Modern Treasury: The Quadrillion $ Quest

The $2 billion, 3-year-old Startup Modernizing Money Movement

Welcome to the 1,311 newly Not Boring people who have joined us since Monday! Join 85,240 smart, curious folks by subscribing here: 85,240

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts (shortly)

Today’s Not Boring, the whole thing, is brought to you by… Modern Treasury

Modern Treasury builds payment operations software to keep businesses’ money flowing. They’re building a world-class team to tackle a quadrillion dollar market. Join them:

Hi friends 👋 ,

Happy Thursday! Today’s post is an Investment Memo x Sponsored Deep Dive (you can read more about my Sponsored Deep Dive selection and thought process here).

Not Boring Capital recently invested in Modern Treasury at a $2 billion valuation, which is on the high-end of our range, particularly for a three-year-old company, so I wanted to walk through what makes the company special, why it’s in such a strong strategic position, and the massive opportunity it has in front of it.

Let’s get to it.

Modern Treasury: Quadrillion Dollar Quest

“People forget. Software is a good business.”

If valuations are any indication, people decidedly have not forgotten, but in the large and growing corner of the market in which Dimitri Dadiomov operates, software is a contrarian business model. Fintech companies normally want to touch the money so that they can earn interest on lending or interchange on spending.

But maybe because both of Dimitri’s parents worked at Microsoft and he grew up appreciating the scale and ambition of businesses built purely on software, he, CPO Matt Marcus and CTO Sam Aarons decided to build a company that makes “software for fintech, but is not fintech.” That company is Modern Treasury.

Instead of going after a specific vertical or customer, Modern Treasury builds horizontal software infrastructure for any company that moves money via bank transfers. It’s a data layer, not a money mover. Software for fintech, not a fintech.

Building software for fintech instead of sitting in the flow of funds is one of two big, non-consensus decisions the company is built on. The other?

Partner with the big banks instead of trying to take them down.

Banks catch a lot of shit around these parts, but they sure do move a lot of money.

In 2020, the ACH network handled $61.86 trillion in volume, $41.7 trillion of which were business to business payments. ACH operates in the US only.

Even more money moves via wires. In August alone, $85.4 trillion flowed through FedWire, the Fed’s system through which banks send money to each other. CHIPS, the largest private USD clearing system, did $1.8 trillion in volume per day. There are more clearing systems besides those two, but those two alone do over $1 quadrillion in annual volume globally. For comparison, credit cards handle roughly $4 trillion in annual volume.

But moving money with banks is not a modern experience. If you’ve sent an ACH or wire through a big bank recently, you kinda know what the experience is like for companies, too. The banks don’t give them some magical software to make all of this easy. Big banks don’t typically make magical software.

So companies either hire people to handle all of their payment operations or build and maintain their own integrations with banks in order to automate everything as much as they can. Either way, they’re throwing valuable people at the problem. And pretty much every company has to do the same thing, figuring out integrations with the same banks, reconciling money the same way.

“If everyone’s building the same thing and there’s no software company serving them, that’s a great recipe for a startup,” Matt told me.

So the three co-founders started Modern Treasury to build APIs into the global banking system. They do the hard work of integrating with banks and creating high-quality software building blocks, and give customers like Gusto, BlockFi, Equi, Marqeta, and Pipe a clean API to handle their payment operations.

Just three years old, it’s reconciling more than $2 billion every month. Last month, the company announced an $85 million Series C, led by Altimeter Capital with participation from Benchmark, Quiet Capital, and others (like Not Boring Capital). The valuation matches monthly reconciled volume: $2 billion.

More important than volume or valuation, though, might be the valuable strategic position Modern Treasury is locking in. They’re building an almost perfect API-first business, and one that can leverage its position in the workflow into becoming the system of record for a company’s money.

That’s Modern Treasury’s real goal, and its opportunity: to become the Salesforce for payments, with a modern twist. To understand it, we’ll cover:

Meet Modern Treasury. From YC to Unicorn in under three years.

Payment Operations? Understanding all of the pieces of the payments puzzle.

Bundled API-First System of Record. A strong and defensible strategic position.

