Reliance: Gateway of India

Part I: The History and Present of Reliance Industries, from Dhirubhai to Jio

Welcome to the 1,034 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 17,234 smart, curious folks by subscribing here!

🎧 If you prefer to hear me stumble over “Atmanirbhar Bharat,” listen here or on Spotify.

Hi friends 👋 ,

Happy Monday! This is my first Not Boring as a dad, and we are absolutely loving it (although please forgive me if there are sections in which it seems like my brain is mush — it is.)

The timing worked out perfectly for this week’s topic. A couple of weeks ago, I asked people on Twitter for their favorite international companies that not enough people know about. The topic of today’s Not Boring, Reliance, was among the most popular answers. So for my first essay as a father to a half-Indian son, I get to tell the story of India’s most important company.

But first, a word from our sponsor:

This week's Not Boring is brought to you by…

As we'll discuss today, Reliance democratized investing in India back in 1977 when it went public at ₹10/share. The low price gave everyone a chance to own a little piece of a public company, and its strong performance since has generated huge returns for regular investors.

Today, Public is democratizing investing by making the stock market social. It's the place where newcomers and experienced investors alike come to discuss their favorite companies and market trends. And it keeps getting better. Just last week, my favorite pseudonymous FinTwit account, Ramp Capital, joined Public.

I’ll be discussing today’s essay over on Public, and can't wait to talk about the surge of Indian IPOs on US exchanges over the next year on there. Join me.

*This is not investment advice. See Public.com/disclosures/.

So throw on some A.R. Rahman…

and chalo!

Reliance: Gateway of India

In Mumbai, a short walk from Leopold Cafe and across the street from the Taj Hotel, where Puja’s parents were married, a large stone arch-monument called Gateway of India sits between the city and the Arabian Sea. The British commissioned Gateway of India in 1911 to commemorate the landing of King-Emperor George V and Queen-Empress Mary, the first British monarchs to visit India. After Indian Independence from Britain in 1947, the last British soldiers left India through the very same gate.

Today, that structure is largely a tourist destination. The real Gateway of India, as far as foreign companies and investors are concerned, is Reliance Industries.

Atmanirbhar Bharat

Since I started writing Not Boring, one type of company has fascinated me more than any other: the Asian tech conglomerate.

Japan’s SoftBank, led by Masayoshi Son, distorted both the private and public markets through its Vision Fund and 555 Fund investments. Masa has been reinventing his company since the ‘80s; today, it’s more investor than operator.

The 2010s were China’s decade. Tencent and Alibaba, with a combined market cap of $1.4 trillion, are now household names in the kinds of households that read Not Boring. They’ve parlayed strong core businesses into unparalleled global equity portfolios.

The 2020s will be India’s decade. And unlike China, which features a fierce competition at the top between Tencent and Alibaba, in India, Reliance is the main game in town.

Reliance Industries Ltd (“Reliance” or “RIL”) is like an India-focused Exxon, Dow Chemical, Walmart, AT&T, and Comcast all rolled into one. If it fulfills its Jio vision, it will add Shopify, DoorDash, Zoom, WeChat, Square, AWS, and more to that roll. Its $200 billion market cap is the largest in India, where its backstory, leaders, products, and dramas are well-known. But when I asked a bunch of smart non-Indian friends what they knew about Reliance, they replied, “Who?”

I salivated. Nothing gets me jazzed like an under-discussed Asian tech conglomerate.

At RIL’s helm is Mukesh Ambani, one of company founder Dhirubhai Ambani’s two sons. Mukesh is the richest person in Asia and the sixth richest person in the world, with a net worth of $85 billion. His house is worth more than whole small cap companies.

Under Dhirubhai, the company was a dominant force in domestic Indian business and politics for nearly thirty years. Under Mukesh, particularly since the start of Coronavirus, it is making a dramatic push into the western consciousness.

This summer, Reliance made waves by selling 33% of its Jio Platforms business for $20.4 billion to a who’s who of international strategic and financial investors, from Facebook to KKR to Mubadala. Over the past three weeks, Reliance has been at it again, selling stakes in its Reliance Retail business to many of Jio’s financial investors, with a potential Amazon investment waiting in the wings.

It’s no surprise that the world’s largest companies, investors, and sovereigns want a piece. India is the world’s most important growth story, and Reliance is its gateway.

Now, I might be biased on the India front. Last week, I became a dad to a half-Indian son, and this is a picture of me at my wedding:

So caveat emptor. But I’m in good company. When many of the world’s smartest investors plow large sums into not one but two Reliance subsidiaries in less than six months, you should take notice. Here’s why they’re excited about India:

The world’s second largest country by population with 1.3 billion people.

