Braintrust: Fighting Capitalism with Capitalism

Or, how web3 businesses can use tokenomics to create and capture long-term value

Welcome to the 2,262 newly Not Boring people who have joined us since last Monday! Join 103,299 smart, curious folks by subscribing here:

🎧 To get this essay straight in your ears: listen on Spotify or Apple Podcasts

Hi friends 👋,

Happy Monday!

I was planning to write this Sponsored Deep Dive on Braintrust and send it last Thursday like I normally do for Sponsored Deep Dives, but as I got deeper into the piece, I realized that Braintrust is a perfect case study on how a web3 protocol can compete with, and potentially beat, web2.0 incumbents.

It’s playing out now, in real-time, and is one of those approachable “real use cases” that supporters and skeptics alike long for.

So this is a Sponsored Deep Dive on a company that I invested in via Not Boring Capital last year. You can read my Sponsored Deep Dive selection and thought process here, but on a Monday, not a Thursday.

I’ve only written one other SDD on a Monday – Solana Summer – and like that piece, I’m only doing it because this is a piece that I would have written on a Monday, and I’m writing it just like I would write a Monday piece. I’m not selling anything – there’s no tracking link anywhere – and I’m not telling you to invest.

It’s just that, in Braintrust, I found the perfect vehicle for so many of the arguments I’ve been trying to put into words.

Disclaimer: Brainstrust has a publicly traded token – BTRST – so let me yell this as loudly as I can: THIS IS NOT INVESTMENT ADVICE. I mean this. BTRST is worth multiples of what it was when I invested last year. The whole crypto market has been volatile, and BTRST has been more volatile. Not Boring Capital owns BTRST tokens, but I have no idea what the price will do in the next day, week, month, year, or decade. The team has said publicly many times that they don’t care what the token price is. Always DYOR.

Let’s get to it.

Braintrust: Fighting Capitalism with Capitalism

In the very first post I wrote about web3 last January, The Value Chain of the Open Metaverse, I wrote:

That’s what excites me most about Web3: the new business models it enables and the new value chains that emerge when the middleman is removed.

I wrote that piece as someone who had previously been curiously skeptical about web3. The first thing that clicked for me was the understanding that as people spent more and more time online, in ~*the metaverse*~, we would want to buy, own, and sell our own digital things without needing to rely on, and more importantly pay an extractive take rate to, someone sitting in the middle.

I made this beautiful graphic to help visualize what that looks like:

As you know, my brain can get out there, and an imagined future in which we rely more heavily on digital assets and would like to own and transact with those assets wherever we go in digital space was enough for me to buy in to the web3 vision.

But I also understand that many people want to see “real use cases” before getting too excited. “Just show me one thing that a normal person would use in their everyday life,” these people reasonably demand, “that is better than the existing alternative because of the use of web3 tools.”

Allow me to introduce Braintrust.

Braintrust is a user-owned talent network that is growing fast and reaching real scale just eighteen months after launching the public beta of the protocol last June. $37 million in Gross Service Value (GSV) – what Clients pay Talent – has flowed through the network, with nearly twice that contracted for the coming months.

This isn’t theoretical or conceptual. It’s happening now, matching real people with real jobs at top companies. You can watch the growth daily on its public dashboard. That dashboard also shows that 2,373 total jobs have been completed at an average project size of $72,474 and duration of 228 days.

Braintrust’s market cap is $315 million, its fully diluted market cap is $896 million, and in December, it announced a fresh $100 million token sale to Coatue, Tiger, and existing investors to fund grants to grow the ecosystem.

This is web3 in the real-world.

Braintrust is not a radically new product or business model. It doesn’t require you to believe that digital objects have value or promise multi-thousand percent yields. Braintrust just connects companies looking to hire flexible technical talent with that talent, and charges a fee for doing so. Simple.

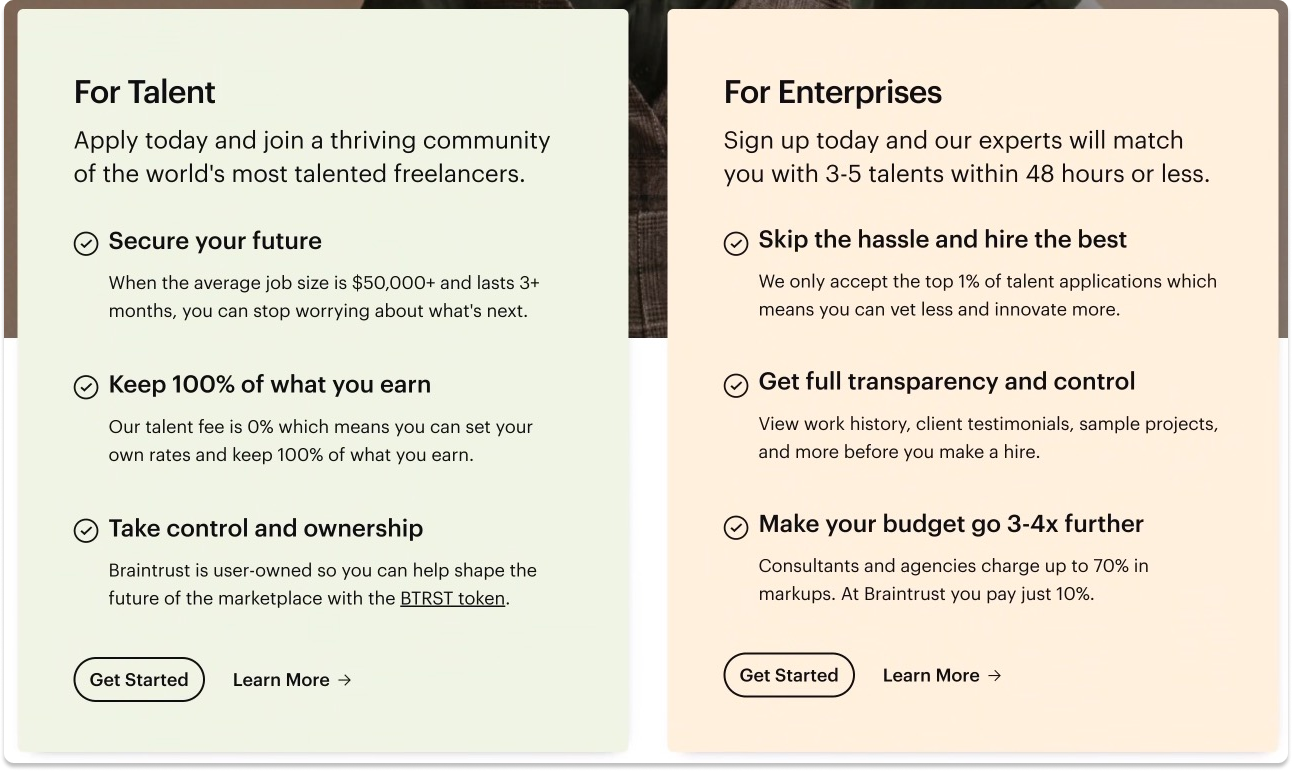

It looks like a normal talent marketplace on the surface. This is its homepage:

It doesn’t slap you in the face with web3. You need to scroll to the fifth section to find the first glimpse: “Take ownership: Braintrust is controlled by you, the Talent, through the BTRST token.”

The value proposition to the two sides of the marketplace – Talent and Enterprises – mentions the token as just one of six reasons to use Braintrust.

Braintrust is a clear distillation of an incredibly important point: good tokenomics can enhance a strong value proposition, but can’t replace a strong value proposition.

Side Note: we’re going to talk about tokenomics a bunch, so let’s define the term. I like to think about it as designing economies by setting rules for how tokens are distributed, what participants can do with them, and how value accrues to them. Tokenomics are one reason tokens have advantages over equities: they can be programmed to do more. OK, back to it.

But even without mentioning a token, the reasons that both sides of the market start using Braintrust are clear:

Enterprises, or Clients, use Braintrust because they can find and hire vetted technical and design talent globally quickly for an industry-low 10% fee. They find the right talent for their project in as little as three days instead of many weeks.

Talent uses Braintrust because they can find high-paying, flexible technical work at top companies like Nike and Porsche and pay no fee on what they earn. They can quit their full-time jobs, get as much work as they want, and log off when they want.

The fact that they can also earn tokens in order to have a vote on the future direction of the network is icing on top, but important icing. When you trust a platform with your livelihood, you want to make sure it can’t break that trust.

Instead of being the network’s raison d’etre, web3 is a toolkit that Braintrust uses to do the long-term strategically rational things that all marketplaces should do but that many can’t because of incentive and time horizon misalignment, like keeping take rates minimally extractive.

To be clear, using web3 tools doesn’t mean that Braintrust is perfect. Tokens aren’t magic beans. This Redditor provides a good first-hand account as a freelancer with both pros and cons. Community governance can be messy and imperfect. Tokens invite people to game or scam the system. I’m sure there will be many unhappy Clients and Talent over the years.

Braintrust isn’t a foregone conclusions, but a series of bets:

That good tokenomics can lower costs and unstick and accelerate the flywheel

That a user-owned network can stay minimally extractive longer than an investor-owned one

That a minimally extractive network can actually be the most valuable

That it can eat so much of the global talent market that a small 10% take rate becomes a very big number

It’s early, but the bets seem to be paying off. Since founding Braintrust in 2018, co-founders Adam Jackson and Gabriel Luna-Ostaseski, along with the core teams and community, have built Braintrust into one of the most pragmatic and fastest-growing web3 businesses on the planet.

But there’s a long way to go to achieve the vision and pull all talent network business onto its protocol. Braintrust has done $37 million in volume all-time. Upwork, a Web2 talent network, did $904 million in its last quarter alone, Fiverr did ~$260 million. Deloitte did $50.2 billion in revenue in 2021. In all, companies spend trillions of dollars on talent every year. In that context, Braintrust’s volume to date should look like a blip in a year or a decade. And now that Braintrust has gone full DAO, it’s up to the community to pull it off.

Ultimately, Braintrust is a familiar business model in one of the oldest businesses in the world – hiring – with a few modern enhancements. Its success will be measured by how it competes against public incumbents over time.

The question for Braintrust is: can a user-owned network both create and capture more value than its investor-owned counterparts?

If by the end of this piece, you can understand how the answer might be yes, then you understand web3. Braintrust is the gateway drug. So today, we’re going to go deep on how it all works:

The Braintrust Manifesto

Web2 Marketplaces and the Take Rate Temptation

How Braintrust Works

Value Accrual and the Protocol Upgrade

The Braintrust Thesis & How User-Owned Network Wins

But first, I want to turn it over to Adam to set the stage.

The Braintrust Manifesto

In October, Braintrust co-founder and CEO Adam Jackson joined my friends Ben and David on the Acquired LP Show. At one point Ben asked him how his “incendiary” comments about Web2 marketplaces jibed with his history as a three-time Web2 marketplace entrepreneur.

Adam’s answer is a modern Greed is Good speech.

I’ll title it Fighting Capitalism with Capitalism. It’s a long block. Read it.

I’ve always felt that if something is good for business, but your customers hate you, there’s opportunity there for competition. Now I get called a Socialist, like somebody from Bloomberg called me a Socialist, are you fucking crazy? I’ve been making money my whole life. I’m a red-blooded, red meat entrepreneur. I helped start a hedge fund, right? I’m not a Socialist.

When marketplace operators or any company is abusive to their customers to the point where the customers are trying to pass laws to change… like, I think there’s opportunity. I don’t believe in the government regulating those things. I think the AB-5 here in California was complete un-well-thought-out corrupt horseshit just like everything else the state does, but these are market-created problems that markets can solve. So if you operate a marketplace and half your customers hate you, that’s an entrepreneur’s dream.

So the dream here is: new technology – blockchain – powering a new organizational model – user-owned, user-controlled – eats away at the central rent seekers who are disproportionately extracting value. Look, without blockchain, there’s no way to compete with these guys. There’s no one more operationally excellent than DoorDash, you have to really tip your hat to them, it’s an amazing app and an incredibly well-run business… but if they’re being abusive to a major part of their marketplace, then the door’s open for disruption.

If web3 had to elect a President to appeal to the widest swath of the population, Adam might be the guy. His is a pragmatic, no bullshit approach. That speech sets the terms for the rest of the piece and makes it clear what he’s going for.

Braintrust will be less extractive than the incumbents, not out of a sense of charity but out of a sense of capitalism. Your take rate is my opportunity, in practice.