The Big Opportunity: A New Payment Network. 👀

Let’s meet the Moderns.

Meet Modern Treasury

Successful startups take many paths. Some emerge victorious from a series of twists, trials, and pivots, like Discord. Others follow a straight line towards their North Star vision, realizing along the way that the opportunity was even bigger than they expected.

Modern Treasury is in this fortunate second camp. Its three co-founders knew the problem they wanted to solve from the beginning; they just didn’t realize quite how big the opportunity would be.

Dimitri, Matt, and Sam met at LendingHome where they built a mortgage marketplace that moved a lot of money to and from a lot of different people. They were responsible for the company’s payment operations, which included funding loans, collecting monthly payments, initiating investor deposits, handling transfers, and then reconciling all of it.

They had to hire people and build tools to connect to their banks, manage all of the money going out in the form of loans and coming back in monthly repayments, and reconcile their books. And still, their payment operations didn’t move at the speed a tech company should. When they looked around for companies doing it smarter who they could copy, they realized that everyone was doing the same thing they were. Even bigger companies were just throwing people at the problem and building in-house.

As entrepreneurs do, they decided they needed to build a solution. They applied to Y Combinator, got accepted, and got to work.

Fun fact: their application didn’t say Modern Treasury; it said Turnkey Treasury. When enough people asked them why they were building a treasury for turkeys, they searched domain names and snagged moderntreasury.com for $7.

Coming out of YC, the rafter (that’s a group of turkeys) wrote a post in August 2018, Introducing Modern Treasury, that clearly laid out the problem they were planning to tackle:

Since more and more payments start with software, we believe software should not just initiate, but also monitor and reconcile this payment activity automatically.

They also gave a clear, concise value proposition as it stood at the time:

Modern Treasury enables its clients to marry bank statements with the company’s business logic to provide an enriched history of the company’s financial transactions.

Three years later, Modern Treasury is holding true to the original vision, but the scope has expanded quite a bit. Today, it gives companies one API into banks to send wires, ACH, and real-time payments, automatically reconciles payments, and lets companies do continuous accounting instead of letting it all pile up until month end. It even built its own Ledger product that can be used to track… anything, from money to points and assets in video games. It powers the on- and off-ramps for large crypto companies like BlockFi, and just built support for wallets and real-time payment via the Signet Network.

And it is growing at an unfathomable clip.

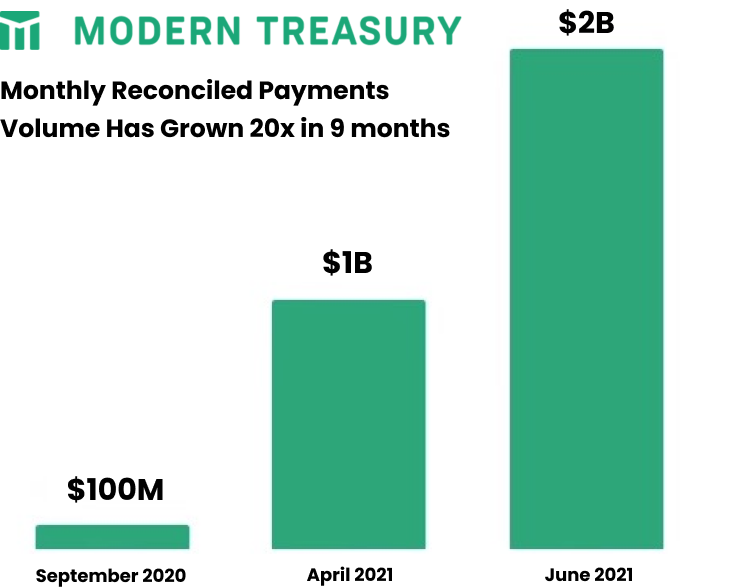

Last September, the company handled $100 million in monthly reconciled payment volume (RPV). This June, just 9 months later, it eclipsed the $2 billion RPV mark, food for 20x growth.

Of course, there are caveats. Reconciled payments volume isn’t a standard metric, the growth comes off of a small early base, and some very big companies are accountable for a lot of the jump, but still, it’s impressive. And investors have been impressed.