The fifth-largest economy in the world by Nominal GDP at $2.94T.

The second fastest-growing trillion-dollar economy behind China.

Expected to grow mobile users by 40% to 800 million by 2023.

Not China. The Indian economy has similar characteristics to China’s without the CCP’s... baggage. Plus, India is leading the anti-China charge, banning 59 Chinese apps after a May border clash between the two countries in the opening salvo of a battle being fought with dollars instead of guns.

Increasingly, India is the play for smart money that wants to bet on Asian growth and technological capability without China’s political or ideological hairiness. And Reliance is the best partner for foreign companies and investors who want exposure to India. These are just a few of its accomplishments:

The first Indian company to cross a $150 billion and then $200 billion market cap.

Responsible for 3% of Indian GDP and 5% of its tax revenues [source].

Reported ₹772,752 crore or roughly $105 billion in revenue for the past fiscal year. (This conversion isn’t intuitive, so from here on out I’ll use dollars, but for our edification, “crore” means 10 million and a dollar is currently worth about 73 rupees.)

Runs India’s largest energy and petrochemicals business, part of which it will spin off to attract more global investment from the likes of Saudi Aramco and BP.

Operates the country’s largest retailer, Reliance Retail, and is pushing into ecommerce with JioMart, in a traditionally super-fragmented market.

Bringing about a mobile revolution with Jio Platforms, slashing data costs by 95% since 2013 and driving a 20x increase in Indian data consumption to 8.3 GB/mo/user, on par with South Korea.

Market cap has grown at a 32% CAGR for the past 43 years.

In 2020, fueled by Jio and Retail, Reliance is up another 47.5%.

Most of Reliance’s success to date is due to its fortress position in its home market. Now, it’s going global. During Reliance’s most recent Annual General Meeting in July, Mukesh Ambani highlighted Reliance’s plan to build products that are “Made in India, Made for India, Made for the World.” He wants to run Amazon’s “First-and-best customer” strategy on a national scale.

In many ways, Reliance’s strategy is a reflection and extension of Prime Minister Narendra Modi’s Atmanirbhar Bharat Abhiyan, which translates to “Self-Reliant India Mission.” Announced in May, Atmanirbhar Bharat is not as isolationist or protectionist as it sounds. It’s meant to make India “a bigger and more important part of the global economy.” No company is better positioned to profit from Atmanirbhar Bharat than Reliance.

To date, Reliance has very much been Made in India, Made for India. Its stock has been the most widely-owned in India for over four decades, but it’s nearly impossible for foreign investors to own directly.

Now, India and Reliance are taking their place on the world stage. No doubt driven by Ambani’s desire to take Jio Platforms public on the Nasdaq, the Indian government is considering changing rules that prohibit Indian companies from listing directly on foreign exchanges.

Now is the time to get smart on India, and this two-part series will serve as your guide to Reliance’s history, present, and future. In Part I today, we’ll cover Made in India, Made for India:

Reliance Under Dhirubhai. Dhirubhai Ambani learned to work the government and its regulations to his advantage in building a multi-billion dollar energy and petrochemicals empire.

Succession. Dhirbubhai’s death precipitated a vicious succession battle between his two sons, Mukesh and Anil.

Reliance Today. Reliance is the first Indian company to hit a $200 billion market cap. While the great majority of its revenue and profits come from its energy and petrochemicals businesses, Mukesh is reshaping the company to focus on Retail and Technology. It benefits from the Modi government’s mission of Atmanirbhar Bharat.

Reliance Retail. Reliance runs the largest retail business in India, and is wrangling entropy on both the supply and demand sides to modernize India’s retail infrastructure in partnership with existing retailers big and very small. It’s attracting investment from abroad, and Amazon might be next.

Jio. By leapfrogging 2G and 3G to focus on 4G and 5G, Reliance built India’s largest telecom network in under a decade. Investors from Facebook to KKR have poured more money into Jio in the past six months than all Indian startups raised in 2019 combined.

In Part II, we’ll make some predictions about Reliance’s future, its opportunity in the Indian technology landscape, and its growing importance on the world stage. We’ll cover how Reliance is ready to Make for the World.

By the end of this two-parter, you’ll understand why Reliance is on the precipice of becoming one of the world’s most important tech companies. When it joins that echelon, it will be unique among its peers in that its most important input in the early days wasn’t silicon, but polyester.

Dhirubhai Ambani: The Polyester Prince

The Dhirubhais [of this world] are to be thanked, not once but twice over. They set up world-class companies [and] by exceeding the limits in which those restrictions sought to impound them, they helped create the case for scrapping those regulations.

-- Arun Shourie, former Indian Minister for Disinvestment, Communication, and Information Technology. Quote from The Billionaire Raj.