Adam wants to make a lot of money through the ownership of his BTRST tokens over time, which means value will need to accrue to token holders.

The rest of this piece is about figuring out whether web3 makes those two seemingly contradictory ideas – extracting less and capturing more value – possible. (Hint: I think it can.)

That requires understanding how marketplaces have typically worked.

Web2 Marketplaces and the Take Rate Temptation

First things first: I think Web2 marketplaces are great. I ordered dinner on DoorDash last night. I took an Uber home the night before that. I’m staying in an Airbnb later this week.

Marketplaces are some of the biggest and most impressive businesses built in the past two decades. Even after recent selloffs, they’re worth hundreds of billions of combined dollars, all value created in the past decade or so (except eBay, which I think came out of Bell Labs in the1950s):

These marketplaces not only organized existing markets and stole share from incumbents; they grew the markets in which they operate through their existence. The vacation rental market is bigger because Airbnb exists. Ridesharing is bigger because Uber exists. Done right, marketplaces attract and match new supply and new demand while removing friction and lowering costs. Great stuff. Love Web2 marketplaces.

But there are also challenges with the model, or opportunities for improvement:

Like the fact that marketplaces need to pay a lot to acquire both supply and demand, often over and over. See: the bloody Uber v Lyft battle.

Or that so many successful marketplace businesses end up becoming advertising businesses – great for the business, annoying for the customer. See: all of the national fast food chain advertisements at the top of your DoorDash screen.

Or that at some point, in order to increase supply, they drop the quality bar and people figure out how to game the system and it gets really hard to figure out what’s good and what’s not. See: Amazon third-party sellers.

Or that successful marketplaces often increase take rates in order to increase profits once they believe participants are sufficiently locked in that they won’t leave. See: practically every marketplace in the history of marketplaces.

These moves don’t happen because every Web2 marketplace employs some Mr. Burns figure who heartlessly steals whatever they can from the little guy for sport. (Except for whichever diabolical DoorDash employee decided to keep drivers’ tips.)

They happen because of the nature of the model. These are businesses run by executives and boards with a fiduciary responsibility to generate max profits and return them to shareholders. Again, that’s not bad. That’s capitalism. I fucking love capitalism.

It’s just that, too often, marketplace businesses start extracting earlier than is optimal for the long-term success of the business because they need to prove to shareholders that they can get profitable. Marketplaces can be really expensive to get off the ground. They need to raise and spend a bunch of money to get the flywheel spinning. Once it’s spinning, they need to increase their cut of the economic activity on the platform to generate a return for investors.

That cut is the take rate, which Benchmark’s Bill Gurley defines as, “The amount that the marketplace charges as a percentage of GMS (gross merchandise sales), which typically represents net revenues for the marketplace.” The 30% Uber charges drivers, the 30% Apple charges developers, and the 10% that Braintrust charges Clients are all the take rate.

Increasing the take rate isn’t bad or immoral or anything. Companies talk about increased take rates with pride in earnings calls and shareholder letters. As one example, in its most recent shareholder letter, Fiverr referred to its 140 basis point take rate increase as an “improvement.”

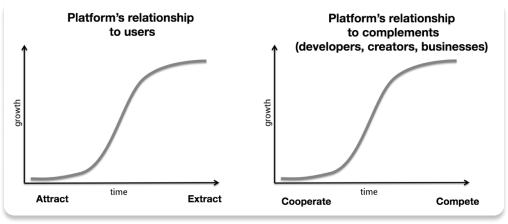

One way of looking at why this happens is that once they’ve locked both sides, marketplaces and platforms can move from attraction to extraction. In the Value Chain piece, I referenced Chris Dixon’s Why Decentralization Matters on this topic, writing:

Once they’ve built those network effects, though, and they know that users, developers, and businesses are locked in, they switch from “attract” to “extract.”

The more positive interpretation of increased take rates is that the ability to increase take rates proves that the marketplace is adding more value. It’s helping them find new customers, or lower costs, or do any number of things that would justify paying more. If a marketplace can increase a take rate from 10% to 20% without much attrition, they were either being too generous before, or their product became a whole lot more valuable to its users.

But “without much attrition” is doing a lot of work in that last sentence. Whether that attrition shows up today, tomorrow, or in five years, increasing take rates beyond levels that marketplace participants find fair sows the seeds for a marketplace’s eventual demise.

In a classic April 2013 blog post, A Rake Too Far: Optimal Platform Pricing Strategy, Gurley wrote about the danger of thinking too short-term when it comes to setting a take rate:

It may seem tautological that a higher rake is always better – that charging more would be better than charging less. But in fact, the opposite may often be true. The most dangerous strategy for any platform company is to price too high…

If your objective is to build a winner-take-all marketplace over a very long term, you want to build a platform that has the least amount of friction (both product and pricing)... In order for your platform to be the “definitive” place to transact, you want industry leading pricing – which is impossible if your rake is the de facto cause of excessive pricing.

The whole piece is worth reading, but the point is this: increasing take rates feels good in the short-term, but it’s strategically sub-optimal if you want to build the de facto marketplace long-term. Increasing take rates can lead supply and demand to look for alternatives.

When a marketplace charges more than the value it provides, participants will look to disintermediate, or go around, the platform.

This was the challenge that many of the on-demand cleaning services faced in the early 2010s. People would use their free three-hour cleaning, find a cleaner they liked, and just ask for their number and tell them they’d pay cash, skipping the fee. Beyond the initial match, those companies didn’t do much to earn their fee.

Same for TaskRabbit. When I was at Breather, I’d find Taskers I liked and work with them directly. They tried to put punishments in place to discourage disintermediation, but that was the wrong approach: they needed to create incentives for Taskers to stay instead of treating them like bad kids. I’d imagine IKEA ended up buying it because they could actually integrate the Tasker more deeply into the ordering flow, providing a reason to keep using TaskRabbit by giving Taskers IKEA-specific superpowers.

Instead of increasing the fees you charge all of your users, Gurley recommends that marketplaces figure out other ways to make more from those users who want more from you. Back then, he brought up advertising as an example. If you can get some of the suppliers in the marketplace to pay for ads, you can effectively earn a higher take without needing to charge everyone more.

Braintrust thinks tokens work even better.

