Welcome to the 898 newly Not Boring people who have joined us since last Thursday! If you aren’t subscribed, join 33,771 smart, curious folks by subscribing here:

Hi friends 👋 ,

Happy Thursday! Today, we’re doing a Sponsored Deep Dive on a company that I’ve been waiting for all my investing life without knowing it: AltoIRA.

Instead of me reading the essay, we’re going to hear the Alto story straight from the mouth of its founder and CEO, Eric Satz. Listen by hitting play above, or on Spotify or Apple Podcasts.

NBD but Sponsored Deep Dives are kinda famous now, after Ben Thompson said on his Dithering podcast yesterday:

There’s another guy that has a newsletter, the name escapes me [ed note: it me], and he will write about the startups and he’s actually paid by the startups to do a big profile of them, and they give him access to what their business is doing and their plans and things like that. But he’s very upfront about it, he’s clear that he’s getting paid to do it. And I think that’s fine, as long as he’s super transparent about the fact that money’s changing hands here, but in exchange, he does get lots of interesting information in the way the company thinks about the business and their opportunity that I don’t get because I’m just someone sitting on the outside relying on earnings calls.

That’s a highlight of my professional life, despite my name escaping him. Ben Thompson is, of course, one of my business analysis idols, and the quote shows why. He captured exactly what I’m going for with these Sponsored Deep Dives: the win-win-win.

I get to write about companies that fascinate me with more access than I’d get as a full outsider or even a journalist, and make money so I can keep doing this.

The sponsor gets an outside perspective on their business, and the chance to share their story with the smartest group of people on the internet.

You get a behind-the scenes look at startups that are shaking things up, and a new product that can be useful (and typically help you make money).

If you want to learn more about the process behind the deep dives: read here. I will always tell you how I’m getting paid - CPM or CPA; today is a combination of the two.

Today’s sponsor, Alto, is one of those “I can’t believe they’re actually paying me to write this” companies, because not only am I personally fascinated by the space they play in, I also got smarter about my retirement savings in this research process than in the entire rest of my life combined. Plus, Alto’s CRO Tara Fung is an actual, long-time Not Boring reader! IRAs aren’t as boring as I thought.

Let’s get to it.

AltoIRA: The World’s Least Boring IRA

IRAs, But Not Boring

Let me get a confession out of the way upfront: for most of my adult life, I thought that retirement accounts were so boring.

Individual Retirement Accounts (IRAs), 401ks, pensions… I knew I had to max my contribution every year, and it hurt, because I assumed that the only option was to have the money sit in a mutual fund and earn average returns. I have friends (and a wife) who get real joy from figuring out whether a traditional IRA makes more sense for them than a Roth, but honestly, I zoned out whenever those conversations started. My apologies to 59-and-a-half year old Packy.

But in November, my friend Nikhil tweeted a screenshot memo about his investment in AltoIRA, and I took note.

AltoIRA is a self-directed IRA for alternative investments. Instead of blindly putting money into index funds and letting it sit there until you retire (or, uhhh, die), AltoIRA lets you invest your retirement savings in startups, art, crypto, real estate, and more, as easily as you’d expect from a modern technology company. It gives regular investors access to the type of diversification that the pros use to construct their portfolios, with the compounding benefits of deferred taxation.

It’s a product I didn’t even know was possible, but have been waiting for all my life.

Alternative asset investment startups like Masterworks, Fundrise, Pipe, Rally Rd., AngelList, and Republic are among my favorite subjects to write about. The fact that regulation and technology are working hand-in-hand to let anyone build the types of portfolios wealthier, more sophisticated investors long have is an incredible thing.

AltoIRA gives people access to a meta-trick the ultra-wealthy use: investing in alternatives from your retirement account, with the same tax advantages as the passive IRA you’re used to. Accredited investors can even invest in Not Boring Syndicate deals in their IRA, through a direct partnership between Alto and AngelList.

If you think I’m going to keep my entire IRA generating average returns in Wealthfront when AltoIRA exists, you haven’t been reading Not Boring very closely. I’m in the middle of transferring 20% of my IRA into Alto as we speak. Today, I’ll tell you why:

Retirement Accounts, Taxes, and Alternative Assets. I’ll try to convince you that I was wrong, and retirement accounts actually aren’t boring, particularly with alternatives.

Meet AltoIRA. What is AltoIRA and how does it work?

Why Now? The intersection of regulatory, market, and technological trends make now the ideal moment in time to build what Alto is building.

Alto Everywhere. Soon, investing with your IRA will be as easy as investing with your bank account.

If you can’t wait to get started, you can sign up for AltoIRA using the special Not Boring link here:

But we’re here to learn, too, about why the combination of IRAs and alternative investments is so powerful. So put on your party pants and come explore the world of retirement accounts with me.