The history of Reliance has been well-told in many places, from books like The Billionaire Raj to The Polyester Prince to Vedica Kant’s excellent essay, Reliance: Origins. I will lean on these sources heavily in this history, and you should read them if you’re interested in learning more.

Born in a small village to a schoolteacher father and his wife in what is now the state of Gujarat in British-ruled India in 1932, Dhirubhai Ambani’s life is a classic rags-to-polyester suits story. When he was in his late teens, Dhirubhai moved to Aden, a British port in modern-day Yemen, where he worked as a Shell pump attendant and then office clerk. At Shell, he learned the oil business, but in the Yemeni souks, he learned to trade. In To Understand Jio, You Need to Understand Reliance, Byrne Hobart recounted this telling story from The Polyester Prince:

In the early 1950s, monetary authorities in Yemen noticed a concerning trend: a currency shortage. After investigating the matter, they traced it back to a young clerk in the city of Aden, who had discovered that at the prevailing exchange rate, Yemeni rials contained more silver than their face value. So he bought them for British pounds, melted them into silver, exchanged the silver for pounds, and repeated the process.

Young Dhirubhai saw that rials were worth less as currency than as metals, and arbitraged the system to generate a tidy profit. It was the first example of what would become a long career of understanding and bending the system to achieve his desired outcome. Soon after, Dhirubhai returned to India and founded Reliance Commercial Corporation in 1966. In 1973, he renamed the company Reliance Industries, representing its expanded focus.

Leaning on his education in the souks of Aden, Dhirubhai started Reliance by trading spices and textiles. He made his first fortune, though, in import licenses.

To encourage manufacturing, the Indian government put strict import limits on yarn and other textiles, giving licenses only to textile exporters who needed to import raw materials. Dhirubhai acquired these “Replenishment Licenses” from the exporters and began to control the supply of yarn. His next moves showcased what would become two major elements of Reliance’s success: vertical integration and cultivating government relationships.

In order to capture more of the profits from the yarn, Ambani set up a textile manufacturing facility, vertically integrating from trade of raw materials to manufacturing finished products.

He also formed important government relationships with aides to Prime Minister Indira Gandhi (no relation to the Gandhi). In The Billionaire Raj, James Crabtree wrote, “His philosophy was to cultivate everybody from the doorkeeper up.”

His relationships paid off early and often. Vedica Kant wrote that in 1971, PM Gandhi’s government set up a High Unit Value Scheme, which allowed the import of polyester filament yarn against exports of nylons. Reliance “accounted for 60% of imports and exports under the scheme.” In 1977, a new Congress scrapped the scheme, forcing Reliance to focus on retailing to the Indian market instead of exporting, which had accounted for much of its business to that point. Dhirubhai created the Vimal polyester suit brand and established a network of Vimal franchises across India to sell product directly to consumers.

That same year, under pressure and needing cash, Reliance decided to go public. It democratized access to public market equity investments in India by offering stock at an incredibly affordable ₹10 per share. Puja’s parents lived in India at the time and told me that everyone bought shares in Reliance. The numbers back them up. In an investment frenzy that makes Tesla and Apple’s stock split-driven demand look tame, Reliance’s IPO was 7x oversubscribed. As Indian stock market investors quadrupled between 1980 and 1985, one in four owned Reliance shares. So many people owned Reliance that, years before Warren Buffett brought Berkshire Hathaway’s shareholders together in Omaha, Dhirubhai Ambani held his Annual General Meetings in sold-out cricket stadiums.

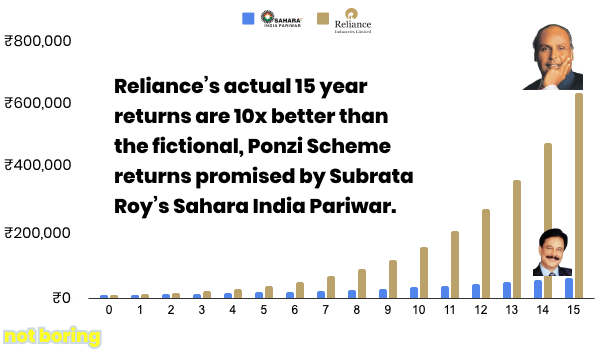

Hobart points out that the IPO “gave Reliance a broader political constituency: instead of buying individual regulators with bribes, they nudged the electorate with dividends.” As Puja’s dad explained it to me, Reliance made a lot of regular Indians wealthy, as the stock grew and split and grew and split and grew and split over the intervening 43 years. At the 2017 AGM, Mukesh Ambani said that ₹10,000 invested at IPO would be worth ₹1 crore in 2017, a 1000x return. The stock is up 3.25x since then, which means that $1,000 invested in 1977 would be worth $3.25 million today. Reliance Industries’ stock has grown at a 32% CAGR for 43 years!