How Braintrust Works

The simple idea behind Braintrust is that it is a talent network that charges Clients an industry-low 10% fee and actually pays Talent a negative take rate by rewarding them with tokens, and that the only way for those things to change is for the users who would be impacted to vote to change them.

Here’s how it works.

According to the Braintrust Whitepaper, “Braintrust is a decentralized talent network that replaces our outdated, fragmented labor market with a liquid, algorithmically-controlled marketplace governed by network participants.”

There are two sides to the network:

Clients like Nike, Porsche, Atlassian, NASA, and more, post their “asks” by posting jobs to the network as specifically as possible, including required skills, geography (or working time zone), and rate.

Talent, mainly engineering and design talent at this point, respond to posts with their “bids” by submitting job proposals.

Talent sets their desired rate and pays no fees. Clients pay a 10% fee on top of the Talent’s invoiced amount, which is used to sustain the network. To be fair, the 10% is coming from somewhere – if the Clients weren’t paying it, maybe they’d be willing to pay Talent 10% more – so the net result is more like a 10% take rate than no fee to Talent and 10% to Clients.

Importantly, all payments occur in local currency – a US-based Client might pay USD and Braintrust will pay the Talent in their local currency. It’s entirely possible to use Braintrust as either a Client or Talent without ever thinking about crypto.

Braintrust can afford to charge such a low take rate for a couple reasons:

Software. The protocol handles a lot of the basic functions of the marketplace – matching talent, settling payments, and rewarding participants – using software at practically zero marginal cost.

Tokens. Braintrust has a native token, BTRST, that it uses to grease the flywheel, incentivize behavior that’s good for the network, and pay for things that a traditional marketplace would need to hire for.

Braintrust pays for everything the network needs through the money it’s raised, the 10% fee Clients pay, and BTRST tokens from the treasury.

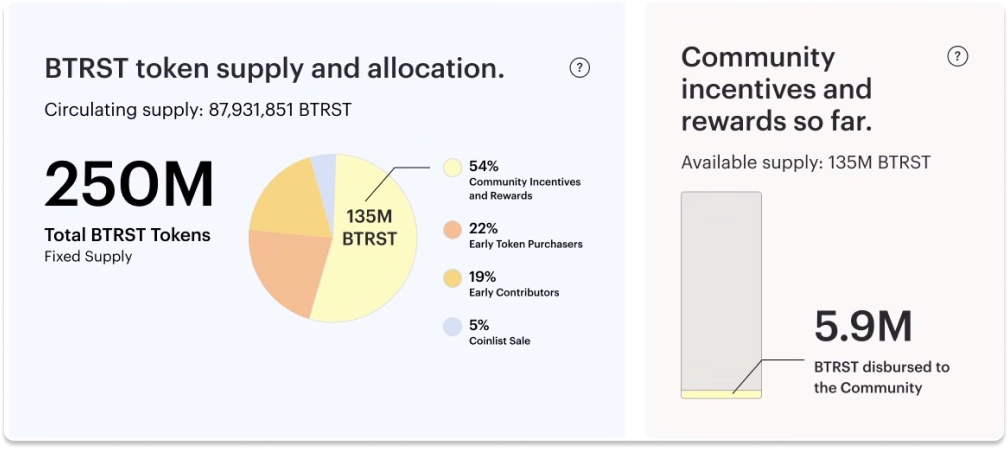

Here’s how token ownership breaks down currently:

To get the network off of the ground, Braintrust raised roughly $24 million from VCs in addition to $11 million via a Coinlist crowdfund last September (Not Boring Capital invested at the Option 2 Terms). Early angel investors and VCs, including Variant, Multicoin, ACME, Hashkey, and more, own 22% of Braintrust’s tokens on a multi-year lockup and crowdfund purchasers own another 5% on a 3-6 month lockup. In December, Coatue and Tiger bought $100 million worth of tokens from the treasury.

There are a couple of important questions to flag here, which I’ll try my best to answer:

If VCs invested, is it really user-owned? This is the Jack Paradox: “You don’t own web3, the VCs and their LPs do. It will never escape their incentives.” Now, as a web3 VC who invested in Braintrust, I’m biased, but a few things:

These businesses still need money to get off the ground when they’re unproven, and that’s what venture capital is good at doing.

22% investor ownership, and 41% investor + team ownership, is much less than most businesses have when they go public.

Web2 businesses don’t even have the concept of just giving half of the ownership to the community; the most forward-thinking let their best users buy a small sliver of pre-IPO shares.

More pressure comes from who companies IPO to: public market investors are typically much more unforgiving than VCs.

Why won’t VCs make Braintrust do the same things that investors supposedly make web2 marketplaces do? Most marketplaces feel the pressure to get profitable not from their VCs, but from the public markets. Uber was getting ready to IPO at $120 billion until public market investors called it on lack of profitability and the fact that it didn’t “winner-take-all” its market and therefore couldn’t increase prices. Web2 companies’ ownership gets more institutional when they exit; web3 companies get more user-owned when they launch their token. Plus, VCs know they won’t be able to fund web3 companies if they get a reputation for screwing communities. DAOs often vote on which VCs to let on the cap table.

Don’t Web2 companies have users who own shares too? How is this different? Let’s say I own $10k worth of Amazon shares and am an Amazon customer, and let’s also say that they put the decision to raise Prime prices $10 to a vote (which they wouldn’t, but play along). That $10 is meaningless to me relative to my shares. If, however, I own $10k of Braintrust and they propose a 10% fee increase, and I make $72k per gig on Braintrust, then the vote will have a $7,200 impact per contract on me. I’d need to have a really good reason to vote to increase the fee on myself - like the network not being able to survive on 10% fees.

Plus, the $100 million Coatue round is an interesting example of how investors can dig in and participate in the network. Coatue and Tiger, who have long been investing in web2 marketplaces, reached out to buy more than they could find on exchanges. They came to a deal to buy $100 million of tokens from the Treasury, the proceeds from which will go to fund grants (which are paid part in USDC and part in BTRST). As part of the deal, Coatue, which has been acquiring recruiting firms for years, offered to lend the network recruiters in order to build out a recruiter talent network. They’re actively participating in the network with more than dollars.

Now, all of this is playing out in real time and whether VCs really won’t, and more importantly can’t, push protocols to overly extract will be crucially important to watch.