Retirement Accounts, Taxes, and Alternative Assets

Let’s start with why I was wrong not to care about optimizing my retirement accounts: there is so much money in retirement accounts, and the benefits of doing it right over time are massive.

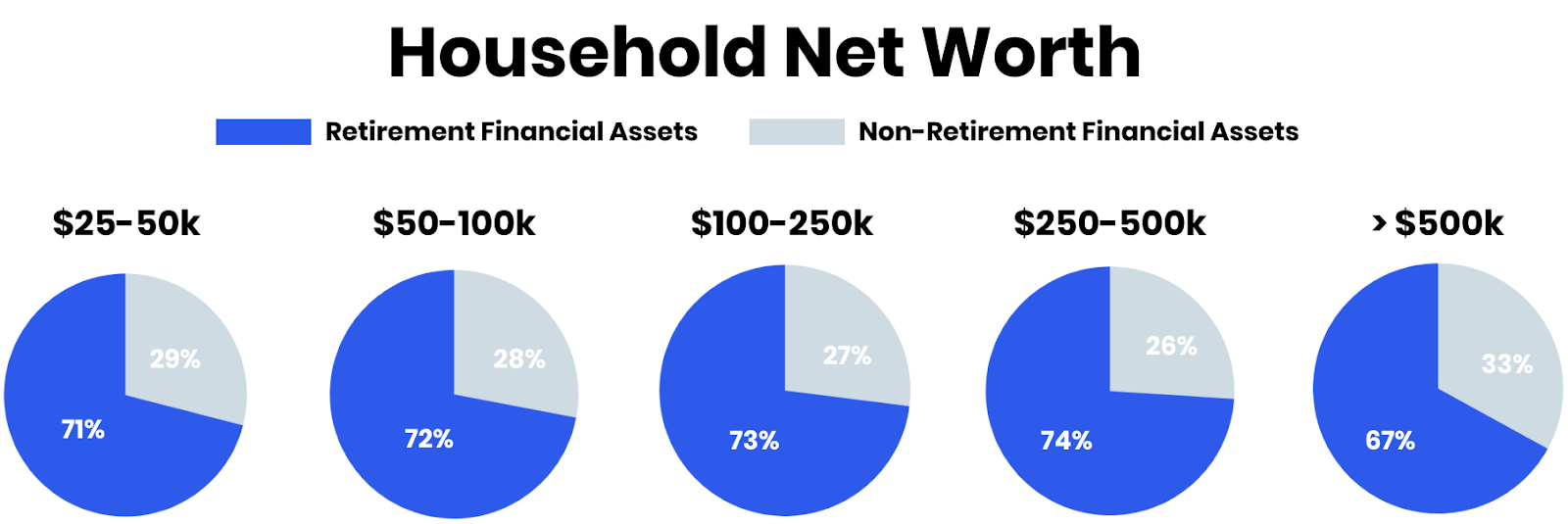

In the United States, there are 150 million retirement accounts that hold over $33 trillion in assets. Excluding home equity, retirement accounts comprise 70% of the average American household’s investable assets.