For context, the new Netflix show Bad Boy Billionaires: India, tells the story of Sahara, a pyramid scheme that promised poor Indians 6.5x returns over 15 years on small amounts of money. Those investors lost everything. Had they invested their money in Reliance stock, instead, they would have multiplied their money by 64x over the same period.

Flush with cash, supported by millions of happy shareholders, and with Indira Gandhi back in power in the early 1980’s, Reliance backward integrated, making its own polyester fibers through a subsidiary, Reliance Petrochemicals. The liberalization of the economy set the stage for further expansion.

Between its independence from Britain in 1947 and 1991, India operated a protectionist economy with heavy state intervention, more akin to the Soviet Union than the United States. (In fact, India was militarily aligned with the Soviets during the Cold War, and still flies MiGs today, although as its economy becomes more American, it’s buying more of its arms from the US.)

Pre-1991, elaborate licenses and red tape, known as the “License Raj,” limited who could set up what type of business. Dhirubhai played this system masterfully to produce Reliance’s early success, and from that strong position, Reliance was well-prepared to take advantage of economic reforms. In 1991, under Prime Minister P.V. Narasimha Rao and Finance Minister Manmohan Singh, India liberalized and laid out a five-point plan to foster the Indian economy:

Abolish the License Raj by removing licensing restrictions for all but the most security-sensitive industries.

Incentivized foreign investment by pre-approving all investment up to 51% by foreign companies, allowing them to bring money, technology, and development.

Incentivized technological advancement by scrapping the need for government approval for technology agreements.

Dismantled public monopolies by selling shares in public sector companies and limiting public sector growth to things western governments do, like infrastructure and defense.

Uncapped company upside by eliminating the concept of an MRTP company, which were placed under government supervision when their assets exceeded a certain value.

My father-in-law told me that this evolution from a state-run to liberal economy was planned all along, and Reliance was prepared. The company still benefits today.

Freed by India’s liberalization, Reliance backward integrated even further, establishing Reliance Petroleum to finance its own oil refinery, Jamnagar, which was the world’s largest when it opened in 2000. (Just to give you a sense of Reliance’s mind-blowing scale, it’s casually the largest exporter of mangoes after the company planted mango trees at Jamnagar to assuage pollution concerns.)

Reliance was on a tear and Dhirubhai was worth $25.6 billion when, in 2002, he suffered a stroke and passed away at age sixty-nine. As captured in the quote at the beginning of this section, he not only built a leading Indian company, he exposed and leveraged holes in the Indian regulatory framework that likely played a part in liberalizing the economy.

Dhirubhai left behind an enduring legacy and a multi-billion dollar empire. His death set off a succession battle fit for Jio TV+.

Succession: Reliance Edition

Dhirubhai Ambani had two sons. Mukesh, the elder brother, was an “unflashy, introverted, and well organized” Institute of Chemical Technology grad who enrolled at Stanford GSB before dropping out to help his father run Reliance. Anil, two years his junior, was a “flamboyant financial wizard” who got his MBA from Wharton. While Dhirubhai was alive, the two sons worked well together, but after his death, they battled fiercely for control of the company.

“The war,” as it was referred to, got so bad that the brothers, who lived in the same building in Mumbai, coordinated their entry and exit through associates so as not to run into each other. The battle was one of the reasons that Mukesh decided to move into his own digs, Antilia, the second most valuable residential property in the world behind Buckingham Palace at $2.2 billion.

After three years of fighting, Mukesh and Anil’s mother, Kokilaben, got them to agree to a peace accord, which she announced in June 2005. Each brother would get half of the company:

Anil: Reliance Group, including RIL’s newer businesses like Reliance Energy (power), Reliance Infocomm (mobile & telephone), and Reliance Capital (non-bank finance).

Mukesh: Reliance Industries, including oil refining, retail, and exploration, and petrochemicals.

As part of the terms of the agreement, the brothers agreed to a ten-year non-compete, meaning that Mukesh couldn’t get into, say, telecoms until 2015. (Hold on to that thought.) At the time of the split, Mukesh was the third richest man in India, with a net worth of $7 billion, with his younger brother right behind him at number four, worth $5.5 billion.

From this point on, we’re going to be following Mukesh’s side of the house, Reliance Industries, because he has outperformed his younger brother by orders of magnitude. You already know that Mukesh is the richest man in Asia, worth $85 billion. How about Anil? In March 2019, Mukesh had to bail him out of a $77 million dollar loan he owed Ericsson, in exchange, the rumors go, for Anil’s attendance at Mukesh’s daughter Isha’s late 2018 wedding. In February 2020, Anil declared before a UK court that he was bankrupt, with assets of $82.5 million and liabilities north of $300 million. Although many don’t believe he’s as poor as he claims, it illustrates how far he’s fallen.

