Spotify Calls Him Daddy

Or, Aggregators and Individuals Team Up to Take on Media

Welcome to the 276 (!!) new subscribers since last Monday’s e-mail! Thanks to everyone who shared, particularly Dan Teran, Patricia Mou, and Byrne Hobart 🙏🏻 If you’re reading this but you’re not subscribed, now’s the time to join our growing family of 1,502 Not Boring people.

Hi friends 👋🏻,

Happy Memorial Day! Memorial Day has always been my favorite holiday. At different times in my life, MDW has meant three glorious school-less months, lifeguarding, internships, ThrowGo rides, Avalon, friends, family, BBQ, beaches, parties.

This year is obviously different, but I’m no less excited. This is going to be a great summer. As we slowly start to add things back to our routines, we have the chance to design what our new normals will be with a near tabula rasa. Let’s make the most of it.

Speaking of making the most of it… Joe Rogan has made the most out of a podcast in the history of podcasting. (It’s a holiday, forgive me that transition, and let’s get to it.)

Spotify Calls Him Daddy

If listening’s more your thing, listen to the audio edition of this essay here.

On January 24, 1848, James Marshall found shiny metal in the ground of the lumber mill he was building for John Sutter. He brought the metal to Sutter, Sutter got it tested, and the test confirmed it. They had struck gold.

Last week, Joe Rogan struck gold, signing an exclusive deal to bring his podcast to Spotify. The exact terms aren’t public, but the consensus seems to be that Spotify will pay Rogan well over $100 million to license the back catalog and future episodes of his podcast, The Joe Rogan Experience.

My corner of the internet blew up with articles, hot takes, and armchair analysis on the deal. But there are three angles that I haven’t read yet that I want to explore today.

Podcasting Strikes Gold: Rogan and Call Her Daddy prove that there’s big money in the Passion Economy.

Barbelling of Media: Media profits will accrue to individuals and aggregators at the expense of the middlemen.

Spotify’s Strategy: The Rogan deal is another proof point that Spotify is backward integrating into supply to win podcasts and audio more generally; they’re just getting started.

Rogan’s deal signals that Passion Economy pursuits like podcasts, newsletters, and online courses, which have fallen somewhere between hobbies and small businesses, can create the kind of eye-popping outcomes typically reserved for athletes, musicians, and tech CEOs.

Today, talented individual creators with unique personalities can leverage new tools and social media distribution to build strong brands, cult followings, and large audiences. One person with a microphone is more suited to the modern media landscape than a legacy media business with a cost structure suited to the pre-internet age. Aggregators and individuals are skipping the middleman and working together to combine reach and niche.

Spotify, led by Worldbuilder Daniel Ek, understands this shift as well as anyone in the world. Ek is working directly with podcasting’s biggest personalities to grow Spotify’s non-music listenership and improve his company’s margins.

Because information is the easiest product to bring online, internet-driven changes impact media first. Understanding what Joe Rogan’s deal tells us about media gives you a crystal ball with which to predict the internet’s impact on every consumer-facing industry.

The Podcast Gold Rush

Joe Rogan’s deal is a major win for creators.

On the surface, this deal looks like just the latest in a long line of celebrities and athletes signing contracts worth more than the market caps of some public companies.

Actors, musicians, and even radio personalities regularly make more than Joe Rogan will through this deal. In 2005, Howard Stern made waves by signing a $500 million 5-year (plus equity grants!) deal with Sirius. Michael Jackson inked the largest record contract ever - $250 million - after he died. Every one of the 100 highest-paid American athletes has a contract worth more than $100 million. Floyd Mayweather reportedly earned $275 million for one 25-minute fight against Conor McGregor in 2017.

Tech IPOs put all of those numbers to shame. Even though Uber’s IPO fell far short of expectations, and it still created three billionaires - Travis Kalanick, Garrett Camp, and Ryan Graves.

In that context, Rogan’s deal seems … average. But we talking about podcasts.

