meet is good enough to preclude Zoom when it comes bundled, for free, with G Suite.

Sheets is good enough for everyone except for a few people on the finance and BI teams, for whom the company buys a couple of Office 365 licenses. (I genuinely love Excel and still use Sheets for most things, like the charts in this piece.)

Slides is good enough to make most presentations, and Keynote comes free on MacBooks anyway for the occasional external deck.

The one thing that’s missing is a channel-based messaging tool to serve as a hub for the company’s communications. Today, the first non-G Suite product that most startups sign up for is Slack.

If G Suite and Slack came bundled, there is almost zero need for a company to look beyond Google to get up and running. At that point, why not buy the upgraded bundle that gives you all of that for the price of Google Cloud Platform?

G Sharp would become what Microsoft Office was in the 80’s - the one-stop productivity and collaboration bundle. G Sharp would easily facilitate cross-company collaboration and productivity better than Office can. The combination is horizontal and vertical.

Slack Connect would serve as the cross-organization hub, and facilitate the usage of G Suite tools - shared Docs for partnership agreements, shared Looker dashboards to track progress, Rimeto directories for the teams to get to know each other, Meet for video conferences. Instead of each company having to buy Office 365 licenses to collaborate, they would either both already be on G Sharp or buy an all-inclusive G Sharp Connect package.

Additionally, Slack is an open platform that already works with 2,200+ apps. If there’s anything that a company needs to collaborate -- either internally or externally -- it’s all in one place.

Importantly, a Google/Slack combination would create a better user experience. As just one example, Google recently added an “Email” option within Google Docs. As email becomes less relevant, particularly for collaborative docs, wouldn’t it be nice to be able to share to Slack directly from inside the Doc?

It’s a little thing, but dozens of small improvements like it would add up to such a seamless user experience that it would be very hard for customers to leave.

Slack is the missing piece in G Suite’s efforts to overthrow Office, and a more complete G Suite + GCP bundle is Google’s best chance to steal cloud services market share from AWS. One acquisition gets Google closer to capturing two of the biggest prizes in tech.

Why Wouldn’t This Happen?

I’m getting excited about this deal happening already, but there are a few reasons it might not happen:

Slack is going to want a hefty price tag. In early June, before earnings, Slack’s market cap crossed $22 billion, and Slack bulls and insiders understand that as a sticky workplace collaboration SaaS business in an increasingly remote world, its best years are ahead of it. I don’t think Slack sells for less than $30-50 billion, which is 3-4x more than Google has ever paid for an acquisition.

Given that the prize is Microsoft’s $1.5 trillion market cap, I think Google will be able to get past the sticker shock.

Amazon might get there first. In June, Slack announced a partnership with Amazon in which Amazon will move hundreds of thousands of employees onto Slack and Slack will increase its usage of AWS and use Amazon’s Chime for voice and video. The move was seen as a way to team up against Microsoft Teams and potentially as the early stages of a courting process that could end in Amazon acquiring Slack.

The multi-year partnership might make a Google deal a little hairier, but Slack and Google are simply a better fit than Amazon because of Google’s distribution into Slack’s target customers and its existing G Suite product.

Stewart already resigned from a big search company once. After selling his photo-sharing company, Flickr, to Yahoo!, Butterfield resigned as soon as his four years were up with a memorable resignation letter highlighted in this 2014 profile. It’s hard to picture the billionaire once again selling to a big search company.

But that same profile contained the reason that Butterfield might roll Slack up into Google. The author, Mat Honan, wrote:

Stewart Butterfield is a Worldbuilder. Everything he’s said in that 2014 profile has come true so far, except for one thing: Slack isn’t yet 80’s-era Microsoft. But it can be, if it teams up with Google to take down today’s Microsoft.

This time, Stewart will be more than the Senior Director of Product Management he was at Yahoo! post-acquisition. With Google’s resources behind him, Stewart will be tasked with redefining the new, open, collaborative way we all work in a post-COVID world.

Big thanks to Puja & my brother Dan for editing this into shape. As a thanks, I’m shouting out his new company, Parade (he doesn’t know I’m doing this). If you’re in the market for women’s underwear, head over and show Dan your thanks - without him, this would have been painful!

We’re getting SO CLOSE to our 10k subscriber goal! If you enjoyed this post, I’d really appreciate it if you shared with your smartest, most curious friend.

Thanks for reading,

Packy