Reliance Today

Mukesh built on his father’s legacy to create an empire spanning energy, petrochemicals, digital services, and media and entertainment. Today, Reliance makes money in six main ways:

It’s super simple, just 158 subsidiaries and seven associate entities:

Reliance even owns my favorite cricket team, the Indian Premier League’s Mumbai Indians. Mumbai won the 2019 IPL Championship led by Mukesh’s wife Nita, who also runs the Reliance Foundation, and his son, Akash, who is an executive on Jio and Retail. It currently sits atop the 2020 IPL standings, too.

As with any multinational conglomerate, there’s a lot going on at Reliance, so to understand the company’s priorities, it’s helpful to look at how the company talks about itself, and for how long:

In Acquisition in the Key of G Sharp, I wrote that one way to think about Google is as the United Arab Emirates: “The UAE is ridiculously wealthy right now because of oil, but it knows the oil money won’t last forever, so it’s investing heavily in new growth opportunities like tech and tourism.” In that essay, I compared search ad revenue to oil.

In Reliance’s case, the analogy holds, except we’re literally talking about oil. Reliance’s Oil-to-Chemicals (O2C) business, spanning the entire energy value chain from exploration and production, to refining and petrochemicals, to marketing and retail, is responsible for 69% of Reliance’s revenue ($73 billion) in 2019-2020 and 63% of its profit ($7.6 billion).

But Ambani realized that oil cannot be the long-term future of the business. In addition to committing to hydrogen, wind, solar, fuel cells, and batteries on the road to its carbon neutral by 2035 goal, Reliance is doing two things with its oil business:

Raising Cash. Last year, Reliance announced a ₹7,000 crore (~$1 billion) investment from BP for 49% of its fuel retailing business, and now it’s in the process of spinning off a big piece of its O2C business, including its oil refinery, petrochemicals, and fuel retailing assets. It’s valuing the subsidiary at $75 billion and is in talks to sell 20% of the unit to Saudi Aramco.

Running the Middle East playbook. Reliance is taking the cash it generates from the legacy oil and petrochemicals business in new growth areas, namely Retail and Jio.

Oil and petrochemicals are Reliance’s past. Retail and Jio are its future.

Reliance Retail and Jio

During the Annual General Meeting, Reliance spent 57 minutes talking about its business lines. It dedicated 42 of those minutes to Jio, the new gem of the portfolio, despite the fact that it makes up only 8.9% of revenue and 25% of profits. It also spent five minutes on Reliance Retail, which is increasingly tightly linked with Jio and key to its future growth plans.

Both Reliance Retail and Jio, two business lines Mukesh started after his father’s passing, follow the New Reliance Playbook:

Use balance sheet and cheap debt to spend on high upfront fixed costs and spread them out over millions, and potentially billions, of customers t low marginal cost.

Build up a complex, capital-intensive business using local know-how, logistics expertise, and connections.

Aggregate hard-to-wrangle Indian demand and supply.

Sell access to that demand to international companies and investors via investment and strategic partnership.

It’s worth noting that an important part of Reliance’s playbooks, old and new, is its governmental relationships. Reliance’s relationship with Modi’s government has helped Jio and Retail succeed, for better or worse. Two examples highlight the cozy relationship:

In 2016, Reliance and the State Bank of India set up a JV to provide banking and remittances through Jio and Reliance Retail.

Modi’s government is making it difficult for BSNL, which provides telecom to India’s poorest and most remote regions, to obtain licenses to upgrade to 4G. The denial is ostensibly because they use Chinese components, but many believe it’s a bid to help Jio at the expense of BSNL.

Critics claim that Reliance unfairly benefits from its relationship with Modi and his BJP government to the detriment of competitors, potential competitors, and consumers. While there seems to be a great deal of truth to the criticism, this is nothing new for Reliance, or indeed, for large corporations anywhere (Oracle/TikTok, anyone?). Dhirubhai built Reliance on the strength of his relationships with the government, and Mukesh is carrying on that legacy, helping Modi achieve his development goals for India and benefiting in the process.

This relationship deserves its own essay, but for now, know that it exists, and is both a tailwind while the BJP is in power and a potential risk if it falls out of power. Before that happens, Reliance needs to further cement its place as crucial infrastructure for the Indian economy so that any government has no choice but to work with it. Retail and Jio are crucial to that aim.