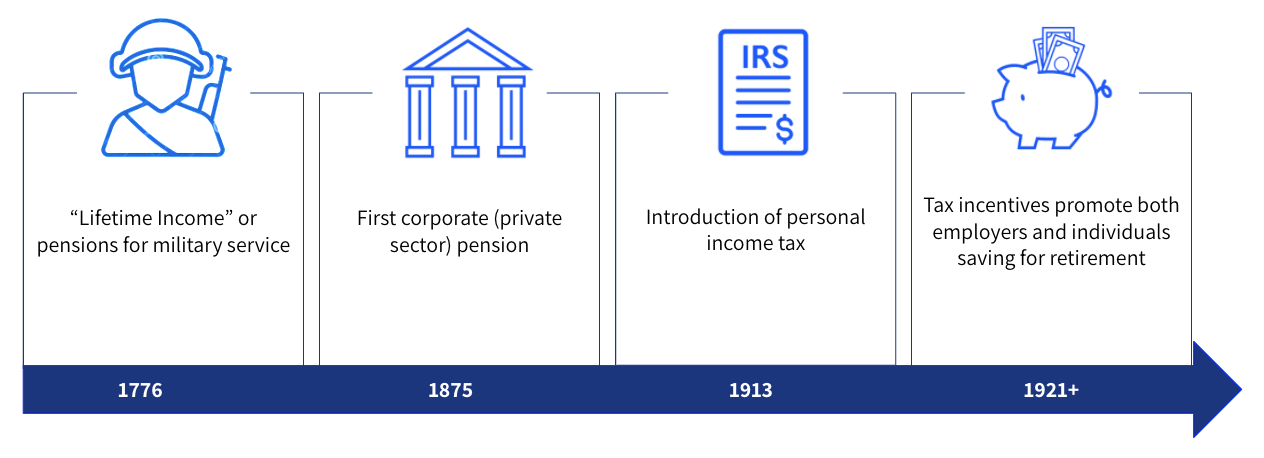

This is by (very old) design. In the US, pensions started as early as the country, with lifetime incomes for military service, but the structure we have in place today largely comes from 1913. That year, the states ratified the 16th Amendment, giving the Federal government the right to impose a federal income tax. At first, pensions were taxable, but the Revenue Act of 1921 exempted retirement accounts from a person’s taxable income.

Since then, the system has evolved, but the purpose (shield retirement revenue from taxes) remains the same. Today, there are five main types of retirement accounts:

IRAs: Account that individuals can use to save for retirement with tax advantages. There are two main types -- Traditional IRA and Roth IRA -- as well as others like SEP IRA and SIMPLE IRA. Traditional IRAs are funded with pre-tax dollars and grow tax-deferred, while Roth IRAs are funded with post-tax dollars and withdrawals are tax-free.

401(k)s: Also known as “defined contribution,” accounts that companies offer to employees. Employees can fund accounts pre-tax through automatic payroll withholding, and companies often match up to a certain % of employee contributions. Like IRAs, there are Traditional and Roth, with the same funding and tax implications.

Public Pensions: Also known as “defined benefit” because they guarantee a set payment in the retirement for the rest of the beneficiary’s life. These are government-funded.

Private Pensions: Like public pensions, but company funded.

Annuity Reserves: Mainly issued by insurance companies, annuities let someone pay in while they’re working in exchange for defined payouts after they retire.

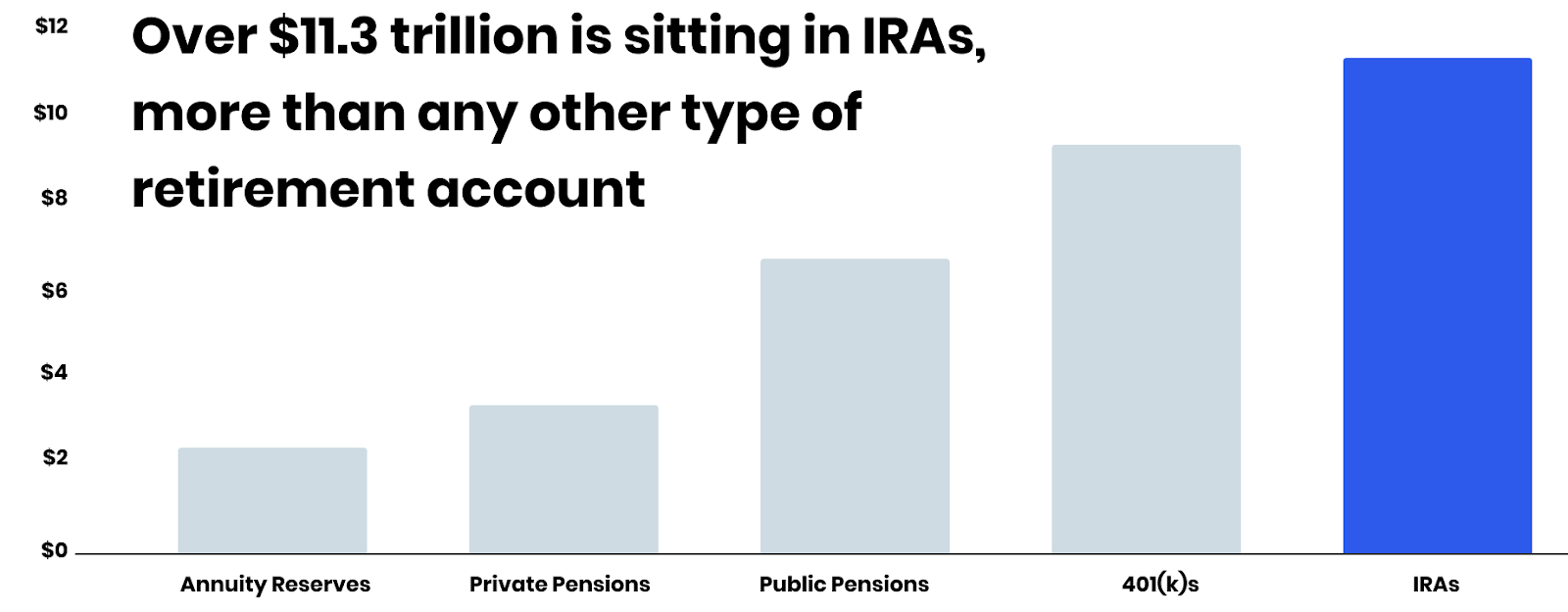

For the rest of this piece, we’ll focus on IRAs: they’re the largest category, with $11.3 trillion in assets, and expected to be the fastest-growing as people switch jobs more frequently and pursue employment in the gig and passion economies, and as baby boomers retire.