Podcasts are still tiny. Two years ago, people were asking me, “You listen to podcasts, right? What’s a good podcast to listen to?” That’s like a 1995 person asking, “Hey, you use the web, right? What’s a good website?”

The numbers back up my experience. According to a16z, 65% of podcast listeners began listening in the past three years. Just over half of the country (51%) has ever listened to a podcast. The entire podcast industry generated $679 million in advertising revenue last year. For comparison, YouTube brought in $15 billion, or 22 entire podcast industries, from ads in 2019.

Until last week, podcasts hadn’t had their Gold Rush moment.

Back in 1848, Marshall and Sutter tried to keep their discovery a secret. But gold doesn’t stay quiet. Within two years, San Francisco’s population increased from 1,000 to 25,000. Over the next seven, 300,000 people would uproot their families, hop on wagons, and head west to stake their claim in the California Gold Rush. (Source)

Humans are predictable; we follow the money.

Joe Rogan’s $100 million+ Spotify deal is like a giant dollar sign bat signal to potential podcasters, and online individual creators more broadly. It means that podcasting can be more than a hobby or a job. Like acting, music, sports, and tech, podcasting is now a viable way to create generational wealth.

Another of this week’s biggest stories lends credence to the argument that starting a podcast is a financially viable path.

On Sunday, Dave Portnoy, the founder and President of Barstool Sports, took over the Call Her Daddy (CHD) podcast to give his side of the story of the dispute between the CHD hosts, Alexandra Cooper and Sofia Franklyn, and Barstool, which owns the rights to CHD.

The whole dispute is fascinating but beyond the scope of this post. Check out Blake Robbins’ thread and Taylor Lorenz’s New York Times piece for the full story.

What is important to note for this essay are the money and power dynamics. According to Portnoy, below is what the “Fathers,” Cooper and Franklyn, have earned thus far and what he offered them in a new deal:

Each co-host was guaranteed $70k for three years plus performance bonuses

With bonuses, Cooper made $506k and Franklyn made $461k in the first season

Portnoy offered the co-hosts a deal for $500k guaranteed each, performance bonuses, 7.5% of merchandise sales, 6 months knocked off the three-year deal, and the opportunity to walk at the end with full rights to the IP.

As of Friday night, Franklyn walked away, Cooper stayed. Both will make significantly more money than they did a year ago.

For an industry to be appealing to the most talented people, it needs both a solid base and the chance for huge upside. These two deals show that the podcast industry at least, and likely the Passion Economy more broadly, has both.

They also show that the balance of power is shifting to individual creators who own direct relationships with customers.

There’s an idea in startups that to see the future, you should look at what the smartest people are doing on nights and weekends. Recently, many of the smartest people I know have been spending their nights and weekends writing newsletters and recording podcasts. Some have even quit great jobs to write and record full-time.

Rogan and CHD will mark a turning point; the Passion Economy is now a visibly viable path for even the most ambitious.

Barbelling of Media

In media, individuals and aggregators are winning; the middle is disappearing.

Ben Thompson’s Aggregation Theory “describes how platforms (i.e. aggregators) come to dominate the industries in which they compete in a systematic and predictable way.” Instead of winning by owning supply, as many of the 20th century’s largest companies had, aggregators win by owning demand.

Aggregators changed the media landscape.

Previously, the name of the game was to integrate supply. Radio stations do a bunch of things - license spectrum, build a studio, hire producers, hire talent, pay royalties, and sell ads - in order to get their content on the air. In spectrum licenses, radio stations owned a positionally scarce resource and a captive audience. Delivering supply into that captive audience allowed them to print money through ads.

Since Spotify launched in 2006, though, radio stocks have gotten crushed. The chart above shows the performance of the largest publicly traded radio companies (all of the negative lines) against the NASDAQ and S&P 500 (the positive lines).