Both business lines speak to Mukesh’s ambition to build a new Reliance of his own design and highlight Reliance’s position as the only serious way for foreign companies to access the Indian market at scale. They also prove that, like Tencent’s Pony Ma, Ambani is a masterful capital allocator, turning legacy assets and cheap debt into two future-ready, cashflowing businesses valued at a combined $120 billion.

Reliance Retail

In 2006, one year after taking the helm of Reliance Industries, Mukesh launched Reliance Retail, a nationwide network of retail outlets. Since then, Reliance Retail has grown into the largest and most profitable retail business in India and the fastest-growing retailer in the world, increasing revenue by 8x and profits by 11x in the past five years alone. Today, it boasts 11,874 stores, more than two-thirds of which are in Tier 2, 3, and 4 cities (which, in India, can mean a few million residents), covering 28.7 million square feet. Its breadth is astonishing:

It has grocery stores, cash and carry stores, corner stores, consumer electronics stores, and fashion & lifestyle stores, along with its own consumer brands in each of those categories. It also boasts exclusive partnerships with many of the world’s largest retail brands. Partnering with Reliance is the easiest way to access Indian consumers.

It is also piloting JioMart in 200 cities across India, powering local kiranas, which are like small, family-run bodegas, to physically overhaul them in 48 hours, set up and manage delivery operations, offer 7% lower prices than competitors, digitally track inventory, and auto-replenish based on inventory levels. It’s arming the existing, super-fragmented network of rebels, proving aptitude not only at wrangling demand but wrangling hard-to-wrangle Indian supply.

JioMart’s approach, combining elements of Amazon, Shopify, and DoorDash to empower instead of replace the local vendors might be the ultimate form of retail entropy wrangling. It even promises to be the first farm-to-home company at scale globally, bringing fruits and vegetables direct from the farmers who make up so much of the Indian population directly into consumers’ homes, sort of like an early Pinduoduo for India.

These are all things that a foreign company just couldn’t do on its own. Instead, in order to participate in the massive growth of the Indian retail economy, foreign companies and investors need to, you guessed it, invest in, and partner with Reliance.

Over the past two weeks, Reliance has sold about 8.5% of Reliance Retail for $5.1 billion to foreign investors, all but one of whom also invested in Jio Platforms (which we will discuss below), valuing the unit at $60 billion.

It is also in talks with Amazon for an investment of up to $20 billion in exchange for a third of the business, despite a potential legal battle brewing between the two. When Reliance acquired Future Group for $3.4 billion in August, it did so despite Amazon’s right of first refusal on the business, which Amazon is now suing Future Group to enforce. It will be fascinating to watch how this plays out in light of Amazon’s potential investment in Reliance Retail. If Amazon, which has struggled to gain a foothold in India due to regulatory issues (coincidence?), capitulates, it will further highlight Reliance’s fortress position as the gateway to foreign investment in India.

Backed by some of the world’s biggest investors, and with the ultimate strategic retail partnership waiting in the wings, Reliance has the cash to subsidize its kirana and merchant partners and wrangle Indian ecommerce. It might also be in a position to export its capabilities to other developing markets with a similar informal retail structure and infrastructure to India. Made in India, Made for India, Made for the World.

And Retail is only Reliance’s second-biggest opportunity…

Jio Platforms

Jio, Reliance’s digital services arm, is Mukesh’s ultimate bet on the digital revolution, which he calls, “the greatest disruptive transformation in the history of mankind, comparable only to the appearance of intelligent humans 50,000 years ago.” (He sounds kind of like Masa when he talks about it.) It burst into the global consciousness this summer when seemingly every major tech company and investor in the world invested billions of dollars in quick succession.