Why do people keep such an enormous percentage of their investable assets in IRAs? Taxes.

People hate paying taxes, and will do anything to avoid them, even if it means keeping money tucked away until retirement. For tax-inefficient investments (i.e. not opportunity zone real estate investments or muni bonds) or potentially high-return investments, like venture and crypto, an IRA lets you grow your investments tax-deferred, and may avoid capital gains altogether.

Historically, though, individuals have done what I’ve done: set it, forget it, and let Fidelity or Vanguard or Voya or Wealthfront or whoever invest in public market equities and bonds via mutual funds and ETFs. As a result, a huge percentage of retirement funds are controlled by a tiny number of balance sheets.

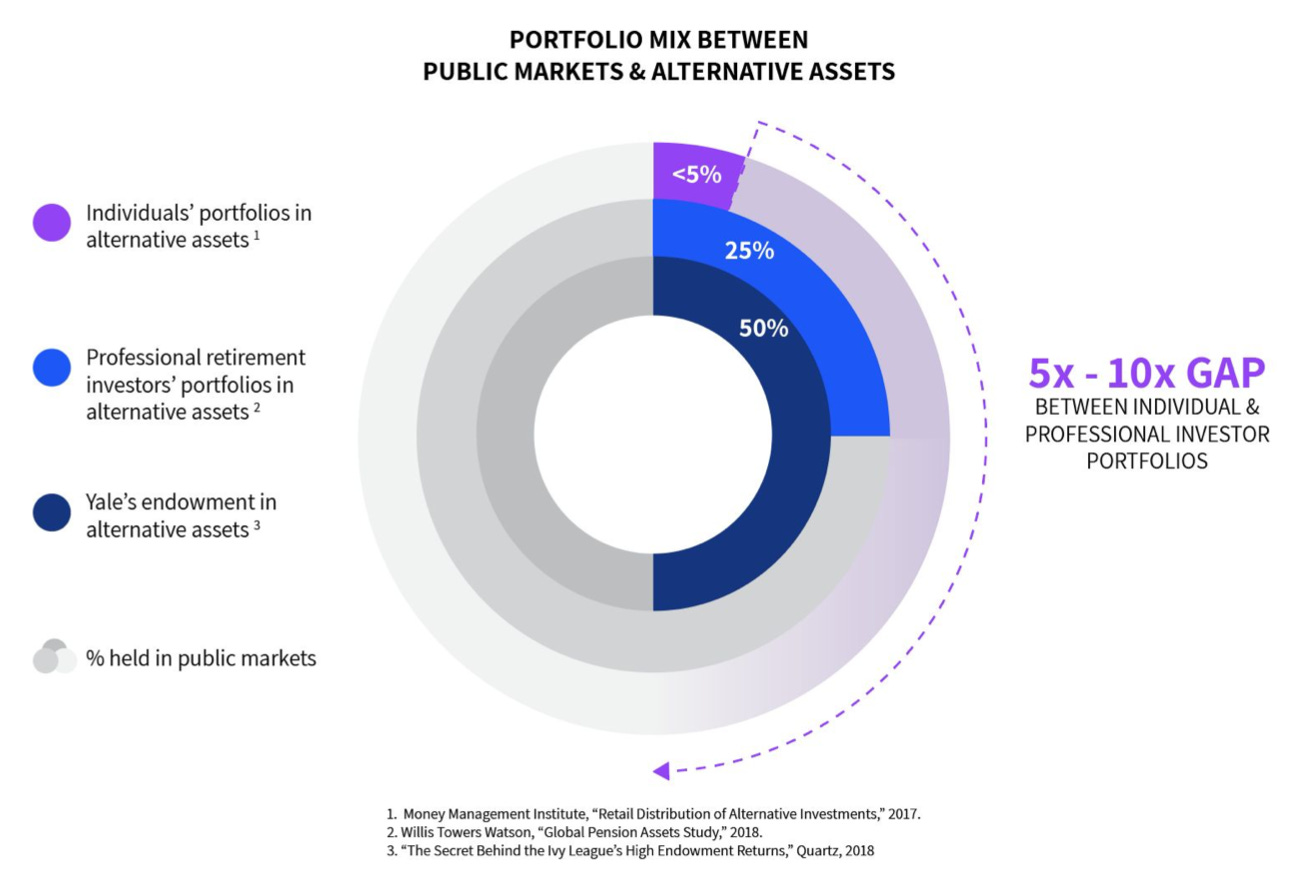

Only 2-5% of individuals’ retirement portfolios are in alternative assets like real estate, startups, crypto, credit, and art. That seems OK, until you realize that it’s not at all how the pros do it.