After raising its seed from YC in summer 2018, Modern Treasury raised a $10M Series A from Benchmark in December 2019 and partner Chetan Puttagunta joined the board, which in the B2B software world is like getting Michael Jordan to join your team. In 2021, Altimeter’s Ram Woo led a $35M Series B in January and an $85M Series C in September, in which Benchmark, Quiet Capital, and little old Not Boring Capital participated. When insiders do back-to-back rounds that quickly, at a big valuation step-up, that is typically a very strong signal.

A $2 billion valuation on $2 billion in monthly reconciled volume is aggressive, but these are smart investors. Blaming a hot market for high prices is lazy. What are they seeing?

First things first, this is an enormous market with a very low product bar. No other industry measures total volume in the quadrillions, and neither ACH nor wires are known for their excellent user experience. Over the last decade, integrating with banks on the consumer side made Plaid a $15B company and making it easy to accept credit cards turned Stripe into a $95B juggernaut. There’s a lot of money in making it a lot easier to work with legacy financial institutions.

In such a market, then, the question isn’t opportunity size but a particular company’s ability to capture it. To that end, Modern Treasury has shown investors enough to convince them that it’s a credible contender to win the market over the past three years across a number of dimensions.

Team. The founding team is strong and has not only relevant experience, but relevant experience together. They’ve also proven their ability to hire top talent in an excruciatingly difficult hiring market.

For example, in September, Shruthi Murthy announced that she was joining as Head of Engineering, from WhatsApp, where she had been an engineer since 2012 and recently headed up WhatsApp Payments. Matt told me that the company is actually pacing ahead of its engineering hiring goals this quarter, which is not something I’ve heard from any other company.

The team is now 51 people strong, with ten more starting next week, up from 35 people in August. But the number of people is less important than the quality.

Beyond the numbers, there’s a certain team je ne sais quoi. A couple of weeks ago, I got to join the team for their weekly Coffee Break (they did one with my friends at Acquired and recorded it, too). Even on Zoom, I could feel the good energy, and the team asked very smart questions. A few brought up the company’s writing culture, which is always a plus in my book.

Customers. Building a company to whom increasingly large companies will entrust responsibility for increasing percentages of their money is a hard challenge. You need to somehow convince an impressive first customer to sign up, and then parlay that into the next, slightly larger customer, and then the next, and the next, and the next. It’s kind of like those challenges in which people take a random household item and try to trade for more and more valuable things until they end up getting a house.

Modern Treasury has been strong on the logo front, too. It parlayed its first customer, Sana, a small business health benefits company, into relationships with larger ones like Gusto, Marqeta, Revolut, BlockFi, each of whom rely on different combinations of Modern Treasury building blocks.

It’s especially impressive that Modern Treasury works with so many fintech companies, and speaks to their position as Software Switzerland, a neutral party between banks and companies with no ambition to dip into the flow of funds.

These early dominoes were likely the hardest to topple over. They’ll help push the bigger ones, which will help push the bigger ones.

That doesn’t mean that it will be easy to sign the companies that move the largest sums of money -- big insurers, healthcare companies, real estate firms, and more -- but it does mean that Modern Treasury is in the best position to do so.

Finally, of course, there’s the product itself. Like the best software companies, Modern Treasury is able to strike the balance between quality and speed, shipping new software without losing customers’ money. It’s a “go slow to go fast” mentality.

Front and center on its home page, Modern Treasury says that it “makes payment operations simple, scalable and secure.”

Which begs the question… what is payment operations?

Product: Payment Operations Software

I have to be honest. Before meeting with Matt and Dimitri, I knew that Modern Treasury had a buzz around it, and that it did something in fintech, and that it had its own ledger product, but I didn’t really know what Modern Treasury does. That’s because payment operations, like a referee, is an ideally invisible role. It’s just supposed to work.

But payment operations keep the economy moving. In its Beginner’s Guide to Payment Operations, Dimitri wrote that there were three times more open payment operations roles on Indeed (95,900) than there were open accounting roles. The responsibilities ranged from servicing loans, to sending and reconciling ACH and wire payments, to posting payments for healthcare bills, to making sure that international payments go through.