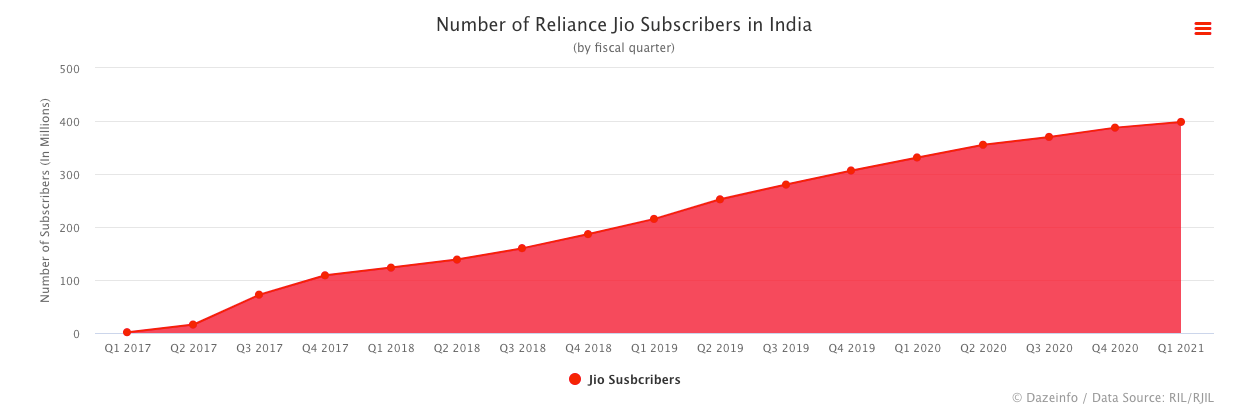

Jio is first and foremost a national telco built from the ground up that skipped legacy telephony systems and opted to go data-only through 4G, and soon 5G, infrastructure. That decision created a significantly lower cost structure that allows Jio to undercut competitors and deliver voice and data and world-low rates. Four years after its 2016 launch, it is the #1 mobile provider in India and the #2 largest mobile provider in the world.

Recall that when Anil and Mukesh Ambani split the Reliance empire, Anil got telecoms and the brothers signed a 10-year non-compete. So how did Mukesh end up as the brother with the enormous mobile network?

In From Oil to Jio, Vedica Kant highlights that in a 2010 effort to restore familial harmony, the brothers scrapped their non-compete, opting for a much simpler agreement that stated that RIL wouldn’t get into gas until 2022. That freed Mukesh up to go hard at telecoms, and he did.

That same year, in June, the Indian government began auctioning off 3G and broadband wireless-access (BWA or 4G) spectrum. Most bidders focused on the 3G, while a little-known company called Infotel won the 4G licenses in all 22 regions. After the winners were announced, Reliance swooped in and bought 95% of Infotel for $670 million. Like Walt Disney buying up the Florida swampland that would become Disney World via shell companies to keep prices down, Ambani used Infotel to keep his deep pockets hidden to other bidders.

When they realized that Infotel was just a front for Reliance, competitors cried foul, to no avail. Ambani had the rights to 4G across India.

Between 2010 and 2017, Reliance spent $32 billion of its own money and debt to build out a nationwide 4G network focused exclusively on data, not traditional 2G and 3G circuit-switched telephony services. That decision meant that voice could be handled over the data network for a fraction of the cost. As Ben Thompson wrote in India, Jio, and the Four Internets, Reliance’s strategy with Jio was the classic technology play: massive upfront costs with near-zero marginal costs. It spent $32 billion to build a 4G network that covers all of India, and offered three to six months of free data and voice to acquire as many customers as quickly as possible.

When Jio officially launched in 2016, the impact was massive. By offering three and even six months of free data and voice, Jio grew from 1.5 million subscribers in its first quarter to 398 million subscribers in the quarter ended June 30, 2020 (although the FT points out that potentially one-fifth of those users are now inactive, largely due to price increases). In four years, Jio acquired more mobile customers than there are people in the United States, with room to spare.

Jio’s low cost structure also made it nearly impossible for competitors to match them. In just three years, it caused four mergers and two bankruptcies, including Anil Ambani’s Reliance Communications.

While Jio was a death knell for competitors, it was incredible for consumers. When Jio launched in 2016, the average Indian used 400MB of data per month. As of June this year, Jio users were consuming an average of 11.3GB, a nearly 30x increase. The national average, including non-Jio customers, is now 8.3GB, on par with tech-forward South Korea, meaning that Jio forced its competitors to up their games, too.

More data consumption doesn’t just mean that people were more tied to their phones, it means that they were connected to the internet -- all of the commerce and communication and education and more -- without lag for the first time.

Jio unlocked massive growth in the Indian tech ecosystem, in both creation and consumption, and in the inflow of foreign dollars. As happened with Retail, investors saw that Jio cracked a challenging Indian distribution problem and poured money into the company to share in the upside and gain access to the Indian market.

In April, Facebook kicked off a flurry when it invested $5.7 billion for a 9.99% stake in Jio. Facebook had tried and failed to bring better* (*arguable) internet to India with its Free Basics, and realized that partnering with Jio was the smarter route. India is WhatsApp’s biggest market (as I can attest based on the flood of WhatsApps messages that stream in from Puja’s family every day), and the two companies have already launched a partnership to let consumers order directly from local JioMart stores via WhatsApp.

Including Facebook, between April and June, Reliance sold 33% of Jio Platforms for $20.4 billion to a range of world-class investors hungry for a piece of the action for financial or strategic reasons, or both. The transactions value the subsidiary between $58 billion (Facebook and Google got a better price for strategic reasons) and $66 billion (for everyone else).

Can we take a second to discuss the brilliance and uniqueness of Reliance’s financing strategy here? It was both a huge bet and a capital markets arbitrage.