Early contributors own 19% of the network. There’s actually no Braintrust, Inc.; most of the work in building the project was done by six Nodes – Freelance Labs, HexOcean, SnowFork, Accelerated Labs, Distributed Labs, and Muses – that did everything from designing the protocol and tokenomics to marketing the project early on, and now handle things like processing payments, handling currency conversions, and importantly, onboarding and managing relationships with large clients like Nike and NASA that need a lot of handholding, paperwork, compliance, and security.

Adam and Gabe, for example, technically work for Freelance Labs, which designed the tokenomics among other things, and the top Client salespeople on the network are a team of three salespeople who set up their own Node.

Braintrust eats its own dog food, too. The Braintrust website, including engineering and design, was built entirely by Talent on Braintrust.

These nodes and early contributors, essentially the founding team split out across multiple organizations, collectively own 19% of tokens. Plus, the 10% that Clients pay goes to pay the Nodes for their ongoing work, who can in turn do things like pay themselves and pay Talent. Hold this thought; we’ll return to the destiny of that 10% fee shortly.

That leaves the 54% Community Rewards and Incentives Pot. These are the BTRST tokens the network uses to incentivize good behavior and reward people and businesses for doing things that a traditional marketplace would need to hire for, like referrals, building, and onboarding.

There are a few main types of contributors who receive Community Incentives and Rewards:

Connectors are anyone who refers talent or clients to the network. They receive rewards for bringing people into the network, and then receive a portion of their referrals’ invoices. Anyone can become a Connector and refer Talent, including individuals like me, professional recruiters, or even recruiting agencies.

Vetters are people who screen new candidates to ensure that they meet Braintrust’s quality bar. These people must complete the courses on Braintrust Academy, for which they receive tokens, and then receive BTRST tokens when they complete screens.

Talent can receive tokens for filling out detailed profiles, taking courses (mini-learn-to-earn), and successfully completing jobs.

Grant Recipients can receive tokens for doing work for the network in three categories: Ambassador Grants, Builder Grants, and Educator Grants. Braintrust is using the $100 million it recently raised from Coatue and Tiger in part to create a Grants Program, which is in its first MVP wave now.

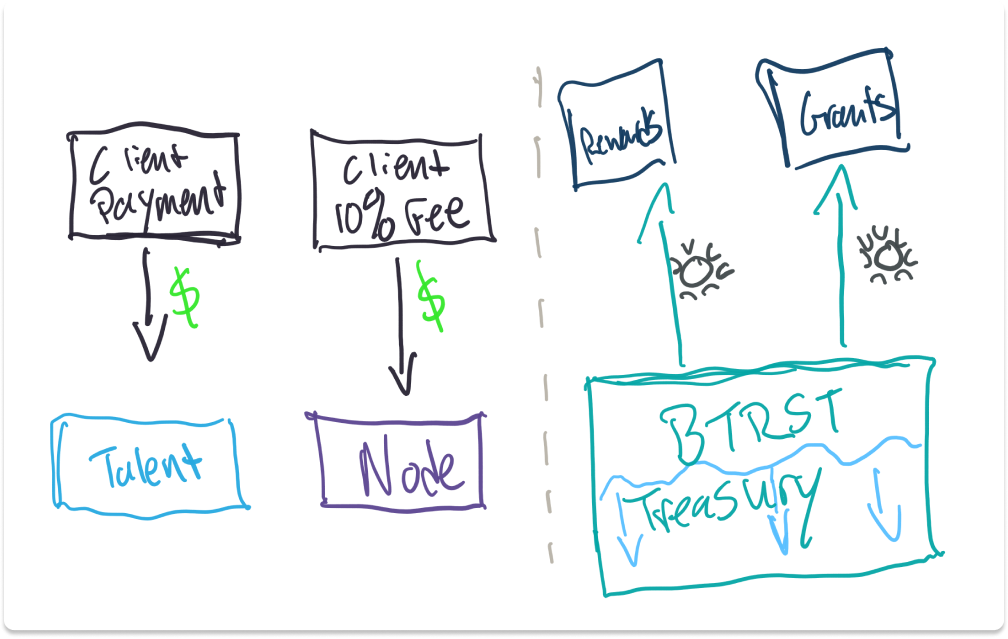

This illustration from the whitepaper does a good job of laying out how the core marketplace dynamics work end-to-end, smoothed by BTRST tokens (anywhere you see the logo on the graphic):

Anywhere there’s a “$” sign, that’s the Client and Talent interacting just like they would on a traditional marketplace, exchanging work for cash.

Anywhere there’s a Braintrust logo is where the magic happens:

That’s where Talent is getting a little extra compared to what they normally would – the negative take rate – for getting approved or earning a five-star review.

That’s where Connectors get rewarded for bringing supply and demand into the network – customer acquisition costs kill marketplaces; Brainstrust doesn’t pay acquisition costs, just tokens.

That last point is important and nuanced. Braintrust doesn’t pay customer acquisition costs in cash, but it does pay them in tokens. That increases circulating supply. As long as Connectors are willing to accept BTRST tokens for their referrals, the system works; but increase circulating supply too much, too fast, the tokens become worthless, and Connectors stop connecting. It’s a delicate balance.

There is no free lunch here. Things that are good for the network inflate the circulating supply, which may be bad for token holders. If you’re a token holder who operates in the network, that’s fine: you’re OK with dilution if it means a lower take on your economic activity. If you’re a purely financial investor, that’s not as great. The float of tokens is going to double in the coming years, not to mention the investor lockups that are going to roll off. But there is a 250 million token cap that Braintrust can never exceed. A financial investor needs to take a very long-term view to believe that when the dust settles, keeping take rates low using token inflation will lead to a more valuable network long-term.

That seems like a bug, but it’s a feature: Braintrust should get the owners it deserves. As more of the Community tokens are issued, there will come a point when the network is majority user-owned; until then, it’s owned by users and contributors, in addition to investors who need to buy into the very long-term vision.

I want to call this out: this is a key reason Braintrust can charge such a low cash take rate and sustain. It’s filling in the gaps with tokens that it’s planned to issue all along. Token holders likely expect those tokens to be directly financially valuable over time, but in the interim, they’re indirectly financially valuable to network participants, in three ways:

Governance. This is the most important. Governance has financial value here because it might mean the difference between paying higher fees or not, or even keeping the network alive or not. At some point, if the token value drops and the network is more reliant on fees, participants may decide it’s actually in their best interest to pay higher (but still minimally extractive) fees in order to fund the network with cash.