Professional retirement investors put an average of 25% of their portfolios in alternative assets, and the Yale Endowment, which is famous for pioneering the Endowment Model of portfolio management, puts up to half of its portfolio into alternatives.

The idea that professionals invest more aggressively into alternatives than individuals should be familiar if you’ve been reading Not Boring for a while, as should the reason they do it.

In Fundrise & The Magic of Diversification, I boiled Bridgewater founder Ray Dalio’s seminal paper, Engineering Targeted Risks and Returns, down to the following sentence:

Allocating money across a diversified portfolio has historically generated better risk-adjusted returns than concentrating in just stocks, bonds, or even the traditional 60/40 split.

I cited that idea in my piece on art investing platform Masterworks, too, to explain why allocating a portion of your portfolio to art, which has historically had an incredibly low correlation to equities, is a smart way to boost risk-adjusted returns.

Diversification is central to understanding the magic of alternative investments generally; taxes are central to understanding why non-taxable funds with long time horizons, like retirement plans and endowments, get better returns from alternative investments than taxable funds.

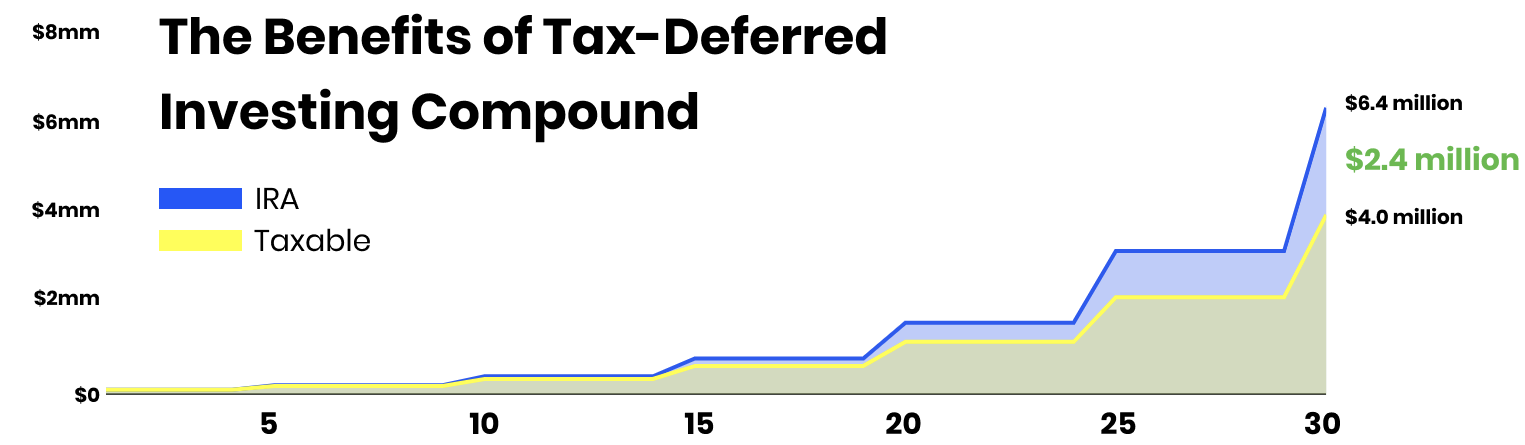

To understand why, let’s look at two $100k portfolios, one taxable and one tax-deferred, that invests in alternative assets over 30 years and make a new investment that doubles every five years, assuming a long-term capital gains tax of 15%.

For the first decade, after the first two liquidity events -- think a portfolio of startup investments, most of which fail and one of which returns 2x the portfolio every five years -- things look pretty even. But at each turn, a 15% capital gains tax is getting removed from the investable amount in the taxable portfolio, whereas the IRA portfolio can keep doubling its money. After 30 years, with the exact same investments, the IRA is worth $2.4 million, or 60%, more than the taxable portfolio!

It’s not just pension funds and endowments that understand and leverage this financial alchemy. Smart individual investors do, too. PayPal co-founder and Affirm founder Max Levchin made an early investment in Yelp through his Roth IRA that netted him nearly $100 million in tax-free gains (assuming he doesn’t cash out until he’s 60). Peter Thiel made a portion of his early Facebook investment through his Roth, potentially generating almost $1 billion in tax-free gains.