Instead of raising equity financing when Reliance kicked off the project years ago, when it would have had to sell huge chunks of the business to raise the requisite $32 billion, more akin to a JV than a subsidiary with outside investors, Reliance took advantage of its existing balance sheet and pristine credit rating to raise non-dilutive debt.

With the business up and running, Reliance was able to sell just one third of the business for $20.4 billion to pay down debt, picking up both strategic partners for Jio Platforms and financial partners for future endeavors (like Retail, and, I think, something bigger soon).

Issued an innovative $7 billion rights offering in June, in which existing shareholders bought shares at a discount with a deferred payment plan, like Affirm for equity, to pay down more of the overall company’s debt.

No other company in India could have pulled this off, large or small. Telcos were locked into their existing networks and didn’t have the borrowing capacity of a large conglomerate. Reliance’s credit rating is higher than the government’s, meaning that it can borrow at the lowest cost of capital in India, and its size and government relationships make it the ideal investment for foreign companies and investors looking to play in India. Once Mukesh convinced himself that this was going to work, a big if, the way he chose to finance it was the highest-upside route.

Today, Reliance has zero net debt, well ahead of its March 2021 goal, with its next big bet ready for market: 5G.

Ambani said at the AGM that "Jio has created a complete 5G solution from scratch, that will enable us to launch a world-class 5G service in India, using 100% home grown technologies and solutions.” Jio plans to both connect India with 5G as soon as spectrum is available, and to export 5G solutions as a complete and managed service to other countries.

This plan was in the works before the May border skirmishes with China, but it benefits from India’s and the western world’s growing discomfort with China. Whereas China’s Huawei had been a critical piece of many countries’ 5G infrastructure plans, the US, UK, and India banned Huawei components, and Belgium recently rewarded its 5G contract to Nokia over Huawei. Huawei’s loss is Jio’s gain, and the 5G war is just one example in a trend away from China and potentially towards India.

And it has more Jio assets up its sleeve. The Jio Platforms investors only bought a piece of the wireless network and services. Reliance also has separate entities for:

Jio Fiber, which provides wired broadband service, and in which Reliance just invested $5.4 billion to buy a 48.4% stake from a trust, valuing the subsidiary around $11 billion.

Reliance Jio Infratel, which owns a portfolio of wireless towers in India, and for which Brookfield Asset Management paid $3.4 billion to acquire a 93% stake in 2019.

Reliance views Jio, including Platforms, Fiber, and the upcoming 5G network, not just as the underlying infrastructure layer, but as the platform on which it can offer a suite of digital services, from chat and payments to education and TV. With 5G, it will extend its Internet-of-Things capabilities.

This is not a new playbook. The spectacular failure that was AOL/Time Warner comes to mind, as does WebTV. The idea of combining the infrastructure with the apps and content makes intuitive sense, but it hasn’t really worked.

Jio has unique characteristics - including a massive market share in an enormous market and partnerships with Facebook and Google - that give it the chance to pull this off, although early adoption of Jio’s apps and services have been less impressive than consumer adoption of its infrastructure.

In just four years, Mukesh built a legacy-defining telco that generates $9.4 billion at a 33% EBITDA margin. Jio did about as much in 2019-20 EBITDA as Twitter did in 2019 revenue. And as India’s wealth grows, Jio will be able to charge more for its service, giving it upside even if consumers shun the apps and services it builds on top.

What’s Next for Reliance?

Whether or not Jio succeeds in getting consumers to use its apps and services, it has the opportunity to emulate a couple of other Asian tech giants that we’ve discussed in previous essays: Tencent and SoftBank.

If it succeeds in building a superapp, it will be in almost exactly the same position that Tencent is in China - controlling the flow of Traffic and Capital. Even if it fails to generate app adoption, though, Reliance controls both the wired and wireless pipes in India, giving it another cash cow that it can use to support and export the Indian tech ecosystem.

Today, we got up to speed on Reliance’s past and present. I hope you leave this essay excited to learn more about the Indian tech scene and Reliance’s role in it, because in Part II, we’ll explore Reliance’s future. That will take us on a journey through:

The Indian startup landscape

Further into China/India relations

Reliance’s Tencent and SoftBank Opportunities

India’s impending emergence onto the global exchanges

Thus far, we’ve focused on Made in India, Made for India. Next time, we’ll discuss how Reliance will Make for the World.

Thanks to Dan for the edits, and to my father-in-law, uncle Sudhir, and Sid Jha for their input! And of course, to Puja, for bringing Dev into the world and still reading drafts 😍

Thanks for reading,

Packy

Packy- I loved reading this. Such a treasure.

Hello, how does one invest in Reliance now and among the India funds is there one that you favor? Most have not been breaking down the fence in terms of total return.tia robert