Generally, Payment Operations includes all the workflow around money movement itself. This includes:

Initiating payments

Setting up approval processes

Tracking and attributing sent and received funds

Resolving payment failures and returns

Reconciling transactions to bank statements

Booking payments to the general ledger.

These workflows traverse numerous systems within a company, ranging from bank portals to spreadsheets to ERP software.

Before Modern Treasury, companies had to hire dedicated people and even full teams to manage all of it. Airbnb, which has to collect money from guests, pay out money to hosts, deal with disputes, and manage all of the complexities with managing marketplace payments, has a full page dedicated to its payments team, including twelve current open roles.

Airbnb is a non-”payments” tech company, and it still needs to throw people at the payments problem, including engineers to build better in-house solutions and people to actually do the work. There’s even a content strategist.

Every company that does meaningful revenue has payment operations, whether in the form of dedicated headcount or people who handle payments work on the side. That might be an engineer building bank integrations when they’d rather be building something sexier, or finance team members spending part of their team sending checks and wires, reconciling payments, and closing the books every month-end.

Modern Treasury exists to build software to make all of that faster, more reliable, and more efficient. Here’s the marketing version of what they do:

Let’s dive a little deeper. Modern Treasury has three core products — Payments, Virtual Accounts, and Ledgers, which include direct bank connections, software features for automatic reconciliation and payment counterparty onboarding, and integrations with accounting systems. These products touch a variety of roles inside of a company, from finance to compliance to engineering. All of its products are meant to free up teams’ time to focus on their core product and do a faster and more accurate job than whatever software or processes a company might build itself.

Modern Treasury’s products include both APIs and user interfaces. On Invest Like the Best, Benchmark’s Eric Vishria describes the two types of B2B software: people interact with software through Graphical User Interfaces (GUIs), software interacts with software through APIs. Modern Treasury makes both.

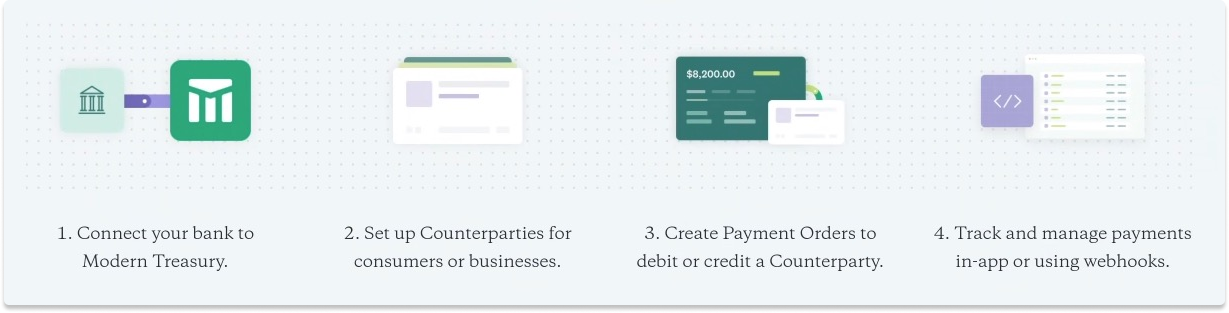

For most customers, it starts with Bank Connectivity.

Companies can connect all of their bank accounts, even from different banks, in one place, so that they can interact with all of their cash and payments through Modern Treasury’s clean interfaces or use APIs to plug the data into their own software.

From there, a company might use Modern Treasury’s Payment APIs to build payments workflows that send money right from their bank accounts at whichever bank they use to “counterparties,” or other businesses, partners, or customers they need to pay or charge.

Importantly, by using Modern Treasury, many businesses can skip sending money through a payment processor or bill pay solution, making payments faster and cheaper.

Beyond smoother and faster payments, Modern Treasury helps businesses track and understand their payments and accounts better, too.

Once your bank accounts are plugged in, Modern Treasury can automatically reconcile payments -- match the specific transaction to the payment posted in the account. It can even kill the dreaded month-end close process by powering continuous accounting, which syncs reconciled payments and bank transactions to your general ledger automatically. In both cases, it takes time-consuming, labor-driven processes and replaces or facilitates them with software.