Levchin and Thiel are two of a handful of people in the country that use self-directed IRAs to shield gains from taxes. In 2014, the Government Accountability Office (“GAO” or “narcs”) wrote a report called Individual Retirement Accounts: IRS Could Bolster Enforcement on Multimillion Dollar Accounts, but More Direction is Needed From Congress. Catchy.

In the report, the GAO highlighted a small number of people with IRA balances over $5 million dollars and argued that the government was losing out on millions of dollars in tax revenue because these people were able to accumulate larger IRAs than the government anticipated. How were they doing it? Using their IRAs to invest in early-stage, private tech companies at low valuations and avoiding or deferring capital gains taxes on successful investments.

At the time of the report, there were only 9,137 people in the entire country with IRA balances over $5 million. There’s nothing legally holding regular investors back from using Self-Directed IRAs like the ultra-wealthy, but to date, they’ve been largely underused. Of the $33 trillion in retirement assets, only about $50 billion, or 0.15%, are self-directed, for three main reasons:

Inaccessible. Vanguard, Fidelity, Schwab and the other retirement giants don’t allow self-directed alternative investments; you need to open a Self-Directed IRA with a specialized custodian.

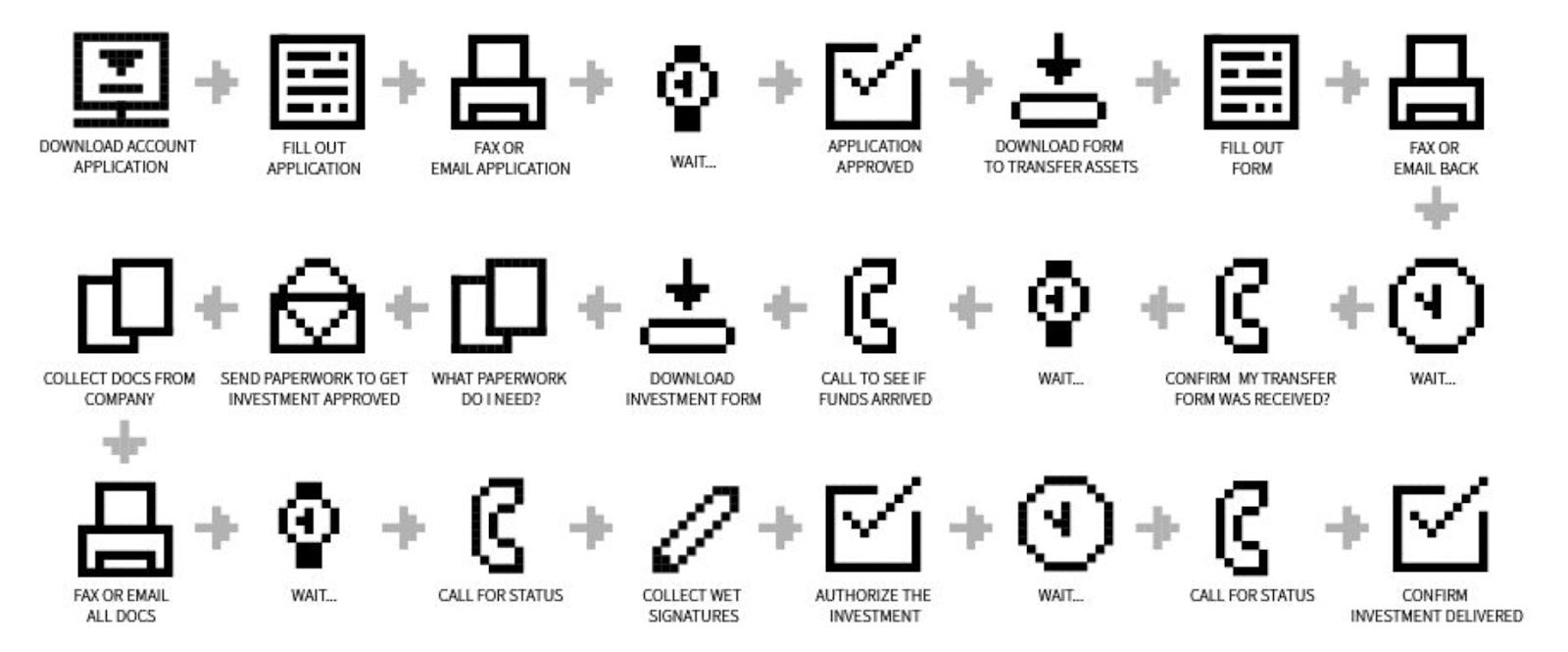

Complex and Painful. Have you ever tried doing something as simple as moving your retirement account from one provider to another? It’s slow, manual, and confusing. Now multiply that by 1,000 and you’ll get a sense for what trying to invest through an incumbent Self-Directed IRA custodian is like.