This is correlation, not causation; Spotify did not kill the radio star. The same factors that allowed for the rise of Spotify spelled the downfall of terrestrial radio. Instead of a limited number of local stations, consumers could listen to anything, from anywhere, at any time. The internet built a bridge over radio companies’ supply-driven moats and made their heavy cost structures a liability.

Meanwhile, with just an app, record labels deals, and recommendation technology, Spotify built up a listenership of 286 million. Through its reach and recommendations, Spotify became a kingmaker; inclusion on one of Spotify’s most popular playlists, like Rap Caviar, can make a career. As a result, artists are tailoring their music and their go-to-market strategies to maximize their chances of being included.

Spotify uses its demand to bend supply to its will. Spotify is the Audio Aggregator.

The aggregators’ wake is littered with media companies. Just as Spotify is increasingly taking share from traditional radio broadcasters, Google and Facebook have crushed publishers from local newspapers to Buzzfeed.

But while aggregators crush the middlemen - radio stations and newspapers - they actually empower individual creators!

Thanks in large part to the aggregators like Twitter, Facebook, Google, and Spotify, individuals have the tools to build their own media businesses.

As Li Jin wrote in Four implications of disruption theory for the Passion Economy:

Now, a new entrepreneurship stack has emerged for online content creators: scaled social networks democratize distribution, and new platforms make it easier than ever to create and monetize content. On the consumer side, people’s information appetites are shifting from bundled media content to curated podcasts, blogs, newsletters, and video content.

One person taking on an industry with a lower-feature, lower-cost product is the ultimate low-end disruption. Podcasts are eating radio and newsletters are just starting to eat everything from local newspapers to large online publishers. Individuals (in which I am including modern, personality-first media businesses like Barstool Sports and The Athletic), can use existing infrastructure and strong personalities to own niches that are very profitable given their minimal cost structure.

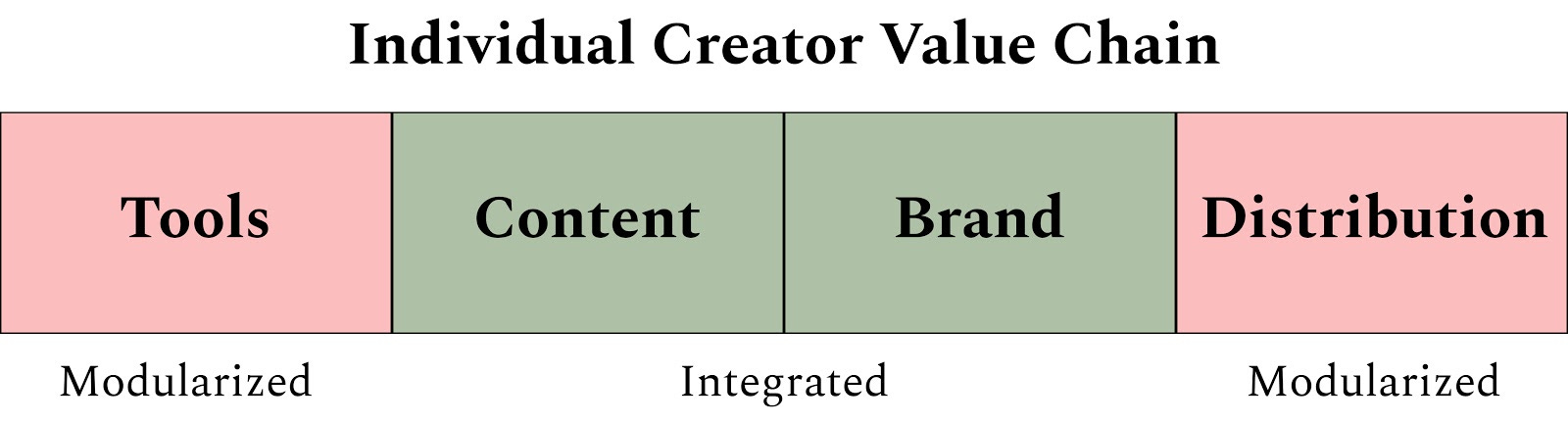

From the individual creator’s perspective, Substack, Anchor, and the new wave of Passion Economy startups (the picks and shovels, to extend the Gold Rush analogy) provide modularized tools, the aggregators provide modularized distribution, and all that’s left is to create and remain authentic.