Bid Staking. Clients and Talent can stake BTRST to stand out to the other party and prove that they’re serious; if an applicant no-shows an interview, for example, they lose their tokens. This is the web3 replacement for the advertising models that web2 marketplaces graduate to.

Career Benefits. This one is a little hand-wavey for now, but the Braintrust website hints at future benefits for token holders; these might be things like educational content, free software, or coaching.

Here’s another important callout that is very different from equities: tokens should be more valuable to network participants than they are to purely financial holders.

I’d never thought of it this way before, but that should be part of the definition of well-designed tokenomics. It’s so important that I’ll say it again:

Tokens should be more valuable to network participants than they are to purely financial holders.

Let’s do a quick example.

If you’re purely an investor, one BTRST token is worth $3.60 at the time of writing.

But if you’re Talent on Braintrust, and bid staking that token means that you’re 0.01% more likely to land a $72,000 job, it’s worth $3.60 + $7.20, or $10.80 to you.

These numbers are made up, and this doesn’t take into account whether you were likely to get another job if you didn’t get this one, but regardless of the numbers, I think the logic stands. And I think it’s one key way that a user-owned network can outperform a purely investor-owned one: by giving away something that’s more valuable to recipients than it is to anyone else.

PLUS, if the tokenomics are really well-designed they should probably incentivize purely financial holders to get involved in building out the network in some way. For example, I own BTRST tokens but I’m not looking for work or talent on the network, so I’m leaking value. Should I be referring Talent to the network, bid staking for them to help them build their reputation, and earning upside as they succeed?

Anyway, I’m thinking out loud and getting off track, but there’s this: those tokens must have been worth something to somebody apart from an ownership stake in the network, because until very recently, the token and network growth actually weren’t directly connected.

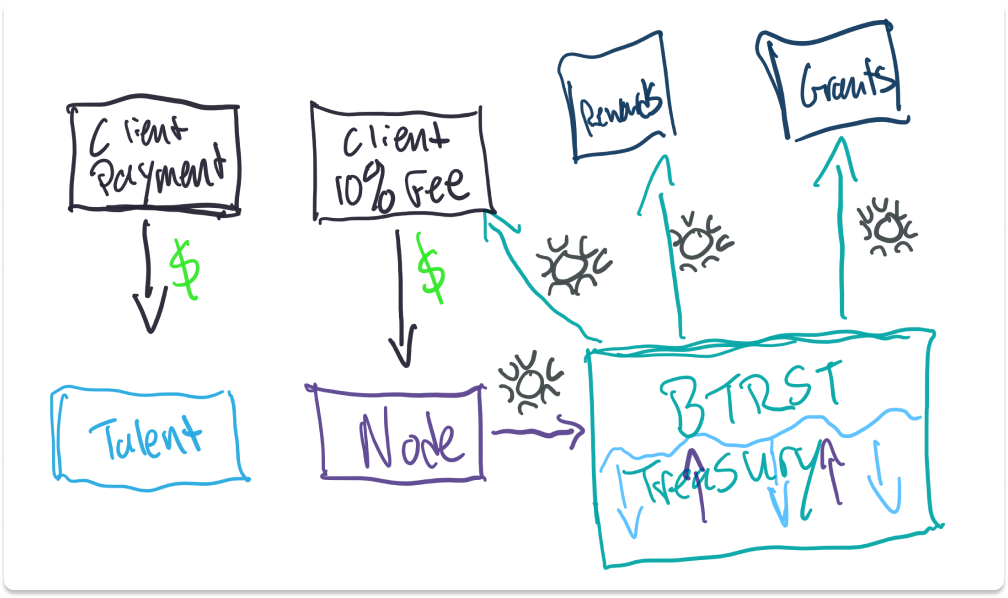

Value Accrual and the Protocol Upgrade

Remember how in the last section, I said that the Nodes received the 10% fees in cash for their contributions to the network? That meant that essentially, there was a huge leak.

Cash came in, cash went out, and Braintrust paid all community rewards and incentives out of its own treasury.

That was necessary. There was no token until last September, and the Nodes had real costs that they had to pay to do the work they were doing. But it wasn’t sustainable and it meant that value didn’t really accrue to the tokens.

In September, when Braintrust publicly launched its token, it decentralized and became a DAO. It put governance power in the hands of token holders. And one of the things that token holders decided to do first was to fix the leak.

In October, BTRST holders voted to approve a major change to Braintrust’s tokenomics. Specifically, instead of fees going to the Nodes as cash, “all fees on the network, including the current client success fee but also any other fees that may be initiated in the future, must be paid in BTRST.”

Clients won’t have to pay the 10% fee in BTRST. When they do pay fees, Nodes will convert them to a stablecoin, USDC, and send them into a Fee Converter smart contract which will buy BTRST tokens directly from an exchange and send them into the treasury to pay rewards.

Instead of ceaselessly depleting the treasury, this protocol upgrade will replenish it every time an invoice is paid, making the network more self-sustaining. Nodes will still be paid out of the 10% fee, but they won’t earn the full thing; their early hard work has been paid for, and their future work will be rewarded with BTRST tokens like everyone else.