Expensive. Self-Directed IRAs are built on very outdated systems, have high cost structures, and pass those costs onto customers, making investing out of them prohibitively expensive unless you’re writing very large checks.

AltoIRA is fixing that, and making the same strategies used by the 0.03% available to everyone. It wants to shift the balance of retirement investing from a tiny number of gigantic balance sheets to a gigantic number of tiny balance sheets.

Meet AltoIRA

AltoIRA came about, as many startups do, from personal frustration. When Eric Satz, a serial entrepreneur and investor, tried to make an investment through an old school Self Directed IRA custodian and spent eight weeks going back and forth on documents, with fees that changed the deeper he went. This is what Eric’s experience, and most Self-Directed IRA experiences, looked like:

Eric hates inefficiency and the bullshit pricing that comes with it, so he set out to build a product that made the process as easy as it should be in this millennium.

The result is AltoIRA, the easiest way to invest in alternative assets with your IRA and generate tax-advantaged returns. It uses software to eliminate the complexity and high costs of traditional self-directed custodians, and makes it easy to open, fund, and invest out of your account, seamlessly, online. When AltoIRA is successful, it will be as easy to invest out of your IRA as it is to invest out of your bank account.

I opened my own AltoIRA account last week, and it took three minutes. The only painful part was figuring out my account number on my ADP/Voya 401K account in order to initiate the transfer (turns out, it was my social security number, which I found out after clicking around the website for 45 minutes and waiting on hold for another 20).

If you want to start fresh instead of transferring an existing account, you can directly contribute up to $6k per year in a couple of clicks.

Once your account is funded, you can use AltoIRA to invest in a wide range of alternative assets, from startups (via partnerships and direct integrations with AngelList, Republic, and WeFunder) to art (via Masterworks) to farmland (via FarmTogether) to growth stage private companies (via EquityZen) to real estate (via Diversyfund) and more. If Alto doesn’t have a partnership set up with a particular platform, you can ask them to set one up, or invest one-off in off-platform deals (ie., deals you find and bring on your own), like buying an investment property or investing in a startup that’s not offering shares through an online platform.

One of the things I like most about Alto is that since 70% of peoples’ investable assets are tied up in retirement accounts, even people who have a lot saved up might not have the cash on hand to invest in alternatives. Alto eliminates the trade-off between maxing out your retirement savings and investing in assets that might make your retirement a lot more comfortable.

To that end, Alto also offers a Crypto IRA, which lets you buy over 30 cryptocurrencies through your Self-Directed IRA, through an integration with the Coinbase exchange.

Plus, buying and selling crypto can be an absolute tax nightmare, because even using Bitcoin to buy Ethereum, or any coin to buy another, counts as a taxable sale. If you’re active, those add up, causing high costs and reporting headaches. By investing through an IRA, you can avoid those headaches. Alto makes money by charging 1% annually on the account balance to cover custody, insurance, and cold storage costs, and a 1.5% fee for each transaction.

Alto is able to deliver a Self Directed IRA product at a much lower cost than incumbents because it’s built from the ground up on new technology, including direct integrations with alternative investment platforms, which gives it a lower cost structure than incumbents. As a result, Alto doesn’t charge based on the size of your account or investments; it charges an annual flat fee and flat per-investment fees. There are two account types (in addition to Crypto):

Pro. Bring your own deals, and invest through Alto’s platform partners, for $250 per year and $10-$75 per private investment.

Starter. If you just want to invest through Alto’s platform partners, like AngelList, Republic, and Masterworks, you can pay $100 annually and $10-$50 per investment.

Since I’ll mostly be using AltoIRA to invest in startups via the Not Boring Syndicate, I went with the Starter plan. If you want to take control of your IRA, diversify your investments, and generate tax-advantaged returns, try it out by setting up an AltoIRA account now:

Once you explore it, you’ll wonder why no one’s built this before.

Why Now?

One of the questions venture capitalists love asking the most is, “Why now?” What regulatory, market, or technological changes make it such that this idea couldn’t have worked in the past, but can now. It’s a question I asked Eric multiple times about Alto, because this seems like an idea that should have existed before; turns out, now is the right time across all three factors.

Regulatory. The government is making moves to democratize alternative investments. As I’ve written about before, Reg A+, passed as part of the 2012 JOBS Act, let companies raise up to $50 million per year from non-accredited investors. Reg D 506(c), also part of the JOBS Act, allows private placements of any size to be generally solicited. This is the regulation that lets people with Rolling Funds and traditional funds on AngelList talk about them publicly (👀). Reg CF, passed in 2015, let online platforms solicit just over $1 million in crowdfunded equity investments with less onerous requirements than Reg A+.