In While Zoom Zooms, Slack Digs Moats, I introduced Hamilton Helmer’s 7 Powers. Individual creators derive their power from one of the seven: Brand. Individuals are able to connect with audiences on a deeper, more personal level than companies are.

In his summary of 7 Powers, Florent Crivello wrote a sentence that perfectly encapsulates why Spotify had to pay Joe Rogan:

There is a positive feedback loop at play with brands and distribution channels. The more people know your brand, the more they expect to see it on the shelves of their favorite store, giving you more leverage over it.

People know and love Joe Rogan, and they expected to see him on Spotify.

Aggregators and individual creators need each other, and work together at the middleman’s expense. As with most things in business, Michael Porter predicted this.

In his 1980 book Competitive Strategy, Porter wrote about the Three Generic Strategies: Cost Leadership, Differentiation, and Focus. According to Porter, a company must choose to be either low-cost or differentiated, and may choose to combine either strategy with a focus on a particular business segment.

Those that pursued neither or a combination of the two strategies were “Stuck in the Middle.”

Applying it to the modern media landscape, aggregators win on Overall Cost Leadership, individuals win on Differentiation (read: Brand), and legacy publishers, saddled with high costs and a product bloated with undifferentiated content, are Stuck in the Middle.

In media, and I suspect in an increasing number of industries, the profits will accrue to the two ends of the barbell: aggregators and individuals.

Spotify’s Strategy

So here’s a question:

If this is an aggregator’s world, and Spotify is an aggregator, what is it doing paying Rogan $100-$200 in addition to the $480 million they’ve already paid for The Ringer and Gimlet Media to backward integrate into supply?

Last June, in From Linear Businesses to Aggregators and Back, I wrote about this strange phenomenon. Airbnb, Uber, Amazon, Zillow, and Netflix had all achieved the holy grail of internet businesses: aggregator status. But for some reason, each one of them started backward integrating into supply. For example, Zillow buys houses and Netflix spends $10s of billions on producing its own content.

On the surface, becoming more asset-heavy and increasing costs makes little sense, but I pointed to three reasons that they would do it: Data Advantages, Superior Customer Experience, and Better Economics.

Since that piece, Spotify has joined the backward-integrated-aggregators, for the three reasons I wrote about then:

Data Advantages: Spotify has more targeted listener data than anyone else, and they have designs on using that data to do to podcasting what Google and Facebook have done to the web - build an ad layer on top of it.

Superior Customer Experience: Before this deal, Spotify listeners could not listen to Joe Rogan on Spotify. Now they can. Whether it’s good for podcast listeners generally is beyond the scope of this post; check out Nathan Baschez’s post, The Open Podcast Ecosystem is Dying - Here’s How to Save It.

Better Economics: This is the key to understanding the deal. Even though Spotify is an audio aggregator, its margins suffer because its suppliers - the music labels - have power over them. Three labels own the vast majority of the rights to the back catalog of all the music that people want to listen to, so Spotify has to pay the labels 70% of its revenues, locking in low margins.

As I wrote about in Earshare: The Idiot’s Guide to Investing in Spotify, podcasts are an upfront investment in a business line that will generate higher margins over the long-run. Over time, once they’ve renegotiated contracts with the labels, the more revenue they generate from podcasts, the more revenue they get to keep.

**BRAG TIME** In Earshare, I argued that pieces of good news about podcasts would break the bearish narrative around the company and send the stock higher. Since that article, Spotify is up 40% versus 8% for the NASDAQ and flat for the S&P 500. Over half of that gain came after Joe Rogan tweeted about the deal on Tuesday at 4:30pm.