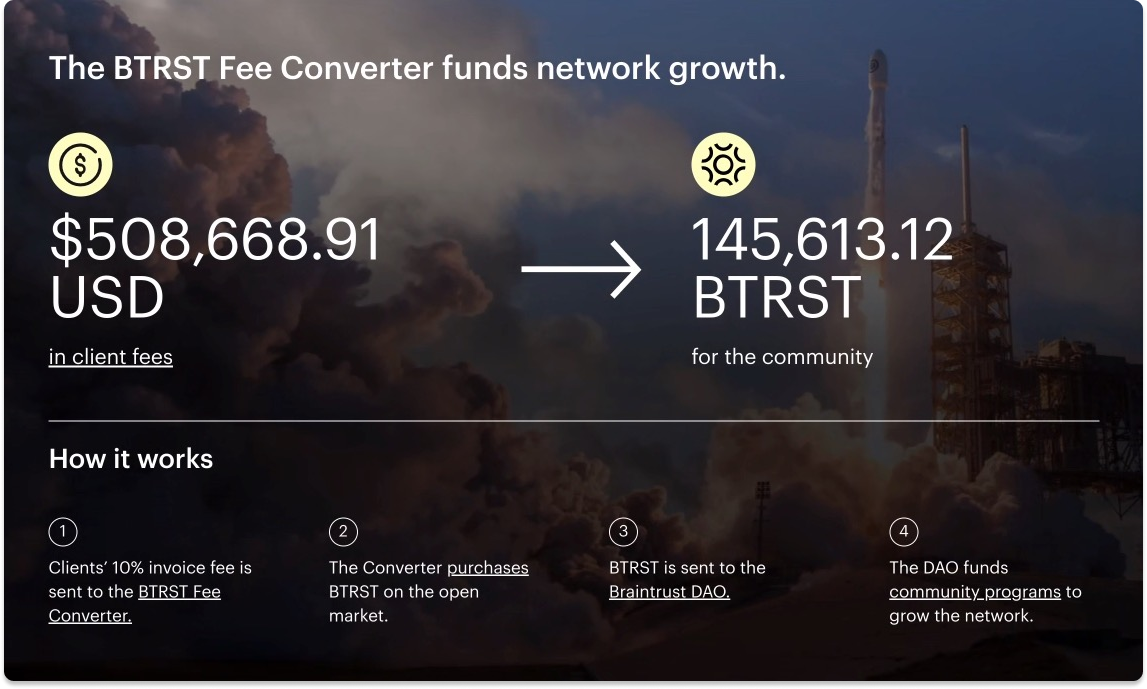

This hasn’t been fully rolled out yet – it’s still in testing until early February – but already, $508k in fees have been used to purchase 145,613 BTRST tokens on the open market.

Even wilder, you can see all of it as it happens, client by client and job by job, because someone in the community built a feed. Imagine a Web2 talent platform publishing its client lists and exact payment amounts, like this…

To me, that fee viewer is the most visceral representation of the fact that this really is a different kind of marketplace. You can go through and search by Client to see how much they paid, when, and for what jobs. Adam tells me that there’s a Twitter bot coming that will tweet things like “Nike just paid an invoice for $1,000, bought 300 BTRST tokens, going to the DAO.” Wild.

The long and short of it is that now, there’s a direct link between the token price and network volume. More volume creates more demand for the token. As the network grows, there will be more fees to buy more tokens from the open market.

Importantly, this doesn’t rely on profits, just fees. Network participants, who also own the tokens, are rewarded in tokens that should get more valuable with more fee volume. Braintrust doesn’t rely on any ponzinomics. It takes in exogenous capital from some of the deepest-pocketed clients in the world, uses those fees to buy back BTRST tokens, and uses those tokens to incentivize behavior that grows the network, bringing in more fees, and kicking it back off.

If the need to issue tokens as rewards outstrips token buybacks, Braintrust will still pay out of the treasury, but if they’ve designed the system right, that means they’re only increasing the circulating supply when participants are doing what the network wants them to do even beyond what client fees can afford to pay down.

It’s like if Uber took its ~30% take rate to automatically buyback UBER shares and then used those shares, plus a pot they’d set aside, to give to people who bring in new riders and drivers. That sounds a lot more sustainable, attractive, and loyalty-inducing than the status quo.

And it’s another reason that a user-owned network can win.

The Braintrust Thesis & How User-Owned Networks Win

Braintrust’s thesis is simple: the least extractive networks will win, and user-owned networks are more likely to be less extractive.

To be clear, this doesn’t mean that web3 marketplaces are guaranteed to win – they still need to provide a great product and do all of the hard things it takes to run a marketplace – or that all web2 marketplaces will be overtaken by web3 competitors any time soon.

On Means of Creation with Li Jin and Nathan Baschez, Adam explained his view on which incumbents web3 marketplaces would topple first. Marketplaces exist on a spectrum from minimally extractive to maximally extractive, with extraction measured as the delta between the take rate the marketplace charges and the unique value it adds.

Adam thinks that the most extractive companies, like DoorDash, which both essentially stole tips from drivers, and as covered here before by Dan Teran, hurts restaurants’ margins, are going to be the first to go. I think there are a couple missing dimensions here, something like product complexity and average order value, that explains why we haven’t seen decentralized Ubers or DoorDashes quite yet, but that the point is valid.

On the other hand, he thinks it’s going to be a very long time before a web3 competitor successfully competes with Airbnb because of how much value Airbnb brings both sides of the marketplace and the reasonable fees it charges (despite all of the hidden fee memes). He actually thinks platforms like Facebook and Twitter aren’t good targets for web3 because they don’t charge anything.

It’s interesting to note that Airbnb, Adam’s least extractive, is the most valuable of the newer web2 marketplaces by market cap, the only one without a formidable direct competitor (although hotels formidable competitors in aggregate), and the one that many people argue has the strongest network effects of any web3 marketplace.

Braintrust is making the same foundational bet that Airbnb seems to be – that the least extractive networks can consolidate the space in which they operate and become the most valuable long-term – and guaranteeing it in code.

That bet doesn’t necessarily mean that tokens need to be involved. Brian Chesky was able to keep Airbnb’s take rate low and support Hosts off the company’s balance sheet during the dark days of early COVID. Jeff Bezos lost money for years to keep margins low. Having leadership and owners who understand what Gurley, Chesky, and Bezos do, that low rakes are often the right long-term strategy, can create long-term defensible outcomes, with or without a token.

But user-ownership make it easier for any network to behave as if Jeff Bezos were running the show, even when no one is:

Who’s more customer-obsessed than the customers themselves?

So back to our original question: can a user-owned network both create and capture more value than its investor-owned counterparts?

First, the value creation side.

According to Gurley, Bezos, and Chesky, the marketplaces that can stay the least extractive for the longest amount of time can consolidate the financial activity in their space and create the most value long-term.

Because Braintrust relies on a protocol for things that humans might do in a normal marketplace, and because it can pay for work that other marketplaces would need to use cash for with tokens, it can keep fees lower (but will need to make it up by giving away ownership). Giving away ownership might actually create more long-term value, because those owners benefit from lower take rates, often more than they’re incentivized by a higher token price, they’ll likely vote to keep take rates lower, longer.

That should mean more growth, which will mean more fees in aggregate, and more fees can pay for more improvements, and potentially even lower fees on Clients, which will help Braintrust capture more of the market.