In 2020, the SEC raised the Reg A+ limit from $50 to $75 million and the Reg CF limit from $1 million to $5 million, and also took steps to broaden the definition of accredited investors. Instead of being solely based on income or wealth, an investor can become accredited based on professional history or by obtaining certifications. This means that more people will be able to invest more money than ever before in alternative assets, an obvious tailwind for Alto.

Market. As a result of Reg A+ and Reg CF, a wave of new alternative investment platforms have sprung up over the past few years, including companies we’ve covered here, like Masterworks for art, Fundrise for real estate, Republic for startup equity crowdfunding, Rally Rd. for collectibles, and more. These companies provide easily accessible central hubs for various types of alternative investments, which makes it relatively easy for Alto to form a small number of partnerships to access thousands of deals instead of handling each investment one-off.

Technology. Alto interfaces with partners through a series of APIs, both the partners’ and Alto’s. On the partner side, for example, Alto works with Coinbase’s exchange API to facilitate seamless crypto investing all on the Alto platform. Alto also builds its own APIs that partners can plug in to add “Invest with Alto” as a payment option at checkout, making investing from your IRA as easy as investing from your bank account, right within the flows through which you normally invest.

It no longer makes sense for individual investment portfolios to be limited to just public equities and bonds. I’ve written about it before and I’ll write it until I’m blue in the face; we are finally at a point at which regular people can invest like the ultra-wealthy have for decades, and I support anything that makes it easier for people to do so, responsibly. Given the tax benefits over time, this is doubly true for retirement accounts. That’s why I’m so bullish that now is AltoIRA’s time.

Alto Everywhere

Alto is just getting started. It spent the first eighteen months of its life heads-down, building, and getting things right (you don’t want to make mistakes in fintech). After letting in its first Alto IRA accounts in May 2018 and its first Crypto IRA accounts in early 2020, and growing steadily, Alto more than doubled funded accounts and tripled total assets under custody between September 2020 and today. Its time has come.

The crypto boom helped -- Alto is the easiest way to invest your IRA in crypto, and a bunch of smart people realized that right in time to catch Bitcoin’s run-up.

Despite the strong early growth, though, it is still comically early in Alto’s quest towards its ultimate vision: Alto everywhere. For the first three years, it was focused on building something better than a traditional self-directed IRA; now, it wants to make investing out of your IRA as easy as investing with your bank.

I asked Eric how he’ll know he’s achieved what he set out to, and he told me he’s looking for two things:

“Whoever the CEO of Southwest Airlines is calls me and says, ‘How do you treat your customers so well?’”

“BlackRock wakes up one day and says, ‘What the fuck just happened? How did we miss that?’”

Those two together represent what it’s going to take to get there -- treating customers absurdly well in an industry in which they’ve historically been treated with hostility (as I can attest from my experiences with Wealthfront and Voya/ADP) -- and what the world will look like when they do -- when the world’s largest investment managers realize how much the balance of power has shifted from their tiny number of massive balance sheets to our millions of tiny balance sheets.

When I asked Nikhil how big he thought Alto could get, he said:

I increasingly think about Alto as the enabling platform or layer for alternative investing. Like PayPal, it will enable you to pay in a bunch of places, but it’s also a consumer destination site. It can become the payment mechanism for investing in alternatives, and a macro bet on the rise and democratization of alternatives.

Today, you can invest from your IRA directly into twenty platforms, at the click of a button. One day, you’ll be able to invest from any retirement account into any alternative asset, seamlessly, from Alto or directly in your investing app of choice. Personally, I’m excited to see the “Invest with IRA” button pop up on all of the alternative investing platforms I love, and to bring a bunch of people in the Not Boring Syndicate on to the platform so that we can reap the tax advantages of investing in startups through our retirement accounts.

(True story: as I was writing this, Carlos Collantes, one of the Not Boring LPs, messaged me about an investment and said, unprompted, “Alto already has our funds on the way.” I asked him how he liked Alto, and he said, “The experience with Alto has been flawless. It is awesome that I can use the (for a long time) untouchable money in the 401k to shape the near future.” You can’t make this stuff up, folks.)

If you’re like me, you’ve read this far and you’re thinking, “Cool, I’m just going to move it all to Alto.” That’s probably not the move. I showed real restraint, and am doing 20% of my retirement account, which Eric said is in range with accepted wisdom on alternatives, and with what the average professional retirement investor does. Obviously, as with anything, before making investments, do your own research!

If you want to invest like the pros and self-direct some of your retirement account into alternatives, sign up for AltoIRA at the Not Boring landing page today:

Thanks for reading, and see you on Monday,

Packy

AltoIRA: Interview with CEO Eric Satz