Last but not least, this June, Modern Treasury rolled out its own Ledgers product.

Every business keeps a ledger -- line-by-line credits and debits -- for bookkeeping purposes, and every accounting software -- Quickbooks, Xero, Netsuite -- works well for that use case. But digital products themselves need ledgers that update in real-time in the product. Think about your balance in your Robinhood account, your Uber credits, or the number of ETH your MetaMask wallet, and historically, they’ve had to build them themselves.

With Modern Treasury’s Ledgers APIs, developers can spin up ledgers for anything from digital wallets, to investment apps, to in-game currency — anywhere you need to store and track value in real-time -- in, you guessed it, a few lines of code.

Talking to Matt and Dimitri, they described their various products as “building blocks” for payments, and they are, but what struck me in researching this piece is that they behave more like puzzle pieces. Customers can use each product individually, but the more pieces they snap into place, the more cleanly everything works. All of it is backed by enterprise-grade controls that are really important to big companies. Ideally, as Modern Treasury builds out its suite of products and integrations, customers will be able to turn to one, trusted source for all of their payments needs.

You’ll remember that old Jim Barksdale quote that I use so often: “There are only two ways I know of to make money: bundling and unbundling.” Modern Treasury believes that when it comes to payments, bundling is the way to make money.

Bundled API-First System of Record

Modern Treasury’s growth gets all of the headlines, but it’s strategic positioning is where the real magic lies.

Modern Treasury makes API-First workflows…

...and leverages the data flowing through its APIs to become the system of record.

When Dimitri told me that he wants Modern Treasury to be the Salesforce for Payments, this is what he meant. I’ll explain.

According to Tomasz Tunguz at Redpoint:

A simple way of dividing the software world is system of record vs workflow application. Systems of record are the single source of truth about a particular department or company. On the other hand, workflow applications enable workers to do work.

The next shift in SaaS will see startups leverage their workflow roots into disrupting systems of record by changing the buying process.

That describes Modern Treasury’s strategy to a T.

First, API-first. In APIs All the Way Down, I made a graphic that I now use too much to describe an archetypical API-first business:

Anything that a company does that is mission critical but non-core is the ideal candidate to be replaced by APIs. Payments are obviously important to a business, but they’re not a differentiating factor. I’m not going to list my house on Airbnb because they pay me on time, but I will not host on Airbnb if they don’t pay me on time. As Matt explained,

Bank integrations are undifferentiated heavy lifting. Companies want clean APIs and developer tooling like what they get in other areas (ie Twilio) so that they can focus on their products.

By building APIs that make it easy to connect to banks and make payments, Modern Treasury has been able to put itself in a very sticky spot within a company’s workflows. It’s used that position to build products on top of the data flowing through the APIs -- like reconciliation and Ledgers -- that make it the system of record for a company’s money.

As a result, it’s not just the engineers or even finance teams that come to rely on Modern Treasury, but anyone in the company who needs to know what’s happening with the money that moves through the company. Modern Treasury hasn’t been purist about being an “API-only” company; it has dashboards and tools that people across departments rely on.

Dimitri told me about one customer, with about 500 employees, that has 72 monthly active Modern Treasury accounts used by employees from customer support, engineering, product, accounting, audit, operations, and finance. Engineering might set up the integrations, but then Modern Treasury becomes the one source of truth for anyone in the company, just like Salesforce is.

Which brings us back to bundling.

The other day, Mario and I wrote about the fact that instead of trying to replace Discord, entrepreneurs are building on top of it. It’s a system of record for group conversation. Despite the fact that Salesforce isn’t the most beautiful product or best experience, its position as the system of record means that entrepreneurs who want to serve Sales and Marketing teams need to integrate with and build on top of Salesforce instead of trying to replace it.

Likewise, Modern Treasury believes that given its position as the system of record for payments, it will make sense for companies that build best-in-class fintech products to integrate with Modern Treasury instead of trying to replace it. The more companies that integrate with Modern Treasury, the stickier it becomes, and the more likely it is to get very big.