Matching Talent with Clients, and taking as little of the transaction as possible, creates real economic value. Making it easier and more financially attractive to bothe find and hire flexible work should expand the freelance market and make it easier for people to do exactly the jobs they want, when they want, and for companies to hire for the work they need, when they need.

I think the answer to the value creation question, as long as Braintrust’s current trends persist, is a yes.

But at some point, every marketplace wants to turn from attract to extract. Even Amazon. Amazon’s third-party seller marketplace is a bit of a mess and its huge advertising business, while one of the most underrated business stories in the world, makes it harder to find the actual best thing for you.

In other words, the point of consolidating the market is that at some point, even if it’s very far in the future, it should make it easier to capture the value you’ve spent years creating. If your business is valued on the present value of future cash flows, you need to show investors that there are enormous cash flows sitting out there in the future that you’re buying with a low take rate today.

But what if you’re not valued in the same way?

This is where Braintrust’s tokenomics come in, and why I think that Braintrust token holders will be able to capture the value the network creates.

Equity prices are based on the present value of future cash flows because that’s what they confer rights to, ultimately. You can’t use Airbnb shares to get free stays or pay a lower fee as a host. You use Airbnb shares to own a percentage of the business, and to vote.

But BTRST tokens offer both ownership and utility. And for network participants, that utility has real, measurable financial value.

So what’s that ownership and utility worth?

This is why it’s important to consolidate as much economic activity as possible on the network. Let’s do a quick reductio ad absurdum: what if Braintrust eats the whole talent market?

According to HBR, the size of the US staffing and recruiting industry was $151 billion in 2019. The three largest agencies globally by revenue do a combined $70 billion in annual revenue, roughly one-third of which originated in the US. So let’s triple that $151 billion and assume, for our sake, that the global staffing and recruiting industry is about $450 billion. Then there are the consulting firms like Tata Consulting Services (TCS), Deloitte, PWC, and the likes. Deloitte did $50.1 billion in 2021 revenue, TCS did $22 billion.

Let’s round the whole thing up to $1 trillion between recruiting/staffing and consulting – it’s way short of the total available pie since we’re really talking about all knowledge worker wages globally – but for our math here, it works.

Braintrust charges companies 10% of whatever they pay people they hire from the platform. So theoretically, if Braintrust could build a machine that consolidated the global flexible talent market over time, its opportunity would be $100 billion in fees per year. That’s a big TAM, and it’s one that Braintrust believes will grow as it becomes easier for people to find flexible opportunities. It cites a $5.3 trillion annual spend in tech alone.

Either way, at $100 billion in fees, that would create $100 billion in demand for 250 million total Braintrust tokens from fees alone, plus the demand from all of those network participants who would be able to gain real financial benefit from using those tokens to stand out in such an active marketplace. And then there’s the governance: how valuable would it be to govern a network that pulls in $100 billion in fees per year and controls the global flexible talent marketplace?

All to say, that is an absurd scenario and a very long way away in the most optimistic case, but there are many ways for the token to capture the value the network creates without raising the take rate.

But for now, we’re still talking about an 18-month-old market that’s done $37 million in total Gross Service Volume and only serves a small segment: engineers, designers, and product people looking for flexible work at large companies. A lot will need to happen for any of this theoretical stuff to even matter.

To that end, in the coming months, expect to see projects emerge from the community that aim to move upmarket and downmarket to eat more of the whole flexible talent pie.

Upmarket, one recent IT Consulting exile is working on a proposal for a Node – essentially a new startup built on the Braintrust protocol, funded by grants – to go after the giants like Deloitte, PWC, and Accenture. By warehousing talent and charging hidden markups, these consulting firms can often pull in 70% take rates.

Downmarket, expect to see similar proposals that go after lower-contract-value talent marketplaces like Fiverr and Upwork.

At a certain size, it might also make sense to offer services and resources that the newly freelance Talent population might need, like group health insurance or 401ks. That’s an opportunity to increase economic activity while driving clear value to the network.

In either case, new Nodes will benefit from the infrastructure, community, and resources that the Braintrust network has built up over the past four years. They won’t need to raise money to fund tokenomics, protocol design, and smart contract audits, because those will have been done. They’ll tap into an existing pool of Connectors and Vetters. They won’t need to raise venture capital because they’ll be able to get grants from the treasury.

There will be challenges, too.

Like the time when Braintrust’s token launched on Coinbase and traded up to above $40, and armies of bots “watched” the short videos in the Braintrust Academy library in order to pick up the BTRST tokens Braintrust offered to incentivize people to learn more about the network. When incentives are baked into everything and backed with a token, you need to be particularly careful about how you design your incentives.

Or the fact that a bigger, more dispersed community makes governance challenging. It’s challenging enough already. When I asked Adam what he’d most disagreed with the community on, he replied quickly:

“Oh, so many things. I think that some of the proposals are just ineffective. But this isn’t mine anymore. We gave up control in September.”

That’s the beauty of this. Good or bad, it’s up to the users who own the network to govern the network. My bet is that they keep fees lower, longer than public market investors would and build a truly enormous talent business, but strap yourselves in, it’s going to be a bumpy ride.

Thanks to Dan for editing, and for Adam and the Braintrust community for working with me!

How did you like this week’s Not Boring? Your feedback helps me make this great.

Loved | Great | Good | Meh | Bad

Thanks for reading and see you on Monday,

Packy

Great article, a couple thoughts:

1. VCs investing in crypto projects is IMO not a big deal because governance rights are so different in web2 versus web3 companies

2. Interesting take on which marketplaces can be disrupted because of take rate. My sense is these marketplaces are forced to charge more because of a weaker network effect. I think there's something worth exploring there - how much can different tokenomics improve these network effects? What can't be improved (e.g., a DoorDash order can only have so much variable margin given the cost of food, versus a home rental which has a much higher variable margin)?

Another excellent post Packy. A question central to this and all similar tokenized web3 enterprises seems like, how is the value of the tokens supported and enforced? If we compare to U.S. Dollar or other major fiat currency-based businesses, the core support holding up the value of the token - the dollar say - is, ultimately, the financial weight and if it comes to it military might of the nation-state sat behind it. The development of fiat currencies in the last few centuries has gone hand in hand with the development of the (oppressive, militaristic etc) nation state. Ten years from now, what force or forces supports and/or enforces the value of the myriad tokens created in web3 businesses? Asking for a friend.