The market loves Spotify’s strategy, and it has rewarded it with an additional $4 billion in market cap. And no wonder - instead of acquiring a full media business with a ton of employees and overhead, and a capital structure that would have likely increased the price of the deal to make investors happy, Spotify was able to acquire a big listenership by partnering directly with one dude.

In that light, the company’s $750 million podcast shopping spree seems like a steal.

What Does it All Mean?

For Joe Rogan

People have questioned whether or not this is a good deal for Joe Rogan. It’s hogwash.

We don’t know the terms of the deal yet, so it’s pretty hard to say it was a bad deal. All indications are that it’s at least a $100 million+ payday.

He will still be able to generate ad revenue.

He gets access to Spotify’s audience of 286 million (and growing) listeners.

As Baschez pointed out, Rogan’s large and casual audience might be hard to monetize through subscriptions.

Along with the Ringer and Gimlet shows, Rogan’s podcast will be a first and best customer for Spotify’s Streaming Ad Insertion product. Generating beaucoup bucks for Rogan will serve as proof for the podcasts it recruits to its ad network.

Given how crucial podcasts are to its future, I wouldn’t be surprised Spotify put equity bonuses in Rogan’s deal to align their interests in establishing podcasts as a core piece of the business, like Sirius did for Stern. I’m bullish on the company; the equity might end up being the most valuable part of the deal.

For Joe Rogan, this deal is a massive win. He’s getting even richer, and serving as the model for millions of individual creators.

For Spotify

Daniel Ek, Spotify’s CEO, is a Worldbuilder. He has been plotting his company’s course to audio domination for over a decade, making short-term painful investments to put Spotify in a strong position long-term.

AirPods ushered in the audio era, and Spotify is moving aggressively to own podcasting in order to improve its margin profile and become the one-stop-shop for audio. Signing the biggest podcaster to an exclusive deal is both a smart customer acquisition move and an announcement that Spotify is playing to win.

I remain incredibly bullish on Spotify, and I don’t think they’re done making acquisitions in the non-label-owned audio space. Three potential targets?

Clubhouse, the audio chatroom that just raised $12mm at a $100mm valuation from a16z and keeps people engaged for hours a day.

Epidemic Sound, its fellow Swede, whose goal is to “soundtrack the world” through owned, royalty-free licensing. Epidemic produces and owns the right to a lot of the kind of music that makes up playlists like Chill Vibes and Deep Sleep that could chew up listening hours without causing royalty payments to labels.

Sonos, the high-end speaker maker, which Brett Bivens and Sid Jha argue would give Spotify material ownership of its distribution.

Spotify is just getting started building its audio-first world.

For You

The gold rush is on. There has never been a better time to be an individual creator. Launch a podcast, write a newsletter, teach an online course, build a small e-commerce brand. If you’re reading this from a computer or phone, you have the tools you need to create. With your Facebook, Twitter, or Instagram account, you have a world of customers within reach.

In Schumpeter’s Gale, I wrote:

COVID has shown many people the importance of having a skill that they can monetize directly with their followers and audiences. I suspect that we will see a proliferation of one-or-two person creative businesses like newsletters, podcasts, courses, design, and coaching. We will also see these business models evolve.

Individuals are more than just viable businesses. The individual creator, in symbiosis with aggregators and picks-and-shovel makers, is best-positioned to earn a significant amount of media industry profits.

Get writing and recording.

Bonus: The first episode of the Joe Rogan Experience from December 24, 2009

The Road to 5,000

It took 313 days for the first 500 people to subscribe to Not Boring, 42 to go from 500 to 1,000, and just 20 to get from 1,000 to where we are now: 1,502.

Thanks for helping this curve go exponential. Only 3,498 to go - spread the word!

📡 Tune in on Thursday for Marc Geffen’s guest essay on Worldconnectors.

Thanks for reading,

Packy

Another great essay :)