In some cases, Modern Treasury will integrate with other companies’ products. In others, it will build its own. As the system of record, it has the luxury of making that choice: it believes payment operations should be bundled, the question is just whether to build, buy, or partner. Other companies may not have the same luxury; if they want to move money, they’ll need to build on Modern Treasury.

That’s why Modern Treasury is focused more on reconciled payments volume than revenue. Being able to reconcile payments means that Modern Treasury has all of the data it needs to be the system of record.

From there, it can go after the really big opportunity.

The Big Opportunity: A New B2B Payment Network

A bet on Modern Treasury is a bet that the big banks will continue to serve the world’s biggest sectors -- healthcare, real estate, education, payroll, manufacturing -- the ones that rely on wires and ACH and soon, Real Time Payments (RTP) for their biggest payments.

That could be a bad bet. Very strong fintech companies are attacking the banks. Web3 might improve so dramatically and become so much more reliable in the next decade that it doesn’t make sense for even the world’s stodgiest industries to send money over old rails. Stripe’s push into web3 might be a death knell for the banks.

But Modern Treasury has two sets of opportunities ahead of it, one very very big and one absolutely massive.

The very, very big opportunity is to continue to expand, to do what they’ve been doing for the last three years on a larger scale, and become the one-stop shop for companies’ payment operations. That means integrating with more banks, pushing into new countries, expanding the product offering, integrating third-party tools to become a one-stop shop, and serving larger and larger customers who move enormous volumes of money. In this world, it will look a lot like a Twilio, crucial infrastructure that’s able to charge a platform fee and a variable fee every time money moves.

But if you believe three assumptions:

Banks remain the way that businesses move large amounts of money

The US adopts real-time payments like other countries have (Signet is here, CHIPS is live, FedNow is coming in a couple years)

Modern Treasury is able to do to payment operations what Stripe did to credit cards and Twilio did to messaging, becoming the de facto solution for companies’ payment ops

..then Modern Treasury’s enormous opportunity might be that it can facilitate payments for enough banks and companies that matter to rebuild the payments network.

Once enough big money movers use enough of Modern Treasury’s products, Modern Treasury could build its own “closed-loop” network through which businesses could move money to each other, from bank account to bank account, in real-time.

It could reconcile the transactions instantly. It could facilitate real-time payments. It could keep the books up-to-date automatically.

As money movement becomes data movement -- two banks updating their respective ledgers -- a software company that works with the banks and is adept at moving and understanding that data could rebuild the global payments network.

In this scenario, Modern Treasury ends up looking like a Modern VISA, which, as it stands, is a $458 billion company that itself started out as a network of banks.

It’s a lofty vision, and every payments company would love to close the loop, but after just three years, Modern Treasury seems best-positioned to make it a reality in the quadrillion-dollar bank-dominated piece of the market. Now, it’s about execution.

If you want to go help build it, Modern Treasury is hiring. Go build the future of money movement:

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Thursday,

Packy

The Big Opportunity: A New B2B Payment Network

Can you maybe expand on how this plays out? Doesn't this require deeper integrations with the banks themselves and build those pipes to create a parallel network to Visa/Mastercard?

And by deeper integrations, I mean each bank has to spend time, effort and money to work with a central network like Visa. This was successful because Visa originated from Bank of America and then evolved to become a consortium of banks before becoming a publicly listed company. What would be the reason for banks to spend this effort to work with a new private player without significant return on the investment?

Money movement becoming data movement - this is not the case due to regulations with respect to KYC and AML and these are today handled only by banks and the card networks. If Modern Treasury has to become a central network, then it has to start handling KYC and AML guidelines which they are not doing today.

Just to add, I have built Hypto.in - a payment aggregation platform in India which currently processes 300K transactions per day and $150 Mn per day for over 2000 businesses. We had the same vision when we started building Hypto but learnt that the barriers to create a new payment network are extremely high and in my opinion, it does not seem like an organic evolution for Modern Treasury to become a payment network.

Packy is becoming the Cal Ripkin of modern business journalism....the hits keep coming